The PBoC Was Buying Gold in London In The Nineties

Koos Jansen

Koos JansenI couldn’t resist translating this must read from 1993 in Dutch newspaper NRC Handelsblad (h/t @frankknopers) about the gold sales by the Dutch central Bank (DNB). Presumably, “a part” of the 400 tonnes sold at the time through the Bank For International Settlements went to the Chinese central bank. Although we don’t know for sure what the Chinese central bank did with the gold – at the time the People’s Bank Of China was the primary dealer in the Chinese domestic gold market and in theory could have sold the gold to Chinese jewelry fabricators – we may assume it was kept for its official reserves.

The other week I published an article about the Chinese Gold Army that was established in 1979 to develop domestic gold mining and exploration. This signifies the People’s Bank Of China (PBOC) was laying the foundation for the Chinese gold market in the seventies. Later on, in 2002 the PBOC started to liberalize the gold market by launching the Shanghai Gold Exchange that took over gold allocation and the pricing mechanism from the central bank. Many of us thought that the PBOC only became active in the international OTC gold market to diversify its lopsided US dollar reserves after, say, 2009. But we were wrong, the PBOC was buying gold in London as early as 1992. No, we don’t know exactly how much or what they did with the gold, though for sure the PBOC has been designing its gold strategy decades ago along side its opening up policy.

