Chinese Banks' Huge Precious Metals Holdings Explained

Koos Jansen

Koos JansenThis post is part of the Chinese Gold Market Essentials series. Click here to go to an overview of all Chinese Gold Market Essentials for a comprehensive understanding of the largest physical gold market globally. This post was updated late 2017.

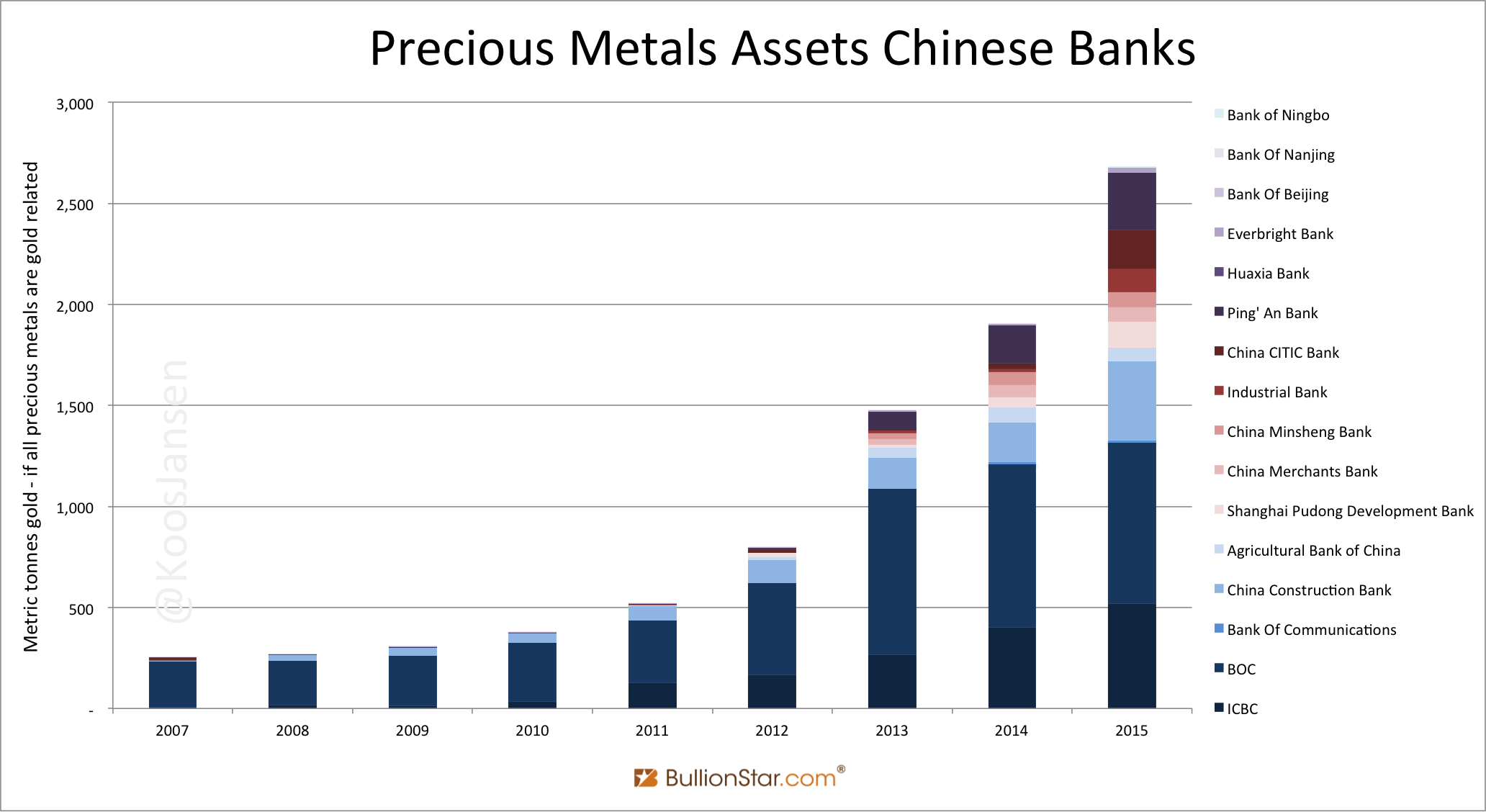

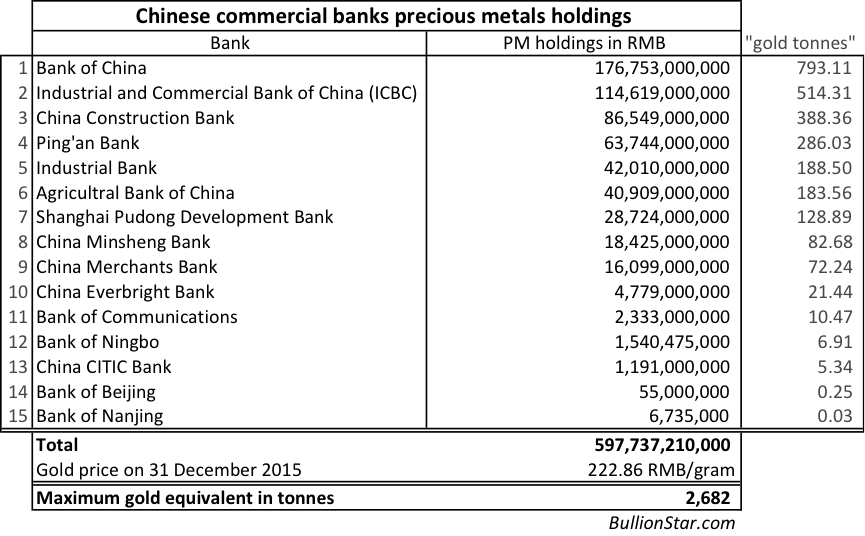

There has been much conjecture since 2014 about the increasing numbers in the “precious metals” category on the balance sheets of Chinese commercial banks. By the end of 2015 China’s largest banks were holding RMB 598 billion in precious metals, which translates into approximately 2,682 tonnes of gold – if all the precious metals were gold related, which is very likely.

Some analysts think that the precious metals on Chinese commercial bank balance sheets are gold reserves purchased on behalf of the Chinese central bank (I don’t agree), while others surmise that Chinese banks buy gold at the Shanghai Gold Exchange (SGE) and then lend it out, so the precious metals on the balance sheets solely represent leased gold. In the latter analysis it’s then assumed the leasing inflates the amount of gold withdrawn from SGE designated vaults. Most certainly there is leased gold on Chinese banks’ balance sheets, but this can hardly influence SGE withdrawals, as I have previously explained.

What do we know beyond the gossip about the precious metals holdings on Chinese commercial bank balance sheets?

From studying the annual reports of the respective banks and additional documentation we know the precious metals can be the following things:

- Gold savings that belong to the banks’ customers (GAP)

- Gold inventory for the banks’ retail gold business

- Gold held for hedging purposes

- Gold held outside China

