Chinese Banks Are Engaging in Synthetic Gold Leasing

Koos Jansen

Koos JansenMore proof the “precious metals assets" on Chinese commercial bank balance sheets have little to do with the “surplus” gold in China’s domestic market.

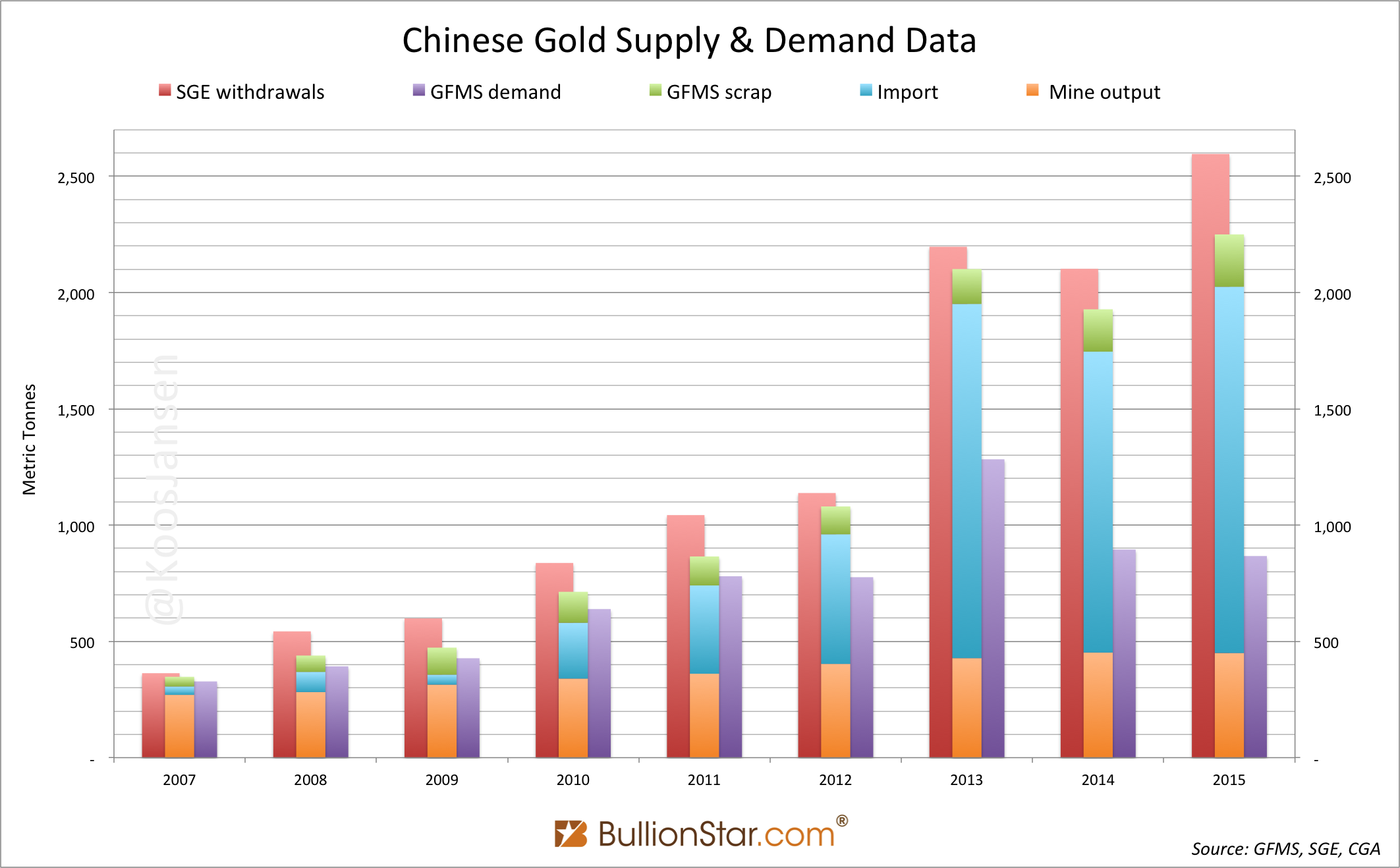

The “surplus" in the Chinese gold market is the difference between withdrawals from the Shanghai Gold Exchange vaults and gold demand as measured by consultancy firms like the World Gold Council and Thomson Reuters GFMS. The “surplus" accounts for over 4,000 tonnes. In reality the “surplus" is true gold demand by Chinese individuals and institutional investors directly at the SGE. Some analysts think the huge tonnages in “precious metals assets" on the balance sheets of Chinese commercial banks have anything to do with the “surplus", but this is not true. And I prefer to explain in detail.

