Estimated Chinese Gold Reserves Surpass 20,000t

Koos Jansen

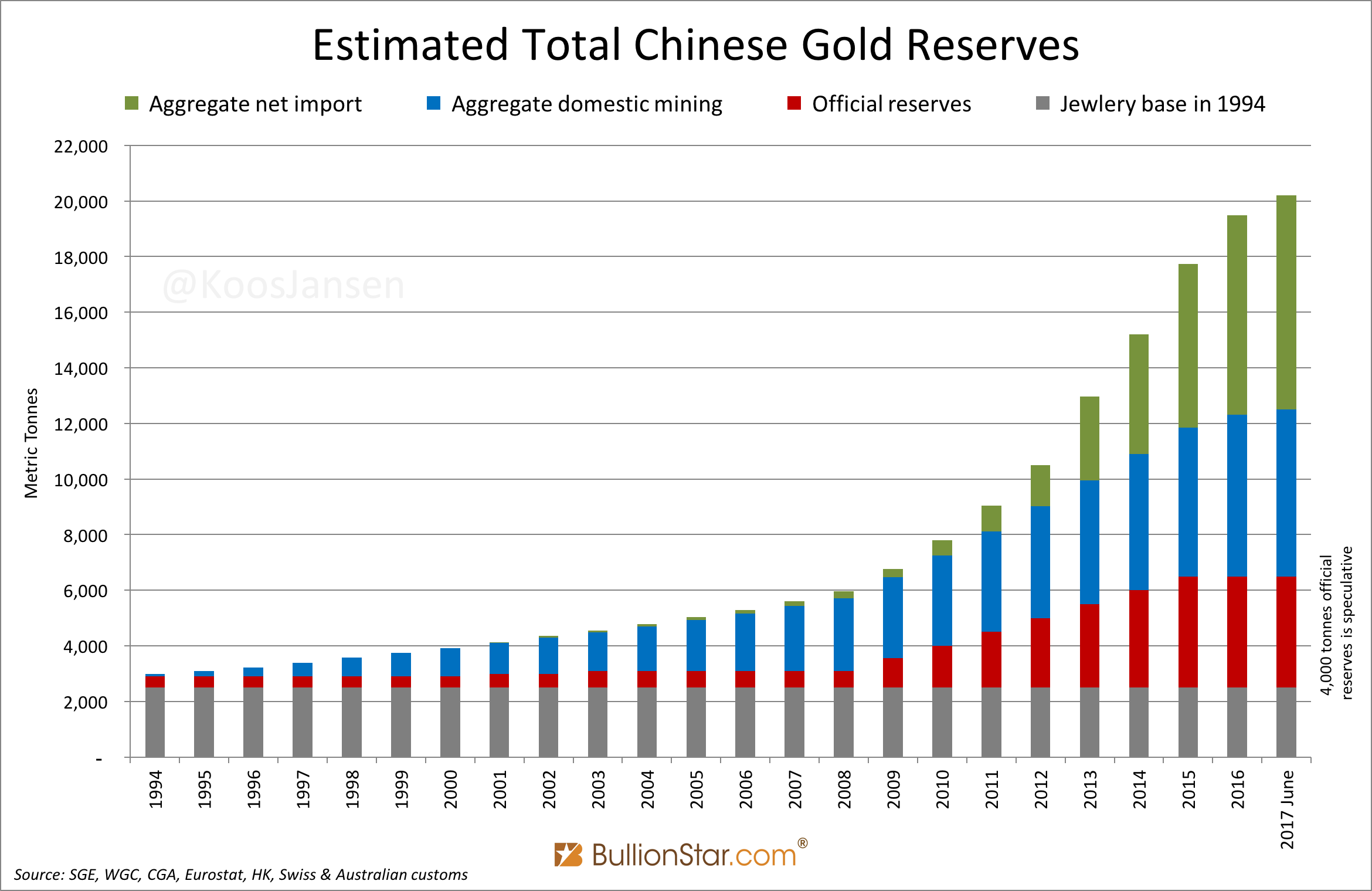

Koos JansenMy best estimate as of June 2017 with respect to total above ground gold reserves within the Chinese domestic market is 20,193 tonnes. The majority of these reserves are held by the citizenry, an estimated 16,193 tonnes; the residual 4,000 tonnes, which is a speculative yet conservative estimate, is held by the Chinese central bank the People’s Bank of China.

