Chinese Gold Market

Introduction

As with most things in China, large is the operative word. This is particularly true of the Chinese gold market. China is the largest gold producer in the world, producing an estimated 450 tonnes of gold mining output in 2015[1], nearly as much as the next two largest producers combined (Australia and Russia). China is also the largest gold importers in the world based on amalgamated import statistics.

China’s Shanghai Gold Exchange is the largest physical gold exchange in the world, with the highest physical turnover and largest physical withdrawals of any gold exchange in the world. Total gold trading on the Shanghai Gold Exchange (SGE) reached a mammoth 17,033 tonnes in 2015, up 84% from gold trading volume of 9,243 tonnes in 2014. Physical gold withdrawals from the SGE totalled 2,596 tonnes in 2015. China’s state-controlled bank ICBC, which is extensively involved in the gold industry, is the largest bank in the world. The Chinese central bank, the Peoples bank of China (PBoC), can also boast the fastest growing official gold reserves in the world.

As the Chinese Government and the PBoC continue to embark on the internationalisation of the Renminbi (RMB), for trade payments, outward investment, and ultimately as a reserve currency, the onshore and offshore trading of gold through the Shanghai Free Trade Zone, and the International Board of the Shanghai Gold Exchange should take on added significance, and allow China to acquire some pricing power in determining the international gold price. This is why the upcoming Shanghai Gold Fix is being eagerly awaited, although expectations about its impact are undoubtedly a case of too high too soon.

Exchange and Venue:

SGETicker Code:

Au (T + D)Deliverable grade:

Gold bullion with a fineness no lower than 99.95%Contract Size:

1kg per lotTick size:

0.01 Yuan per gramPrice Quotation:

Yuan per gramPrice Limit:

+/- 7% closing price of previous trading dayTrading Hours:

Morning: 9:00am – 11:30am, Afternoon: 1:30pm – 3:30pm, Night: 8:00pm – 2:30amDelivery Days:

Each trading dayDelivery Method:

Physically Delivered – Delivery versus PaymentDelivery Unit:

Delivery standard: 3kg gold ingot with fineness >= 99.95% or 3 * 1kg gold ingots with fineness >= 99.99%Delivery Locations:

SGE certified vaultsExchange:

SGEVenue:

Shanghai International Gold Exchange (SGEI)Ticker Code:

iAu99.99Underlying grade:

1 kg gold ingot of minimum 99.99% finenessContract Size:

10 grams per lotTick size:

0.01 Yuan per gramPrice Quotation:

Yuan per gramPrice Limit:

+/- 30% closing price of previous trading dayTrading Hours:

Morning: 9:00am – 11:30am, Afternoon: 1:30pm – 3:30pm, Night: 8:00pm – 2:30amDelivery Method:

Physically Delivered – Delivery versus PaymentDelivery Period:

T+0Delivery Unit:

Gold ingots with Standard Weight of 1 kg and fineness >= 999.9 from SGE certified gold producers or producers accredited by London Bullion Market Association (LBMA).Delivery Locations:

Delivery Vaults certified by SGE international boardExchange:

SHFEProduct:

GoldContract Symbol:

AUContract Size / Trading Unit:

1 kilogram/lot (standard gold)Price Quotation:

(RMB) Yuan /gramMinimum Price Fluctuation:

0.05 Yuan/gramDaily Price Limit:

Within 3% above or below the settlement price of previous trading dayContract Series:

Monthly contract covering the nearest 3 consecutive months and then consecutive even months contracts within the most recent 11 monthsTrading Hours:

Day sessions: 9:00am – 11:30am & 1:30pm – 3:00pm (Beijing Time) Night session 9:00pm – 2:30am next morning (Beijing Time) and other trading hours as prescribed by the SHFELast Trading Day:

15th day of spot month (if holiday, day after holiday)Delivery Period:

5 consecutive business days after last trading dayGrade and Quality:

Domestic gold : Gold bullion with fineness greater than or equal to 99.95% (can be 99.99%) Non-domestic gold: Standard bullion of refiners on LBMA good delivery list (gold) that are certified by SHFE for physical deliveryDelivery Unit:

Weight (net weight): 3 kilogram/warrant, delivery made in integral multiples of each warrant If 1 kg bars are delivered, gold content >= 99.99%. If 3kg bars delivered, gold content >= 99.95% (gold for each warrant delivered should be from the same producer with the same brand and gold content)Delivery venue:

A SHFE Certified Delivery WarehouseSettlement Type:

Physical DeliveryContents

- 1. Introduction

- 2. Infographic – The Chinese Gold Market

- 3. China’s involvement with Gold in the 20th Century

- 4. China’s large state-controlled banks

- 5. The Shanghai Gold Exchange

- 6. Shanghai Pilot Free Trade Zone

- 7. Shanghai International Gold Exchange (SGEI) – International Board

- 8. SGE Trading Details

- 9. Price Matching Market

- 10. Price Asking Market

- 11. SGE ‘Standard’ gold

- 12. SGE and SGEI ‘Price Matching’ Gold Contracts

- 13. Chinese Interbank Gold Trading Market

- 14. SGEI Members

- 15. SGE and SGEI Trading Volumes

- 16. SGE Withdrawals Data

- 17. SGE and SHFE Gold Vaults

- 18. SGE International Collaboration

- 19. Shanghai Futures Exchange (SHFE)

- 20. SHFE Gold Futures Contract

- 21. Chinese Central Bank – Peoples Bank of China (PBoC)

- 22. China Gold Association and World Gold Council

- 23. Gold Mining in China

- 24. Gold Refineries in China

- 25. Chinese Gold Coin Mints

- 26. Gold Imports into China

- 27. Gold Exports from China

- 28. Chinese Gold Demand

- 29. Conclusion

- 30. References and Links

Infographic – The Chinese Gold Market

China’s involvement with Gold in the 20th Century

An understanding of the contemporary official Chinese perspective on gold requires a brief understanding of China’s political and monetary system during the 20th century and the emergence of the communist Peoples Republic of China (PRC). While many other economies were on a gold standard during the early 20th century, the then Republic of China, or more practically the financial centre of Shanghai, employed a silver standard, and the region remained on this silver standard until November 1935, with the Shanghai tael (equal to 518.512 grains of silver) used as the accepted silver measurement unit until 1933[2]. During this period, silver coinage (and gold coinage) circulated freely as money within China. Even after the departure from the silver standard, both monetary metals continued to be circulated as money, and during the 1930s and 1940s, Shanghai was the largest gold trading centre in East Asia[3].

From 1927, a low-key civil war was fought between the then dominant and ruling political party of the Kuomintang (KMT) (Nationalist Party), and the Communist Party of China (CPC). This inter-party war took a back seat during the period of full-scale war that took place between the Republic of China and the Empire of Japan which started in 1937 and ended in August 1945 (part of WWII). After the Japanese were defeated in 1945, the Chinese civil war again came to the fore and lasted 4 more years, however, it was not obvious at that time that the CPC would be victorious. For example, in 1946, the International Monetary Fund (IMF) had even authorised the addition of the Central Bank of China in Shanghai as one of the IMF’s 5 designated gold depositories within the Bretton Woods monetary system. In 1949, when it became fully obvious that the Communists had defeated the KMT, the IMF then ‘temporarily’ removed Shanghai from the gold depository list. See BullionStar blog “The IMF’s Gold Depositories – Part 2, Nagpur and Shanghai, the Indian and Chinese connections” for more details.

By 1949, the defeated KMT had fled to Taiwan (with the nation’s official gold reserves), and the CPC then established the Peoples Republic of China (PRC) in 1949. As a centrally controlling governing structure, one of the PRC’s first initiatives was a ban on private ownership of both gold and silver[4], and a seizure of control over the banking system to form the Peoples Bank of China(PBoC), as well as a seizure of the economy’s financial markets (including gold and silver trading).

In June 1983, the PRC published ‘Regulations on the control of gold and silver’, which specified detailed controls (35 articles long) on managing the precious metals markets, covering purchases and sales of gold and silver, imports and exports of silver, and controls over gold and silversmiths in China[5]. These regulations were implemented by a set of PBoC rules published in January 1984 –“Detailed rules for the implementation of the regulations on the control of gold and silver of the People’s Republic of China”[6].

