The Chinese Gold Lease Market Explained

Koos Jansen

Koos JansenThis post is part of the Chinese Gold Market Essentials series. Click here to go to an overview of all Chinese Gold Market Essentials for a comprehensive understanding of the largest physical gold market globally. This post was updated late 2017.

The main arguments presented by Western consultancy firms, such as GFMS and the World Gold Council (WGC), to explain the difference between SGE withdrawals and Chinese consumer gold demand relate to Chinese Commodity Financing Deals (CCFDs). However, this analysis is incorrect as I will demonstrate in this post.

CCFDs are used by Chinese speculators to acquire cheap funds using commodities as collateral. When it comes to using gold as collateral for CCFDs there are two options: round tripping and gold leasing. First we’ll discuss round tripping.

Round Tripping

Goldman Sachs (GS) has properly described the round tripping process in a report dated March 2014. We’ll start by reading a few segments from GS about financing deals [brackets added by me]:

While commodity financing [round tripping] deals are very complicated, the general idea is that arbitrageurs borrow short-term FX loans from onshore banks in the form of LC (letter of credit) to import commodities and then re-export the warrants (a document issued by logistic companies which represent the ownership of the underlying asset) to bring in the low cost foreign capital (hot money) and then circulate the whole process several times per year. As a result, the total outstanding FX loans associated with these commodity financing deals is determined by:

- – the volume of physical inventories that is involved

- – commodity prices

- – the number of circulations

Our understanding is that the commodities that are involved in the financing deals include gold, copper, iron ore, and to a lesser extent, nickel, zinc, aluminum, soybean, palm oil and rubber.

…Chinese gold financing deals are processed in a different way compared with copper financing deals, though both are aimed at facilitating low cost foreign capital inflow to China. Specifically, gold financing deals involve the physical import of gold and export of gold semi-fabricated products to bring the FX into China; as a result, China’s trade data does reflect, at least partially, the scale of China gold financing deals. In contrast, Chinese copper financing deals do not need to physically move the physical copper in and out of China, so it is not shown in trade data published by China customs. In detail, Chinese gold financing deals includes four steps:

- Onshore gold manufacturers pay LCs to offshore subsidiaries and import gold from Hong Kong to mainland China – inflating import numbers

- offshore subsidiaries borrow USD from offshore banks via collaterizing LCs received

- onshore manufacturers get paid by USD from offshore subsidiaries and export the gold semi-fabricated products – inflating export numbers

- repeat step 1-3

Important to understand is that gold in round tripping needs to be physically imported into China and then exported, in contrast to copper. The reason for this, which GS fails to mention, is that the cross-border trade rules for gold in China are different than for all other commodities. Only through processing trade gold can be imported into China mainland by enterprises that do not carry a PBOC gold trade license. Round tripping by speculators can only be done through processing trade, as it’s not possible through general trade to ship gold into China without a PBOC license. Consequently, round tripping flows are completely separated from the Chinese domestic gold market where the SGE operates. And hence, round tripping cannot inflate SGE withdrawals.

Only by bending the rules – set up a fake jewelry enterprise in a CSSA – speculators can import gold to round trip. By using processing trade, in order to import gold into China, speculators are required to subsequently export the exact same amount of gold, because these speculators pretend to be jewelry manufacturers importing gold for genuine production, which upon completion must be exported. This is why the gold is round tripped. The requirement for export in processing trade can be read in the official PRC Customs Supervision and Administration of Processing Trade Goods Procedures (2004):

“Processing trade” shall refer to the business activity of import of operating enterprises of all or some raw and auxiliary materials, components, parts, mechanical components and packing materials (Materials and Parts) and the re-export thereof as finished products after processing or assembling.

Now we can understand why GS wrote [brackets added by me]:

Specifically, gold financing deals [round tripping] involve the physical import of gold and export of gold semi-fabricated products to bring the FX into China…

The speculators export semi-fabricated gold products to keep up the appearance they are genuine gold fabricators, for which the gold imported must be processed and exported.