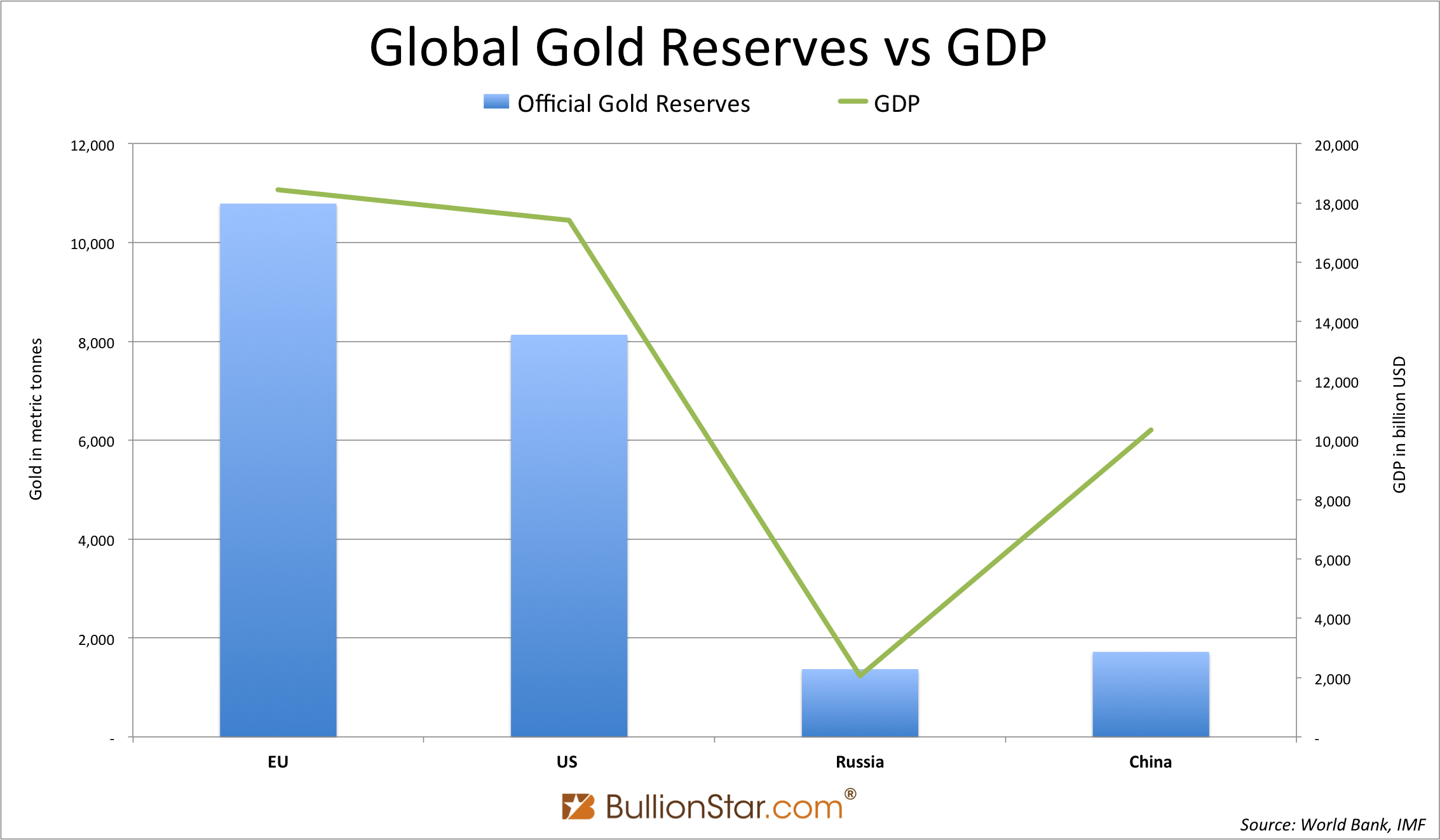

Remarkably, the article from NRC noted that the Dutch central bank sold gold “to equalize its holdings relative to other important gold holding nations” and “it’s known China is working to increase its gold reserves to bring it more in line relative to its GDP”. One of the theories about our current international monetary system – that was detached from gold in 1971 – is that it can only shift to a new gold anchored system when the power blocks have equalized the chips (Jim Rickards). In other words, if the US, Europe, Russia and China all have an equal ratio of official gold reserves to their GDP, the international monetary system could make a transition towards gold.

Within the aforementioned theory China should have about 6,000 tonnes to come to the gold/GDP ratio the EU and Russia have (the US has a little less gold proportionally). Although it’s impossible to know how much the PBOC really holds, it’s certainly more than what they disclose at the moment, which is 1,743 tonnes. In a forthcoming post we will discuss the most recent ins and outs regarding PBOC official gold reserves. For now, enjoy the full article.

