Gold In London & Hong Kong Is Used To Settle COMEX Futures

Koos Jansen

Koos JansenPhysical gold located in Hong Kong and London is used to settle COMEX gold futures contracts through “Exchange For Physical” trading in the over-the-counter market.

This post is a sequel to Understanding GOFO And The Gold Wholesale Market and COMEX Gold Futures Can Be Settled Directly With Eligible Inventory – in which Exchange For Physical (EFP) trading is explained and how it can increase or decrease open interest at the COMEX. If you’re new to this subject it’s advised to first read my previous posts.

Most gold analysts surmise COMEX 100-ounce gold futures contracts (GC) can only be physically settled through taking and making delivery. This is technically true when excluding the possibility of EFP trading in GC through the over-the-counter (OTC) market. While on Exchange trading in GC is “executed openly and competitively”, trading GC in the OTC realm (and thus the price of the gold, its form and location) is a “privately negotiated transaction” between buyer and seller. The COMEX is a subsidiary of CME Group, which offers its clients OTC trading on a platform called ClearPort.

Because the COMEX in New York is the most liquid gold futures exchange globally – offering precious metals futures denominated in the world most used currency the US dollar, gold industry participants use GC for a variety of reasons, including hedging metal held outside the contract’s deliverable geography. Subsequently, the contracts can be physically “settled” anywhere at any price through EFP.

In EFP two parties sign a futures contract (short and long) and simultaneously execute a reverse spot transaction (buy and sell). One side sells short the futures contract and buys spot gold (the spot leg is referred to as the related position by CME), while the other buys long the futures contract and sells the related position. EFP trading can increase the open interest, decrease the open interest, or not change it, depending on the existing positions held by both parties before they enter into an EFP transaction. When EFP decreases the open interest the phrase “settle positions” is applicable. Another way of saying it would be “offsetting positions” or “netting out positions”.

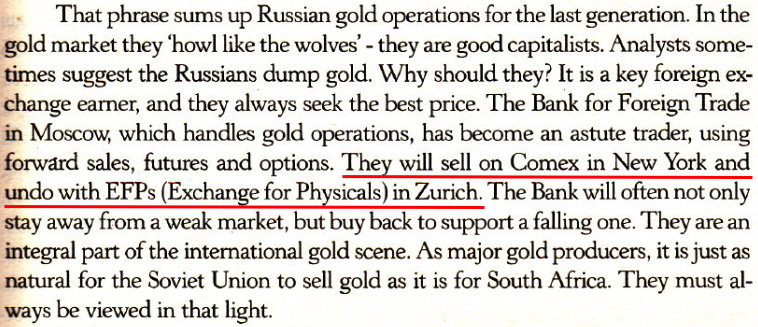

Let us have a look at a real life example. The next picture was sent to me by data wrangler and gold specialist Nick Laird (website Goldchartsrus.com). It’s taken from the book The Prospect for Gold: The View to the Year 2000 by Timothy Green. In the excerpt the author describes how the Russians sold their gold in Switzerland during the eighties.

This example matches my previous one regarding EFP (hedging metal held outside the contract’s deliverable geography). Any bullion bank, miner or refinery can sell short on COMEX and when the gold needs to be physically “settled”, for example in Switzerland, the short position can be unwound through EFP. The only requirement is that “the quantity of the related position component … must be approximately equivalent to the quantity of the Exchange component” – meaning the spot leg must be more or less 100-ounces of gold, which is the underlying asset of GC. In this example the GC short holder connects through CME ClearPort to Exchange For Physical. In the EFP transaction he will buy long a futures contract and simultaneously sell spot. His long and short will then be netted out while he sells spot the physical in Switzerland. Effectively, a COMEX short has been physically settled outside the contract’s deliverable geography. Naturally, a long position can also be unwound in Switzerland, which is then the other side of the trade.