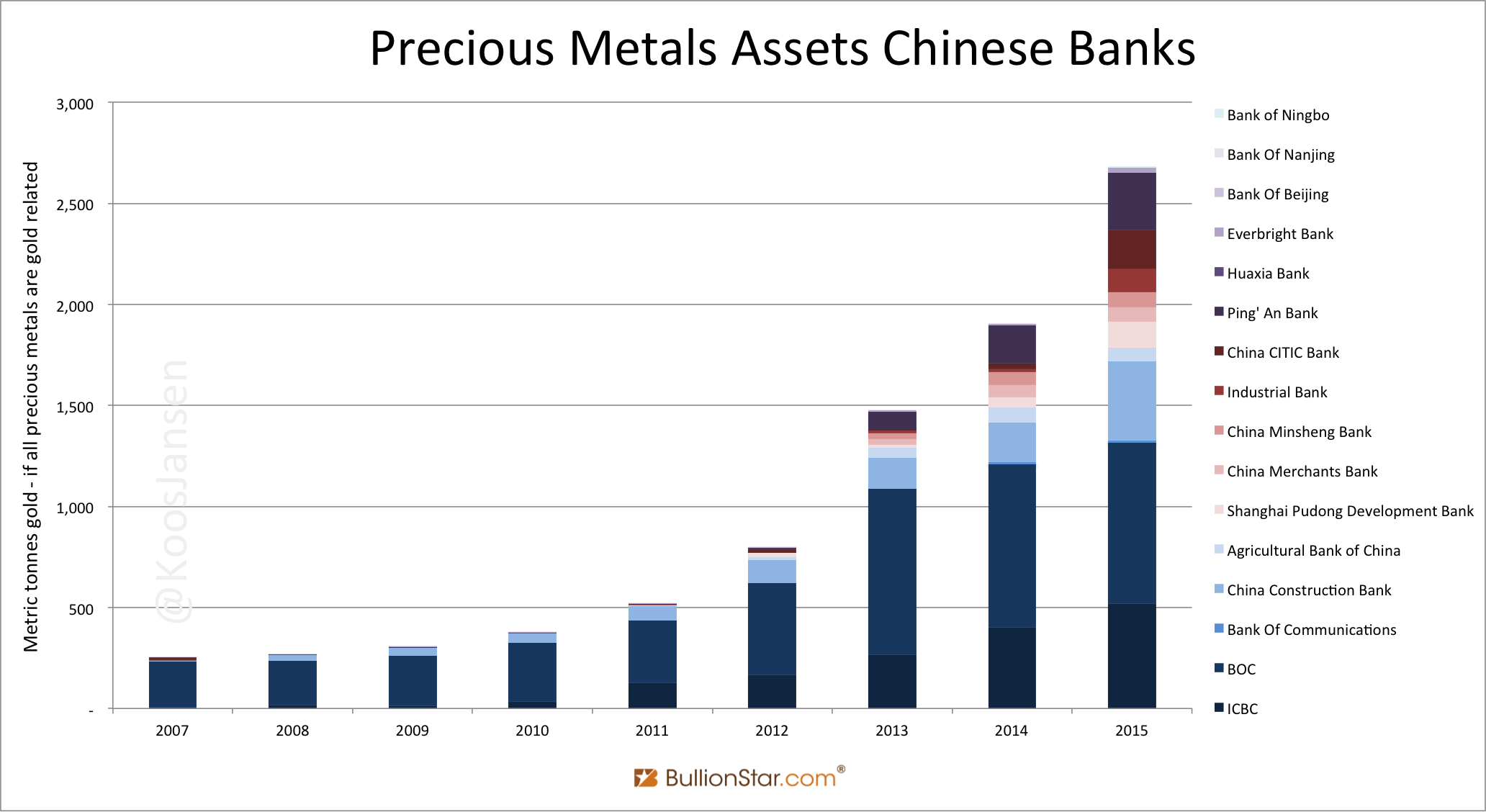

One of the topics about the Chinese gold market that has not been fully illuminated is the “gold" on the 16 Chinese commercial banks’ balance sheets. At the end of 2015 the aggregated “precious metals assets" on the bank balance sheets accounted for 598 billion yuan (RMB), which translates into approximately 2,682 tonnes of gold – if all the precious metals were gold related, which is very likely.

In my previous post on this subject we learned from examining the banks’ annual reports from 2015, that there are at least five gold assets that can appear in the “precious metals” line item on the balance sheets. Namely:

- Gold savings that belong to the banks’ customers (Gold Accumulation Plans, GAP)

- Gold inventory for the banks’ retail gold bar business

- Gold leasing business

- Gold held for hedging purposes

- Gold held outside China

In this post we’ll examine more thoroughly the (Chinese and English) annual reports from 2007 until 2014 of the 16 banks, to learn more on what these huge tonnages represent. The most significant new finding is that Chinese banks conduct synthetic leases – in other words: swaps. By performing synthetic leases, Chinese banks can show “precious metals assets" but no “precious metals liabilities" on their balance sheets. Then, at the very surface it seems these banks own gold, in reality they own zero gold.

Also note, swaps can be executed with foreign banks, through which gold is subsequently imported into the domestic market. And because the Chinese banks have been importing thousands of tonnes in recent years, it should come as no surprise these trades have influenced the “precious metals” line item on their balance sheets.

More findings that will be addressed in this post are:

- Chinese reported lease volume reflects yearly turnover.

- Gold stored in Shanghai Gold Exchange (SGE) designated vaults owned by commercial banks does not to appear on the custodial bank’s balance sheet.

- More confirmation some gold on the balance sheets is stored outside China.

My conclusion is that the “precious metals” on the Chinese commercial bank balance sheets do not account for the “surplus” gold in the Chinese domestic market Western consultancy firms pretend to be ignorant about. The Chinese banks do not own much gold of themselves, as some analysts have speculated, nor are these banks preparing for a new gold standard designed by the PBOC, according to my sources and analysis.

This post is divided in three segments. The first segment is about accounting, which supports the second segment about swaps and other gold related line items on the Chinese bank balance sheets. The first segment can be skipped if you already posses thorough knowledge on accounting. The third segment displays all the “precious metals" related data of the 16 bank balance sheets from 2007 until 2015.

I Accounting Background

Before we can discuss the details of the “precious metals” mentioned in the financial statements of the annual reports of the 16 banks, we need to do some studying on accounting structures (study the definitions of a financial statement, balance sheet, an income statement, assets/liabilities, financial assets/liabilities and derivative financial assets/liabilities). This study will prove valuable for future posts as well. The bank balance sheets are an important topic in the Chinese gold market; understanding accounting helps us to illuminate the Chinese gold market.

Financial Statement

Financial statements of banks are divided in three main segments: a balance sheet, an income statement and a cash flow statement.

Balance Sheet

On Investopedia we can read the definition of a balance sheet:

Balance Sheet

A balance sheet is a financial statement that summarizes a company’s assets, liabilities and shareholders’ equity at a specific point in time. These three balance sheet segments give investors an idea as to what the company owns and owes, as well as the amount invested by shareholders.

The balance sheet adheres to the following formula:

Assets = Liabilities + Shareholders’ Equity

A number of ratios can be derived from the balance sheet, helping investors get a sense of how healthy a company is. These include the debt-to-equity ratio and the acid-test ratio, along with many others. The income statement and statement of cash flows also provide valuable context for assessing a company’s finances, as do any notes or addenda in an earnings report that might refer back to the balance sheet.

An example would be, ICBC holding 1 tonne of gold in small ICBC brand bars as inventory for retail sales. This gold is an asset of ICBC.

Income Statement

Next to a balance sheet, banks disclose an income statement in their annual reports. From Investopedia we read:

Income Statement

An income statement is a financial statement that reports a company’s financial performance over a specific accounting period. Financial performance is assessed by giving a summary of how the business incurs its revenues and expenses …. It also shows the net profit or loss incurred over a specific accounting period.

Unlike the balance sheet, which covers one moment in time, the income statement provides performance information about a time period.

In example, ICBC buys gold at the SGE worth 1,000,000 RMB and has the metal recast in small 200 gram ICBC brand bars. If ICBC subsequently sells the newly casted bars for in total 1,100,000 RMB, then 100,000 RMB is profit and will be included in the income statement.

Cash Flow Statement

Next are the cash flows, from Investopedia:

Cash flow is the net amount of cash … moving into and out of a business.

Total aggregated cash flows are measured over the course of a period, for example one year, as with the income statement. But unlike the income statement, it records all things related to cash flows. For example, if ICBC buys a new building worth 10,000,000 RMB, this will affect the balance sheet (cash decrease, asset increase) and the cash flow statement, but not the income statement.

An Asset

From China’s Accounting Standard for Business Enterprises: Basic Standard we can read how an asset is defined:

Article 20 An asset is a resource that is owned or controlled by an enterprise as a result of past transactions or events and is expected to generate economic benefits to the enterprise.

“Past transactions or events” mentioned in preceding paragraph include acquisition, production, construction or other transactions or events. Transactions or events expected to occur in the future do not give rise to assets.

“Owned or controlled by an enterprise” is the right to enjoy the ownership of a particular resource or, although the enterprise may not have the ownership of a particular resource, it can control the resource.