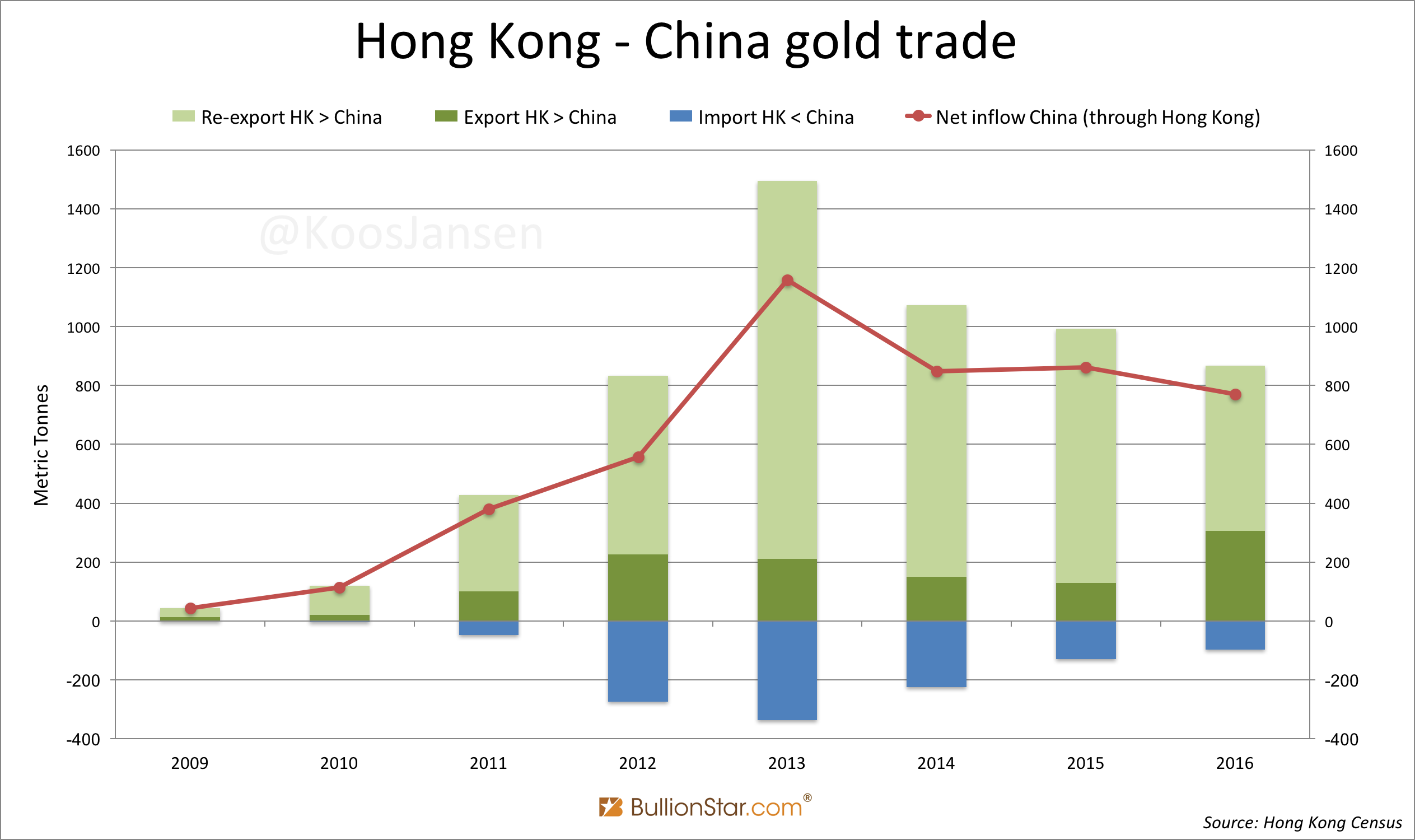

On a side note, the amount of gold used in round tripping can be at most the amount of gold yearly exported from China (to Hong Kong). Though the total exported gold will also contain genuine processing trade, so round tripping will likely be less than this amount.

Round tripping does not inflate net export from Hong Kong to China, only gross trade. The net amount of gold imported into China is shipped through general trade, via the SGE, into the Chinese domestic gold market and is prohibited from being exported.

In the chart above we can see China exported 330 tonnes to Hong Kong in 2013. Let’s guess 200 tonnes of that was genuine processing trade (jewelry manufactured in a Chinese CSSA).