Although various periods of economic reforms were implemented in China beginning in 1978, and continued with large-scale privatisations in the late 1990s, it was only in March 2001 that the PBoC announced an end to its monopoly on management of the gold market[7]. This was part of China’s broader gold market liberalisation strategy, which was stated in its 10th Five Year plan of 2001. The gold market liberalisation strategy was first referenced in the World Gold Council organised “2000 China Gold Economic Forum” held in Beijing in October 2000[8].

This gold market liberalisation, after over 50 years of State control, included a move from State monopoly on the gold market to a free-market gold sector, the proposal of a ‘gold exchange’ in Shanghai, the removal of licensing requirements for gold market participants (including encouraging the retail public to participate in the domestic gold market), and the gradual abolition of gold import and export controls.

In 2001, the China Gold Association (CGA) was launched by the PRC and the State Economic and Trade Commission. A very early version of the CGA website from March 2002 can be seen here[9]. In October 2002, the Shanghai Gold Exchange (SGE) was officially launched, having been in a test phase for the previous 11 months. At launch there were 108 members authorised to trade gold on the Exchange. By 2004, private citizens in China were again allowed to transact and possess gold bullion. In 2008, the first Chinese gold futures contract was launched by the Shanghai Futures Exchange (SHFE). Finally, in September 2014, the SGE launched the Shanghai International Gold Exchange (SGEI).

China’s large state-controlled banks

China’s four large state-controlled banks are critical components of the Chinese gold market. These four banks are the Industrial and Commercial Bank of China (ICBC), Bank of China (BoC), China Construction Bank (CCB), and Agricultural Bank of China (ABC).Therefore, before looking at the Chinese gold market, it’s important to be aware of the identities and backgrounds of these banking entities. These four banks were all previously state-owned but each went through transformations in the 2000s whereby they became joint-stock companies and their equity was then listed on both the Hong Kong and Shanghai stock markets. However, the PRC still maintains controlling interests in these banks, mainly through a Beijing headquartered company called ‘Central Huijin Investment Company’[10].

Central Huijin Investment Company was created by China’s State Administration of Foreign Exchange (SAFE)[11] in 2003, and since 2008 has been a fully-owned subsidiary of China’s sovereign wealth fund China Investment Corporation (CIC)[12]. CIC is itself owned by the PRC. The sole role of Central Huijin is to invest equity in China’s large state-owned financial enterprises and to represent the wishes of the State Council on the boards of these companies.

It’s therefore important to keep in mind the interactions between the PRC, the PBoC, SAFE, CIC and these ‘Big 4’ Chinese banks. Apart from the Big 4 banks, Central Huijin holds equity stakes in other entities such as China Development Bank, China Everbright Bank, China Export & Credit Insurance Corp etc. A full list of Central Huijin’s investments can be seen on its website.

Industrial and Commercial Bank of China (ICBC) was incorporated in January 1984. It transformed from a state-owned bank to a state-controlled joint-stock commercial bank in 2005, before becoming dual-listed on the Hong Kong and Shanghai stock exchanges in October 2006. The PRC’s Ministry of Finance is still one of ICBC’s controlling shareholders[13]. Another controlling shareholder is the Central Huijin Investment Company.

Bank of China (BoC) was founded in 1912. In 1949, BoC was taken over by the PRC and in 1950 began to be managed by the PBoC, at which point it became a specialised foreign exchange bank. In 1979 BoC was detached from the PBoC, and given responsibility for SAFE, and for China’s wider foreign exchange operations. In 1983, the PBoC became a central bank and SAFE was detached from BoC. BoC then remained a specialised foreign exchange bank with the PBoC providing oversight until 1994 when BoC became a state-owned commercial bank. In 2004, Central Huijin Investment Company took a controlling interest in BoC, and in July 2006, BoC was dual listed on the Hong Kong and Shanghai stock exchanges[14].

The predecessor of China Construction Bank (CCB) was established in 1954 as a state-owned bank, to specialise in funding Chinese construction and infrastructure projects. CCB converted from a state-owned bank to a joint-stock commercial bank in 2004 through the participation of Central Huijin Investment Company, and part of the bank was spun off into another entity called Jianyin. CCB was listed first on the Hong Kong Stock Exchange in 2005, and subsequently listed on the Shanghai Stock Exchange in 2007[15].

Agricultural Bank of China (ABC) was founded in 1951 as a specialist bank for the Chinese agricultural sector. At that time it was known as the Agricultural Cooperative Bank. ABC transformed from a state-owned bank to a state controlled joint-stock company in 2009, and became dual listed on the Hong Kong and Shanghai stock exchanges in 2010[16].

Bank of Communications (BoCom) is a Shanghai headquartered nationwide Chinese commercial bank. Although its outside of the Big 4 list, BoCom is noteworthy in that its very involved in the Chinese gold market. BoCom is state-controlled and it also floated on the Hong Kong stock market (2005) and Shanghai stock market (2007) as a joint-stock company[17].

Note that until 1978, PBoC was the only bank in China, and it engaged in central banking and commercial banking. In 1979, Bank of China and CCB were split off from the PBoC. Agricultural Bank of China separated out into a state owned entity in the late 1970s. By 1983, all commercial banking operations had been fully split off from PBoC. What remained of the PBoC was then officially designated by the PRC in 1983 as the Chinese Central Bank. Note that ICBC was only incorporated on 1st January 1984, after the PBoC became the central bank.

The Shanghai Gold Exchange

The Shanghai Gold Exchange(SGE)[18] was formally launched on 31 October 2002[19] by the Peoples Bank of China (PBoC), and since establishment, the Exchange has been supervised by the PBoC. At launch date, the Chinese Government and PBoC transitioned some of their gold market management functions to the SGE.

All SGE trading platforms are electronic. The SGE offers spot and deferred trading, as well as forwards, options and leasing, and also runs the Exchanges’ central market clearing process for all of the above products, and the delivery, transfer, and vaulting services for the gold flowing into, out of, and held in the Exchanges’ vaults.

The Exchange’s building is located at No.99 Middle Henan Road in the central Huangpu District of Shanghai. The SGE is the world’s largest physical gold exchange. In 2014, 18,500 tonnes of physical gold were traded on the Exchange.

The SGE categorises its members as domestic or international. The Exchange has over 180 domestic members representing approximately 10,000 corporate customers and approximately 8.3 million individual customers. Within the domestic membership category, ‘Financial Members’ (institutions) are authorised by the Exchange to engage in brokerage transactions and proprietary trading. There are approximately 36 of these institutions. Most of the other institutional members are ‘General Members’ (129 members) that are permitted to only engage in proprietary trading. There is also a domestic membership category of ‘Special Member’ representing 10 members, and 2 ‘Proprietary members’[20]. Domestic members can transfer their membership to other entities.

Some of the initial foreign banks that became domestic members of the SGE in 2008-09 were HSBC[21], Standard Chartered, ANZ, Scotia, and Credit Suisse.

In 2014 the Chinese authorities and the SGE embarked on the launch of an International Board of the SGE as part of China’s ongoing internationalisation of its gold market and currency market. The International Board offers ‘international’ members access to Renminbi trading of gold on the SGE and International Board certified precious metals vault located in the Shanghai Free Trade Zone.

Shanghai Pilot Free Trade Zone

The China (Shanghai) Pilot Free Trade Zone, commonly called Shanghai Free Trade Zone[22], Shanghai FTZ, or just SHFZT, was established in September 2013. At establishment, it was the first FTZ in China, but in 2015, three further FTZs have been launched in Tianjin (near Beijing), Fujian (near Taiwan), and Guangdong (near Hong Kong and Macau).