“Expected to generate economic benefits to the enterprise” is the potential to bring inflows of cash and cash equivalents, directly or indirectly, to the enterprise.

Article 21 A resource that satisfies the definition of an asset set out in Article 20 in this standard shall be recognized as an asset when both of the following conditions are met:

(a) it is probable that the economic benefits associated with that resource will flow to the enterprise;

and

(b) the cost or value of that resource can be measured reliably.

Article 22 An item that satisfies the definition and recognition criteria of an asset shall be included in the balance sheet. An item that satisfies the definition of an asset but fails to meet the recognition criteria shall not be included in the balance sheet.

Financial assets/liabilities

Financial assets/liabilities can be subdivided in several categories, such as financial assets/liabilities designated at fair value through profit and loss, financial assets/liabilities held for trading and derivative financial assets/liabilities. Financial assets/liabilities are included on the balance sheet and the change in fair value of most financial asset/liabilities will appear in the income statement. Not all banks subdivide financial assets/liabilities in the same manner. For example, ICBC lists “financial assets/liabilities held for trading” parallel to “financial assets/liabilities designated at fair value through profit and loss”. Other banks only disclose “financial assets/liabilities designated at fair value through profit and loss” as a total. The details on accounting are beyond the scope of this post.

Let’s have a look at an example of a financial liability. We’ll use plain gold leasing. Suppose ICBC borrows 1 Kg of gold for 1 year and instantly sells the gold at 280 RMB/gram. ICBC will then record a cash asset of 280,000 RMB and a financial liability held for trading of 280,000 RMB on its balance sheet. Say, after one month the gold price surges to 380 RMB/gram. For ICBC the cash asset remains at 280,000 RMB, but the bank will increase the carrying amount of the financial liability held for trading to 380,000 RMB. The 100,000 RMB, which is a loss, will go into the income statement. In the income statement there is a separate line for this called net profit or loss on financial assets or liabilities designated at fair value through profit and loss.

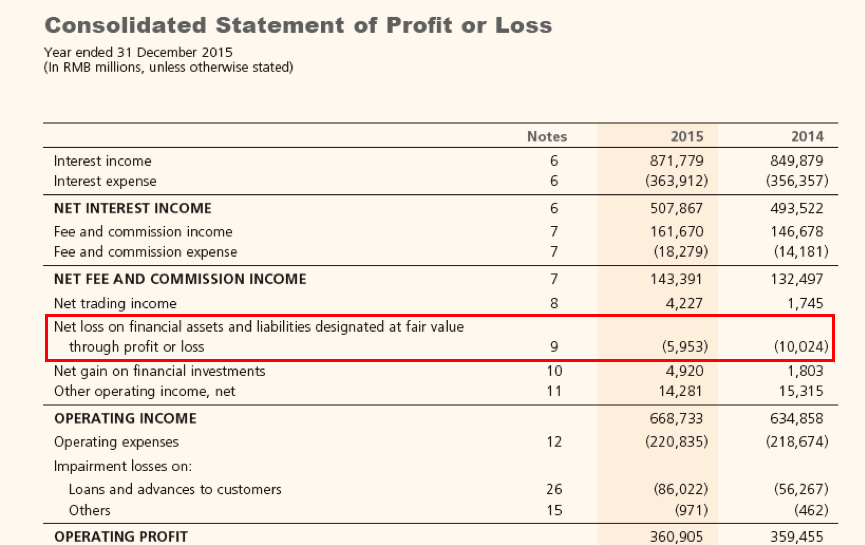

Below is part of the income statement from ICBC’s 2015 annual report.

Derivative financial assets/liabilities

Derivative financial assets/liabilities on balance sheets must not be commingled with derivative instruments such as futures or forwards, of which the notional values are recorded off-balance sheet. Let me show how derivative financial assets/liabilities are acquired.

We’ll use futures as an example. Suppose ICBC buys long a SHFE gold futures (1,000 grams) contract at 280 RMB/gram on 1 November 2016 that is to expire in June 2017. The futures contract itself (derivative instrument) is recorded off-balance sheet, but the profit or loss arising from it creates a “derivative financial asset/liability” recorded on the balance sheet and the income statement. At 1 November 2016 the fair value of the futures contract is 0 because the future price has not moved yet so there is no profit or loss. The notional value of the futures contract is 280,000 RMB (1,000*280). On 1 November 2016 ICBC’s financial statement would be:

- ICBC’s derivative financial asset/liability held for trading on the balance sheet = 0

- Fair value ICBC’s derivative financial asset/liability held for trading recorded in the income statement’s “net profit or loss on financial assets or liabilities designated at fair value through profit and loss” = 0 RMB

- Notional value of ICBC’s derivative financial instrument recorded off-balance sheet = 280,000 RMB

Suppose one month later, on 1 December 2016, the gold price has surged to 380 RMB/gram. ICBC is long gold so it will have a mark-to-market profit of 100,000 RMB. This profit will go into the income statement in “net profit or loss on financial assets or liabilities designated at fair value through profit and loss”. At the same time ICBC has created a derivative financial asset held for trading worth 100,000 RMB. (If gold would sink below 280 RMB/gram, ICBC would record a derivative financial liability held for trading.) On 1 December 2016 ICBC’s financial statement would be:

- Derivative financial asset held for trading on the balance sheet = 100,000 RMB

- Fair value ICBC’s derivative financial assets held for trading recorded in the income statement’s “net profit or loss on financial assets or liabilities designated at fair value through profit and loss” = 100,000 RMB

- Notional value of ICBC’s derivative financial instrument recorded off-balance sheet = 380,000 RMB

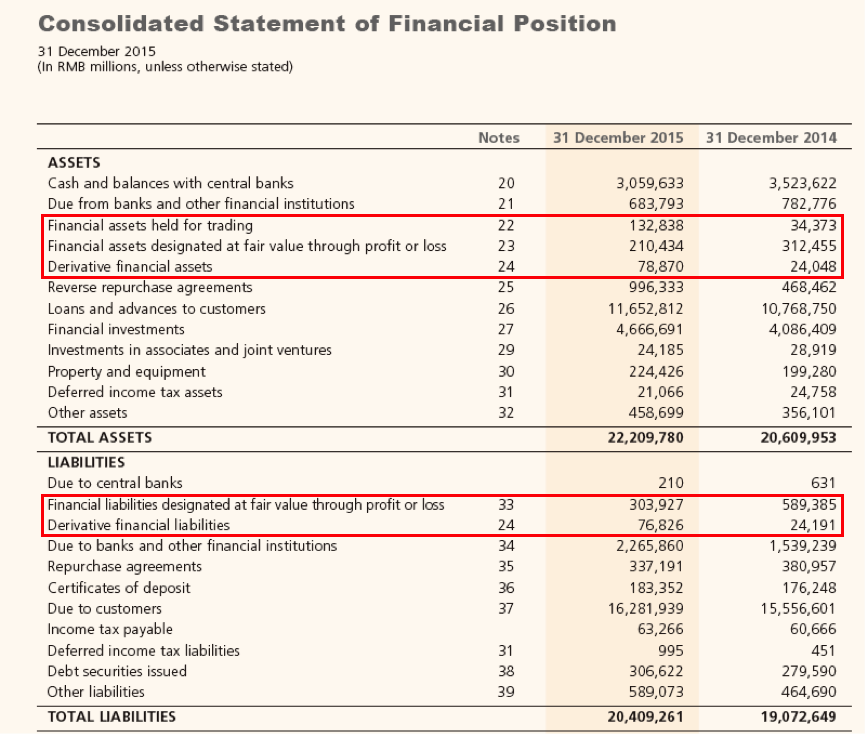

Below you can view a balance sheet and an off-balance sheet account from ICBC’s 2015 annual report.