330 – 200 = 130 tonnes

Possibly, there was 130 tonnes imported into China for round tripping and subsequently exported back to Hong Kong. Or, 10 tonnes was imported into China for round tripping and subsequently exported to be round tripped an additional 12 cycles, making 13 rounds in total.

13 x 10 = 130 tonnes

In the latter scenario a lot less physical gold is involved (10 tonnes versus 130 tonnes). In reality it’s more likely a gold batch used in round tripping is making multiple rounds than one round.

The Chinese Gold Lease Market

The other gold financing deal that can be conducted by Chinese speculators is gold leasing (which is the same as gold lending). In general gold leasing is a normal market practice.

To become familiar with the lease market I have categorized all potential gold lessees (borrowers) in three groups for us to have a look at examples (with US dollars) of how gold lending is done in financial markets:

- A gold miner needs funds to invest in new production goods. It can borrow dollars from a bank at a 7 % interest rate, or borrow gold at 2 % – the gold lease rate is usually lower than the dollar interest rate. The miner chooses to borrow 10,000 ounces and sells it spot at $1,500 an ounce. The proceeds are $15,000,000 that can be used to invest in new production goods. In a years time the miner has mined 10,200 ounces to repay the principal debt plus interest (the interest on gold loans can be settled in gold or dollars, depending on the contract). Through gold leasing the miner has acquired cheap funding compared to a dollar loan.

- A jeweler needs funds to buy gold stock for production. It can borrow dollars from a bank for 7 %, or borrow gold for 2 %. The jeweler borrows 10,000 ounces of gold, with which it can start fabricating jewelry. To hedge itself against price fluctuations the jeweler can sell spot, for example, 10 % of the 10,000 ounces it has borrowed (1,000 ounces at $1,500 makes $1,500,000) to buy gold futures contracts in order to lock in a future price. After a year the jeweler has sold the 9,000 ounces (as jewelry) for dollars and can take delivery of the long futures contracts to repay the gold loan.

- A speculator is looking for cheap funds. It can borrow dollars from a bank for 7 %, or borrow gold for 2 %. He borrows 10,000 ounces and sells it spot at $1,500 an ounce. The proceeds are $15,000,000 and subsequently these newly acquired funds can be used to invest in higher yielding products (> 2 %). If the trader chooses to hedge itself in the futures market is up to him. After a year the 10,000 ounces plus interest need to be repaid, either the trader can purchase gold with the profits made on the higher yielding investment or from delivery of futures contracts.

In China gold leases are settled and transferred through the SGE. The mechanics of the lease market in China was best described in an essay by the PBOC from 2011:

…the SGE provides a crucial role in gold leasing. The SGE’s block trading system is the trading platform used by gold leasing participants; the SGE also provides transfer and settlement services.

…

China’s gold leasing does not involve the central bank. Gold leasing takes place between commercial banks and enterprises as well as between commercial banks, the former being key.…

- An enterprise that intends to be a lessee approaches a branch office of a commercial bank with a rate request and application.

- The commercial bank carries out due diligence and then submits a review to their head office for approval.

- Upon approval the head office quotes a lease rate with the international gold lease rate as a benchmark plus additional basis points taking into account the potential lessee’s credit, physical gold management costs and other factors.

- If the potential lessee accepts the offer, a commercial bank branch manager will sign a lease contract with the customer including the terms and conditions clearly laid out.

- According to the “Shanghai Gold Exchange Lease Transfer Procedure”, after signing the lease, the head office of the commercial bank and lessee, or his agent, shall make a lease application through the exchange’s membership system. After verification, the SGE shall transfer the commercial bank’s gold from its SGE bullion account to the lessee’s SGE bullion account. The lessee can now trade the physical gold that it has leased or withdrawal the gold from the vaults.

- Upon expiration of the lease the lessee shall deposit or purchase physical gold through the SGE to repay the gold. Corresponding physical gold will be transferred from the lessee’s SGE bullion account to the commercial bank’s bullion account. Leasing fees involved will be settled in currency. At this point, the lease is completed.

I would like to insert a comment supplementing the PBOC’s description of gold leasing in the Chinese domestic gold market. In the paper it says:

“After verification, the SGE shall transfer the commercial bank’s gold from its SGE bullion account to the lessee’s SGE bullion account. The lessee can now trade the physical gold that it has leased or withdrawal the gold from vaults.”

