Confusion at the LBMA Conference About Gold Round Tripping

Koos Jansen

Koos JansenMuch to my surprise speakers at the LBMA conference in Vienna (held from 18 until 20 October 2015) have been discussing how gold round tripping and gold leasing in China inflates withdrawals from the vaults of the Shanghai Gold Exchange (SGE). These Chinese Commodity Financing Deals (CCFDs), which gold round tripping and gold leasing can be labeled as, were presented at the conference as the explanation for the huge difference between SGE withdrawals and Chinese consumer gold demand as disclosed by the World Gold Council (WGC).

By any measure the aggregated difference has transcended 2,500 tonnes of gold, which is more than the official gold reserves of Russia, India, Singapore, South Africa and Mexico combined. If CCFDs could inflate SGE withdrawals it would be a legitimate argument to lodge with, but gold round tripping cannot inflate SGE withdrawals and gold leasing can only inflate SGE withdrawals to a limited extent (not 2,500 tonnes).

Regular readers of this blog know I’ve written numerous articles about CCFDs and that I have clearly exposed round tripping and gold leasing cannot explain the difference the gold space is apparently still ignorant about. Once more we’ll thoroughly set out all the gossip that is making rounds about CCFDs and elucidate the true workings of the Chinese gold market. This post is focused on round tripping, or actually about the rules on the import and export of gold in and out of China, in a succeeding post we’ll extensively discuss gold leasing.

Back to the LBMA conference, this is what I think has happened. On 20 October at 12:15 pm the following BullionVault tweet was published live from the LBMA conference in Vienna:

Numbers complex, but huge gap between SGE withdrawals and demand data is simple – leasing + round tripping #LBMA

— BullionVault (@bullionvault) October 20, 2015

The same message was tweeted 18 minutes later by Mark O’Byrne from Goldcore who was attending the LBMA conference as well:

Is ‘complex’ but huge gap between SGE withdrawals a& demand data is simple – leasing & round tripping #LBMA cc @ronanmanly

— Mark O’Byrne (@MarkTOByrne) October 20, 2015

From looking at the programme of sessions and speakers on 20 October (click here to view the schedule and slides presented) I assume the message in the tweets was supplied by a panel that was on stage halfway the conference day. As, the moment this panel was talking could very well have coincided with the moment the tweets were published, 12:15 pm and 12:33 pm. The panel on stage consisted of:

- Raymond Key, Senior Partner & Head of Metals & Mining, TrailStone Australia Pty Ltd

- Albert Cheng, Advisor to World Gold Council

- Anne Dennison, Consultant, LPPM

- Jeremy East, Managing Director, Head, Metals Trading & Commodities, Northeast Asia and Greater China, Financial Markets, Standard Chartered Bank

- Philip Klapwijk, Managing Director, Precious Metals Insights Limited

- Gerry Schubert, Founder, Schubert Commodities Consultancy, DMCC

The members of the panel Cheng, East and Klapwijk are known for having an interest in the Chinese gold market, so it would make sense for them to come up with the statements the tweets referred to.

In addition, in the morning of 20 October the second speaker on the programme was Jiang Shu, Chief Analyst of Shandong Group (click here to view the slides from Jiang). Let’s have a look at his slides, here is number three:

The header of the slide says, “China’s Demand Is Thought To Be Inflated: Two Possible Sources”. Obviously, Jiang’s keynote speech is about the difference between SGE withdrawals and Chinese consumer gold demand, for which Jiang mentions two possible causes, (i) commodity financing deals “which use the import and export of gold”, here Jiang refers to round tripping, and (ii) gold leasing.

So, likely in the morning of 20 October Jiang talked about the difference in the Chinese gold market and CCFDs, a few hours later the panel chatted along the same lines, which (again) seduced a big chunk of the international gold community to think the difference in the Chinese gold market is simply caused by Chinese Commodity Financing Deals.