Having said this, the practice of categorizing precious metals assets and liabilities varies from bank to bank in China. Nevertheless, there are excellent observations to make from the financial statements of the banks. This will be quite complex, if I didn’t explain it properly, please refer to the introduction of this post that serves as a simplified summary.

II Findings

Banks Do Synthetic Back-To-Back Gold Leasing Through Swaps

From the previous post, we know that gold leasing – mainly back-to-back borrowing and lending – overstates the precious metals assets and liabilities of Chinese banks. However, what was not mentioned in the previous post was that banks do synthetic back-to-back leasing through swaps. This way, it’s possible that banks that are active in the gold lending market, will show precious metals assets on their balance sheet – without precious metals liabilities, while not owning a single gram of metal themselves. The bank will synthetically borrow gold through a swap, and lend it out for a few extra basis points. The result is synthetic back-to-back leasing.

From a Chinese bank’s perspective a synthetic gold lease is conducted by borrowing RMB to buy spot gold, lend that metal to a customer, and at the same time sell short a forward contract. When the gold loan to the customer comes due the metal is returned to the bank, which then will be sold through the forward contract to repay the bank’s RMB loan. That’s the definition of a swap: buy spot and sell forward (sell spot and buy forward for the counterparty).

If gold is in contango, and the forward price is higher than spot, the Chinese bank will make a profit on the swap. However, in contango, the costs for the RMB loan transcend the swap profit. The difference between both is the cost equal to the gold lease rate (GLR). In my previous post Understanding GOFO And The Gold Wholesale Market we could read about these relationships (and the exact workings of swaps).

Fiat interest rate – swap rate = GLR

Effectively, by borrowing RMB for a swap the bank pays GLR to synthetically borrow gold.

As the international gold lease rate is likely lower than the gold lease rate in China, Chinese banks can make a profit by (synthetically) borrowing gold abroad, import the metal and lend it through the SGE system at a higher GLR. (Whenever a gold loan is to be repaid from the Chinese domestic gold market to an international lender, not the physical metal is exported, but funds cross the Chinese border, as physical gold export is prohibited from the Chinese domestic gold market.)

For example, Minsheng Bank can synthetically borrow gold for 3 months from HSBC at GLR in the interbank market. When Minsheng lends the gold for 3 months to a jeweler at GLR + 30 BPs, then Minsheng earns 30 BPs in this trade.

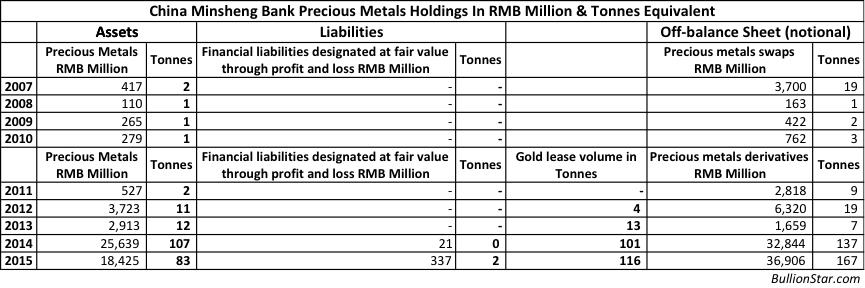

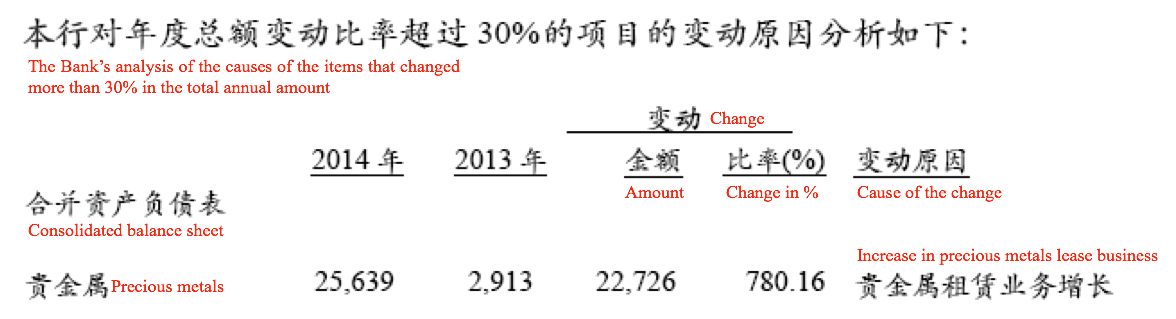

In the real world, this is exactly what banks have been doing. Let’s still use Minsheng Bank as an example. Please view the table above. We can see Minsheng’s gold lease volume jumped from 13 tonnes in 2013 to 101 tonnes in 2014, and the precious metals assets surged from 2,913 million RMB in 2013 (~12 tonnes) to 25,639 million RMB in 2014 (~107 tonnes). The surge in precious metals assets was fully caused by the increment in the gold lease business, as can be seen in the excerpt below from Minsheng Bank’s 2014 annual report. All the numbers are in millions of RMB.

It’s disclosed the precious metals assets jumped from 2,913 million RMB in 2013 to 25,639 million RMB in 2014, due to a 22,726 million “increase in precious metals lease business”.

But note we can only see an increase in “precious metals assets” on Minsheng’s balance sheet (exhibit 4), there are no “precious metals liabilities”. This is because the gold lend by Minsheng was sourced through swaps. Minsheng didn’t literally borrow gold (precious metals liability), it swapped gold for RMB collateral.

This is how it works in Minsheng’s case. When it enters a swap transaction these are the spot and the forward legs to be recorded in the financial statement. Minsheng borrows RMB and buys spot gold to lend out to a customer at GLR plus a few basis points. At that moment a precious metals asset (the gold loan) is recorded on the balance sheet, but not a precious metals liability (the related RMB liability is not disclosed in exhibit 4). Simultaneously, Minsheng sells short a forward contract that is recorded off-balance sheet. In due time the gold loan is repaid, the forward settled, etc.