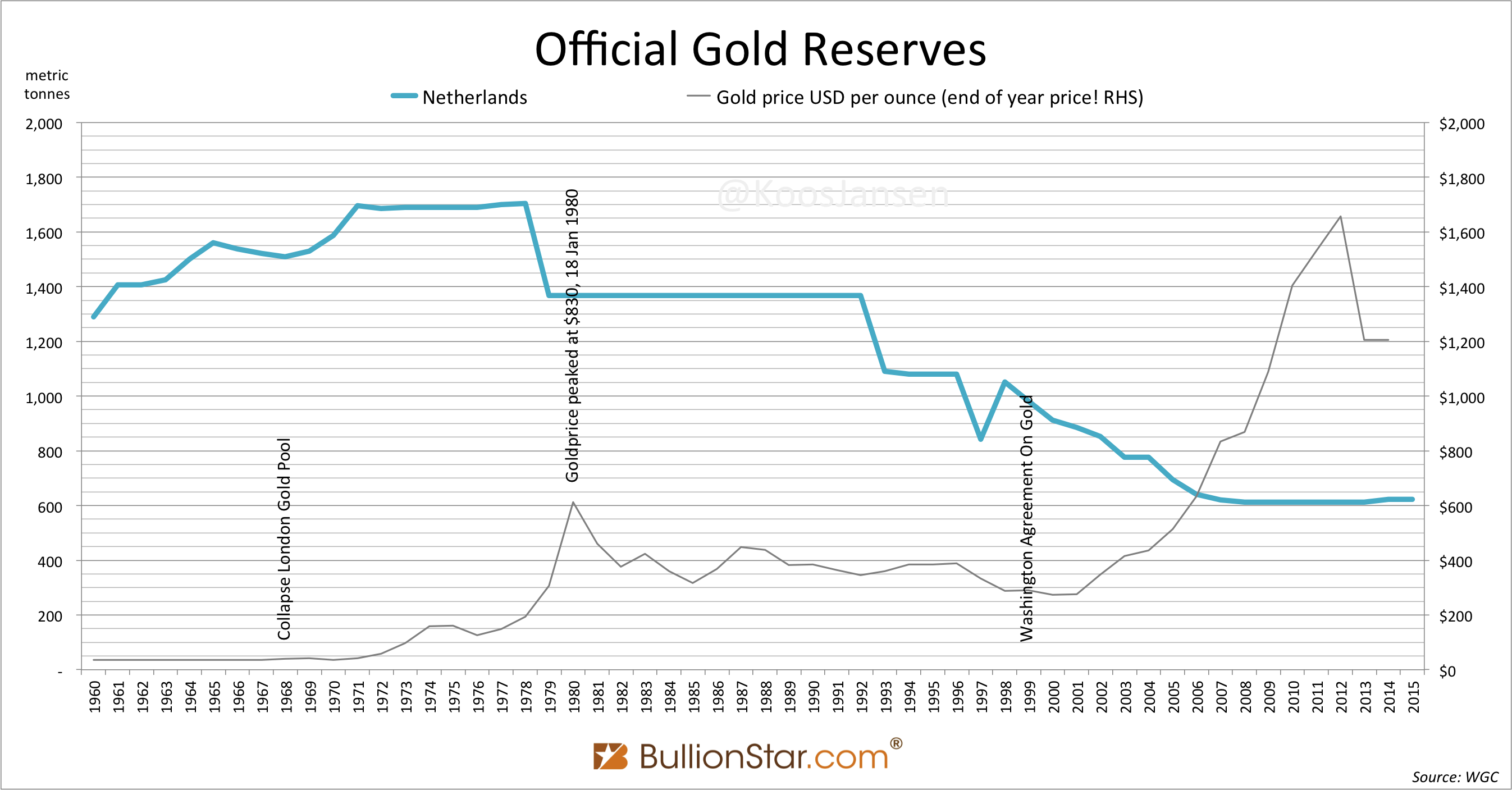

Note, at the time the article was published DNB held 1,090 tonnes of gold.

Operation Gold

(NRC Handelsblad, 27 March 1993).

Last summer the President of the Dutch Central Bank, W. Duisenberg, persuaded the Minister Of Finance, W. Kok, of the need to sell a quarter of the Dutch gold reserves: “The time is right”. Part of the Dutch gold was probably sold at the end of last year to the People’s Republic Of China. The multi billion operation that has taking place in utmost secret is producing the state an annual 400 million guilders in extra benefits since 1994. “Part of the sale was handled outside the market."

van Ewijk and L.J.R. Scholten: The profitability of De Nederlandsche Bank, in: ESB 1-7-1992. In ESB 19-8-1992 there was a sequel and in ESB 20-1-1993 both authors went on about the gold sales.

March 27, 1993

No. The gold of De Nederlandsche Bank [DNB] was not secretly loaded into a Chinese cargo plane at Schiphol and flown to Beijing. The gold of the Dutch Central Bank remained where it was, in the vaults of the Bank of England where it has been for years. Only the signs with the name of the owner of the gold bars were changed. A new name: for traders in the international gold market there is no doubt that the People’s Bank Of China (PBOC) has bought a part of the 400 tonnes of gold, a quarter of the Dutch gold reserves, which DNB has sold late last year in utmost secrecy.

“With 99 percent certainty we know that the People’s Bank of China has been one of the buyers of the Dutch gold”, said Philip Klapwijk from Goldfields Mining Services, an institute in London affiliated with the South African gold mines that specializes in research into the gold market. Also other London bullion dealers have a strong suspicion that China was involved in the gold sales of DNB. “We have noted that the Chinese central bank has bought gold in recent months”, said John Coley of the London bullion dealer Sharp Pixley and spokesman of the London Bullion Market Association.

At the Ministry of Finance in The Hague and at DNB in Amsterdam they know the story of the Chinese connection, but they remain tight lipped. “Everything is sold locally in London”, said the spokesman of DNB, JH du Marchie Sarvaas. The central bank is silent on the question of who was engaged in the sale and who the buyers were. “It is not in our interest to make announcements about it”, he said. Servaas will only tell us that the transactions have been set up in different ways and that DNB has not entered the market directly itself.

The spokesman of the Ministry of Finance, Dr. RP Florisson, stated not to know where the gold that was sold has gone. Some things, he added, you would rather not know. Members Of The House have neither any idea in what way the gold was sold. With the letter from 12 January by Kok that notified the Members Of the House about the gold sale came an attachment, though in it the ‘technical details’ from the original correspondence between Duisenberg and Kok were omitted. This was a crucial passage, which disclosed the name of the mediator in the gold sales, the Bank for International Settlements, the central bank of central banks.