Attendants of the LBMA conference must have reasoned, “if a gold analyst from China (Jiang) is saying CCFDs cause SGE withdrawals to inflate and experts like Cheng, East and Klapwijk agree with him it must be true”. On 23 October Sharps Pixley published an article that quoted Jiang and stated gold leasing is to blame for the +2,500 tonnes difference. The same day Dundee Capital Markets (Martin Murenbeeld) published a newsletter:

…These totals leave some unanswered questions. Where do the extra 500 tonnes of gold end up (the 500 tonne difference between domestic production plus net imports minus domestic consumption)? And what does the 1000-tonne difference between total SGE deliveries and the 1600 tonnes of domestic production and imports imply?

The first answer is that the extra 500 tonnes are likely to end up 1) in PBoC reserves and 2) in commercial bank stocks to support gold leasing transactions, and such. (Lawrie Williams, writing on the Sharps Pixley website, alluded to a presentation at this year’s LBMA meeting in Vienna, in which an analyst from the Shandong Group suggested some 1,370 tonnes of gold are now tied up in leasing arrangements…).

This is how information spreads through the gold space.

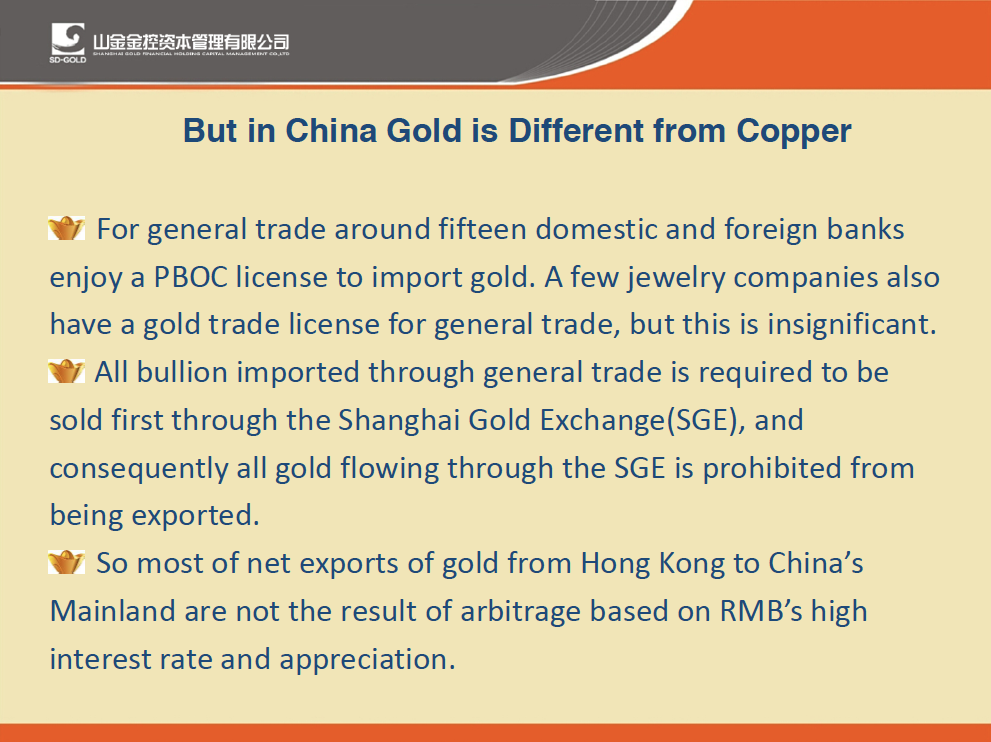

When I read Jiang’s slides I sensed a feeling of familiarity with the words. Reading some of my own posts on CCFDs confirmed my hunch; Jiang had copied my writings. Below is slide number seven from Jiang:

Jiang’s second point is an exact copy from my post “Chinese Gold Trade Rules And Financing Deals Explained”, in which I wrote:

For general trade fifteen banks enjoy a PBOC license to import gold.

…

All bullion imported through general trade is required to be sold first through the SGE, and consequently all gold flowing through the SGE is prohibited from being exported. Detail: a few jewelry companies also have a gold trade license for general trade, but this is insignificant.

We can also see that Jiang’s first point is a composition of my writings, the second sentence being an exact copy. Apparently Jiang reads my blog and uses the content for his own analysis. This is noteworthy as it influences our qualification of Jiang’s independent expertise.