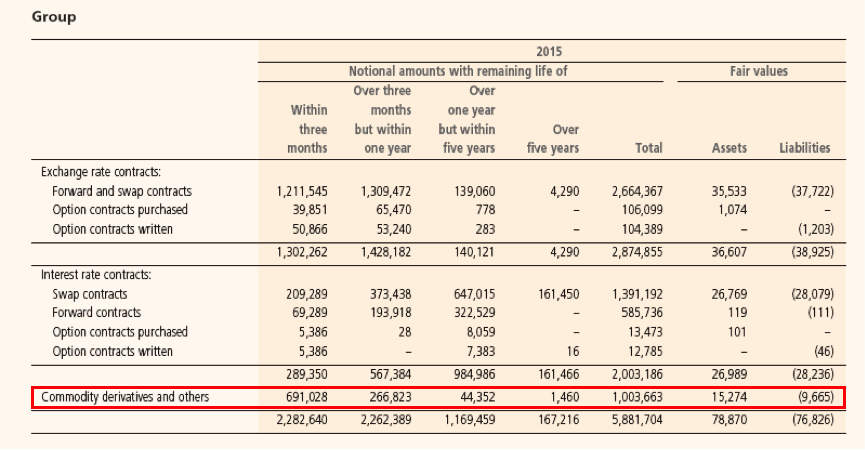

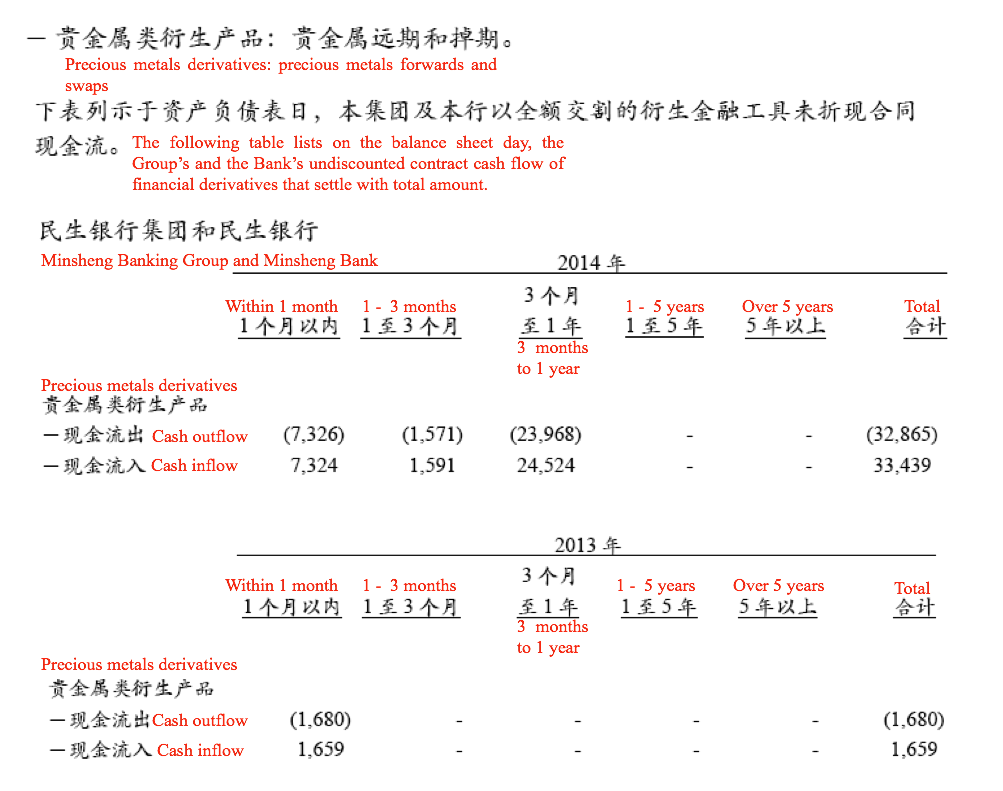

The off-balance activities are shown in exhibit 4, additionally they’re disclosed in Minsheng’s financial statement to be viewed below. Again all numbers are in millions of RMB.

We can see that the large increase in precious metals derivatives trading from 2013 to 2014 was mainly caused by “3 months to 1 year” “forwards and swaps”, of which most have been swaps used for synthetic back-to-back leasing.

Also note:

- Exhibit 5 shows there was a 22,726 million RMB (~ 94 tonnes) increase in leases from 2013 to 2014. Exhibit 6 shows ~ 24 billion RMB (~ 100 tonnes) in “3 months to 1 year” swaps have been executed in 2014, over zero in 2013. Likely, the majority of the swaps have been in tenors close to 1 year, as by 31 December 2014 roughly 107 tonnes in precious metals assets were on the balance sheet.

- In 2014 the “3 months to 1 year” “cash inflow” (Minsheng’s sell forward leg) transcended the “cash outflow” (buy spot leg) because gold was in contango that year in China. (Exhibit 6)

- Perhaps you have noticed that Minsheng Bank counts only 1 leg of the gold swap off-balance sheet. Yes, if we compare the total “precious metals forwards and swaps” “cash outflow” 32,865 million RMB with the total notional amount in precious metals derivatives off-balance sheet, 32,844 million RMB, the two numbers are roughly equal.

All in all, at the surface it seems Minsheng Bank holds approximately 100 tonnes in precious metals assets, in reality this is merely reflecting synthetic back-to-back leasing through swaps. More proof there can be little “surplus” gold on the commercial banks balance sheets.

As long as Chinese annual lease volume grows, the commercial bank balance sheets can mushroom as a consequence.

Chinese Lease Volume Reflects Yearly Turnover.

In the past there has been some doubt whether the reported Chinese gold lease volume reflected the total turnover over a certain period, or the gold that has been leased out at a certain point in time. Already in May 2015 I wrote China’s reported gold lease volume reflects turnover – because traders at Chinese banks told me – and now there is more confirmation to be presented. From Minsheng Bank’s financial statements we can understand that the gold lease volume means the lease turnover per annum. Have another look at exhibit 4.

Minsheng bank leased out 116 tonnes of gold in 2015, which was an increase from 2014. But at the end of 2015, the “precious metals assets” wherein gold leasing is recorded, decreased to 83 tonnes. This can only be possible if the lease volume is annual turnover. Apparently, in 2015 Minsheng’s leasing business grew, but it conducted more deals in tenors shorter than 1 year, causing the annual turnover to increase (to 116 tonnes) but the outstanding leases at year-end on the balance sheet to decline from the previous year.

The World Gold Council (WGC) seems the have come to the same conclusion recently. In the Gold Demand Trends Q2 2016 report, it stated (page 15) the gold lease volume “captures the total amount of gold leased in the reporting period, for example, if Commercial Bank A lends 1t to Jeweller B for three months and Jeweller B returns it back for the Commercial Bank A to lend again to Bank C, a total of 2t of leasing volume will be recorded for the period”. This confession by the WGC is remarkable, because from April 2014 until early 2016 the WGC was spreading a myth about the gold involved in the Chinese lease market. From the WGC’s China’s Gold Market Progress And Prospects, April 2014:

No statistics are available on the outstanding amount of gold tied up in financial operations [leases] linked to shadow banking but Precious Metals Insights believes it is feasible that by the end of 2013 this could have reached a cumulative 1,000t.