EFP Moves Kilobars Through CME’s Hong Kong Vaults

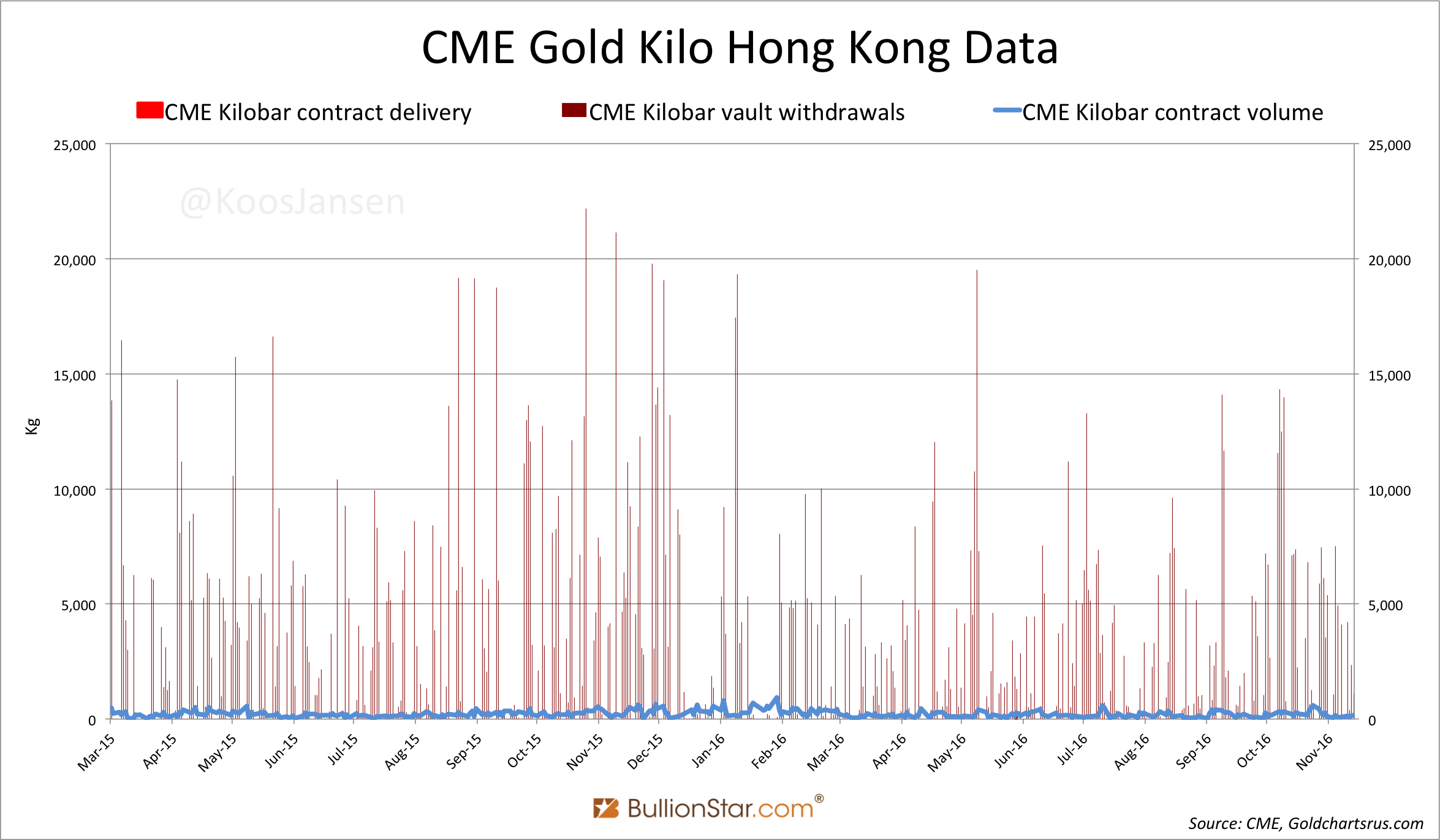

In March 2015 CME launched a Gold Kilo Futures contract (GCK) physically deliverable in Hong Kong, but ever since implementation there has been poor participation in this instrument. From the start GCK trading volume has been close to nothing and deliveries rarely occur. Notwithstanding, there are massive volumes of kilobar gold flowing through the CME approved warehouse in Hong Kong owned by Brink’s, Inc.. On average 3.9 tonnes per day are withdrawn from this vault, but sometimes daily withdrawals are as high as 20 tonnes.

Because volume and delivery for GCK on Exchange is so low, the withdraws must be explained by OTC trades. A CME representative actaully confirmed this to me; the physical movement through the Hong Kong vaults is caused by EFP transactions.

But if we look at the GCK volume page we can never observe any EFP trades being disclosed. In contrast, EFP volume of GC is substantial. Can it be gold kilobars in CME’s approved warehouses in Hong Kong are used to settle the 100-ounce futures contracts? Yes.

