Australia Confirms Our Analysis On Gold Exports to China

Koos Jansen

Koos JansenSince 2015 I’ve stated the raw data published by the Australian Bureau of Statistics (ABS) on gold export to China mainland do not accurately reflect what is imported by China from the land of down under. In my previous post I’ve written Australia’s gold “export to China” should be adjusted by Hong Kong’s gold “import from Australia” as a substantial amount of gold Australia declares to export to China is in fact travelling through Hong Kong. A written statement from ABS now supports this analysis.

Obviously, what we’re after is exactly how much (non-monetary) gold China is importing from all countries around the world. As China doesn’t disclose its cross-border trade statistics for gold, the only way to reach our objective is by establishing net gold export from all countries around the world to China, subsequently to aggregate these numbers and come to an estimate of total Chinese gold import.

One of the largest exporters of gold to China is Australia, but calculating Australia’s gold export to China is complicated, as we need to be cautious to avoid double counting in computing China’s total net gold import. The thing is, ABS bluntly alters any “export to Hong Kong” into “export to China” when they suspect the gold is shipped to Hong Kong but will reach the mainland as its final destination – this is what ABS confirmed to me. Therefor, from using Australia’s “export to China” double counting can arise when any gold flowing from Australia via Hong Kong to China would then be declared as “export to China” by Australia and “export to China” by Hong Kong.

Let us clarify this subject. Have a look at the chart below. If we focus on the period from January 2013 until December 2014 we can observe that Australia’s “export to China” (purple bars, data sourced via ABS/COMTRADE) roughly matches Hong Kong’s “import from Australia” (turquoise bars, data sourced from the Hong Kong Census and Statistics Department). We must conclude that over this period roughly all gold Australia exported to China was transferred via Hong Kong. If we then would sum up Australia’s gold “export to China” to Hong Kong’s gold “export to China” this would result in double counting.