The SellerPerhaps the phrase “silence is golden” finds its origin in the world of central banks. Like is the case in Operation Gold. In April 1992 DNB developed the intention to sell part of its gold stock and add the proceeds to its foreign exchange reserves. The Board Of Governors of the central bank, consisting of President Dr. WF Duisenberg and three other Directors, approved the plan. Only a few other employees were notified. In June Duisenberg shared his plan with Kok during one of their weekly lunch meetings. Kok hesitated at first because he feared he would be remembered as The Seller of the national gold.

Duisenberg explained that it was the sound fiscal policies from Kok and the strong position of the guilder that made the gold sales possible. Kok was persuaded. At the Ministry Of Finance the Deputy Comptroller General and the Director were informed. On 29 September Duisenberg sent a letter to Kok in which he explained that the sale was intended ”to equalize our gold holdings relative to other important gold holding nations”. The sale should not lead to loss of confidence in the guilder, not serve to fill the state coffers and not lead to disruption of the gold market. “Therefore, a high degree of secrecy is warranted”, Duisenberg wrote. If unexpected complications would arise DNB would waive the operation.

Kok agreed on 2 October and in the fall several sales transaction followed in the London forwards market. In addition, the Bank has for International Settlements (BIS) was involved as an intermediary. The BIS, which is based in Basel and was established in 1930 to administer the German reparations, is as closed as the Swiss banking secrecy. Who calls the BIS can enjoy the long version of Eine kleine Nachtmusik as on-hold music, to finally be told the BIS never releases any information.

Duisenberg expanded on the gold sales at a meeting of the BIS on 12 January 1993. The sale had already taken place, only the gold had yet to be delivered. Not all members of the BIS welcomed the Dutch move, nor were they consulted for its decision. That same day DNB published the news. A team from a TV news network was – under the pledge of secrecy –flown to Basel for an interview with Duisenberg. “The time is right” for the sale of part of the Dutch gold reserves, the President said.

The news dropped like a bomb. Rumors were circulating in the gold market late last year about possible Dutch gold sales, based on these rumors a reporter from news agency Reuters asked DNB for a response in November. It replied no announcements were ever made on market transactions. Gold traders were particularly surprised by the volume of sales: “It was very well done. I never knew that the market could absorb such an amount in such a short time without drastic price distortions”, said one gold dealer.

It was a huge deal. Four hundred tonnes is nearly a quarter of the total annual gold mine production. It is the equivalent to 32,000 gold bars of 12.5 Kg [400-ounce] and 26 centimeters in length, which placed end to end form of line of 8.32 kilometers. That is almost as long as the symbol of our national pride, the Oosterscheldedam.

With the sale DNB earned 7.5 billion guilders in US dollars, D-marks and Japanese yen that have been added to the foreign exchange reserves of the central bank. As these foreign exchange earn interest – unlike gold – the profit starting from 1994 is an annual 400 million guilders which will flow to the state coffers. Recent pleas from Members Of The House to invest this money in infrastructure have been rejected by Kok, who agreed with DNB that this amount, like other profits of the central bank, flow to the Treasury.

Economics Journal

Seldom a critical note is written about the policy of DNB. Coincidentally, last year, while Duisenberg was preparing the gold sales in secret, a remarkable article in the journal for economists, ESB, was published. Casper van Ewijk and Bert Scholten, both working at the economics department of the University of Amsterdam, questioned the profitability of DNB. They concluded that the central bank, with its relatively large reserves of gold and foreign exchange, yields an extremely poor result on its investments. With that, the annual profit payment to the Treasury is a lot lower than possible.

In a second article – after the gold sale – the two economists claimed that DNB had sold too little gold and had waited too long with the sale. Now the gold was sold for an average of 18,800 guilders per kilo, while ten years before it could have been twice that amount. In those ten years, the gold yielded not one cent and its value only declined. The addition of the gold to the foreign exchange reserves was in their opinion, “unnecessary and therefore undesirable”, as the Netherlands has more than enough foreign exchange reserves. And the revenue of the sale, according to Van Ewijk and Scholten, could be better used to reduce the national debt. That gives the government more financial benefit than an annual interest income.