In theory, the FTZ supports the deregulation of the Chinese economy, and the internationalisation of the Renminbi, encourages foreign trade and investment into China, provides foreign companies with access to customs ‘lite’ logistics and storage areas and a lightly regulated business environment, however, in practice, the Shanghai FTZ has had limited success since inception[23]

Initially the FTZ consisted of a ‘FTZ Bonded Area’ east of downtown Shanghai which encompassed an area around Pudong International Airport, the Yangshan area including Yangshan port and harbour, and the Waigaoqiao free trade zone and logistics park. This area comprises 28.78 square kilometres. In early 2015, the Chinese Government substantially expanded the Shanghai FTZ to include the Lujiazui financial area, the Zhangjiang high tech park area, and the Jinqiao export zone, making the entire Shanghai FTZ 102.72 square kilometres.

Shanghai International Gold Exchange (SGEI) – International Board

The Shanghai International Gold Exchange[24], abbreviated as SGEI, and also known as simply ‘the International Board’ was launched in September 2014[25]. Shanghai International Gold Exchange Co. Limited (SGEI) is a wholly-owned subsidiary of the Shanghai Gold Exchange. The SGEI is located within the Shanghai Pilot Free Trade Zone and its office address is 42/F, Bank of China Tower, 200 Yincheng Road Central, in the Pudong District of Shanghai, which is across the river Huangpu in the financial district to the east of the SGE building. The International Board certified precious metals vault is also located within the FTZ, which, for SGEI members, simplifies moving gold into and out of China, since customs declarations are speedier and less erroneous.

Members of the SGEI (i.e. International members of the SGE, can be either ‘Full Members’ (called Type A members), Proprietary Members (called Type B members), or ‘Special International Members’. Full members are authorised to engage in proprietary trading and brokerage, whereas proprietary members, as the name suggest, can only engage in prop trading.

Since the Shanghai International Gold Exchange is known as the ‘International Board’ of the SGE, the original non-International SGE is now sometimes referred to as the ‘Main Board’.

SGE Trading Details

SGE consists of two specific trading markets, namely a “Price Matching Market” and a “Price Asking Market”. The Price asking market cover a wholesale OTC market and a Leasing Market.

Price Matching Market

SGE trading takes place on an electronic trading platform where buy and sell orders are matched, hence the name ‘Price Matching Market’. For gold, the Exchange offers physical trading (T+ 0) and trading with deferred settlement (T + D), where T = Trade Date, and D = Number of Days deferred. The 16 SGE/SGEI products referred to below are all on the ‘Price Matching Market’.

Physical trading

The SGE’s ‘physical trading’ is spot trading with same day settlement or T+0. With physical trading and intra-day settlement, buyers must hold the full cash value of an order in their accounts, and the seller must hold the required physical gold in their accounts. Buyers can re-sell the purchased gold on the same day and withdraw or transfer it the following day. Sellers may use up to 90% of same day sales proceeds within subsequent trades.

Trading with Deferred Delivery

The SGE also offers deferred trading on margin, which is simply margin trading with an in-built option on delivery dates. With delivery dates for physical metal unknown, the SGE uses a mechanism of deferred interest and what it calls a ‘delivery equaliser’, to cover undelivered lots. For example, if a seller decides to defer or postpone delivery of a transaction, deferred interest is charged on the undelivered contract lots. Ultimately, the delivery has to happen, and another participant can step in as the ‘Delivery Equaliser’ to deliver, and this entity then receives the accumulated deferred interest.

Price Asking Market

Products on the SGE ‘Price Asking Market’ consist of Spot, Forwards and Swaps (PAu99.99 PAu99.95 iPAu9999 iPAu99.5 iPAu100g), Options (OAu9999 OAu9995), and Interbank Leasing(LAu99.95 LAu99.9 iLAu9999 iLAu99.5 iLAu100g).

The OTC market and the SGE

The SGE allows market participants to trade spot, forwards, swaps and options, bilaterally on the OTC market and then confirm these trades details using the SGE price asking platform, and then clear the trades through the SGE’s clearing system. The contract names for OTC products have a ‘P’ suffix for spot, forwards and swaps, and an ‘O’ for options:

- PAu99.99

- PAu99.95

- iPAu9999

- iPAu99.5

- iPAu100g

- OAu99.99

- OAu99.95

SGE gold leasing market

The SGE facilitates gold leasing, gold pledging, and gold location swaps through its transfer system. Members of the International Board can lease, pledge and swap deliverable product gold between each other and also with those domestic members of the SGE that have a gold import license. Lending by International Board members to domestic members who do not have gold import licenses requires SGC approval.

Accounts

An SGE account consists of two components, a margin account and a bullion account, but they are really two parts of the same account, one part for cash and the other part for gold bullion. Any Chinese individual can open ‘one’, and only one, SGE account to transact gold from. In the margin account, a customer holds a trading margin and a clearing deposit. SGE accounts are opened at participating Chinese banks. The Chinese public can even trade gold at the SGE using a mobile phone app. See BullionStar blog “In China Everyone Can Buy Gold At The SGE” for details.

Trading sessions on the SGE

The Exchange’s trading hours are Monday to Friday within 3 trading sessions:

Morning Session: 9:00am – 11:30am

Afternoon Session: 1:30pm – 3:30pm

Night Session: 8:00pm – 2:30am

SGE ‘Standard’ gold

The SGE only accepts ‘standard gold’ into SGE designated vaults: Standard gold is defined by the SGE as follows:

- Gold that is cast by an SGE approved refinery

- Aacceptable weights: 50g, 100g [bars], 1Kg, 3Kg, 12.5Kg [ingots]

- Acceptable purities: 9999, 9995, 999, 995

The PBoC obliges domestic gold producers to sell all of their Standard gold via the SGE. Domestic gold producers could sell non-Standard gold off the SGE in a less processed form such as doré or ore bars, however nearly all Chinese domestic gold mining output is refined into Standard gold and sold through the SGE. This is because gold mines have a nbumber of incentives to refine their gold output to this ‘Standard’.

Firstly, Standard gold traded on the SGE has the deepest liquidity, so domestic gold mining companies will invariably direct that their output be converted into standard gold form (either 50g, 100g, 1kg, 3kgs, 12.5kgs bars of 9999, 99995, 999 or 995 fineness) so as to access this deep liquidity. A further incentive is that Standard gold sold on the SGE is VAT exempt while Standard gold sold away from the SGE is not VAT exempt. Scrap gold in China is not obliged to be sold through the SGE. But because SGE standard gold is VAT exempt, gold refineries again have an incentive to convert scrap into Standard gold bars and trade these bars through the SGE.

In a similar way to the LBMA’s good delivery gold ‘chain of integrity’ in London, Standard gold bars withdrawn from the SGE vault network is not accepted back into the SGE vault network as its provenance cannot be determined. Standard gold that has been withdrawn from the SGE would first have to be remelted, recast and assayed by an SGE approved gold refinery before being accepted back into the SGE vault network.

SGE and SGEI ‘Price Matching’ Gold Contracts

The SGE offers 16 precious metals contracts[26], 12 of which are on gold, 3 on silver and 1 on platinum. Of the 12 gold contracts, 8 are for physical delivery and 4 for deferred delivery 9or margin trading). Of the physical contracts, 5 are on the Main Board and 3 are on the International Board. All SGE and SGEI contracts are priced in RMB.

Drawing on the SGE standard gold specifications, the 5 gold contracts on the Main Board of the Exchange for physical and spot gold trading, and their respective delivery bar standards are:

Au99.5 12.5 kgs ingot, fineness 995*

Au99.95 3 kgs ingot, fineness 9995

Au 99.99 1 kg ingot, fineness 9999*

Au 100g 100g bar, fineness 9999*

Au 50g 50g bar, fineness 9999

(* equivalent contract also listed on the SGEI)

These contracts are traded in onshore Renminbi (CNY). The Au99.99 and Au99.95 were the first contracts to be offered on the SGE. Both were launched in October 2002. This was followed by the launch of the retail Au50g contract in June 2004. Next launched was the Au100g in December 2006. The Au99.5 contract, for large Good Delivery bars, was launched in December 2013.

For trade settlement, the SGE has certified 18 settlement banks for currency clearing.

The 3 gold contracts offered on the International Board are named with an ‘i’ prefix. These 3 contracts are replicas of 3 of the Main Board contracts:

iAu100g 100 gram gold bar, fineness 999.9

iAu99.99 1 kg gold ingot, fineness 999.9

iAu99.5 12.5 kg gold ingot, fineness 995.0

These contracts are traded in offshore Renminbi (CNH). The three contracts on the International Board, iAu100g, iAu99.99 and iAu99.5 were launched in September 2014.