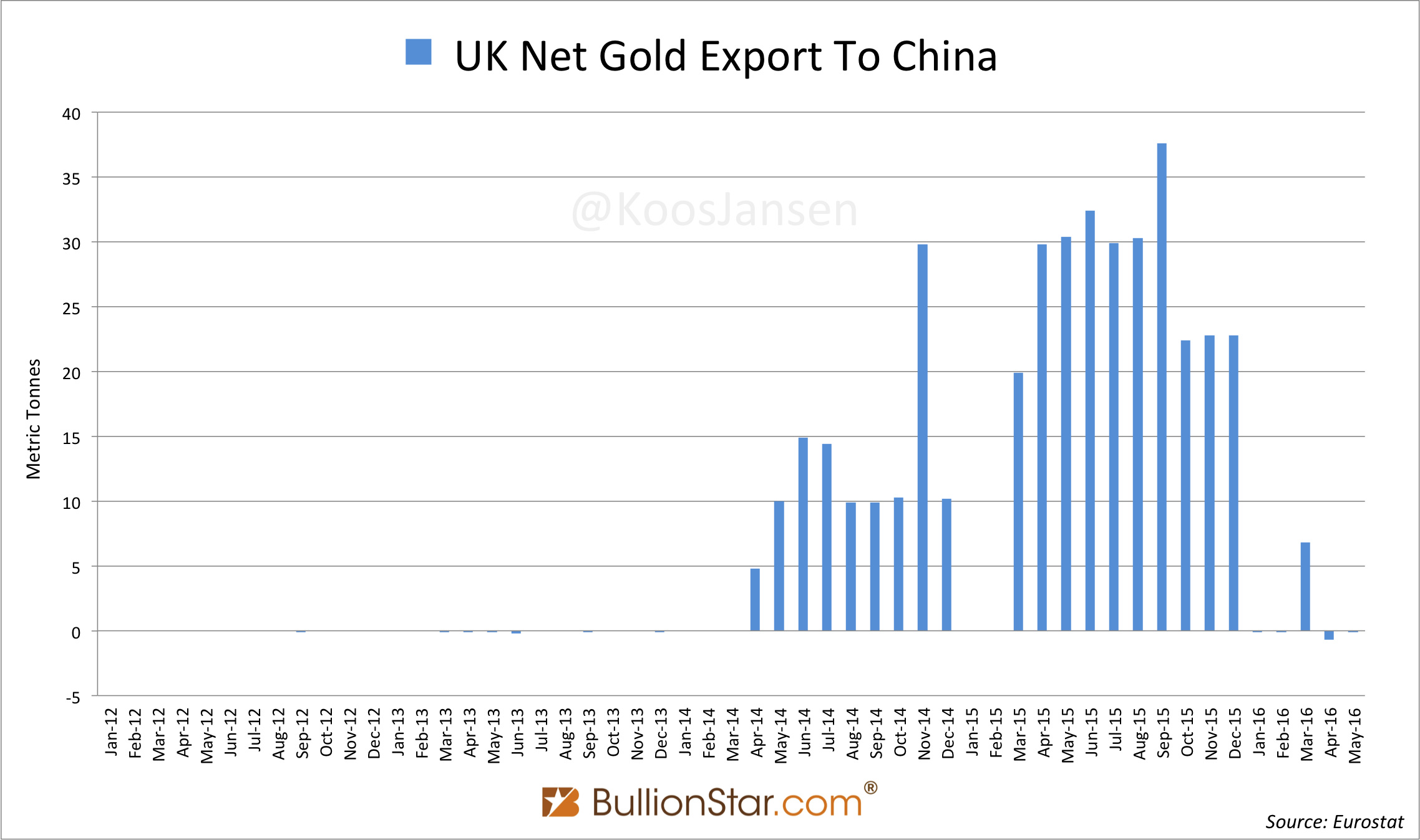

Historically, Hong Kong has been the main entry point for gold into China. Not surprisingly Australia’s gold “export to China” was all directed through Hong Kong until December 2014, as we can see above. The situation changed early 2014 when China openly stated to stimulate direct gold imports from all over the world, bypassing Hong Kong. Soon after, we’ve witnessed the birth of direct gold export to China from for example the UK.

The strategic move from Beijing to stimulate direct import was also mentioned on Chinese state television channel CCTV in 2014, see the clip below starting from 1:30.

Exhibit 3. Courtesy CCTV.

Tellingly, what Australia declared as “export to China” started to exceed what Hong Kong declared as “import from Australia” (exhibit 1) in early 2015. The difference reflects Australia’s direct export to China, which took off in January 2015. To compute Australia’s direct export to China we should subtract Hong Kong’s “import from Australia” from what Australia declares as “export to China”.

When I wrote ABS about my general findings displayed in exhibit 1 they replied [emphasize en brackets by me]:

… I can confirm that we are reporting basically as you described.

The ABS developed a policy some time ago in relation to reporting country of origin [final destination] for gold exports. The policy dictates that some trade with a reported country of destination as Hong Kong, should be corrected to China. This was based on our investigations at the time, which found that although Hong Kong is a central hub for gold trade, the goods are predominately sent elsewhere in the Asia/Pacific region. We also confirmed that in some cases the destination beyond Hong Kong was not known by the exporter at the time of export. China was assessed as the most likely destination …. We acknowledge that this blanket approach is not ideal, and can lead to the series differing from expectations.

We will continue to report in this fashion in the foreseeable future. However, as some time has passed since the initial investigation we will be conducting a review of the policy discussed above. We will be sure to inform you of any outcomes resulting from the review process.

Exhibit 4. Quote from email of the Australian Bureau of Statistics (ABS) to Koos Jansen.

Case closed? No, I have a few more thoughts I would like to share.

To come to the most precise amount of bullion net exported from Australia to China mainland we should set up a formula. We have a few flows of bullion between Australia, Hong Kong and China to work with. Some are known and publicly disclosed, some are unknown but can be calculated:

- We have publicly disclosed by ABS/COMTRADE what Australia declares as net “export to China” (C).

- Effectively, what ABS declares as net “export to China” (C) either is a direct net export to China (Y) or exported to Hong Kong but disclosed by ABS as export to China (X) as they guess the final destination is the mainland (so C = X + Y). What we want to know is the partition of Y and X, but this is unknown.

- Then we have also publicly disclosed by ABS/COMTRADE what they consider Australia to net “export to Hong Kong” as a final destination (B). This amount is small but relevant for our formula. (Actually, for us it is not important what ABS thinks the final destination is, as long as we know this gold is arriving in Hong Kong.)

- Finally, we have publicly disclosed by the Hong Kong Census and Statistics Department (HKCSD) Hong Kong’s net “import from Australia” (Z).