- Back- to-back gold leasing

- Synthetic leases – in other words: swaps

Since the Chinese silver market was liberalized much earlier than gold I don’t think there is any edge for Chinese commercial banks to have a predominant role in the silver market. So, probably most of the precious metals on the balance sheets in question are gold related.

Below is an overview of the precious metals holdings of listed Chinese commercial banks as of 31 December 2015, measured in yuan (RMB). There are 16 listed Chinese commercial banks on China’s A-share market but Huaxia Bank didn’t disclose its precious metals holding in its annual report. If all aggregated precious metals holdings relate to gold, the upper bound is approximately 2,682 tonnes of gold.

1. Customers’ Gold Savings (GAP)

A substantial amount of the precious metals reflect (fully backed) customers’ gold deposits in the form of Gold Accumulation Plans (GAP), recorded as an asset and a liability on the balance sheets of the banks. However, to me it’s unknown how much gold is exactly accumulated in China through GAPs.

Let’s go through the annual reports of the Chinese banks having the largest precious metals holdings, seeking for information with respect to GAPs.

According to the 2015 annual report of Bank of China (BOC):

Precious metals comprise gold, silver and other precious metals. The Group retains all risks and rewards of ownership related to precious metals deposited with the Group as precious metals deposits, … and it records the precious metals received as an asset. A liability to return the amount of precious metals deposited is also recognized.

From the BOC website its GAP seems to be in its infancy, so I don’t expect it to comprise much gold. ICBC on the other hand, introduced a GAP in 2010 and is thought to be largest in China.