The defense of DNB – as expressed in replies from the Minister Of Finance to questions by the parliament – is that a central bank is not a hedge fund. The gold and foreign exchange reserves are not intended to maximize returns but to conduct a proper exchange rate policy and to ensure confidence in the guilder. As a result, it is also necessary to hold currency that offers a low rate of return. The gold is not held for speculation, but is a cornerstone of the monetary policy of the Netherlands as a major gold holding nation. When deciding on the time at which it sold some of the gold, the gold price did not play any role whatsoever.

The suggestion to use the principal proceeds to flow to the treasury could no find grace: the change in the composition of reserves (gold was converted into US dollars, D-marks and yen) is not a reason to pour assets of the central bank into the hole of the national deficit. If DNB would give in to this temptation that would be a monetary sin: financing the government deficit by the central bank. That happens in South America, or in Italy, but not in countries that appreciate a hard currency.

Parity

Gold plays a vital role in finance since trade emerged. Late last century all European countries and the United States went on the classical gold standard. The direct link between the amount of money in circulation to gold reserves at central banks broke the economies of the industrialized countries in the economic depression of the thirties. The Netherlands held on to gold until 1936 as one of the last countries together with Switzerland and France.

After the Second World War the US dollar ruled. Under the Bretton Woods system, which was set up in 1944 under US-British leadership, all currencies were pegged to the US dollar. This provided stability and dynamics because the Americans constantly pumped new dollars into the world economy. The Bretton Woods system created unprecedented economic growth for a quarter of a century. The gold did not disappear completely. To increase the credibility of the system, the United States declared their readiness to ensure the conversion of dollars into gold at a fixed price of 35 dollars per troy ounce (31.1 grams). The Americans could easily make that offer, because in 1944 they were in possession of three quarters of all the gold reserves in the world.

The Dutch government in exile had largely spent its gold reserves during the war. During the reconstruction foreign exchange reserves piled up in the fifties and sixties and DNB happily took advantage of the opportunity to convert dollars that were earned through exports, for gold in the US. Together with France The Netherlands was in those years the largest gold accumulator. French President General Charles de Gaulle said, in a famous news conference on 4 February 1965, about the US dollar hegemony and gold, “Ah! Gold its nature never changes, not in any form, bars or coins. It has no nationality, it is held eternal and universal as the unchangeable and trustworthy value par excellence”. Also in The Netherlands gold was held as an article of faith.

During the sixties the US gold reserves in Fort Knox severely declined. Eventually, President Nixon decided in 1971 to temporarily suspend the convertibility of dollars into gold. The ‘gold window’ was closed; the world had spent well over twenty five years to tap into the US gold reserves.

Since 1971 the gold reserves of DNB hardly changed. The spectacular rise in gold price to $850 dollars per troy ounce in early 1980 led to a great gain in the books but that was all. However, politicians in the seventies had their greedy eyes on the gold stocks to use these for employment projects and other fun things for the people to finance. President of DNB at the time, Dr. Jelle Zijlstra, abhorred such ideas. Not a single gram of gold was sold from the vaults of DNB.

Zijlstra and his successor Duisenberg feared gold sales would affect the position of the guilder. Moreover, the government deficit was so huge in the eighties that sales would be interpreted by financial markets as weakness. Gold supported confidence in the guilder and provided an aura of invulnerability.

Drawbacks

During 1991 the gold inventories were casually mentioned in a conversation between senior officials of the Ministry Of Finance and DNB during the preparations for the Economic and Monetary Union (EMU) – the plan for a European central bank and a common currency, which was clinched in the Maastricht Treaty. It was clear that the size of the Dutch gold stock was well above average in the EC. This would be disadvantageous if in a few years DNB must transfer part of its reserves to the European Central Bank (ECB).

As a rich gold country the Netherlands is at a disadvantage, because it participates for a relatively small amount in the ECB. The Netherlands threatens to get stuck in the monetary union with a huge amount of gold – that doesn’t yield – because according to ECB rules participating central banks may only purchase or sell gold and foreign exchange reserves with approval by the ECB. After ratification of the Maastricht Treaty, the freedom of DNB would be very limited. “The Netherlands has no interest in a large amount of gold”, said a source familiar with the matter.