Since I have not attended the LBMA conference I don’t know if Jiang gave me verbal attribution, but me thinks chances are slim. I don’t have a problem with colleague gold analysts consulting my writings and using it for their own reports or presentations, but attribution is a requisite, especially when writings are copied one on one. Unfortunately, this is not a single occurrence. Frequently I come across writings from colleagues that resemble my work remarkably close – you know who you are. I would kindly suggest everyone adds full and proper attribution.

Round Tripping Does Not Inflate SGE Withdrawals

To understand why round tripping cannot inflate SGE withdrawals, we need to get more familiar with how goods can be imported into and exported from China. There are two types of cross-border trade with China: general trade and processing trade.

Only through general trade gold can be imported into the Chinese domestic gold market where it’s required to be sold first through the SGE. Gold imported through processing trade must be used for manufacturing or assembling purposes after which the finished goods are required to be exported.

Processing trade is meant for China’s manufacturing industry to efficiently connect with the rest of the world. The Chinese and foreign companies engaging in processing trade are exempt from, in example, import duties and value added tax.

Often processing trade is conducted through Customs Specially Supervised Areas (CSSAs) – also called Customs Specially Regulated Areas, Special Customs Supervision Areas or Customs Special Supervision Regions, these are all the same. When processing trade is performed outside CSSAs (the rest of the mainland, non-CSSA) the materials will be strictly monitored by Chinese customs.

In this post I will demonstrate round tripping can only be done through processing trade in which it cannot enter the Chinese domestic gold market or interfere with the SGE system. Consequently, round tripping cannot inflate SGE withdrawals and thus has nothing to do with the difference we’re after.

Customs Specially Supervised Areas

CSSA is a collective noun for free trade zones, export processing zones, bonded logistics parks, bonded ports, comprehensive bonded zones, etc. Without going into detail what the differences are between various types of CSSAs, all such areas must be seen as regions in China mainland where rules for taxes, customs and foreign exchange administration can be different from the rest of the mainland.

Through CSSAs cross-border trade between China mainland and foreign countries can be established without China having to fully open up its borders. By slowly increasing the number of CSSAs and easing cross-border trade rules between these areas and the rest of the world, the State Council gradually allows China to open up. Hong Kong is not a CSSA, but a Special Administrative Region of the People’s Republic of China. In terms of trade Hong Kong must be treated as a separate country from China mainland, having its own customs department and currency.

Some CSSAs are physically open to the rest of the mainland, people are free to go in and out without being asked to show documentation by Chinese customs, others are restricted, surrounded by a fence and goods moved in or out can be subject to checks.

Processing Trade vs General Trade

To study processing trade we’ll use the official PRC Customs Supervision and Administration of Processing Trade Goods Procedures (2004) and Managing Trade & Customs in China (2011, KPMG) as our guides. To avoid misunderstandings, henceforth we’ll work with the nomenclature provided in these documents. According to the PRC Customs Supervision and Administration of Processing Trade Goods Procedures the definition of processing trade is:

“Processing trade” shall refer to the business activity of import of operating enterprises of all or some raw and auxiliary materials, components, parts, mechanical components and packing materials (Materials and Parts) and the re-export thereof as finished products after processing or assembling. It includes processing of supplied materials and processing of purchased materials.

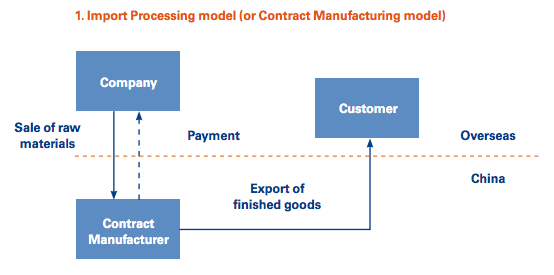

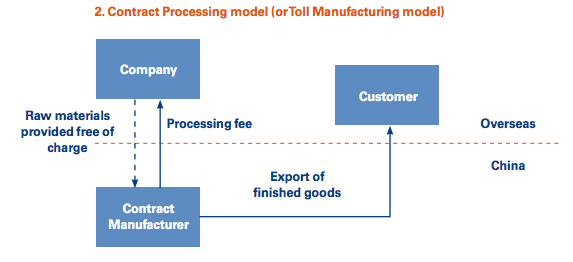

Let’s examine the two types of processing trade to get a better understanding of the wider concept. There is the Processing Of Purchased Materials Model (or Contract Manufacturing model) and the Processing Of Supplied Materials Model (or Toll Manufacturing model).