From reading ICBC’s 2015 annual report [brackets added by me]:

Seizing the opportunities arising from customers’ wealth increase and capital market growth, the Bank made efforts to establish a mega asset management business system across the whole value chain and enhance its specialized operating capabilities on the strength of the Group’s asset management, custody, pension and precious metal businesses, …

The [ICBC] Group records the precious metals received as an asset. A liability to return the amount of precious metals deposited is also recognized. …

On ICBC’s website we read:

统计显示,截至2014年末,工行积存金的业务规模已超过250吨,同比增长超过150%,积存客户数量已超过100万户。

According to statistics, by the end of 2014, the business size of ICBC’s GAP was more than 250 tonnes, a 150% YOY increase. GAP clients are more than 1 million.

Note, the 250 tonnes disclosed on ICBC’s website represents GAP turnover and not total holdings. The latter is unknown.

In the 2015 annual report by China Construction Bank (CCB):

While consolidating our traditionally advantageous businesses in housing finance and cost advisory service among other things, we actively expanded our presence in … precious metals.

The Bank supported product innovation, provided and optimized new products such as … gold purchase and saving.

The Bank proactively responded to changes in the precious metals market via pursuing marketing expansion, enlarging customer base and enforcing product innovation. The Bank launched innovative products and business models, including gold accumulation plan ….

To me it’s unknown how much gold CCB’s GAP comprises.

All in all, part of the precious metals on the listed Chinese commercial banks’ balance sheets are gold savings held on behalf of clients instead of reflecting the banks own metals. (By the way, gold saved in ICBC’s GAP is partly stored in SGE designated vaults.)

2. Bank Retail Gold Inventory

Chinese banks offer a wide range of retail gold investment products for sale at local branches and through internet order. Naturally, any gold inventory for this business is recorded on the balance sheets. From ICBC’s 2015 annual report:

To echo the changes in market demands, the Bank developed a variety of new brands on assorted themes and introduced a slew of products, e.g. Chinese Zodiac Coins and Panda Gold and Silver Coins, under agent sales. The Bank expanded the online channels, through which the flagship store “ICBC Gold Manager” witnessed substantial growth of sales, and it also piloted the direct distribution of logistics suiting to the characteristics of e-commerce.

According to the World Gold Council roughly 60 % of Chinese retail gold investment demand is supplied through commercial banks. Consequently, Chinese banks’ own gold inventory for retail business (showing up on their balance sheets) can not be neglectable.

Additionally, the gold inventory in the vaults of the SGE does not appear on the Chinese custodian bank balance sheets (unless it’s part of GAP gold).

3. Hedging

China’s commercial banks offer derivatives to retail and institutional customers. Bank of China’s Qi Jin Bao is an example. Qi Jin Bao is in fact gold option business. The retail customer pays a certain amount of money (option premium) and buys a gold call option or put option.

For example (simplified): suppose the current gold price is $1300/oz and a retail customer is bullish on gold and believes that the gold price will rise in 3 months time. Therefore, the retail customer buys a 3 months call option with a notional amount of 100 oz of gold at the strike price of $1300/oz from Bank of China and pays an option premium of $35/oz. If the gold price indeed goes up in 3 month’s time, the retail customer will make money. However, derivatives are a zero-sum game. If the retail customer makes money, then the Bank of China definitely loses money. If the gold price goes up to $2000/oz, Bank of China will lose big time. In order to mitigate this risk, Bank of China will (borrow money to) buy gold to hedge the short call position and the gold purchased will appear on the balance sheet.

4. Gold Held Outside China

Gold on the balance sheets of Chinese commercial banks doesn’t necessarily have to be gold held in China. Chinese banks like ICBC, BOC and Bank of Communications have direct access to the LBMA. As a result, gold on the balance sheets of Chinese commercial banks can be located outside China mainland.

On January 29, 2014, ICBC bought 60 % of the existing shares in Standard Bank Plc from Standard Bank London Holdings Limited. After completion of the acquisition, Standard Bank Plc was renamed as ICBC Standard Bank on 27 March 2015. In the 2015 annual report of ICBC (Group), which includes ICBC Standard Bank data, we see that ICBC Standard Bank held RMB 18,426,000,000 in precious metals assets (equivalent to 83 tonnes of gold) on December 31, 2015.

As ICBC Standard Bank can be seen as the international gold arm of its group – ICBC Standard Bank is a London Bullion Market Association market maker for spot trading and a clearing member of London Precious Metal Clearing Limited (LPMCL) – we may assume any precious metals assets of ICBC Standard Bank are not located in China mainland.