What we want to calculate is Y (Australia’s direct net gold “export to China"), but the only figures published are C and B by ABS, and Z by HKCSD. Fortunately, we can calculate Y from C, B and Z.

We know Hong Kong’s “import from Australia” (Z) equals Australia’s “export to Hong Kong” (B) plus Australia’s export to Hong Kong data that is altered into “export to China” (X). ABS may alter the data but nevertheless the physical gold flows to Hong Kong. Therefor:

Z = B + X

As Z and B are publicly disclosed, from here we can calculate the amount ABS alters from “export to Hong Kong” into “export to China”, which is X.

X = Z – B

By knowing X we can finally calculate how much gold is directly net exported from Australia to China (Y).

C = Y + X

Y = C – X

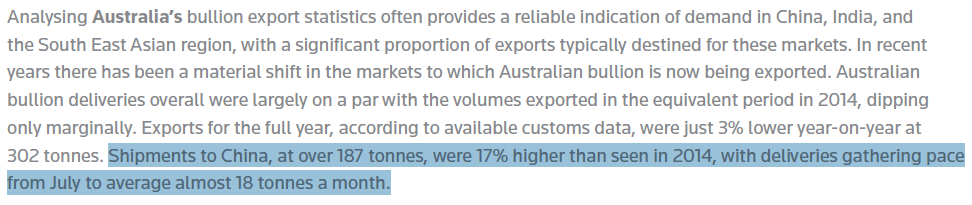

By using this formula Australia net exported 124 tonnes of gold to China mainland in 2015. In contrast, GFMS that wrote in their Gold Survey 2016 Australia exported 187 tonnes to China in 2015, which is the raw data disclosed by ABS (Australia’s gross gold “export to China”). The numbers by GFMS cannot de accurate.

One final point. How do we know the gold exports from Australia to Hong Kong are re-exported to China mainland and not for example to Thailand?

Re-exports are products which have previously been imported into Hong Kong and which are re-exported without having undergone in Hong Kong a manufacturing process which has changed permanently the shape, nature, form or utility of the product.

Exhibit 6. Definition of re-exports by HKCSD.

Well, next to the fact ABS isn’t always sure what the final destination is of gold exported to Hong Kong, neither do I. But, once the gold has arrived in Hong Kong we shouldn’t care about ABS data, we must rely on HKCSD’s data. The HKCSD states Hong Kong to re-export hundreds if not thousands of tonnes of gold per year – Hong Kong is one the largest gold trading hubs globally. Therefor, I assume they accurately declare how much imported gold is re-exported. If the HKCSD declares so many re-exports why wouldn’t they accurately declare re-exports from Australia to the mainland?