The underlying asset of GC is “either one (1) 100 troy ounce bar, or three (3) one (1) kilo bars, … with a weight tolerance of 5% either higher or lower, … [assaying] to a minimum of 995 fineness”, the underlying asset of GCK is “one kilogram bar (32.15 troy ounces) … [and] shall assay to a minimum .9999 fineness”. It’s thus within the indicated confinements on EFP trading that the 100-ounce gold futures contract is physically settled with three kilobars in Hong Kong.

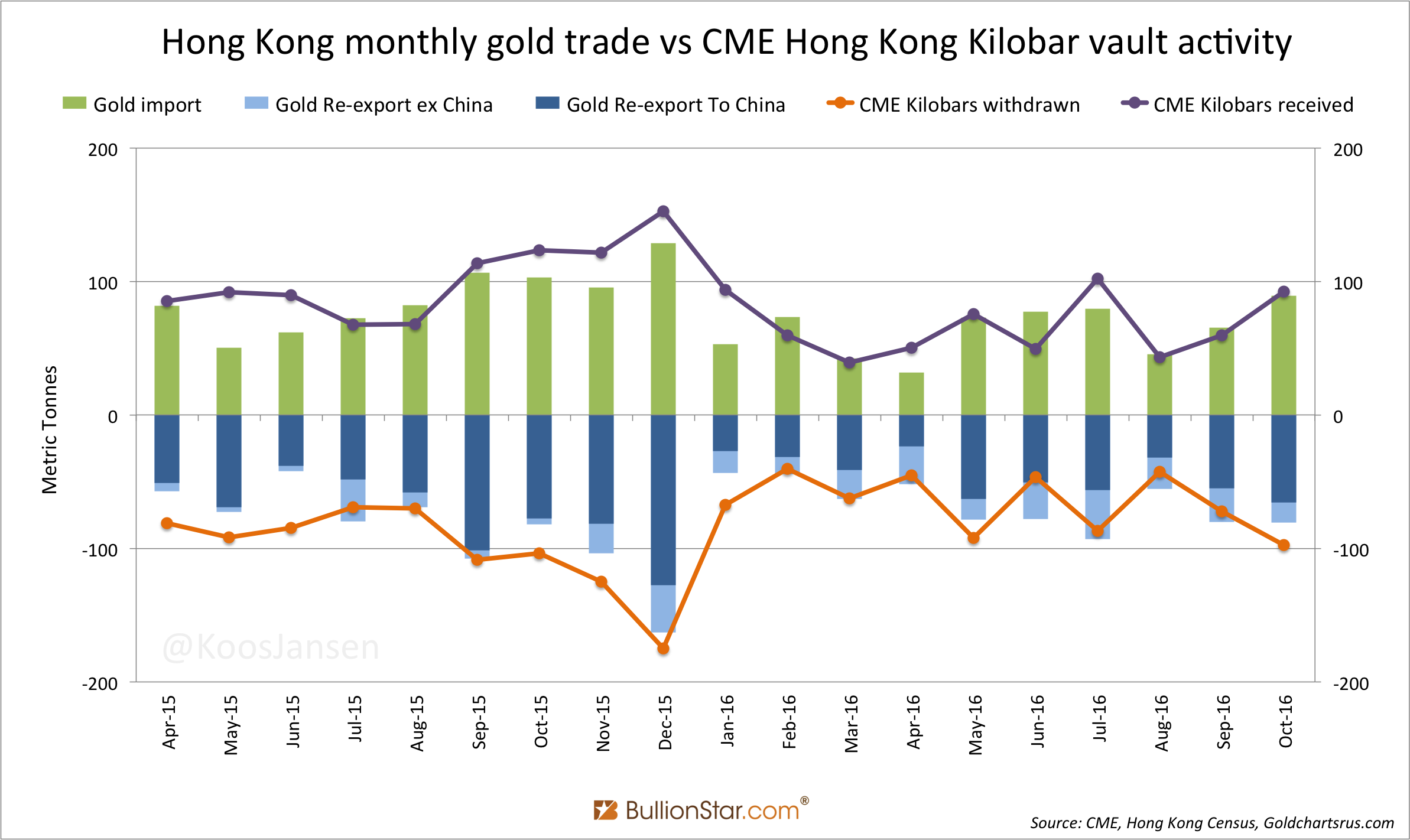

My theory is that kilobars bought by bullion banks in the West, for example at Swiss refineries, to be consigned to China are hedged on the COMEX and once the gold arrives is Hong Kong the shorts are unwound through EFP. From there the gold is transported by armored truck to Shanghai Gold Exchange designated warehouses in Shenzhen by Brink’s that has a cross-border logistics license from the Chinese government. Supportive to my theory, see exhibit 3 below. Notice the strong correlation between “gold import into Hong Kong versus kilobars received in CME’s vaults" and “re-export from Hong Kong versus kilobars withdrawn from CME’s vaults".