The SGE refers to gold contracts for deferred delivery as T + D contracts, where D = number of days to delivery. mAu stands for ‘mini’, i.e. 100 grams trading unit. Two of these contracts only require deferred interest to be paid once per year and are labelled as T + N contracts.

Au (T + D) Trading unit 1kg lot, delivery unit 3kg 999.5 ingot or 3 * 1kg 999.9 ingots

mAu (T + D) Trading unit 100g lot, delivery unit 1kg 999.9 ingot

Au (T + N1) Deferred interest paid in June, delivery unit 3kg 999.5 ingots or 3 * 1kg 999.9 ingots

Au (T + N2) Deferred interest paid in Dec, delivery unit 3kg 999.5 ingots or 3 * 1kg 999.9 ingots

In SGE deferred trading, trading margin is variable but, for example, was 7% during 2015. The margin is paid to the Exchange as the central clearing party.

All SGE trading and delivery rules are detailed on the Exchange’s website[27].

The SGEI uses an electronic trading platform known at the International Trading System. The SGEI has certified 7 Settlement Banks for currency clearing. These banks are ICBC, ABC, BOC, CCB, BOCOM, CMB, and SPD Bank.

Chinese Interbank Gold Trading Market

In January 2016, the SGE and China Foreign Exchange Trade System launched interbank (bi-lateral) gold trading among 16 mostly Chinese banks, 10 of which were deemed first tier market-makers, namely, ICBC, CCB, BoC, ABC, BoCom, China Merchants Bank, China CITIC Bank, Bank of Ningbo, Industrial Bank Co, and the Shanghai branch of Australia and New Zealand Banking Corp (ANZ) , with another 6 second-tier smaller Chinese bank market making participants. The aim of the launch is to enhance gold trading liquidity in the Chinese gold market[28]. With interbank gold trading, participating banks are able to buy and sell gold between each other directly, and are not obliged to trade solely with the SGE as counterparty, as was the case previously.

SGEI Members

There are approximately 52 international members of the SGEI (as of July 2015), however this figure includes the Shanghai Free Trade Zone branches of the large Chinese banks which are classified as international members of the SGEI. The SGEI has three types of membership, full members (type A members), proprietary members (type B), and special international members. Full members are permitted to carry on proprietary trading and brokerage. Proprietary members, as the name suggests, only engage in proprietary trading. Special international members include entities such as the Chinese Gold and Silver Exchange Society (CGSE Society). Unlike domestic members, international members can’t transfer their memberships to other entities, although they can withdraw and then reapply,

Foreign bank members of the SGEI include HSBC, Standard Chartered, Scotiabank, Goldman Sachs, UBS, ICBC Standard Bank, Natixis, Trafigura Pte, Mitsubishi (Japan), Bank of Taiwan, Bank of China (Hong Kong), Bank of Communications (Hong Kong), Australia and New Zealand Bank (ANZ) (FTZ Branch), Bank of Taiwan.

Non Chinese gold refiners represented are Metalor, Heraeus (Hong Kong), PAMP (+ MKS). The Chinese Gold & Silver Exchange Society (of Hong Kong) is an exchange members of the SGE and the SGEI. Other non-Chinese entity members include Thai gold refiner and wholesaler through its Singapore branch, YLG Bullion Singapore Pte, and from Dubai, Kaloti Jewellery International DMCC. Kaloti is a Limited Member.

Many Chinese banks are members of the SGEI, represented by their Shangahi Pilot FTZ Branch. Thes ebanks include ICBC, Bank of China, China Construction Bank, Bank of Communications, Agricultural Bank of China, China Minsheng Bank, China Merchants Bank, China Everbright Bank, Shanghai Pudong Development Bank, Bank of Shanghai, Industrial Bank, China CITIC Bank, and Pingan Bank.

Note that Deutsche Bank and JP Morgan Chase are not listed as members of the SGEI despite the SGE having earlier reported that they were[29]. Around the launch date of the SGEI in 2014, the SGE also mentioned that Citibank, Société Générale, Valcambi, and the Perth Mint were potential future members of the International Board, but as of yet, they are not.

To trade on SGEI, a member or its customer needs to set up a free trade zone account (FT account) in offshore RMB (CNH) with a clearing bank[30].

SGE and SGEI Trading Volumes

On the SGE Main Board, trading in the deferred contracts in highest, led by the Au (T + D) contract. In the spot contracts, the Au9999 contract consistently sees the highest trading volumes. Of the International Board contracts, the iAu9999 contract records the highest trading volumes.

Trading volumes in kgs reported by the SGE are bilateral so these need to be halved to avoid double counting.

SGE Withdrawals Data

Gold supply for any country can be captured by the formula: Gold Supply = Gold from Mining + Scrap recycling + Gold Imported.

All ‘Standard gold’ from Chinese gold mining companies has to be sold on the SGE. Likewise, all ‘Standard’ gold imported into China by the banks with import licenses has to be sold on the SGE. These are PRC / PBoC rules. Finally, most gold from scrap sources sold by Chinese refineries is sold through the SGE in the form of ‘Standard’ bars because the SGE is VAT free and the market is most liquid. Therefore, in China, the addition of Mining + Scrap + Imports is a good proxy of total Chinese gold supply.

Conversely, as the vast majority of wholesale gold sold in China is sold through the SGE and then withdrawn, then it is a very good proxy to use the equation that:

Chinese wholesale gold demand = SGE gold withdrawals

In other words, the widest measure of supply (mine supply, imports, scrap/recycling) = the widest measure of demand (SGE withdrawals). See BullionStar blog “The Mechanics Of The Chinese Domestic Gold Market” for further details.

For 2015, SGE gold withdrawals totalled a massive 2,596 tonnes, up from 2,102 tonnes in 2014 and 2,181 tonnes in 2013. This 2,596 tonne withdrawal is 81% of 2105 world gold mining output and shows that China is consuming far more gold than the mainstream media reports claim.

Up until the end of 2015, the SGE published weekly and YTD gold withdrawal data (in Chinese), and so annual gold withdrawal data from the SGE was readily discernible. From the beginning of 2016, this withdrawal data appears to only be published monthly (in Chinese) due to some SGE procedural changes. See BullionStar blog “SGE Continues To Publish Withdrawals Figures?” for details.

Some gold consultancies, such as the World Gold Council, calculate an annual figure for Chinese gold demand that is just based on retail demand. For 2015, the World Gold Council estimates that Chinese gold demand was 984 tonnes. This substantially understates the true figure because it does not take into account net investment by corporate and individual customers of the SGE withdrawing gold directly from the vaults of the Exchange.

SGE and SHFE Gold Vaults

The Shanghai Gold Exchange has certified 55 vaults for gold storage nationwide across 36 Chinese cities, and 3 certified vaults for silver, making 58 vaults in total. The vaults are in locations proximate to either gold refineries or jewelley/consumer centres.

The SGE International Board certified vault located in the Shanghai Free Trade Zone is managed by Bank of Communications (BOCOM)[31], and operates under the supervision of FTZ Customs staff. Based on the structure of the FTZ, gold imported into the SGEI vault remains outside China, since the FTZ is considered to be external to China.

This vault has a capacity of 1500 tonnes of gold and other precious metals.The SGEI – BOCOM vault is located at “20 Wanrong 1st Road, Zhabei District, Shanghai”[32]. Note that ICBC is planning to build a second SGEI certified vault in the Shanghai free trade zone.

In turn, the International Board (IB) Certified Vault, run by BoCom, has appointed Shanghai Huanyu Customs Broker Ltd as the designated agent for handling SGEI generated physical customs declaration applications in and out of China[33], and appointed G4S International Logistics (Shanghai) Ltd as designated secure transport operator to deliver gold to and from Shanghai airport and the IB vault[34][35].