I’m aware I’ve been absent from writing about the Chinese gold market for a long time, so for some of you it can be burdensome to pick up where we left a few months ago. It is not feasible for me to explain the entire structure of the Chinese gold market again; my suggestion would be to follow the links provided in the text for more background info. Most knowledge is covered in previous BullionStar posts, Mechanics Of The Chinese Domestic Gold Market, Chinese Cross-Border Gold Trade Rules, Workings Of The Shanghai International Gold Exchange.

To substantiate my estimates on above ground gold reserves in China mainland, we’ll first discuss private gold accumulation in China through the Shanghai Gold Exchange (SGE), after which we’ll address official purchases by the People’s Bank of China (PBOC) and its proxies that operate in the international over-the-counter market.

Chinese Private Gold Accumulation

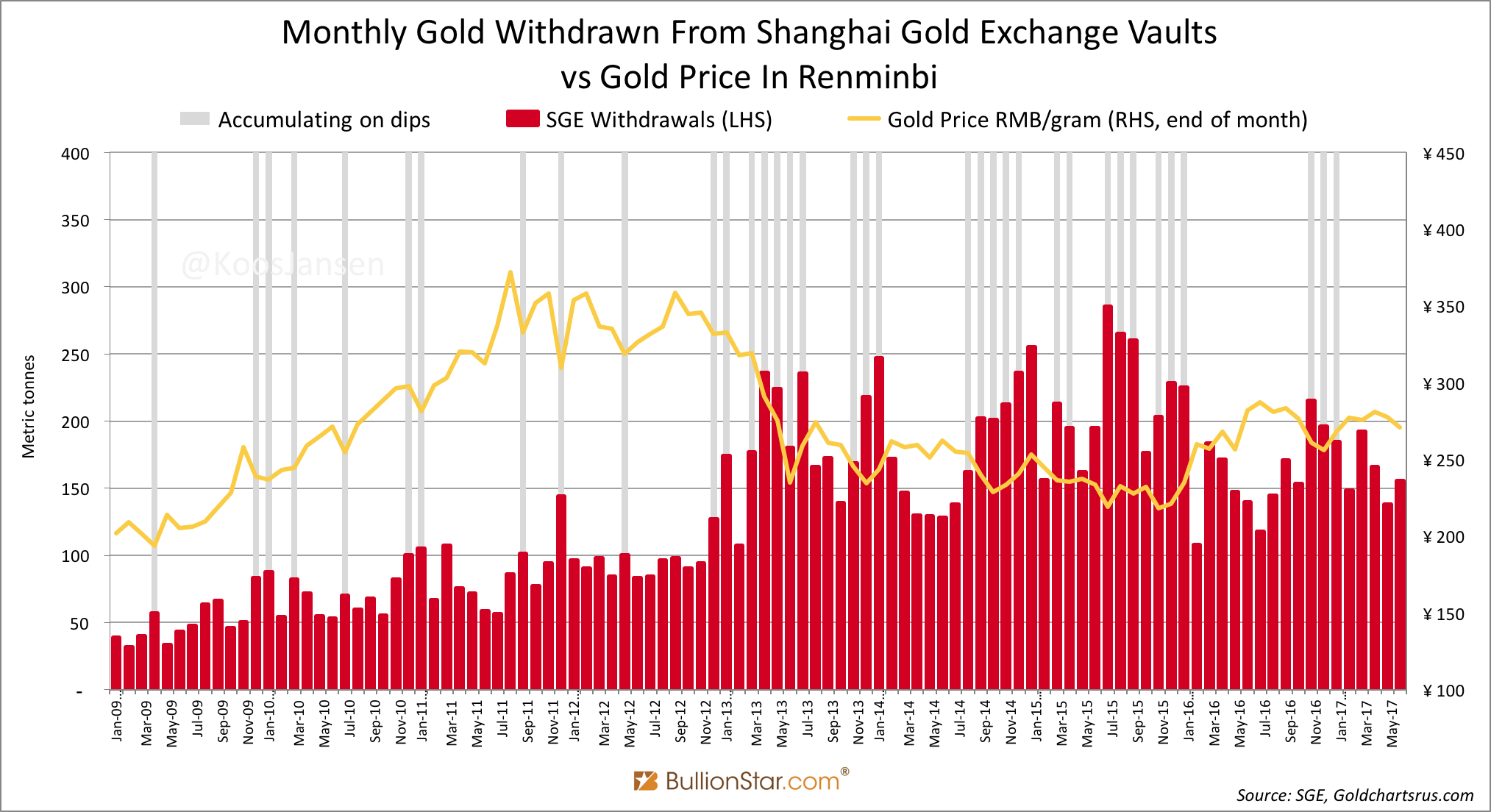

A few days ago, you could read on the BullionStar Gold Market Charts page that withdrawals from the vaults of SGE in June accounted for 156 tonnes. Year to date SGE withdrawals have reached 984 tonnes, which is 16 % shy of the record year 2015 when 1178 tonnes were withdrawn by this time. Since 2013 gold demand in China has remained extremely elevated – don’t let the World Gold Council tell you anything different – which exposes spectacular years of physical gold accumulation by the Chinese.

The amount of SGE withdrawals provides a fairly good proxy for Chinese wholesale gold demand, although not all gold passing through the SGE adds to above ground reserves. In China, most scrap supply and disinvestment flows through the Shanghai bourse as well, next to mine output and imports. Needless to say, recycling gold within China doesn’t change the volume of above ground reserves. So, simply using SGE withdrawals won’t fly for calculating above ground reserves. What we’re interested in are net imports and mine production in the Chinese domestic gold market.

Although gold exports from the Chinese domestic market are prohibited, exports from the Shanghai Free Trade Zone (SFTZ) where the Shanghai International Gold Exchange (SGEI) is located, are permitted. Before calculating Chinese net imports, let’s have a brief look at exports from the SFTZ – which reflects to what extent the SGEI is developing as a physical gold hub in Asia. As far as I can see, China’s gold bullion export from the SFTZ is still negligible. From the United Nations’ international merchandise trade statistics service COMTRADE, it shows the only countries that have imported tiny amounts from China in 2017 are the UK and India. But the amounts are so small, they carry little importance for our analysis.