In the chapter “Some Of Chinese Banks’ Gold Is Indeed Outside China" of this post we can read that also smaller banks like Ping’ An are likely to hold gold outside of China.

5. Back-to back Gold Leasing

Probably the largest share of the precious metals on the balance sheets have to do with gold leasing. At the moment, there are no standard accounting rules or guidelines related to how to record bank’s gold leasing activities. (In this post, I don’t distinguish between gold leasing and gold lending because the essence is the same.) However, most banks seem to still put gold leasing activity in the precious metals category of their balance sheet.

If you have little knowledge on accounting rules please read this crash course before continuing.

According to the A-share annual report of the Bank of Communications [brackets added by me]:

与本集团交易活动无关的贵金属包括经营章币销售等按照取得时的成本进行初始计量,以成本与可变现净值两者的较低者进行后续计量。与本集团交易活动有关的贵金属包括贵金属租赁、拆借等按照公允价值进行初始计量和后续计量,重新计量所产生的公允价值变动直接计入当期损益。

Precious metals that are not related to the Group’s trading activities including coins and medallions sales are initially measured at acquisition cost and subsequently measured at the lower of cost and net realizable value. Precious metals that are related to the Group’s trading activities including precious metals lease and [precious metals] interbank lending are initially and subsequently recognized at fair value, with changes in fair value arising from re-measurement recognized directly in profit or loss in the period in which they arise.

Apparently, the Bank Of Communications has its gold leasing business disclosed on its balance sheet in the precious metals category.

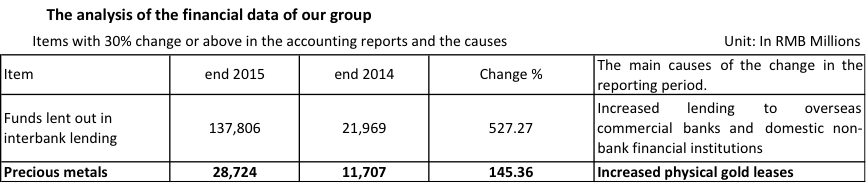

Below is from the 2015 annual report of Shanghai Pudong Development Bank (page 17):

Translated:

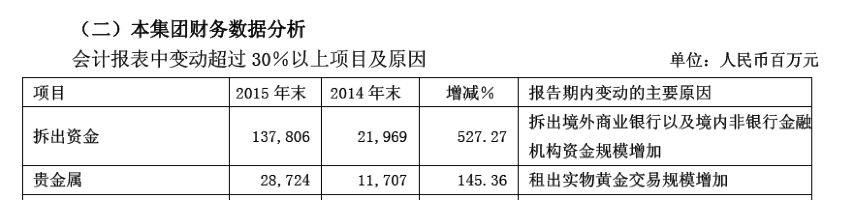

Shanghai Pudong Development Bank saw its precious metals holdings grow from RMB 11,707,000,000 on December 31, 2014, to RMB 28,724,000,000 on December 31, 2015. As the main cause for the growth in precious metals is considered to be “increased physical gold leases", we must conclude in the case of Shanghai Pudong Development Bank nearly all precious metals on its balance sheet relate to gold leasing. But does this mean Chinese banks buy gold on the SGE and then lease it out? Not necessarily.

Chinese banks mainly do back-to-back gold leasing – simply connecting supply and demand. Banks don’t have much money of their own. They need to borrow money or gold either from savers or in the interbank market. Would it make sense for banks to borrow money in order to buy gold to subsequently lend out gold? Or would it be more logic for banks to borrow gold to subsequently lend out gold (striking a small fee)?

From a source who worked at the precious metals trading desk at ICBC in 2014 I was told first hand ICBC has little gold of itself for leasing, most of the gold lend out is borrowed from third parties. These third parties are mostly SGE members or overseas banks that lend gold through the Chinese OTC market. (By the way, all commercial bank gold leasing is settled through the SGE system.)

ICBC operates in the lease market as an intermediary by connecting supply (lessors) and demand (lessees), while striking a fee. ICBC can borrow gold from international banks or local gold owners with an SGE Bullion Account, and lend the gold to miners, jewelers or speculators. My assumption is that the international gold lease rate is lower than the Chinese gold lease rate, which attracts gold from the international market into the Chinese domestic gold market. (Whenever a gold loan is to be repaid from the Chinese domestic gold market to an international lender, not the physical metal is exported, but funds cross the Chinese border, as physical gold export is prohibited from the Chinese domestic gold market.)