My source at ICBC’s precious metals trading desk told me ICBC has little gold of itself for leasing, most of the gold lend out is sourced from third parties. These parties are either SGE members or overseas banks that supply gold through the Chinese OTC market. ICBC operates in the lease market as an intermediary by connecting supply and demand, it can lease from international banks or local gold owners with an SGE Bullion Account and lend the gold to miners, jewelers or speculators. My suspicion is that the international gold lease rate is lower than the Chinese gold lease rate, which can attract gold from the international market into the Chinese domestic gold market.

The Chinese lease market in short: in China all gold leases are settled through the SGE (there can be an off-SGE lease market, but it would be highly illiquid). Both lessor (lender) and lessee (borrower) are required to have an SGE Account. If a lease is agreed between two parties gold is transferred from one SGE Bullion Account to the other, when the lease comes due the gold is returned. At SGE level it’s as simple as that.

There is a big difference between jewelers that lease gold in contrast to miners and speculators. Jewelers lease gold because they need physical gold for fabrication; miners and speculators lease gold because they are seeking cheap funds, they will always sell spot the leased gold (without withdrawing the metal) at the SGE to use the proceeds. Why would a speculator withdrawal the metal?

Therefor, if SGE withdrawals capture leased gold this is for genuine jewelry fabrication that eventually ends up at retail level. When a jeweler needs to repay the lease it simply buys gold at the SGE to subsequently transfer it from its SGE Bullion Account to the lessor’s SGE Bullion Account. It’s not likely a jeweler would buy gold off-SGE to repay a lease, which then would need to be refined into newly cast bars by an SGE approved refiner to enter the SGE vaults. Gold leasing by jewelers can increase SGE withdrawals (for genuine gold business) but not so much supply to the SGE.

In a report the World Gold Council (WGC) released in April 2014, China’s gold market: progress and prospects, it was stated:

… No statistics are available on the outstanding amount of gold tied up in financial operations … but Precious Metals Insights [PMI] believes it is feasible that by the end of 2013 this could have reached a cumulative 1,000t…

This 1,000 tonnes figure is based on a misunderstanding regarding the Chinese gold lease market. PMI assumed there was 1,000 tonnes of gold tied up in financing deals based on the yearly lease volume in China, which was 1,070 tonnes in 2013. However, the yearly lease volume is not the gold that is leased out at any point in time, but reflects the aggregated volumes disclosed on all lease contracts that are executed over one year’s time in the Chinese domestic gold market (turnover). Meaning, if 100 mining companies lease 2 tonnes of gold for 1 month in 2016 and all leases are rolled over 4 additional months, the yearly lease volume would be 1,000 tonnes (100 x 2 x (1 + 4)), while on 31 December 2016 the total amount of gold leased out could be nil. (It’s impossible there was 1,000 tonnes used in round tripping as gross export from China has never been more than 330 tonnes)

In addition, the WGC used the words ‘tied up‘ for the gold used in financing operations, which sounds as if the market will be flooded when the gold is untied. The words ‘tied up’ can be misleading, let me explain: If a speculator borrows gold he will promptly sell it spot, this gold will not leave the SGE system. During such a lease period there is nothing tied up, there is just a debt to be repaid. When the lease comes due the lessee has to buy gold in the market (SGE) to settle the debt, which is the opposite of what the WGC insinuates what happens when gold is untied. In case a jewelry company leases gold the words tied up are more appropriate, in my view, as the borrowed gold bars are in transit from being processed to being sold as jewelry. Gold involved (tied up) in these leases can only be a share of the total amount of gold leased out in any point in time, because we all agree most leases in China are done for financing. There is only a small percentage of total gold loans tied up by jewelry companies.

Phillip Klapwijk, analyst with Precious Metals Insights (PMI) in Hong Kong, previous Executive Chairman of Thomson Reuters GFMS and consultant for the World Gold Council, has stated:

… a good part of the withdrawals represent gold that is used purely for financing and other end-uses that are not equivalent to real consumption.