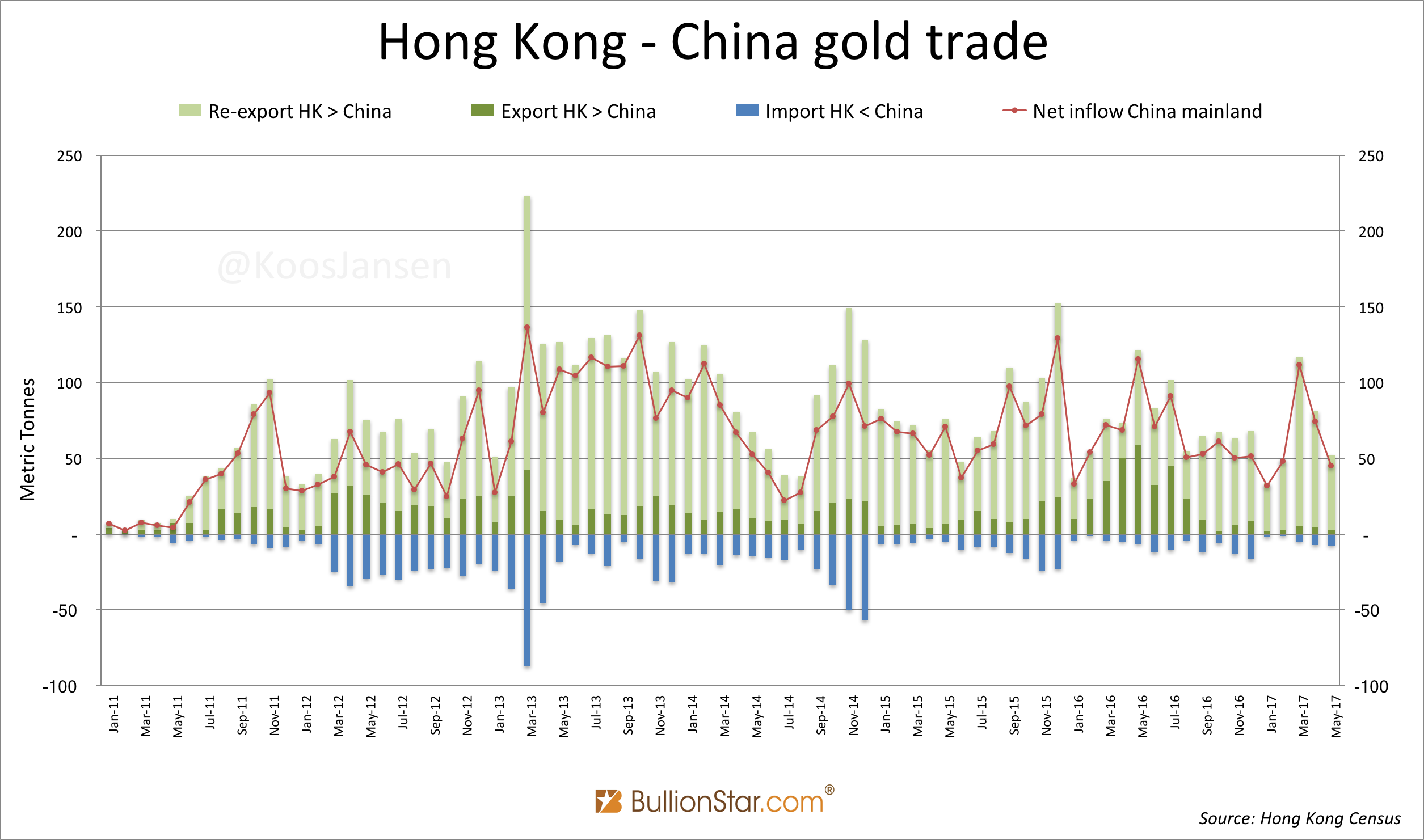

There is one region that is importing significant amounts of gold from China, which is Hong Kong, though, this likely isn’t exported from the SFTZ but from the Shenzhen Free Trade Zone. The vast majority of China’s jewellery manufacturers are in Shenzhen, and for quite some years gold jewellery, ornaments, industrial and semi-manufactured parts are being exported from this Chinese fabrication base to Hong Kong. These events haven’t got anything to do with the SGEI in my opinion. Thereby, Hong Kong exports far more gold to China than vice versa.

For computing net gold export from Hong Kong to China we’ll subtract “imports into Hong Kong from China” from “exports and re-exports from Hong Kong to China” (as you know China doesn’t disclose gold trade statistics itself). Imports into Hong Kong accounted for 23 tonnes, while exports and re-exports to China accounted for 333 tonnes. Accordingly, China net imported 311 tonnes from Hong Kong in the first five months of 2017.