For several years the WGC pretended any lend/borrowed gold was “tied up in illegal leasing schemes”, and if the leases would be unwound this event would flush the physical market dragging down the price. Although this was nonsense, copy-paste media outlets like Reuters and the Financial Times simply reproduced what the WGC was writing, adding to the confusion in the gold community. (By the way, the consfusion simply appeared to be a pack of lies invented by Western consultancy firms that were trying to uphold the illusion the supply and demand data they had been selling for decades was complete.)

While at it, the WGC admitted most of the leased gold doesn’t leave the SGE vaults:

It’s estimated that around 10 % of the leased gold leaves the SGE’s vaults. The majority is for financing purposes and is sold at the SGE for cash settlement.

This is what I’ve written since February 2015: gold leasing has little impact on SGE withdrawals, as the vast majority of leases are for financing purposes and are thus settled within the SGE system.

Gold In SGE Vaults Is Not On The Custodian’s Balance Sheets

In China, most of the SGE vaults are actually owned by commercial banks but approved by the SGE as “designated vaults”. In addition there are other types of enterprises that own “SGE designated vaults” – probably jewelry companies in Shenzhen, the heart of China’s jewelry manufacturing industry. In my previous post I shared the possibility that SGE vaulted gold appears on the balance sheets of custodian commercial banks. But further research has pointed out that is not the case. SGE vaulted gold does not appear on the balance sheet of the custodians, only on the balance sheet of the owner.

As has been written at the beginning of this post, in order for a custodian, in this example ICBC, to recognise the gold owned by another entity, in this example BOC, in its SGE-designated vault as an asset, the gold has to be “owned or controlled” by ICBC. In reality ICBC wouldn’t have any ownership of this gold. ICBC would have, to a certain extent, some control over BOC’s gold, but in order for ICBC to recognise the gold as an asset on its balance sheet, it should be “probable that the economic benefits associated with that resource will flow to the enterprise”. In other words, ICBC should be able to sell or lease out BOC’s gold in its vaults to record the metal as asset. Though, an SGE custodian would never go there or its business would collapse promptly.

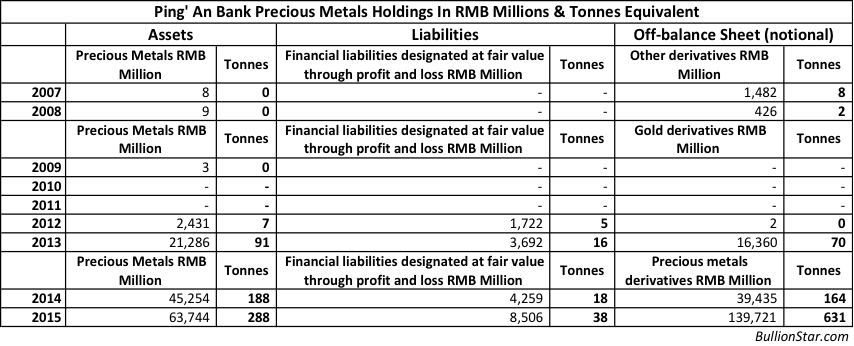

There is more confirmation. On the balance sheet of Ping’ An Bank, the volume of precious metals holdings for 2011 and 2010 were both nil. At the same time, according to Ping’ An’s annual report of 2010, its total gold withdrawals ranked No. 8 among all SGE designated vaults.

黄金仓储业务继续保持增长态势,交割量列交易所交割仓库前8名。

Gold vaulting service keeps increasing and the withdrawal number is listed the eighth among SGE designated vaults.

And in 2011 Ping’ An’s gold deposit and withdrawal total accounted for 10% of all SGE warehouse activity. It is hard to believe that Ping’ An had no gold in its SGE-designated vaults at the end of 2010 and 2011, while Ping’ An’s vaults were such an important part of the SGE system. Concluding, Ping’ An didn’t recognize other SGE clients’ or members’ gold in its vaults as its assets. Hence we have for 0 for Ping’ An’s precious assets in 2010 and 2011.

Some readers may point out the following paragraph in ICBC’s 2015 annual report:

The Group records the precious metals received as an asset. A liability to return the amount of precious metals deposited is also recognised.

However, if readers check ICBC’s 2015 annual report in Chinese, they will find the original paragraph was written like this:

本集团收到客户存入的积存贵金属时确认资产,并同时确认相关负债。

The group recognises an asset when the group receives the precious metals deposited by the customer for accumulation, and at the same time recognises the related liability.

Therefore, ICBC was actually referring to the gold in its Gold Accumulation Plan (GAP) and the key information was lost in translation.

Gold in Chinese ETFs is neither recognized by its custodian as an asset.

Some Of Chinese Banks’ Gold Is Indeed Outside China

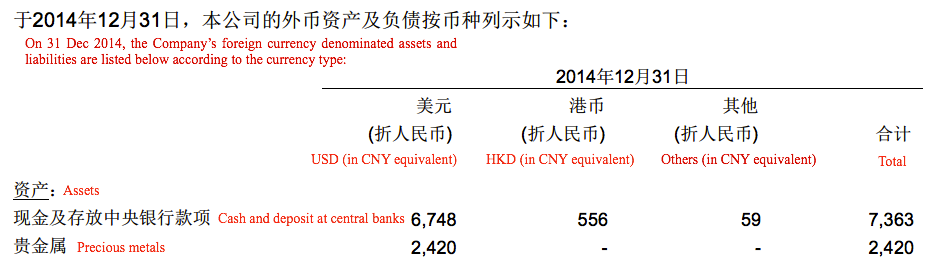

I mentioned in the previous post that some of Chinese banks’ precious metals holdings could be outside China. ICBC acquired Standard Bank in 2015 and Standard Bank’s precious metals are outside China. However, even some medium-sized Chinese banks hold precious metals outside China. The following table is from Ping’ An’s 2014 annual report (page 196, numbers are in millions of RMB).

What we see is that Ping’ An held gold assets in US dollars worth 2,420 million RMB. The disclosed “foreign exchange equivalent” for Ping’ An’s precious metals would only be mentioned like this if the precious metals are held outside China. If the precious metals would have been located inside China, Ping’ An never would have listed the value of the assets as “USD (in CNY equivalent)”.

III Data

We will not extensively analyze every Chinese bank’s financial statement like we’ve done with Minsheng Bank and Ping’ An Bank above, though I do like to share all the data I’ve collected. The practice of categorizing precious metals assets and liabilities varies from bank to bank so readers should pay attention to the notes below the tables and are recommended to read the original annual reports for more information. The derivative instruments are listed according to the notional amount (off balance sheet) instead of the fair value. The notional amount is not comparable between banks because for swaps, some banks only consider one leg while others add both the spot and forward legs, for example Bank of Ningbo, together.

Assuming all precious metals mentioned are gold related.