The Processing Of Purchased Materials Model involves a Chinese manufacturer to import raw materials and parts from abroad into China (a CSSA) to assemble or process into finished goods. Upon completion the finished goods will be exported and sold in an overseas market by the Chinese manufacturer.

The Processing Of Supplied Materials Model involves a foreign company to export raw materials and parts to China (a CSSA) to be processed by a Chinese manufacturer into finished goods. Upon completion the finished goods are exported to an overseas market to be sold at the discretion of the foreign company. This foreign company will pay the Chinese manufacturer a processing fee for its services provided.

Example given of a processing trade with gold:

Bullion from Hong Kong is exported to the CSSA in Shenzhen where 4,000 Chinese gold manufacturers are located. Subsequently, the gold is fabricated into jewelry and upon completion imported back into Hong Kong to be sold in jewelry shops. This trade can be either conducted through the Processing Of Purchased Materials Model or the Processing Of Supplied Materials Model.

Essential to understand is that the flow of gold in processing trade is completely separated from the Chinese domestic gold market, though this gold crossing the Chinese border is included in customs statistics. From the PRC Customs Supervision and Administration of Processing Trade Goods Procedures we can read:

Article 21. Goods imported and exported by operating enterprises in the form of processing trade shall be included in customs statistics.

Processing trade – and the rules just mentioned – explains how gold can be imported into China from Hong Kong and exported back from China to Hong Kong.

As you can see in the chart above there is a difference between gross gold trade and net gold trade, which is caused by processing trade.

Now we understand processing trade, let us move on to study trade between the Chinese domestic market and foreign countries.

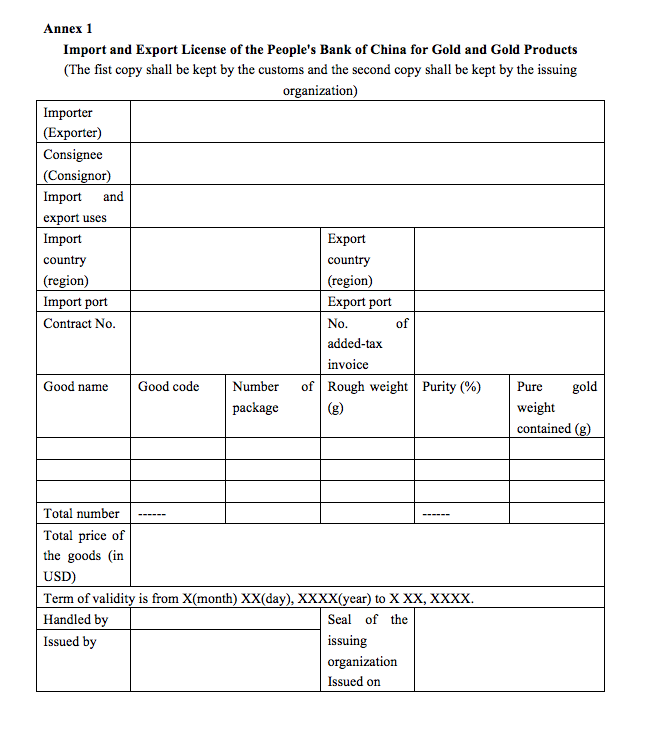

If goods are imported into/ exported from the Chinese domestic market this is referred to as general trade. Regarding general trade the rules for gold diverge from the rules for all other commodities. The agency that controls all forms of gold in general trade is China’s central bank, the People’s Bank Of China (PBOC). Only financial institutions and gold enterprises that carry the Import and Export License of the People’s Bank of China for Gold and Gold Products (The License hereafter) can get gold to pass customs into the Chinese domestic gold market. Recently BullionStar published the translation of the official Measures for the Import and Export of Gold and Gold Products (The Measures hereafter) drafted by the PBOC in March 2015. For the first time these rules are now publicly available in English. From The Measures we can read:

For the import and export customs clearance of gold and gold products as included in the Catalogue for the Regulation of the Import and Export of Gold and Gold Products, the Import and Export License of the People’s Bank of China for Gold and Gold Products (Annex 1) issued by the People’s Bank of China or a People’s Bank of China branch shall be submitted to the Customs.