As well as transaction services for gold deliveries and transfers related to Exchange transactions, the SGEI vault also provides segregated safe deposit storage for other customer gold unrelated to Exchange transactions. Any gold that is withdrawn from the SGE vault system must be re-assayed before being accepted back into the SGE system. This allows all gold with the SGE vault system to maintain its chain of integrity. Metal coming into SGE/SGEI vaults is referred to as ‘load-in, and conversely, metal being withdrawn is referred to as ‘load-out’.

Only those banks that hold gold import licenses can transfer gold from the SGEI vault to an SGE vault for trading on the SGE Main Board market.

The Shanghai Futures Exchange (SHFE) has approved 32 designated warehouses in China for delivery of gold for its gold futures contracts. These 32 warehouses are operated by the four large Chinese banks, namely, ICBC, CCB, Bank of China, and BoCom[36].

Other gold vaults in China

As part of the CSGE – SGE Gold Connect initiative, the Chinese Gold and Silver Exchange Society is building a precious metals vault in mainland China at Qianhai, in the Shenzhen region. See Hong Kong gold market for full coverage and the CSGE – SGE Gold Connect)

Commercial Vault Operators in Shanghai

Malca Amit recently opened a new precious metals vault in Shanghai’s FTZ[37]. Brinks has a substantial presence in China’s main gold hubs including China including Shanghai, Shenzhen, and Qingdao[38].

SGE International Collaboration

The SGE is increasingly engaging with other major global gold market participants in various collaborative efforts.

In July 2015, the London Bullion Market Association and the Shanghai Gold Exchange announced agreement on mutual recognition of the specifications for a 1 kilo gold bar of 9999 fineness[39][40].

In July 2015, the SGE and the Hong Kong based Chinese Gold & Silver Exchange (CGSE) Society launched the ‘Shanghai – Hong Kong Gold Connect’. After signing a Memorandum of Understanding in November 2014[41], the SGE announced in July 2015 that it would list bullion products on the CME trading platform[42], and allow CME members to trade SGE products. This has not yet happened. These listing plans include future reciprocal listing of gold contract products on both exchanges, so that SGE members will in future be able to trade CME listed gold products.

Reuters reported in June 2015 that the SGE has been in discussions with the Dubai Gold & Commodities Exchange on a linkup and the creation of “yuan-denominated” gold products listed on Dubai’S DGCX. While this Dubai development has not yet occurred, the DGCX did launch a cash-settled Yuan currency futures contract in late December 2016[43], which may be a precursor to a yuan-denominated gold product on the DGCX.

In 2015, Bank of China and ICBC joined the daily LBMA Gold Price auction as direct participants[44], although neither was a direct participant when the benchmark was launched in March 2015. In June 2015, ICBC also expressed interest in joining the auction [45], however it has not yet joined up.

This indirect link between the SGE and the London Gold Market through the LBMA Gold Price auction, and the presence of Chinese banks in a daily London gold benchmark auction process should be watched in terms of the SGE planned daily yuan gold fix, scheduled for April 2016. In June 2015, the SGE announced at a LBMA Bullion Market Forum in Shanghai that it planned to launch a “Yuan Gold Fix” in late 2015[46]. On 9 December 2015, the SGE was scheduled to reveal trading details of this Yuan gold fix at the 10th China Gold and Precious Metals Summit in shanghai[47], however, on 10 December 2015, Reuters reported that the launch would be delayed until April 2016[48]. The yuan gold fix launch is now scheduled for 19 April 2016[49].

From information revealed to date by the SGE, the SGE Yuan-denominated gold price benchmark is expected to be structured as follows:

- fix price for a 1kg contract of 9999 gold deliverable at SGE certified vaults

- most likely using the iAU99.99 contract specifications

- the 10 Chinese banks that are the first tier market makers in the recently launched interbank gold trading market are expected to be the initial participants in the fix

- fix process will last for a few minutes (3-5minutes) each day where participants trade against SGE as central counterparty and an equilibrium price is derived

- timing probably during SGE morning session at 11:30am so that the benchmark can be distributed in the Asian and Middle East region, or alternatively at 1:30pm at start of afternoon SGE session

In theory, this yuan gold fix should give the Chinese gold market more input into global gold price discovery, and is undoubtedly being pursued by Chinese as part of the Chinese Government’s long-term gold reactivation strategy.

Shanghai Futures Exchange (SHFE)

The Shanghai Futures Exchange(SHFE)[50] was formed in 1999 through the merger of three existing commodity exchanges, Shanghai Commodity Exchange, Shanghai Metal Exchange and Shanghai Cereals & Oils Exchange[51]. The SHFE is headquartered at 500 Pudian Road in Shanghai and is regulated by the China Securities Regulatory Commission (CSRC)[52]. As well as a gold futures contract, the SHFE lists futures on silver, futures on a series of base metals, and contracts on fuel oil and rubber. The SHFE has more than 200 members of SHFE, 80% of which are futures firms. A 2014 ranking of futures exchanges globally by the Futures Industry Association (FIA) put the SHFE as the world’s 9th most active futures exchange, with the SHFE’s 1kg gold futures contract ranked 2nd to that of the CME’s Comex 100oz gold futures contract[53].

There are 2 other active commodity exchanges in China, namely the Zhengzhou Commodity Exchange[54], and the Dalian Commodity Exchange[55], which both specialise in agricultural and base metal products, and neither of which lists any precious metals contracts.

SHFE Gold Futures Contract

The SHFE launched a gold futures contract in January 2008, after securing contract approval in September 2007. The contract size of 1kg was decided upon after consultation with the market[56][57]. The contract’s original trading hours were 9:00am – 11:30am and 1:30pm – 3:00pm. In July 2013, the SHFE also introduced night trading for the gold futures contract (as well as for its silver futures contract[58].Night trading hours, which the SHFE also calls ‘continuous trading’, spans 9pm until 2:30am the next morning.

The SHFE gold contract’s trading unit is 1kg, while its delivery unit is 3kgs of gold with minimum 99.95 fineness. The delivery unit of 3kgs is therefore comparable to that of the CME COMEX 100oz gold futures contract[59]. Delivery Regulations for the SHFE gold futures contract can be viewd on the Exchnage’s website[60]

Chinese Central Bank – Peoples Bank of China (PBoC)

China’s official gold reserves are held by the People’s Bank of China. The PBoC accumulates its gold reserves from domestic production, secondary domestic scrap sources, purchases in foreign markets, and other transacting in the domestic market. It is thought that the PBoC does not make widespread use of the Shanghai Gold Exchange.

Since 2001, the PBoC has announced the following increases in its official gold reserves:

2001: From 394 to 500 tonnes

2003: From 500 to 600 tonnes

2009: From 600 to 1,054 tonnes

July 2015: From 1,054 to 1,658 tonnes

August 2015: From 1,658 to 1,677 tonnes

From 2009 until July 2015, China’s official national gold reserve figure remained unchanged as the PBoC did not report any updates. From July 2015, the PBoC confirmed that it would now follow the SDDS international reserves reporting template and provide updated gold reserve data to the IMF on a regular basis. At this time, the PBoC also began to value its gold holdings at market value on its balance sheet. Since July 2015, the PBoC has reported monthly increases in its gold reserves each and every month, and added over 100 additional tonne to the August 2015 figure. As of February 2016, the PBoC officially holds over 1,778 tonnes of gold[61].

With the PBoC now announcing regular updates to its official gold holdings, on the surface this could be interpreted as the PBoC actually buying extra gold in the month before it makes the relevant announcement. However, this is not necessarily the case. The PBoC is not the only Chinese State entity authorised to hold gold within the PRC, and other entities such as SAFE, CIC, or even ICBC could theoretically also hold official Chinese gold, and then intermittently make gold transfers to the PBoC. Since these other entities do not publish their gold holdings, its impossible to know. What seems to be more discernible is that the PBoC does not source its gold from the SGE but buys using other routes such as on the international market. See BullionStar blogs “The London Float And PBOC Gold Purchases“, and “PBOC Gold Purchases: Separating Facts from Speculation” which discuss evidence of the PBoC buying gold in the London Gold Market.

China Gold Association and World Gold Council

The China Gold Association (CGA) was founded in 2001 by the then Chinese State Economic and Trade Commission and the Ministry of Civil Affairs. CGA members include gold exploration and production companies, gold refiners and investment companies. The main purpose of the CGA is to promote the development of the Chinese gold market, act as a liaison between the PRC and the industry, foster international cooperation, support scientific research, and promote gold consumption in China[62].