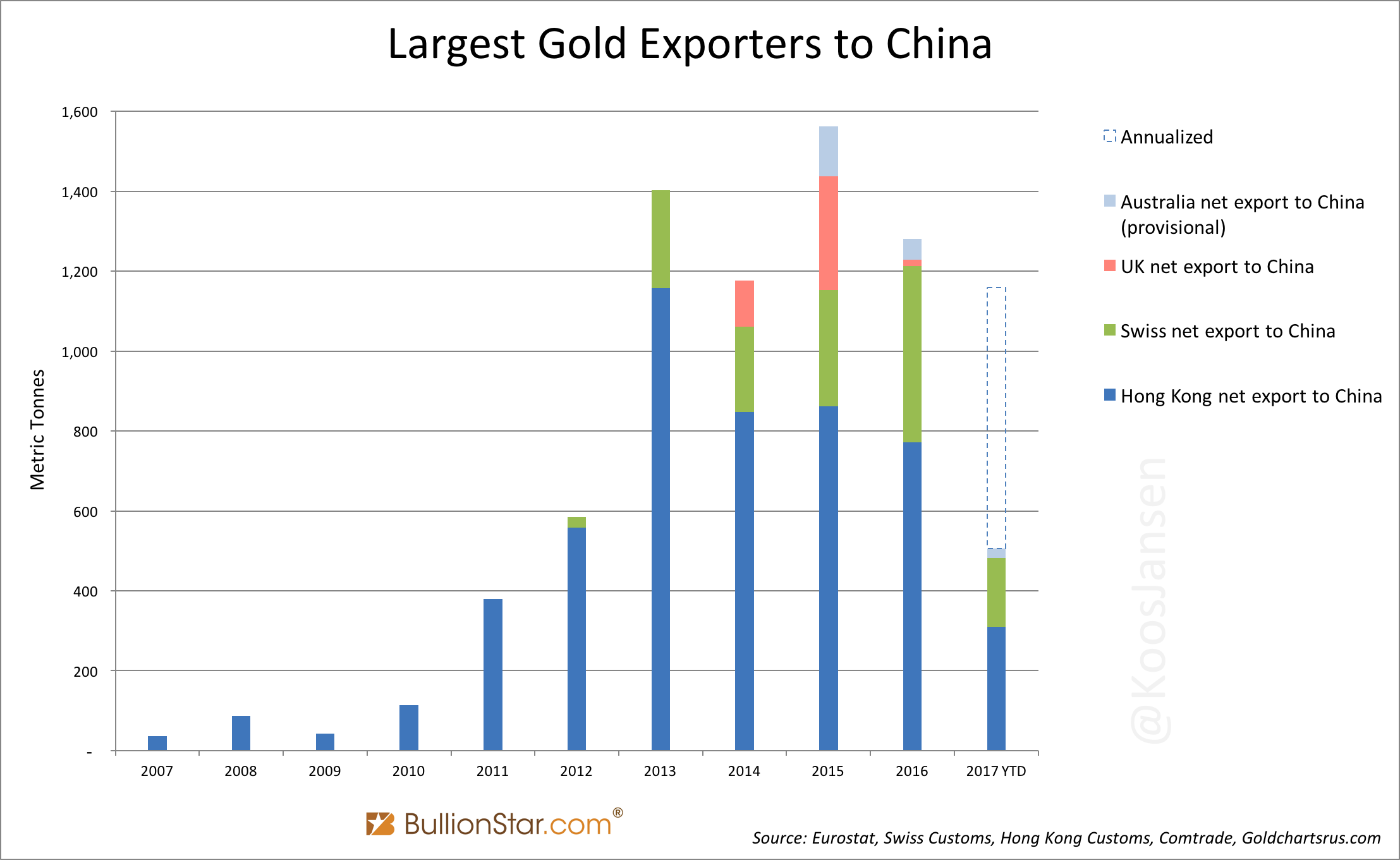

If we apply the same math to Switzerland’s customs data, it shows China net imported 172 tonnes from the Swiss in the first six months of this year.