The Catalogue for the Regulation of the Import and Export of Gold and Gold Products (click here to view) describes all forms of gold (powder, coins, bullion, unwrought, scraps, jewelry) that can cross the Chinese border. For gold to be imported into the Chinese domestic gold market the material is required to be accompanied by The License.

Currently there are fifteen commercial banks that can apply for The License to import standard gold, which in the Chinese system is bullion in bar form weighing 50g, 100g, 1Kg, 3Kg or 12.5Kg, having a fineness of 9999, 9995, 999 or 995. The fifteen commercial banks are:

- Shenzhen Development Bank / Ping An Bank

- Industrial and Commercial Bank of China

- Shanghai Pudong Development Bank

- Agricultural Bank of China

- China Construction Bank

- Bank of Communications

- China Merchants Bank

- China Minsheng Bank

- Standard Chartered

- Bank of Shanghai

- Industrial Bank

- Bank of China

- Everbright

- HSBC

- ANZ

All standard gold imported through general trade into the Chinese domestic gold market is required to be sold first through the SGE (the core of the Chinese domestic gold market). From The Measures we can read [brackets added by me]:

… An applicant for the import and export of gold … shall have corporate status, … it is a financial institution member or a market maker on a gold exchange [SGE] approved by the State Council.

… The main market players with the qualifications for the import and export of gold shall assume the liability of balancing the supply and demand of material objects on the domestic gold market. Gold to be imported … shall be registered at a spot gold exchange [SGE] approved by the State Council where the first trade shall be completed.

Next to standard gold there is non-standard gold in the Chinese system, for example bullion bars weighing 1,040 gram, jewelry, coins, ore and doré. Non-standard gold is not required (and not allowed) to be sold through the SGE when imported into the Chinese domestic gold market. Only a very limited number of gold enterprises can apply for The License to import non-standard gold under general trade. Although, The Measures released in March 2015 by the PBOC loosened the requirements for The License.

Example given of a gold enterprise that can import non-standard gold into the Chinese domestic gold market:

On 26 May 2015 Zijin Mining Group bought a 50 % stake in Barrick Gold Corp’s Porgera mine in Papua New Guinea for $298 million. On 9 October 2015 China Gold Network wrote that Zijin Mining was one of the first mining companies to be granted the qualification by the PBOC to import gold under general trade, allowing Zijin to import doré from Papua New Guinea into the Chinese domestic gold market. Note, if the dore is imported and refined into standard gold, the bars are required to be sold through the SGE.

From China Gold Network:

9月25日,紫金矿业获得中国人民银行批复允许从事黄金进口业务,打破了国内只有金融机构从事该业务的惯例,开创了国内大型黄金企业从事黄金进口业务的先河。

Translated [brackets added by me]:

On Sept 25, Zijin Mining was granted by the People’s Bank of China the permission to do gold import business [under general trade], which broke the common practice that in China only financial institutions do this business, and became the first case that a big domestic gold miner does gold import business [under general trade].

By loosening the rules for enterprises to import non-standard gold into the Chinese domestic gold market the PBOC has helped Chinese mining companies to strive for more overseas acquisitions.

Above we can see The License form that commercial banks have to fill in for every gold import. Being able to apply for The License does not grant unlimited permission to import gold into the Chinese domestic gold market – from abroad or CSSAs – as for every shipment a stamp from the PBOC is needed. From the Measures we can read:

There shall be one Import and Export License of the People’s Bank of China for Gold and Gold Products for each batch of product and the License shall be used within 40 work days since the issuing date.

Gold export from the Chinese domestic market is prohibited by the PBOC (except for golden Panda coins). The reason The Measures mention export is because if the PBOC would ever change its policy in allowing gold export from the Chinese domestic gold market it doesn’t need to rewrite all the rules. Currently, if one of the fifteen banks (or Zijin) will submit a request at the PBOC for an export license it will be rejected.