The correlation points out most gold moving through Hong Kong, which is headed for China, is in kilobar form and moves through CME’s vaults. And because most of this throughput is EFP related, I assume the kilobars are used to settle COMEX futures.

It’s hard to test if my theory is accurate because EFP transactions are executed in the OTC realm and little information is available. Possibly, al throughput in Hong Kong is EFP related but doesn’t impact the GS open interest. If anyone has a different theory please comment below.

London Gold Offsets COMEX Futures

We’ve established gold in Switzerland and Hong Kong is used to “settle" gold futures. But there is also proof gold in London is used to phase out positions on the COMEX. When researching this topic I reached out to William Purpura who is, inter alia, Chairman at Northport Commodities, member of the COMEX Governors Committee, and previously traded on the COMEX floor from 1982 to 2007. I asked Purpura for an example of how EFPs are used. He replied [brackets added by me]:

Most of it [EFP] is done by bullion banks. … It’s mainly for netting out. Lot’s of times London versus New York. You see lots of EFPs posted around 8am in New York on COMEX.

There it is, “London versus New York”, and, “netting out”. From this quote we learn loco London gold is used to execute EFPs to wash out New York futures positions. One can argue the related position in London is “unallocated" – I’m not sure. In the latest formulation by CME on EFP (Market Regulation Advisory Notice RA1311-5R) it’s stated:

Where the related position component … is a physical transaction … the transaction should be submitted for clearing as an EFP transaction type.

Often in wholesale gold market parlance physical is also used for “unallocated gold", which is not exactly physical in my opinion.

I’m sure there are many more methods than I’ve mentioned to use EFP, or any other privately negotiated transaction (PNT) available on ClearPort, that influences the open interest at the COMEX. One thing is for sure, conventional delivery is not the only way to terminate futures positions. In the gold futures rulebook this is explicitly noted by CME Group. The excerpt below is about terminating a gold futures contracts [brackets added by me].

113102.E. Termination of Trading

No trades in Gold futures deliverable in the current month shall be made after the third last business day of that month. Any contracts remaining open after the last trade date must be either:

(A) Settled by delivery which shall take place on any business day beginning on the first business day of the delivery month or any subsequent business day of the delivery month, but no later than the last business day of the delivery month.

(B) Liquidated by means of a bona fide Exchange for Related Position [/EFP] … .

This is important for our comprhension of the global paper and physical gold market. COMEX gold futures delivery statistics are not all there is to it.

H/t Ronan Manly, Bron Suchecki, Nick Laird from Goldchartsrus.com

Popular Blog Posts by Koos Jansen

China’s Secret Gold Supplier is Singapore

China’s Secret Gold Supplier is Singapore

Audits of U.S. Monetary Gold Severely Lack Credibility

Audits of U.S. Monetary Gold Severely Lack Credibility

China Gold Import Jan-Sep 797t. Who’s Supplying?

China Gold Import Jan-Sep 797t. Who’s Supplying?

The Gold-Backed-Oil-Yuan Futures Contract Myth

The Gold-Backed-Oil-Yuan Futures Contract Myth

Estimated Chinese Gold Reserves Surpass 20,000t

Estimated Chinese Gold Reserves Surpass 20,000t

PBOC Gold Purchases: Separating Facts from Speculation

PBOC Gold Purchases: Separating Facts from Speculation

U.S. Mint Releases New Fort Knox Audit Documentation

U.S. Mint Releases New Fort Knox Audit Documentation

China Net Imported 1,300t of Gold in 2016

China Net Imported 1,300t of Gold in 2016

Why SGE Withdrawals Equal Chinese Gold Demand and Why Not

Why SGE Withdrawals Equal Chinese Gold Demand and Why Not