Also note, if banks would buy the gold to lend out, they are exposed to the price risk of gold. In order to cover this risk, banks need to hedge but this will involve additional costs. The logical solution is for banks to do back-to-back gold leasing.

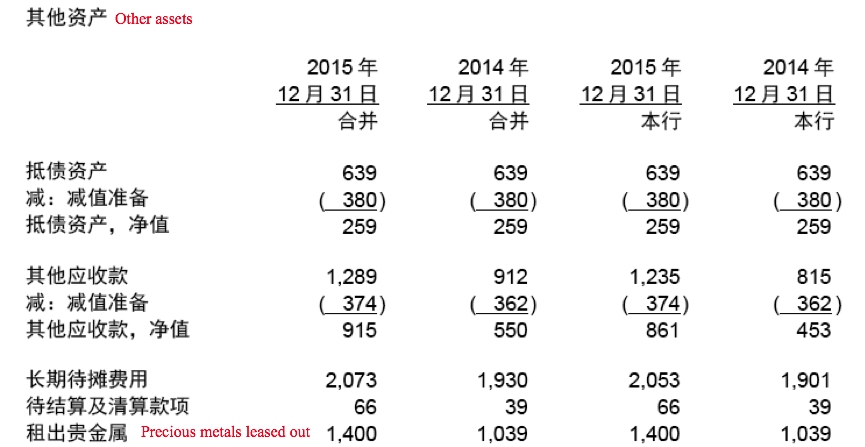

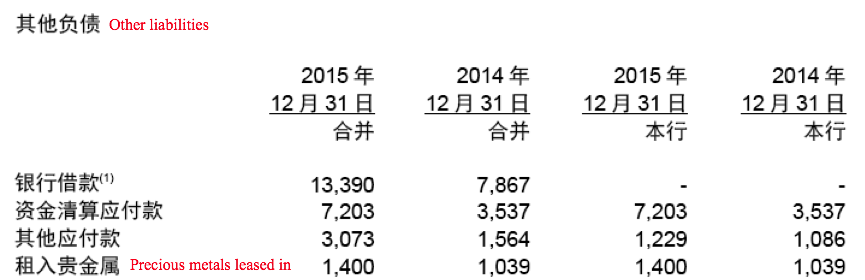

The Bank of Beijing is a good example to illustrate back-to-back gold lending. Unlike other Chinese banks, the Bank of Beijing does not put gold leasing in the precious metals category. It has a separate line in its books for gold leasing.

According to the 2015 annual report of the Bank of Beijing (page 123 and 132):

As readers can see from the excerpts above, the Bank of Beijing indeed does back-to-back gold leasing as precious metals “leased in” (RMB 1,400,000,000) are equal to precious metals “leased out”(RMB 1,400,000,000). I suspect most gold leasing by Chinese banks is back-to back leasing.

Because the Bank of Beijing has its leasing business noted in a separated line than its “precious metals", we can see a huge discrepancy between the Bank of Beijing’s precious metals holdings in exhibit 1 (RMB 55,000,000) and its back-to back leasing business in exhibit 6 (RMB 1,400,000,000).

Other banks don’t have a separate line for the gold leased out but as mentioned before, they put it in the precious metals category. A widely-accepted method to treat borrowed gold is to include a liability called “financial liability at fair value through profit and loss”. Readers who can understand Chinese are recommended to click this and this link. The ICBC annual report provides an example of how the liability is recorded.

In conclusion, back-to-back gold leasing will result in an asset and a liability on the banks’ balance sheets, for most banks highly “overstating" the precious metals category. When looking at exhibit 8 we can see the enormous growth in yearly Chinese gold leasing turnover, which must have enlarged Chinese banks’ balance sheets.

According to my analysis a large portion of the precious metals on the balance sheets of Chinese banks is back-to-back leasing, which, by the way, is nearly all gold that stays inside SGE vaults, and thus does not impact SGE withdrawals.

6. Synthetic Leases

Additionally, Chinese banks conduct synthetic leases – in other words: swaps. By performing synthetic leases, Chinese banks can show “precious metals assets" but no “precious metals liabilities" on their balance sheets. Then, at the very surface it seems these banks own gold, while in reality they own zero gold.