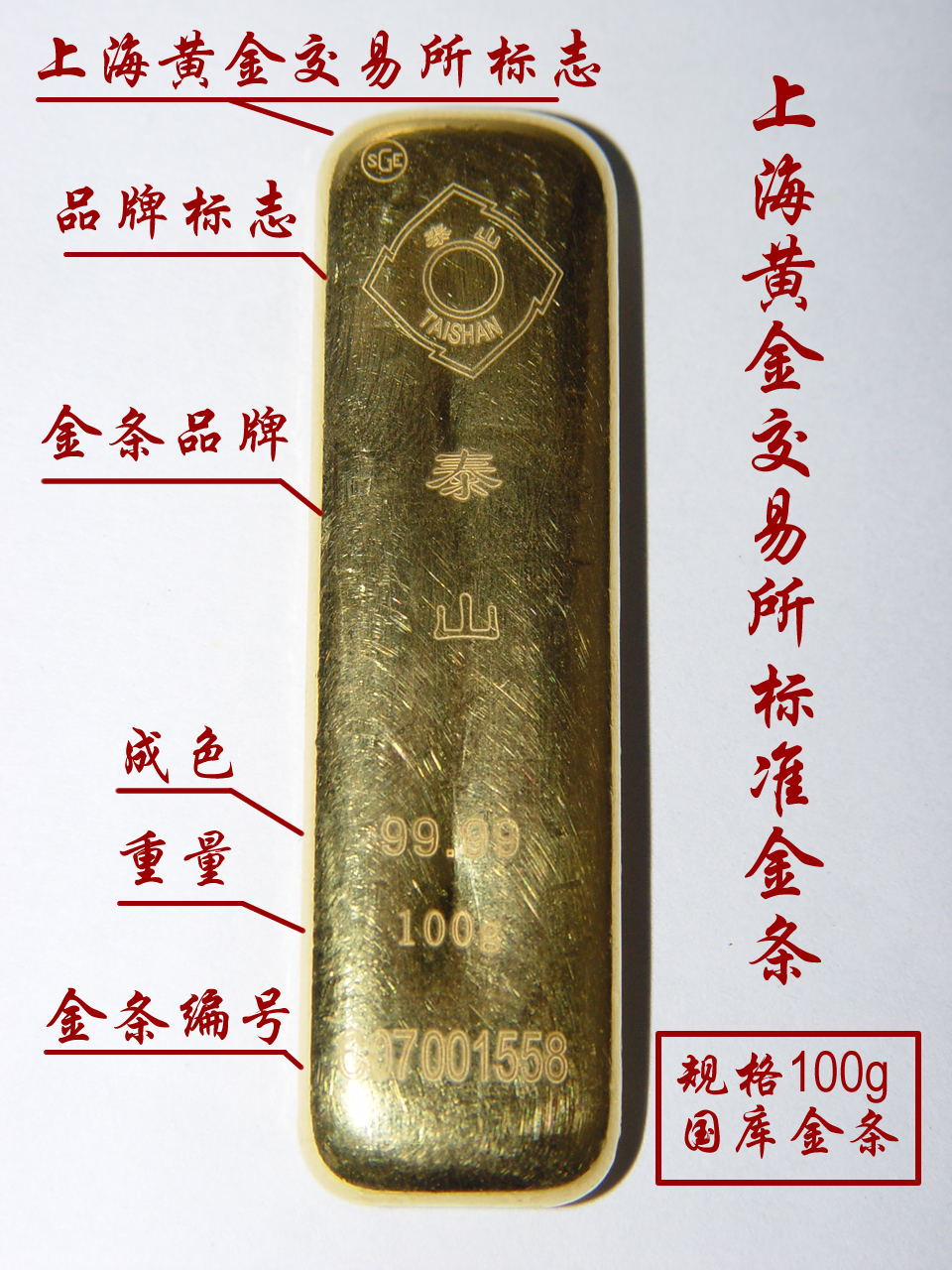

Has anybody ever seen an SGE bar outside China mainland? Likely not. This is because the SGE system operates in the Chinese domestic gold market and thus bars withdrawn from the SGE vaults are prohibited form being exported.