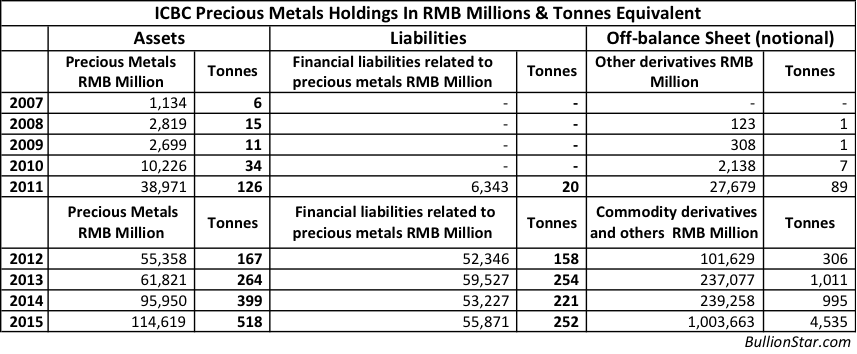

1. Industrial and Commercial Bank of China (ICBC)

We can observe ICBC precious metals assets started to transcend its financial liabilities related to gold in 2014. The possible causes are increases in ICBC brand gold bar sales (more inventory), customers purchased more options (ICBC would need to buy more gold to hedge), and more synthetic gold leasing.

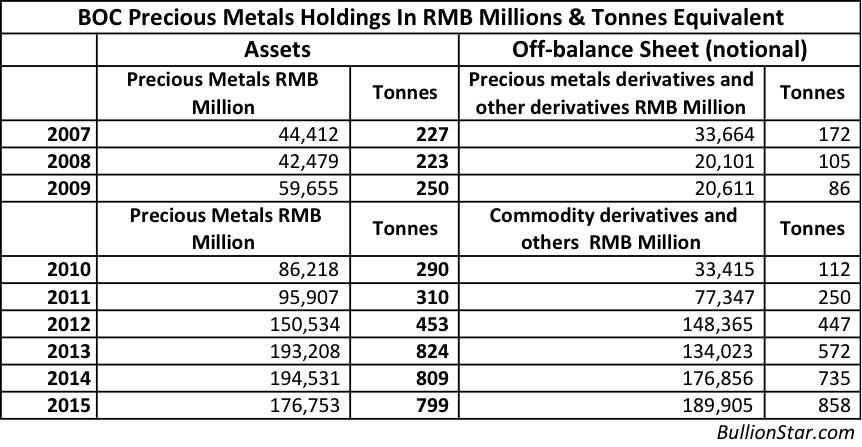

2. Bank of China (BOC)

“Commodity derivatives and others” were called “precious metals derivatives and other derivatives” before 2010. BOC doesn’t have any significant numbers related to precious metals in financial liabilities designated at fair value through profit and loss.

Noteworthy, at the end of 2007 BOC had 7,982 million RMB (~ 41 tonnes of gold) in precious metals pledged as collateral, and late 2009 this figure had grown into 27,271 million RMB (~ 114 tonnes of gold). The precious metals were used as collateral in swap transactions for financing, according BOC’s accounting practice.

From BOC’s 2009 Annual Report:

贵金属互换交易,根据其交易实质,按照在抵押协议下出售的贵金属交易处理。抵押的贵金属不予终止确认,相关负债在“拆入资金” 中反映。

Precious metals swap transactions, based on the transaction nature, are treated as precious metals sales under collateral agreement. The precious metals pledged as collateral are not ceased to be recognized and the related liability is reflected in “borrowings through interbank lending”

3. Bank of Communications

Bank of Communications lists precious metals assets in two separate categories. I’m not sure what is identified with “precious metals contracts".

Bank of Communications reported in its 2013 annual report that it conducted overseas gold swap business:

成功开展境外黄金掉期交易业务

[Bank of Communications] successfully conducted overseas gold swap transactions.

In 2013, Bank of Communications conducted gold interbank lending with HSBC and HSBC became the most important source of physical gold for the Bank of Communications:

双方在2013年不仅实现了黄金寄售与黄金拆借的「第一单」合作,且合作量快速攀升。汇丰银行已成为本行实物黄金的重要进口来源。

The two parties [Bank of Communications and HSBC] not only conducted “first deal” cooperation in gold consignment and gold borrowing, but also realized surging cooperation volume. HSBC has become an important import source of physical gold for the bank.

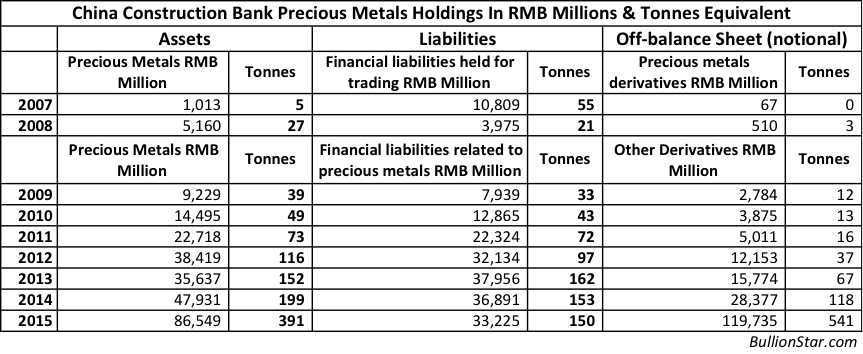

4. China Construction Bank

Not everything in the “other derivatives” category are precious metals.

Not everything in the “other derivatives” category are precious metals.

China Construction Bank (CCB) wrote in its annual reports that the market share of physical sales to the public was No. 1 in 2010, and in the same year the market share of gold leasing was 40 %. From CCB’s 2010 annual report:

本行个人实物品牌金销售市场占比保持第一;黄金租借市场占比40.30%;账户金市场占比37.41%。

The Bank [China Construction Bank] has maintained the rank of No 1 in branded physical gold to individuals. The market share of gold leasing was 40.30 %. The market share of account gold was 37.41 %.

CCB offered physical withdrawal on precious metals accounts since 2013 and its own gold accumulation plan since 2015.

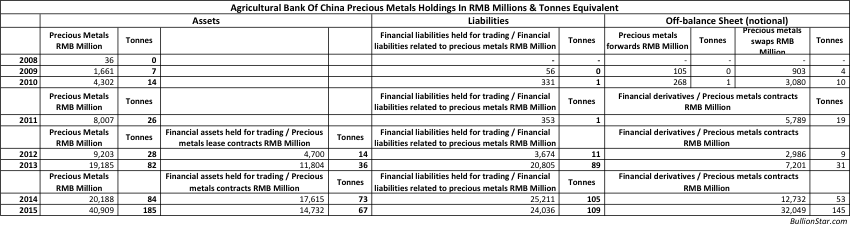

5. Agricultural Bank of China

Before 2014 “precious metals contracts” were called “precious metals lease contracts”. Not sure what “precious metals contracts” can be next to “precious metals lease contracts” – perhaps SGE physical contracts like Au99.99.