Most definitely Australia has exported gold bullion directly to China in 2017 as well, but the Australian Bureau of Statistics (ABS) has changed its methodology regarding this data somewhere in 2016 and is reluctant to share the details with me. Using my old way to compute Australia’s export directly to China results in 23 tonnes (this number is provisional and will be amended).

The UK, a large gold exporter directly to China in 2014 and 2015, hasn’t shipped any gold directly to China year to date, according to Eurostat.

What’s remarkable is that Chinese true gold demand is far greater than what the World Gold Council (WGC) and GFMS are reporting as “Chinese consumer gold demand”. This is due to incomplete metrics applied by the WGC and GFMS. The immense tonnages imported by China have been waived in previous years, by the aforementioned Western consultancy firms, with dishonest arguments. (If you like to study the details regarding gold demand metrics read this.) In reality, thousands of tonnes are being imported into China and this metal is not coming back in the foreseeable future; causing a bull run on steroids if institutional interest for gold rebounds in the West. Ascending above ground reserves within China imply declining above ground reserves in the rest of the world. And the more scarce the metal in the West, the higher price when demand revives. I’ve described this phenomenon in my previous post How The West Has Been Selling Gold Into A Black Hole. In a forthcoming posts I will add more texture to my analysis.

Domestic mine production in China is not allowed to be exported, effectively all output can be added to above ground reserves. The China Gold Association (CGA) wrote on April 28, 2017, that Chinese domestic mine output in the first quarter accounted for 101 tonnes. Lacking the data for the second quarter, makes me estimate mine production from January until June by doubling 101, which is 202 tonnes. By the way, the CGA added:

Gold is a special product with the dual attribute of general commodity and currency. It is the cornerstone of important global strategic assets and the national financial reserve system. It plays an irreplaceable role in safeguarding national financial stability and economic security.

Based on data publicly available, in the first six months of 2017 China net imported at least 506 tonnes into the domestic market and mined 202 tonnes. An addition of 707 tonnes to Chinese private gold reserves.

Chinese Official Gold Purchases

I can be short on PBOC gold purchases: the Chinese central bank does not buy any gold through the SGE – its increments must be treated in addition to all visible flows – and it buys in secret not to disturb the global market. I’ve shared my analysis regarding the PBOC buying gold through proxies in the international over-the-counter (OTC) market for several years on these pages. Although, my reasoning has been confirmed countless times, it’s worth noting it was affirmed once more not long ago.

Early 2017 world renowned gold analyst Jim Rickards was in a meeting with the three heads of the precious metals trading desks of largest Chinese bullion banks. These gold dealers told Rickards that indeed the PBOC does not buy any gold through the SGE. Rickards stated in the Gold Chronicles podcast published January 17, 2017 (at 25:00) [brackets added by Koos Jansen]:

What I [J. Rickards] don’t know is about the Shanghai Gold Exchange sales, they’re pretty transparent, how much of that is private and how much of that is the government [PBOC]. And I was sort of guessing 50/50, 70/30, whatever. What they told me, and these guys are the dealers [the three heads of the precious metals trading desks], it’s 100 % private. Meaning, the government operates through completely separate channels. The government does not operate through the Shanghai Gold Exchange. … None of what’s going on on the Shanghai Gold Exchange is going to the People’s Bank Of China.

In fact, the PBOC uses Chinese banks as proxies to buy gold in countries like the UK, Switzerland and South-Africa after which the metal is transhipped to Beijing. Note, monetary gold shipments do not show up in customs reports of any country.

I haven’t come across any clues in the past months that have changed my estimate on the PBOC’s true official gold reserves. My best substantiated guess still is 4,000 tonnes (in contrast, the PBOC publicly discloses it holds about 1,840 tonnes). For more information on how and when the PBOC stacked up to 4,000 tonnes, continue reading at the BullionStar Gold University by clicking here.