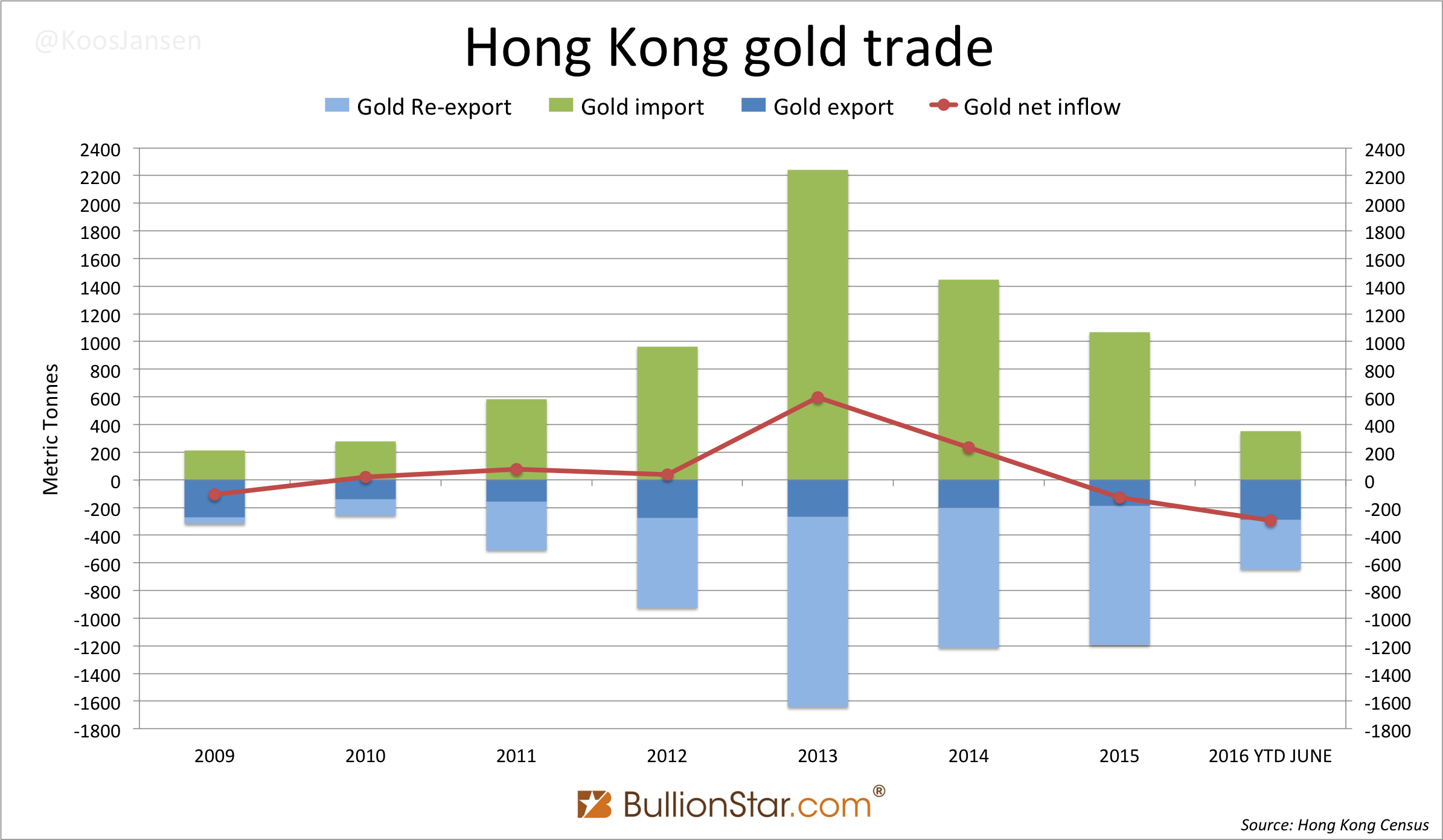

Eventually, by calculating Australia’s direct net gold “export to China" (Y) through the formula above, and adding Hong Kong’s “export and re-export to China" from HKCSD data we should have the best assessment of China’s net gold import from Australia and Hong Kong.

My assessment for China’s total net gold import for 2015 is 1,575 tonnes. If we add domestic mine output at 450 tonnes and a few hundred tonnes of scrap supply and disinvestment, total supply has been well over 2,000 tonnes for the year. Not surprisingly SGE withdrawals accounted for 2,596 tonnes in 2015.

I know, I owe you all a respons to the Gold Survey 2016 by GFMS in which they stated Chinese gold demand in 2015 was 867 tonnes – quite a gap with SGE withdrawals. As some of you know, or might have guessed by now, I’ve had some health issues in recent years hence my writing hasn’t been constant. Hopefully, things are turning for the better again and I can continue publishing on the Chinese gold market (my ongoing disagreement with WGC and GFMS), global gold flows and a whole bunch of other planned articles.

Popular Blog Posts by Koos Jansen

China’s Secret Gold Supplier is Singapore

China’s Secret Gold Supplier is Singapore

Audits of U.S. Monetary Gold Severely Lack Credibility

Audits of U.S. Monetary Gold Severely Lack Credibility

China Gold Import Jan-Sep 797t. Who’s Supplying?

China Gold Import Jan-Sep 797t. Who’s Supplying?

The Gold-Backed-Oil-Yuan Futures Contract Myth

The Gold-Backed-Oil-Yuan Futures Contract Myth

Estimated Chinese Gold Reserves Surpass 20,000t

Estimated Chinese Gold Reserves Surpass 20,000t

PBOC Gold Purchases: Separating Facts from Speculation

PBOC Gold Purchases: Separating Facts from Speculation

U.S. Mint Releases New Fort Knox Audit Documentation

U.S. Mint Releases New Fort Knox Audit Documentation

China Net Imported 1,300t of Gold in 2016

China Net Imported 1,300t of Gold in 2016

Why SGE Withdrawals Equal Chinese Gold Demand and Why Not

Why SGE Withdrawals Equal Chinese Gold Demand and Why Not