Needless to say I don’t agree for the reasons just mentioned regarding gold leasing (speculators and miners borrowing gold will never withdraw the metal). Am I the only one? No. When Na Liu of CNC Asset Management Ltd, visited the SGE in May 2014 he spoke to the President of the SGE Transaction Department. From Na:

First, the withdrawal data reflects the actual gold wholesales in China. In 2013, the total gold withdrawal from the SGE vaults amounted to 2,196.96 tonnes. The President of SGE Transaction Department (The President) said: “This 2,200 tonnes of gold, after leaving our vaults, they entered thousands of Chinese households in the form of jewellery and investment purchases.”

… Second, none of the 2,200 tonnes of gold was bought by the Chinese central bank. The President said: “The PBOC does not buy gold through the SGE.”

… Third, the financing deals do not exaggerate SGE’s assessment of China’s gold demand. This is because “the financing deals do not take place after the gold leaves the vaults.”

The President of the SGE’s Transaction Department is clearly stating most leasing happens within the SGE system and this metal is not withdrawn. Therefor, gold leasing by speculators does not inflate SGE withdrawals and thus does not explain the difference between SGE withdrawals and Chinese consumer gold demand as disclosed by the GFMS.

Remarkably, when I asked the WGC about the details in 2014 they replied [brackets adde by Koos Jansen]:

Gold leasing: Banks have built up this business to support China’s burgeoning gold industry. Miners, refiners and fabricators all have a requirement to borrow gold from time to time. For example, fabricators borrow gold to transform into jewelry, sell and then repay the bank with the proceeds. It is an effective way for the fabricator to use the bank’s balance sheet to fund its business. Banks have strict policies in place for who they can lend to, and these have been tightened over recent years, but during PMIs field research it identified that, in some instances, organizations other than genuine gold business had used this method to obtain gold, which it would then sell to obtain funding [in this case the gold wouldn’t be withdrawn from the SGE vaults]. It would then hedge its position. According to PMI, this can generate a lower cost of funding than borrowing directly from the bank. Our colleagues in China think this would be a very small part of total gold leasing; the majority of it would be used to meet the demands of genuine gold businesses.

In their email the World Gold Council admits gold leases that are withdrawn from the SGE vaults are used for genuine gold business and being part of true gold demand. This is more confirmation gold leasing cannot explain the difference.

More recently (August 2016) the World Gold Council officially stated little borrowed gold leaves the SGE system [brackets added by me]:

Over recent years we have observed a rising number of commercial banks participating in the gold leasing market. … It’s estimated that around 10% of the leased gold leaves the SGE’s vaults. The majority is for financing purposes and is sold at the SGE [and stays within the SGE vaults] for cash settlement.

In conclusion, (i) round tripping gold flows are completely separated from the Chinese domestic gold market (SGE) and therefor cannot have caused the difference. In addition, (ii) gold leasing only inflates SGE withdrawals when used for genuine gold business and therefor cannot have caused the difference either.

More detailed information about the Chinese gold lease market can be found in my posts A Close Look At The Chinese Gold Lease Market, Gold Chat About The Chinese Gold Lease Market, Zooming In On The Chinese Gold Lease Market, Chinese Gold Leasing Not What It Seems and Reuters Spreads False Information Regarding The Chinese Gold Lease Market.

Popular Blog Posts by Koos Jansen

China’s Secret Gold Supplier is Singapore

China’s Secret Gold Supplier is Singapore

Audits of U.S. Monetary Gold Severely Lack Credibility

Audits of U.S. Monetary Gold Severely Lack Credibility

China Gold Import Jan-Sep 797t. Who’s Supplying?

China Gold Import Jan-Sep 797t. Who’s Supplying?

The Gold-Backed-Oil-Yuan Futures Contract Myth

The Gold-Backed-Oil-Yuan Futures Contract Myth

Estimated Chinese Gold Reserves Surpass 20,000t

Estimated Chinese Gold Reserves Surpass 20,000t

PBOC Gold Purchases: Separating Facts from Speculation

PBOC Gold Purchases: Separating Facts from Speculation

U.S. Mint Releases New Fort Knox Audit Documentation

U.S. Mint Releases New Fort Knox Audit Documentation

China Net Imported 1,300t of Gold in 2016

China Net Imported 1,300t of Gold in 2016

Why SGE Withdrawals Equal Chinese Gold Demand and Why Not

Why SGE Withdrawals Equal Chinese Gold Demand and Why Not