The miner-funded World Gold Council maintain offices in both Shanghai and Beijing. The Shanghai office is located at No. 1717 Nanjing West Road, Wheelock Square, in the Jing’an District, and the Beijing office is at 5/F China Life Tower, No. 16 Chaowai Street, in the Chaoyang District.

Gold Mining in China

China is now the world’s largest gold producing country, with (estimated) gold mine output in 2015 reaching 490 tonnes[63]. Although China hosts some large mining companies, the industry is still quite fragmented with over 600 mines nationwide[64].

China National Gold Group Corporation[65], usually known as China Gold or CNG, is China’s largest gold producing company. CNG is state-owned and state supervised and is a member of the World Gold Council[66]. CNG is essentially an integrated gold sector conglomerate consisting of various operations including Zhongjin Gold[67], Zhongjin Gold Jewellery, and China Gold International Resources Corporation[68].

Zhongjin Gold is the largest gold mining company in China and has the largest in-ground gold reserves of all Chinese mining companies. Zhongjin Gold Jewellery supplies gold to about 1,600 franchised gold jewellery stores throughout China that sell CNG branded gold bars and other gold investment products. CNG has a 39% stake in China Gold International which owns 2 mines in China. China Gold International is listed on the Toronto Stock Exchange and the Hong Kong Stock Exchange.

Other large Chinese gold mining companies include Zijin Mining Group[69], Shandong Gold Group[70], Zhaojin Mining[71], and Hunan Gold[72].

Gold Refineries in China

By any measurement, China has a large number of sizeable gold refineries relative to other countries. The identities of these refineries can be established by consulting a number of sources such as the approved gold refinery lists of the SHFE and SGE, as well as the London Bullion Market Association’s (LBMA) good delivery list for gold, and indeed the LBMA’s membership list.

The Shanghai Futures Exchange has approved a number of international and domestic refiners as acceptable delivery for its gold futures contract. The SHFE’s approved Chinese refiners are:

- Great Wall Gold & Silver Refinery of China, Chengdu

- Inner Mongolia Qiankun Gold & Silver Refinery Share Company, Huhhot

- Jiangxi Copper Company, Guixi City

- Zhongyuan Gold Smelter of Zhongjin Gold Corporation, Sanmenxia City [owned by China Gold Corp]

- Zijin Mining Group Company, Shanghang

‘Great Wall’ is the only Chinese gold refinery in the above lists that’s an Associate of the LBMA.

The full SHFE approved refiners list (both Chinese and foreign refiners can be seen on the SHFE website[73]

The current LBMA Good Delivery List for Gold also includes the above 5 SHFE approved refiners plus 4 additional Chinese gold refiners, namely:

- Shandong Zhaojin Gold and Silver Refinery Company, Zhaoyuan City

- Sichuan Tianze Precious Metals Company, Chengdu

- The Refinery of Shandong Gold Mining Company, Laizhou City

- Daye Nonferrous Metals Company, Huangshi City

According to the SGE, additional domestic gold refiners are expected to apply for Good Delivery accreditation from the LBMA[74]. The SGE has approved a vastly larger number of Chinese gold refineries as good delivery. The SGE’s full list is of both domestic refiners and non-Chinese refiners eligible to deliver gold (good delivery) to the Exchange. The full list of domestic gold refiners that have been accredited by the SGE can be viewed in the 2014 Goldbarsworldwide publication from Grendon International Research[75]. This list is taken from the 2013 Shanghai Gold Exchange annual report, and is divided into two specific lists, one with 35 refiners across the country that are accredited to deliver ‘Ingots’ (bars of weights 12.5 kg, 3 kg and 1 kg), and a subset list of 22 refiners (many of which are in the first list), that are accredited to deliver ‘Bars’ (bars of weights 100 g and 50 g).

Chinese Gold Coin Mints

The Chinese Gold Panda coin is produced by Shenzhen Guobao Mint, which is part of China Gold Coin Inc (CGCI)[76], which in turn is owned by the Chinese State. The Chinese Silver Panda is also produced by one of the divisions of CGCI.

Gold Imports into China

Only commercial banks with a PBoC gold import license are authorised to import gold into China. Currently, only 15 banks hold this licence, 12 of which are Chinese banks, and the remaining 3 are Chinese branches of foreign banks.

Until late 2013, 9 Chinese banks were authorised to import gold into China. In December 2013, HSBC and ANZ, as well as Chinese bank Everbright, also received gold import licences from the PbOC[77]. Standard Chartered was subsequently granted an import license in August 2014. Shanghai Pudong Development Bank and China Merchants Bank also received import licences at that time[78].

The full list of these 15 banks is as follows:

3 ‘Foreign’ Banks:

- HSBC Bank (China) Ltd

- Australian and New Zealand Bank (China) Company Ltd

- Standard Chartered Bank (China) Ltd

12 ‘Local’ Banks:

- Industrial and Commercial Bank of China (ICBC)

- China Construction Bank (CCB)

- Bank of Communications (BoCom)

- Bank of China

- Agricultural Bank of China

- Bank of Shanghai

- China Minsheng Bank (CMB)

- Industrial Bank

- Shenzhen Development Bank (SDB) / Ping An Bank

- Everbright

- Shanghai Pudong Development Bank

- China Merchants Bank

All gold imported into China has to be sold through the SGE. All gold imported into China for delivery to the International Board of the SGE must be from accredited refiners on the LBA Good Delivery List. All import deals have to be reported to the PBoC. Each time an authorised gold importer wants to import gold into China, the importer still requires pre-approval from the PBoC. This means that the PBoC is always aware of all planned and potential gold imports into China even before they have even occurred. Any other ‘foreign’ bank with gold to import into China has to use one of the above banks. The foreign bank is required to deposit the gold with the designated license holding bank, which will then handle the sale on the SGE.

One proxy for Chinese gold imports is non-monetary gold imports from Hong Kong, although China has been increasingly importing gold directly from other countries since 2014 (such as from the UK and Australia), so this proxy is not as complete as previously. Chinese ‘net imports’ from Hong Kong totalled 862 tonnes in 2015, up from 816 tonnes in 2014, but down from 1158 tonnes in 2013. This drop from 2013 is not surprising given that direct imports from countries rose.

For example, the UK exported 114 tonnes of non-monetary to China in 2014, and 173 tonnes in 2015, after literally zero exports from UK to China in 2013 or previously. See BullionStar blog “Record UK Gold Export To China In September, Chinese Gold Import Reaches 156t” from November 2015. Australia also exported 105 tonnes of gold directly to China in 2015. See BullionStar blog “Australia Gold Export To China In August A Record 13t” for further details. Switzerland also exported 290 tonnes of gold directly to China during 2015[79].That’s 568 tonnes of gold exports directly to China in 2015 from just 3 countries. Adding in Chinese gold imports from Hong Kong is another 800+ tonnes. Then there are Chinese gold imports from South Africa also. Rand Refinery is a supplier of gold directly to China, supplying one third of China’s gold imports. In 2013, Rand Refinery stated that:

“We are also currently exporting to China about a third of that country’s gold imports and have begun investing time and effort into developing relationships with the Chinese in terms of selling our products and sourcing material for refining“[80]

A small number of Chinese jewellery companies also hold a gold import license, but only for non-standard gold. In January 2016, the Chinese General Administration of Customs announced that from the beginning of 2016, the importation of gold for industrial purposes would no longer require a PBoC license[81].