Also note, swaps can be executed with foreign banks, through which gold is subsequently imported into the domestic market. And because the Chinese banks have been importing thousands of tonnes in recent years, it should come as no surprise these trades have influenced the “precious metals” line item on their balance sheets.

From the previous chapter, we know that gold leasing – mainly back-to-back borrowing and lending – overstates the precious metals assets and liabilities of Chinese banks. However, what was not mentioned in the previous chapter was that banks do synthetic back-to-back leasing through swaps. This way, it’s possible that banks that are active in the gold lending market, will show precious metals assets on their balance sheet, though not owning a single gram of metal. The bank synthetically borrow gold through a swap, and lend it out for a few extra basis points. The result is synthetic back-to-back leasing.

From a Chinese bank’s perspective a synthetic gold lease is conducted by borrowing RMB to buy spot gold, lend that metal to a customer, and at the same time sell short a forward contract. When the gold loan to the customer comes due the metal is returned to the bank, which then will be sold through the forward contract to repay the bank’s RMB loan. That’s the definition of a swap: buy spot and sell forward (sell spot and buy forward for the counterparty).

In my previous post GOFO And The Gold Wholesale Market we could read about the relationships (and the exact workings of swaps) between fiat interest rates, swap rates and the Gold Lease Rate (GLR).

Fiat interest rate – swap rate = GLR

Effectively, by borrowing RMB for a swap the bank pays GLR to synthetically borrow gold.

As the international gold lease rate is likely lower than the gold lease rate in China, Chinese banks can make a profit by (synthetically) borrowing gold abroad, import the metal and lend it through the SGE system at a higher GLR. (Whenever a gold loan is to be repaid from the Chinese domestic gold market to an international lender, not the physical metal is exported, but funds cross the Chinese border, as physical gold export is prohibited from the Chinese domestic gold market.)

For example, Minsheng Bank can synthetically borrow gold for 3 months from HSBC at GLR in the interbank market. When Minsheng lends the gold for 3 months to a jeweler at GLR + 30 BPs, then Minsheng earns 30 BPs in this trade.

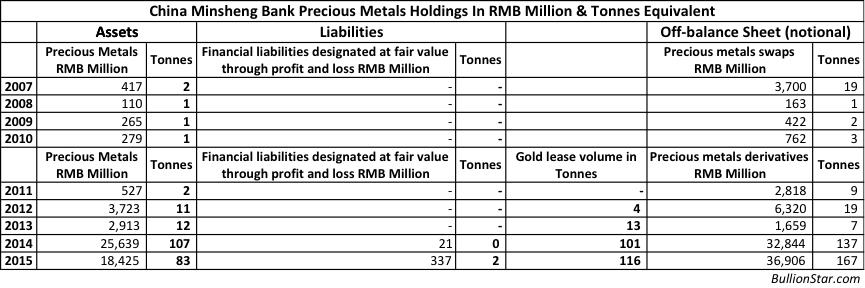

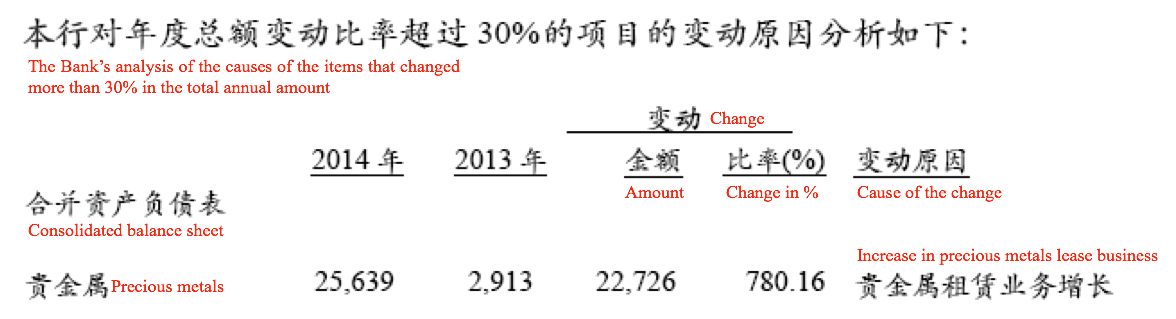

In the real world, this is exactly what banks have been doing. Let’s still use Minsheng Bank as an example. Please view the table above. We can see Minsheng’s gold lease volume jumped from 13 tonnes in 2013 to 101 tonnes in 2014, and the precious metals assets surged from 2,913 million RMB in 2013 (~12 tonnes) to 25,639 million RMB in 2014 (~107 tonnes). The surge in precious metals assets was fully caused by the increment in the gold lease business, as can be seen in the excerpt below from Minsheng Bank’s 2014 annual report. All the numbers are in millions of RMB.