1. 上海黄金交易所标准金条 SGE Standard Gold Bar.

2. 上海黄金交易所标志 SGE Logo.

3. 品牌标志 Brand Logo.

4. 金条品牌 Bar Brand (泰山 is Mount Tai, which is produced by Shandong Gold).

5. 成色 Fineness.

6. 重量 Weight.

7. 金条编号 Bar Number.

However, there is one possibility to export an SGE bar from the Chinese domestic gold market. Individuals can bring 50 grams of gold when traveling abroad. Though this rule is not very stringent on the import side, on the export side one individual would be allowed to bring a 50g SGE bar across the border, two individuals would be allowed to bring a 100g SGE bar with them, etc.

More important, through processing trade enterprises not carrying The License can import and export gold. From The Measures we can read:

…, gold and gold products imported and exported by the following means shall exempted from handling Import and Export License of the People’s Bank of China for Gold and Gold Products and shall be supervised by the customs instead:

… Imported or exported by processing trade…

There you have it. Enterprises can import gold into and export from China through processing trade without The License from the PBOC – because CSSAs are separated from the Chinese domestic gold market. These enterprises are required to be engaged in gold business, for example, as jewelers or refiners.

Gold trade between a CSSA and the Chinese domestic market is considered as general trade. Meaning, for gold to be imported from the Shanghai Free Trade Zone into the Chinese domestic gold market The License must be provided.

From slide number six of Jiang we can read his description of round tripping:

The way Jiang explains round tripping is exactly what Goldman Sachs wrote in 2014 (what a coincidence), though I agree this is how the scheme is executed. In Jiang’s slide we can clearly see round tripping is done through processing trade. The reason being, gold trade rules in China dictate enterprises can only import and export gold without The License through processing trade. The only possibility to round trip gold in China is through processing trade, which requires the gold to be physically imported and exported. Goldman Sachs correctly pointed out in 2014 [brackets added by me]:

…Chinese gold financing deals [round tripping] are processed in a different way compared with copper financing deals, though both are aimed at facilitating low cost foreign capital inflow to China. Specifically, gold financing deals [round tripping] involve the physical import of gold and export of gold semi-fabricated products to bring the FX into China; as a result, China’s trade data does reflect, at least partially, the scale of China gold financing deals.

By and by, not every enterprise is approved by Chinese customs to conduct processing trade. If speculators wish to illegally engage in gold round tripping they must erect a shell gold company (like a jewelry company). Under this disguise the gold can be imported into/ exported from China through processing trade in order to round trip.

I wish to abstain from expanding on the fiat gains accrued by speculators in round tripping, as this is beyond the scope of this post. The key takeaway is that the physical gold flows involved in round tripping are separated from the Chinese domestic gold market and thus cannot interfere with the SGE system, let alone inflate SGE withdrawals. Because gold round tripping requires the metal to be imported and exported through processing trade it cannot possibly interfere with the SGE system.

Popular Blog Posts by Koos Jansen

China’s Secret Gold Supplier is Singapore

China’s Secret Gold Supplier is Singapore

Audits of U.S. Monetary Gold Severely Lack Credibility

Audits of U.S. Monetary Gold Severely Lack Credibility

China Gold Import Jan-Sep 797t. Who’s Supplying?

China Gold Import Jan-Sep 797t. Who’s Supplying?

The Gold-Backed-Oil-Yuan Futures Contract Myth

The Gold-Backed-Oil-Yuan Futures Contract Myth

Estimated Chinese Gold Reserves Surpass 20,000t

Estimated Chinese Gold Reserves Surpass 20,000t

PBOC Gold Purchases: Separating Facts from Speculation

PBOC Gold Purchases: Separating Facts from Speculation

U.S. Mint Releases New Fort Knox Audit Documentation

U.S. Mint Releases New Fort Knox Audit Documentation

China Net Imported 1,300t of Gold in 2016

China Net Imported 1,300t of Gold in 2016

Why SGE Withdrawals Equal Chinese Gold Demand and Why Not

Why SGE Withdrawals Equal Chinese Gold Demand and Why Not