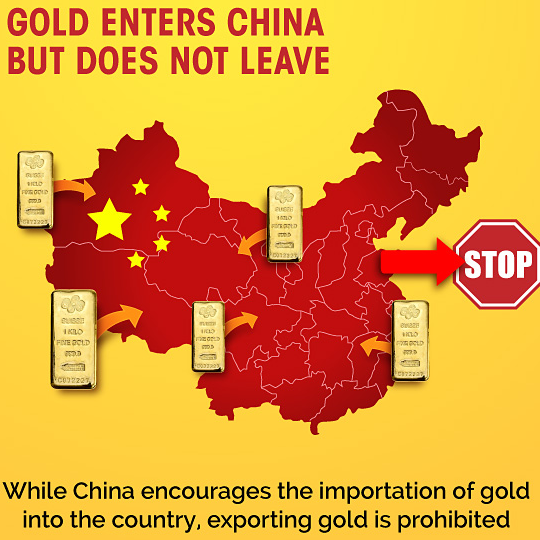

Gold Exports from China

Generally, exporting gold out of the Chinese gold market is prohibited, the main exceptions being processing trades from Free Trade Zones and exports such as Chinese gold coins.

Chinese Gold Demand

Chinese Jewellery sector

Shenzhen, located close to Hong Kong, is the centre of China’s gold jewellery manufacturing sector. The World Gold Council (WGC) and precious metals consultancy GFMS estimate that there are at least 4,000 manufacturers of gold jewellery in Shenzhen, and that the Shenzhen producers fabricated over 700 tonnes of gold jewellery in 2013, 85% of which was for the domestic Chinese market.

The WGC estimates that there are over 100,000 retail jewellery stores across China (see “understanding_chinas_gold_market report from the World Gold Council, July 2014) owned by a cross-section of entities from large groups, such as China National Gold Corp, to Hong Kong based jewellery companies such as Chow Tai Fook and also many smaller local operators. According to the World Gold Council, mainland Chinese gold jewellery demand totalled 807 tonnes in 2014. and 783.5 tonnes in 2015[82].

Chinese Investment gold demand

Thousands of Chinese bank branches and jewellers also stock investment grade small gold bars. These bars are 9999 fine, and include kilobars, through 100g and 50g weights down to very small 5g bars, and also bars produced in denominations of the traditional tael weight system. According to the World Gold Council, mainland Chinese investment gold bar (and coin) demand was 166 tonnes in 2014, and 201 tonnes in 2015.

Conclusion

In 1973-1974 Chinese Premier Zhou Enlai, via Vice Premier Chen Yun, commissioned the Bank of China to research various topics on foreign trade and the monetary system, and asked for answers to 10 questions, including details of the gold reserves of the US, Japan, the UK, West Germany, and France[83]. Three of the ten questions specifically relating to gold were as follows:

“How much are the foreign currency reserves and gold reserves [of these countries]?

What is current global annual gold output? What is the annual output of the main gold-producing countries?

Finance Minister Valery Giscard d’Estaing of France has advocated a linkage between currency and gold. Can we derive an approximate ratio between the total monetary flow and the total possession of gold in the world?”

That the Chinese premier asked such questions at that time should not be surprising since gold was beginning to experience its US orchestrated push out of the international monetary system. What should also not be surprising is that the Chinese play a very long game. Such pertinent Chinese questions in the early 1970s about the gold reserves of major competitor nations, and curiosity about the link between currency and gold, perhaps demonstrates that the PRC has always planned to take gold back into centre-stage of the international monetary system, and that what we are witnessing now with Chinese official (and county-wide) gold purchases, is but an implementation of a plan long decided upon in Beijing many years ago.

References and Links

1.^ China Gold Association, press release, 3 February 2016 http://www.cngold.org.cn/newsinfo.aspx?ID=1336

2.^ “The Silver clause in China”, Dickson H. Leavens, The American Economic Review, Vol. 26, No. 4 (Dec., 1936) http://www.jstor.org/stable/1807993?seq=3#page_scan_tab_contents

3.^ “The Growing and Evolving Gold Retail Investment Market in China“, Albert L.H. Cheng, World Gold Council, in the Alchemist, Issue 68, October 2012 http://www.lbma.org.uk/assets/blog/alchemist_articles/Alch68Cheng.pdf

4.^ “China’s gold market: progress and prospects“, Albert L.H. Cheng, World Gold Council, April 2014, http://www.gold.org/supply-and-demand/chinas-gold-market-progress-prospects

5.^ “Regulations on the control of gold and silver”, 15 June 1983, State Council of PRC http://www.asianlii.org/cn/legis/cen/laws/rotcogas425/

6.^ “Detailed rules for the implementation of the regulations on the control of gold and silver of the People’s Republic of China“, 1 January 1984, PBoC http://www.asianlii.org/cn/legis/cen/laws/drftiotrotcogasotproc1071

7.^ “The Liberalisation of the Gold Bullion Market in China“, speech by Roland Wang of the World Gold Council, during LBMA Indian Bullion Market Forum, January 2003 http://www.lbma.org.uk/assets/3b_wanglbmand2003.pdf

8.^ World Gold Council, “2000 China Gold Economic Forum release action plan to deregulate China’s gold market”, press release, 15 November 2000 https://www.gold.org/download/file/2756/151200a.pdf

9.^ China Gold Association, archived website from March 2002 http://web.archive.org/web/20020331114533/http://www.cngold.org.cn/

10.^ Central Huijin Investment Company http://www.huijin-inv.cn

11.^ State Administration of Foreign Exchange (SAFE) http://www.safe.gov.cn/en/

12.^ China Investment Corporation (CIC) http://www.china-inv.cn

13.^ ICBC History http://www.icbc-ltd.com/ICBCLtd/Investor%20Relations/IR%20Contacts%20and%20Services/FAQs

14.^ Bank of China History http://www.boc.cn/en/aboutboc/ab1/200808/t20080814_1601747.html

15.^ China Construction Bank History http://www.ccb.com/en/investor/history.html

16.^ Agricultural Bank of China (ABC) history http://www.abchina.com/en/about-us/about-abc/Overview

17.^ Bank of Communications (BoCom) history http://www.bankcomm.com.hk/en/aboutus/bankprofile.html

18.^ Shanghai Gold Exchange: http://www.en.sge.com.cn

19.^ “Shanghai Opens Gold Exchange for Trading“, China.org.cn, October 2002 http://china.org.cn/english/2002/Oct/47277.htm

20.^ “Guide of Shanghai Gold Exchange – International Business”, SGE, July 2015 http://www.en.sge.com.cn/upload/resources/file/2015/07/21/30123.pdf

21.^ HSBC among first foreign banks to join SGE and SGEI http://www.about.hsbc.com.cn/~/media/china/en/news-and-media/news20140918-en.pdf

22.^ China (Shanghai) Pilot Free Trade Zone: http://en.china-shftz.gov.cn

23.^ “Shanghai free-trade zone struggles for relevance”, Financial Times, 27 September 2015 http://www.ft.com/intl/cms/s/0/8cec0faa-6364-11e5-9846-de406ccb37f2.html#axzz41qnirC9z

24.^ Shanghai International Gold Exchange: http://www.en.sge.com.cn/about-us/sge-overview/sgei-intro

25.^ “Shanghai Gold Exchange International Board Successfully Put into Operation”, SGE press release, September 2014 http://web.archive.org/web/20140923043504/http://www.en.sge.com.cn/news-announcement/news/520477.shtml

26.^ SGE Price Matching products http://www.en.sge.com.cn/products/price-matching-products/t0-products/product-list/

27.^ SGE Rules http://www.en.sge.com.cn/rules-regulations/rules/sgerules/

28.^ “China launches interbank gold trading system”, CCTV.com, January 2016 http://english.cntv.cn/2016/01/13/VIDECIyZTNdLnmCfXrduywEf160113.shtml

29.^ SGEI Introduction, September 2014 http://www.en.sge.com.cn/about-us/sge-overview/sgei-intro

30.^ SGEI account set up procedures http://web.archive.org/web/20160914021507/http://www.en.sge.com.cn/account-opening/account-opening-guide/517989.shtml

31.^ “Announcement of the Shanghai Gold Exchange on Establishing the International Board Certified Vault” SGE press release, September 2014 http://web.archive.org/web/20160507095255/http://www.en.sge.com.cn/news-announcement/announcement/520051.shtml

32.^ SGEI, BOCOM vault location http://www.en.sge.com.cn/upload/resources/file/2014/09/18/28855.xlsx

33.^ “Announcement of SGE on Appointment of the Customs Clearance Company for SGE’s International Board”, SGE press release, 17 September 2014 http://www.en.sge.com.cn/news-announcement/announcement/520047.shtml