The Netherlands receives a 4.7 percent share in the ECB based on the size of the Dutch population and the national economy. That’s less than the Dutch share of 7.3 percent in total international reserves (gold and foreign exchange) of all central banks in the EC and much less than the share of 11.7 percent in gold reserves. Even after the sale of 400 tonnes the Netherlands retains a stake in the EC gold reserves of 9.4 percent. DNB is expected to sell another 685 tonnes of gold to bring their gold share in line with that of the ECB. To reassure the gold market DNB states it will not sell any more gold, though financial experts expect that the gold reserves by EC central banks, including DNB, will be further adapted within the framework of the monetary union. “Last year the Belgian and Dutch central banks sold gold. That made gold sales by central banks respectable. Additional sales threaten the market”, said a London bullion dealer.

In the beginning of 1992, still in the fuddle of Maastricht and nine years after the traumatic devaluation of the guilder in 1983, the position of the guilder was very strong and the Dutch budget deficit was considerably reduced. In The Hague no one advocated to do any more fun things with the Dutch gold stocks. The time was right to proceed to sale.

Small World

It was not possible that DNB would enter the gold market itself, because that would be known immediately in the closed world of gold trading. The few remaining Dutch players in the gold market are tiny. In London, there are four major gold traders, Sharps Pixley, Samuel Montague, Mase Westpac and Rothschild. According to John Coley, spokesman of the London Bullion Market Association, it was obvious that DNB would use the BIS as an intermediary. Duisenberg is very well known in Basel because he was President Of The Board of the BIS from 1988 to 1990.

The advantage of the BIS is, as “central bank of central banks", that it guarantees anonymity and direct access to the central banks of the member countries in Eastern and Western Europe as well as Australia, Canada, Japan and South Africa. A London trader suggested that DNB used the central bank of another member state of the BIS to bring the gold to the market. That could have been the central bank of South Africa, whose gold offers would not surprise any traders. South Africa is always very active in the London bullion market. The BIS could have acted as an intermediary between DNB and the South African central bank.

“Part of the sale was handled outside the market”, says Philip Klapwijk of Goldfield Mining Services. He says he came to this conclusion because the price of gold last year, although down slightly, it should have shown much greater fluctuations if 400 tonnes would have been sold – even if the supply would be split into small tranches.

The BIS probably made contact with the People’s Bank of China as the buyer. Why precisely the People’s Republic of China? Chinese love gold, says an expert, and he refers to the huge Taiwanese gold purchases in 1987. Second, China has large dollar surpluses as a result of the spectacular economic growth. And third, China announced that it is working to build up its reserves in order to bring it more in line with the size of the Chinese GDP.

The weekly table of DNB, which is published every Wednesday in the newspaper, we can see since February a decline in Dutch gold reserves. Presumably, the increase in the gold reserves of China will never be visible. The statistics produced by the International Monetary Fund for China record the same amount of gold for a decade, coincidentally about 400 tonnes. China experts, however, know that the People’s Bank has second secret gold reserves, which are held outside the statistics in “non-monetary gold”. If part of the gold reserves of DNB have been added to these, as many suspect, no one will ever officially know.

Popular Blog Posts by Koos Jansen

China’s Secret Gold Supplier is Singapore

China’s Secret Gold Supplier is Singapore

Audits of U.S. Monetary Gold Severely Lack Credibility

Audits of U.S. Monetary Gold Severely Lack Credibility

China Gold Import Jan-Sep 797t. Who’s Supplying?

China Gold Import Jan-Sep 797t. Who’s Supplying?

The Gold-Backed-Oil-Yuan Futures Contract Myth

The Gold-Backed-Oil-Yuan Futures Contract Myth

Estimated Chinese Gold Reserves Surpass 20,000t

Estimated Chinese Gold Reserves Surpass 20,000t

PBOC Gold Purchases: Separating Facts from Speculation

PBOC Gold Purchases: Separating Facts from Speculation

U.S. Mint Releases New Fort Knox Audit Documentation

U.S. Mint Releases New Fort Knox Audit Documentation

China Net Imported 1,300t of Gold in 2016

China Net Imported 1,300t of Gold in 2016

Why SGE Withdrawals Equal Chinese Gold Demand and Why Not

Why SGE Withdrawals Equal Chinese Gold Demand and Why Not