It’s disclosed the precious metals assets jumped from 2,913 million RMB in 2013 to 25,639 million RMB in 2014, due to a 22,726 million “increase in precious metals lease business”.

But note we can only see an increase in “precious metals assets” on Minsheng’s balance sheet (exhibit 9), there are no “precious metals liabilities”. This is because the gold lend by Minsheng was sourced through swaps. Minsheng didn’t literally borrow gold (which would have caused a precious metals liability), it swapped gold for RMB collateral.

This is how it works in Minsheng’s case. When it enters a swap transaction these are the spot and the forward legs to be recorded in the financial statement. Minsheng borrows RMB and buys spot gold to lend out to a customer at GLR plus a few basis points. At that moment a precious metals asset (the gold loan) is recorded on the balance sheet, but not a precious metals liability (the related RMB liability is not disclosed in exhibit 9). Simultaneously, Minsheng sells short a forward contract that is recorded off-balance sheet. In due time the gold loan is repaid, the forward settled, etc.

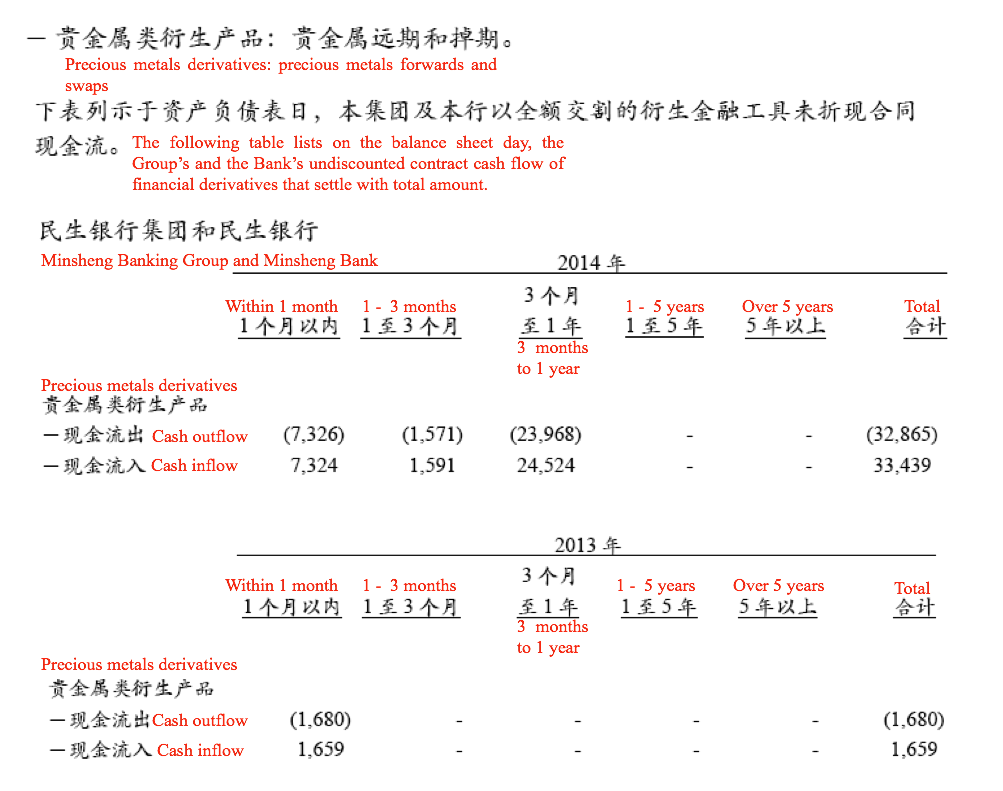

The off-balance activities are shown in exhibit 9, additionally they’re disclosed in Minsheng’s financial statement to be viewed below. Again all numbers are in millions of RMB.

We can see that the large increase in precious metals derivatives trading from 2013 to 2014 was mainly caused by “3 months to 1 year” “forwards and swaps” – of which most have been swaps used for synthetic back-to-back leasing.