34.^ “Announcement on the Transportation Company for the International Board of the Shanghai Gold Exchange” SGE press release, 8 October 2015 http://www.en.sge.com.cn/news-announcement/announcement/530162.shtml

35.^ G4S International Logistics appointed approved service provider to SGE and BoCOM http://www.g4s.com/en/Media%20Centre/News/2015/09/24/G4Si%20Shanghai%20Gold%20Exchange/

36.^ Shanghai Futures Exchange designated delivery warehouses for gold futures contracts http://www.shfe.com.cn/upload/dir_20111216/89100_20111216.htm

37.^ Malca-Amit http://www.malca-amit.com/shanghai.html

38.^ Brinks China http://www.brinks.com.hk/china01.html

39.^ LBMA and SGE endorse a “9999 Kilobar Standard” http://www.lbma.org.uk/_blog/lbma_media_centre/post/9999-kilobar-standard-endorsed-by-lbma-sge

40.^ Specifications of the LBMA/SGE mutually recognised 9999 Kilobar http://www.lbma.org.uk/assets/Press%20Releases/9999%20Kilobar%20Standard.pdf

41.^ Memorandum of Understanding between SGE and the US CME Group announced November 2014 http://web.archive.org/web/20160816002235/http://www.en.sge.com.cn/news-announcement/news/522596.shtml

42.^ “Shanghai Gold Exchange in talks to list products on CME”, Reuters, June 2015 http://www.reuters.com/article/us-gold-china-sge-idUSKBN0P610220150626

43.^ “Introduction to Chinese Yuan Futures Cash Settled Contracts”, DGCX annoucemen, 30 November 2015 http://www.dgcx.ae/index.php/en/notices/item/download/501_2194b76ce4e10b92289ca8fcdd42fd1f

44.^ LBMA Gold Price – direct participants list http://www.theice.com/iba/lbma-gold-price#participants

45.^ “China’s ICBC says keen on joining London gold price benchmark”, Reuters, June 2015 http://www.reuters.com/article/china-gold-icbc-idUSL3N0ZB1X320150625

46.^ “China likely to get central bank nod for yuan gold fix soon”, Reuters, June 2015, http://www.reuters.com/article/china-goldconference-yuanfix-idUSL3N0ZB1AD20150625

47.^ China Gold Summit, December 2015 http://www.chinagoldsummit.com

48.^ “China to launch yuan gold benchmark in April: Sources”. Reuters via Economic Times of India, 10 December 2015 http://economictimes.indiatimes.com/news/economy/policy/china-to-launch-yuan-gold-benchmark-in-april-sources/articleshow/50122460.cms

49.^ “China plans to launch yuan-denominated gold fix on April 19 – sources”, FastMarkets, 25 Frbruary 2016 http://www.fastmarkets.com/asia/update-china-plans-to-launch-yuan-denominated-gold-fix-april-19-sources-109581

50.^ Shanghai Futures Exchange(SHFE) http://www.shfe.com.cn/en

51.^ History of Shanghai Futures Exchange, archived site page, September 2000 http://web.archive.org/web/20000926030445/http://www.shfe.com.cn/english/pr03.html

52.^ China Securities Regulatory Commission (CSRC) http://www.csrc.gov.cn/pub/csrc_en/

53.^ Futures Industry Association, Exchange Rankings, 2014, page https://fimag.fia.org/sites/default/files/content_attachments/2014%20FIA%20Annual%20Volume%20Survey%20%E2%80%93%20Charts%20and%20Tables.pdf

54.^ http://english.czce.com.cn/

55.^ Dalian Commodity Exchange http://www.dce.com.cn

56.^ SHFE Circular on launch of gold futures trading, 2 January 2008 http://web.archive.org/web/20080104023706/http://www.shfe.com.cn/docview.jsp?docid=80221

57.^ “Stellar launch for Chine Gold as more commodities planned”, Futures and Options World, January 2008 http://www.fow.com/1852773/Stellar-launch-for-China-gold-as-more-commodities-planned.html

58.^ SHFE opens Night Trade of Gold and Silver Futures, July 2013. http://www.shfe.com.cn/en/AnnouncementandNews/SHFENews/911318955.html

59.^ SHFE gold futures contract delivery specifications http://www.shfe.com.cn/en/products/Gold/contract/11116494.html

60.^ SHFE Gold Futures Delivery Regulations http://www.shfe.com.cn/en/products/Gold/regulation/591.html

61.^ “China adds 15.98 MT of gold to Reserves in January”, Platts, February 2016 http://www.platts.com/latest-news/metals/london/china-adds-1598-mt-of-gold-to-reserves-in-january-26363146

62.^ About the China Gold Association (in Chinese) http://www.cngold.org.cn/about.aspx

63.^ USGS Gold Survey 2016, estimates by country http://minerals.usgs.gov/minerals/pubs/commodity/gold/mcs-2016-gold.pdf

64.^ “The History and Economics of Gold Mining in China”, Ore Geology Reviews, March 2014, http://www.researchgate.net/profile/M_Santosh/publication/266476559_The_history_and_economics_of_gold_mining_in_China/links/00b7d533ebf780eb51000000.pdf

65.^ China national Gold Group Corporation http://www.chinagoldgroup.com/eng/index.html

66.^ World Gold Council members list http://www.gold.org/about-us/our-members

67.^ Zhongjin Gold http://www.zjgold.com

68.^ China Gold International Resources Corp http://www.chinagoldintl.com

69.^ Zijin Mining Group http://www.zijinmining.com/about/About-Us.htm

70.^ Shandong Gold Group http://en.sd-gold.com

71.^ Zhaojin Mining http://en.zhaojin.com.cn/

72.^ Hunan Gold http://en.hjdmi.com/

73.^ SHFE approved refiners list http://www.shfe.com.cn/upload/dir_20111216/25836_20111216.htm

74.^ Shanghai Gold Exchange – A Responsible Gold Market, LBMA Bullion MArket Forum, Shanghai, June 2015 http://www.lbma.org.uk/assets/events/BMF2015/lila1.pdf

75.^ Shanghai Good Delivery Gold Ingots and Bars, domestic refiners lists, pages 6-7 http://www.goldbarsworldwide.com/PDF/BG_11_Shanghai_Good_Delivery.pdf

76.^ China Gold Coin Inc (CGCI) (In Chinese) http://www.chinagoldcoin.net/index.html

77.^ “China grants gold import licenses to foreign banks for first time: sources”, Reuters, January 2014 http://www.reuters.com/article/us-chinagold-banks-idUSBREA0E08N20140115

78.^ “China allows 3 more banks including StanChart to import gold -sources”, Reuters, August 2014 http://uk.reuters.com/article/uk-gold-china-imports-idUKKBN0GJ0IS20140819

79.^ Sharelynx.com http://www.sharelynx.com

80.^ Rand refinery, 2012 Annual Report, page 46, Chairman’s review https://web.archive.org/web/20130423131717/http://www.randrefinery.com/brochures/Rand%20Refinery%20Integrated%20Annual%20Report%202012.pdf

81.^ “China to remove gold import license for industrial purposes-customs”, Reuters, January 2016 http://af.reuters.com/article/commoditiesNews/idAFB9N14P03720160107

82.^ “Gold Demand Trends – Full Year 2015”, World Gold Council, February 2016 http://www.gold.org/download/file/4815/GDT_Q4_2015.pdf

83.^ Chinese Premier Zhou Enlai commissioning research into gold reserves of US, Japan, UK, FR Germany, France, 1973-74, “Punctual Delivery of Ten Research Topics Assigned by Vice Premier Chen Yun (1973)” http://www.boc.cn/en/aboutboc/ab7/200809/t20080926_1601853.html

Subscribe to Gold University Articles

Copyright Information: BullionStar permits you to copy and publicize articles or information from the BullionStar Gold University provided that a link to the article's URL or to https://bullionstar.com is included in your introduction of the article or blog post together with the name BullionStar. The link must be target="_blank" without re="nofollow". All other rights are reserved. BullionStar reserves the right to withdraw the permission to copy content for any or all websites at any time.