Estimated Total Gold Reserves China 20,000 Tonnes

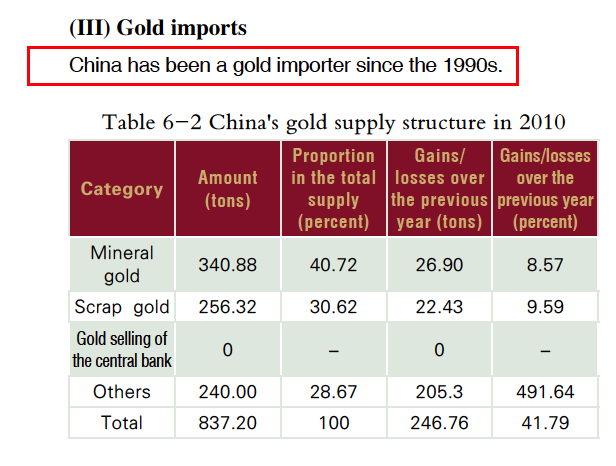

Let us put the pieces of the puzzle together. We know the PBOC doesn’t buy gold though the SGE, but prior to 2007 the Chinese gold market wasn’t fully liberalized and back then the PBOC was primary dealer in the domestic market. Any PBOC purchases prior to 2007 could have been from Chinese gold mines. What else do we know? China is said to be a gold importer since the 1990s, suggesting domestically mined gold was not exported after, say, 1994. In the next screen shot from the China Gold Market Report 2010 we can read “China has been a gold importer since the 1990s”.

For the sake of simplicity, we’ll calculate from 1994 onwards. Precious Metals Insights (PMI) has estimated that 2,500 tonnes of gold jewellery were held by the Chinese population in 1994. Furthermore, I have data on Chinese non-monetary gold import starting in 2001 – which started slowly but ramped up in 2010 (exhibit 2).

In 1994 PBOC official reserves accounted for 394 tonnes and Chinese domestic mine output accounted for 90 tonnes. So, our starting point in 1994 is:

2,500 (jewellery base) + 394 (official reserves) + 90 (mining) = 2,984 tonnes

From here, we can aggregate domestic mine output and net imports for every succeeding year. As stated above, my assumption is that the PBOC sourced its official gold from domestic mines prior to 2007, but shifted these acquisitions to the international market after 2007. The official gold increments in 2001 (105 tonnes) and 2003 (100 tonnes) I’ve subtracted from “aggregate domestic mine output”, the increments in 2009 (454 tonnes) and onwards I did not subtract from “aggregate domestic mine output”.

The previous calculation has resulted in the following chart:

In the chart the green, blue and grey bars represent private gold reserves, and summed up account for an estimated 16,193 tonnes at the time of writing. The red bars reflect the PBOC’s official gold reserves – I would like to stress this number is speculative – and currently account for 4,000 tonnes. My best estimate as of June 2017 for total above ground gold reserves within the Chinese domestic market is 20,193 tonnes.

Popular Blog Posts by Koos Jansen

China’s Secret Gold Supplier is Singapore

China’s Secret Gold Supplier is Singapore

Audits of U.S. Monetary Gold Severely Lack Credibility

Audits of U.S. Monetary Gold Severely Lack Credibility

China Gold Import Jan-Sep 797t. Who’s Supplying?

China Gold Import Jan-Sep 797t. Who’s Supplying?

The Gold-Backed-Oil-Yuan Futures Contract Myth

The Gold-Backed-Oil-Yuan Futures Contract Myth

Estimated Chinese Gold Reserves Surpass 20,000t

Estimated Chinese Gold Reserves Surpass 20,000t

PBOC Gold Purchases: Separating Facts from Speculation

PBOC Gold Purchases: Separating Facts from Speculation

U.S. Mint Releases New Fort Knox Audit Documentation

U.S. Mint Releases New Fort Knox Audit Documentation

China Net Imported 1,300t of Gold in 2016

China Net Imported 1,300t of Gold in 2016

Why SGE Withdrawals Equal Chinese Gold Demand and Why Not

Why SGE Withdrawals Equal Chinese Gold Demand and Why Not