Also note:

- Exhibit 10 shows there was a 22,726 million RMB (~ 94 tonnes) increase in leases from 2013 to 2014. Exhibit 11 shows ~ 24 billion RMB (~ 100 tonnes) in “3 months to 1 year” swaps have been executed in 2014, over zero in 2013. Likely, the majority of the swaps have been in tenors close to 1 year, as by 31 December 2014 roughly 107 tonnes in precious metals assets were on the balance sheet.

- In 2014 the “3 months to 1 year” “cash inflow” (Minsheng’s sell forward leg) transcended the “cash outflow” (buy spot leg) because gold was in contango that year in China. (Exhibit 11.)

- Minsheng Bank counts only 1 leg of the gold swap off-balance sheet. If we compare the total “precious metals forwards and swaps” “cash outflow” 32,865 million RMB (exhibit 11) with the total notional amount in precious metals derivatives off-balance sheet, 32,844 million RMB (exhibit 9), the two numbers are roughly equal.

All in all, at the surface it seems Minsheng Bank was holding/owning approximately 100 tonnes in precious metals assets late 2014, in reality this was merely reflecting synthetic back-to-back leasing through swaps.

As long as Chinese annual lease turnover grows, the commercial bank balance sheets can mushroom as a consequence. (See exhibit 8.) For more data on the “precious metals" on Chinese bank balance sheets read the chapter “III Data" of this post.

Conclusion

From the descriptions above, the precious metals holdings on the balance sheets of Chinese commercial banks are quite complicated to decipher. One thing is for sure, it’s not all gold owned by banks and leased out, neither is it gold purchased by banks on behalf of the Chinese central bank. In my opinion it’s a mixture of GAP gold, retail inventory, gold held for hedging, gold outside China, and back-to-back leasing and synthetic leasing.

In order for us to learn exactly what the precious metals on the balance sheets represent we need more information, more investigation is needed by gold analysts. Hopefully this blogpost can serve as a springboard to a better collective understanding.

Addendum

In addition to Gold Accumulation Plans many Chinese banks offer a variety of (paper) gold hedging and speculation broker services to their clients, but these are recorded off-balance sheet. For example, in the annual report 2014 from Agricultural Bank of China (ABC) we can read:

… Precious metals

… As a major precious metal market maker in the PRC, the Bank provided customers with precious metal trading, investment and hedging services through … trading of precious metal derivatives … and trading … the Shanghai Futures Exchange and the London precious metals market.

So, through ABC clients can trade paper gold, but these derivatives would be recorded off-balance sheet, or in a separate line next to “precious metals". More from the ABC annual report 2014:

Our off-balance sheet items primarily include derivative financial instruments, contingent liabilities and commitments. We enter into currency rate, interest rate and precious metals related derivative financial instruments for the purposes of trading, asset and liability management and business on behalf of customer.

Similarly, in BOC’s annual report 2015 we read:

Off-balance Sheet Items

Off-balance sheet items include derivative financial instruments, …. The Group entered into various derivative financial instruments relating to … precious metals and other commodities for trading, hedging, asset and liability management and on behalf of customers.

Implying, from my judgement, all the precious metals on-balance sheet are not (customers’) paper gold.

Popular Blog Posts by Koos Jansen

China’s Secret Gold Supplier is Singapore

China’s Secret Gold Supplier is Singapore

Audits of U.S. Monetary Gold Severely Lack Credibility

Audits of U.S. Monetary Gold Severely Lack Credibility

China Gold Import Jan-Sep 797t. Who’s Supplying?

China Gold Import Jan-Sep 797t. Who’s Supplying?

The Gold-Backed-Oil-Yuan Futures Contract Myth

The Gold-Backed-Oil-Yuan Futures Contract Myth

Estimated Chinese Gold Reserves Surpass 20,000t

Estimated Chinese Gold Reserves Surpass 20,000t

PBOC Gold Purchases: Separating Facts from Speculation

PBOC Gold Purchases: Separating Facts from Speculation

U.S. Mint Releases New Fort Knox Audit Documentation

U.S. Mint Releases New Fort Knox Audit Documentation

China Net Imported 1,300t of Gold in 2016

China Net Imported 1,300t of Gold in 2016

Why SGE Withdrawals Equal Chinese Gold Demand and Why Not

Why SGE Withdrawals Equal Chinese Gold Demand and Why Not