Before 2011, precious metals derivatives were reported separately as forwards and swaps. The precious metals lease business was reported to be launched in 2010.

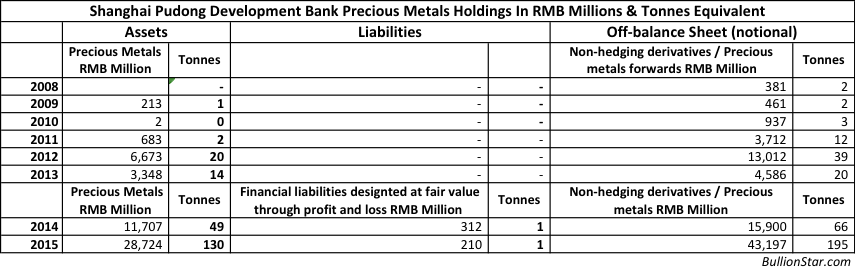

6. Shanghai Pudong Development Bank

The change in “Financial liabilities at fair value through profit and loss” was caused by precious metals shorts (?) according to Shanghai Pudong Development Bank’s annual reports.

7. China Merchants Bank

The increase in “precious metals assets” was caused by the increase in proprietary trading and gold lease according to the annual reports. From China Merchants Bank’s 2014 annual report:

In 2013, China Merchants Bank reported to have conducted precious metals leasing of 60 tonnes, a 203 % increase from 2012.

8. China Minsheng Bank

The fine data was discussed in the previous chapter.

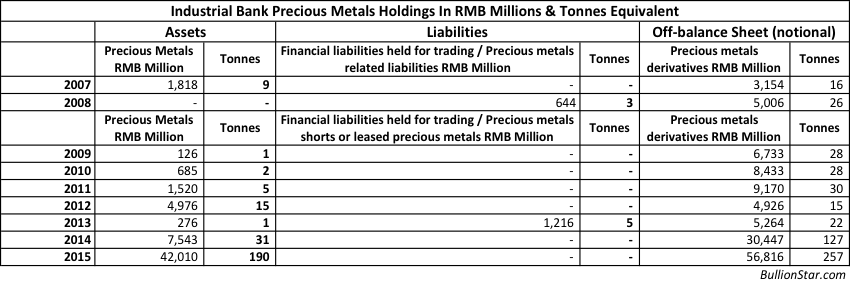

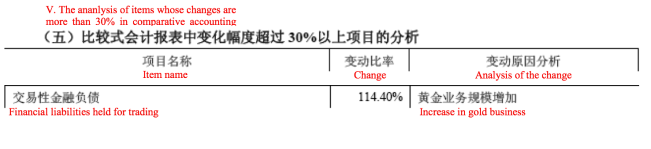

9. Industrial Bank

The 644 million RMB precious metals related liabilities were caused by “gold pledge business” according to Industrial Bank’s 2008 annual report.

“Precious metals shorts and leased precious metals” are a subcategory under “financial liabilities held for trading”.

10. China CITIC Bank

According to the annual reports, the surge in the precious metals and precious metals contracts in 2014 was caused by the increase of precious metals lease and proprietary business.

According to the annual reports, the surge in the precious metals and precious metals contracts in 2014 was caused by the increase of precious metals lease and proprietary business.

According to CITIC bank’s 2014 annual report:

报告期内黄金租赁业务和贵金属自营交易量均实现了快速增长

In the reporting period, the gold lease business and precious metals proprietary trading business all achieved rapid growth.

11. Ping’ An Bank (former Shenzhen Development Bank)

Before 2014 precious metals derivatives were called gold derivatives. Before 2009, Ping’ An only gave a lump sum of all the derivatives. Just in case there were any gold derivatives in this category, I’ve included the lump-sum numbers.

The increase in the “financial liabilities designated at fair value through profit and loss” in 2013 was caused by the increase in “financial liabilities held for trading” related to “gold business”, according to the annual report. Therefore all the numbers in “Financial liabilities designated at fair value through profit and loss” are listed here, although this category may include some liabilities not related to precious metals. From Ping’ An’s 2013 annual report:

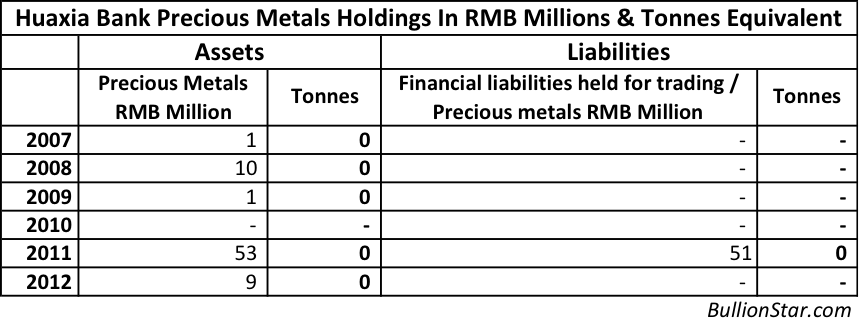

12. Huaxia Bank

12. Huaxia Bank

The precious metals assets in 2007 and 2008 were a result from physical gold sales according to the annual reports.

13. Everbright Bank

According to the annual reports, Everbright Bank started to conduct gold consignment sales and gold leasing in 2013. Therefore, the increase in precious metals holding in 2013 was probably caused by these activities. From to Everbright Bank’s 2013 annual report:

获批黄金进口资格,开展黄金寄售和黄金租售业务

[Everbright Bank] acquired the gold import qualification, started to conduct gold consignment and gold lease business.

14. Bank of Beijing

Clearly the Bank of Beijing participates in back-to-back leasing, as precious metals leased out are exactly equal to precious metals leased in.

15. Bank of Nanjing

The Bank of Nanjing only disclosed 6 million RMB in precious metals assets in 2014 and 7 million RMB in 2015.

16. Bank of Ningbo

Popular Blog Posts by Koos Jansen

China’s Secret Gold Supplier is Singapore

China’s Secret Gold Supplier is Singapore

Audits of U.S. Monetary Gold Severely Lack Credibility

Audits of U.S. Monetary Gold Severely Lack Credibility

China Gold Import Jan-Sep 797t. Who’s Supplying?

China Gold Import Jan-Sep 797t. Who’s Supplying?

The Gold-Backed-Oil-Yuan Futures Contract Myth

The Gold-Backed-Oil-Yuan Futures Contract Myth

Estimated Chinese Gold Reserves Surpass 20,000t

Estimated Chinese Gold Reserves Surpass 20,000t

PBOC Gold Purchases: Separating Facts from Speculation

PBOC Gold Purchases: Separating Facts from Speculation

U.S. Mint Releases New Fort Knox Audit Documentation

U.S. Mint Releases New Fort Knox Audit Documentation

China Net Imported 1,300t of Gold in 2016

China Net Imported 1,300t of Gold in 2016

Why SGE Withdrawals Equal Chinese Gold Demand and Why Not

Why SGE Withdrawals Equal Chinese Gold Demand and Why Not