COMEX Gold Futures Can Be Settled With Eligible Inventory

Koos Jansen

Koos JansenThe 100-ounce Gold futures contract listed on the COMEX in New York can be traded in OTC market through which the contract can be “settled" with anything that resembles the underlying asset, for example gold recorded as eligible inventory in COMEX approved depositories.

Make sure you’ve read GOFO And The Gold Wholesale Market before continuing.

It’s widely discussed COMEX gold futures contracts (GC) can only be physically delivered with gold recorded as registered inventory in COMEX approved depositories, which currently stands at multi year lows. In the same spirit it’s discussed the ratio between the open interest and registered inventory is at an all time high. I would say this is technically true. However, essential to mention is that the COMEX facilitates a mechanism through which trading in GC does not have to be “executed openly and competitively on the Exchange”. Effectively, “settlement" of gold futures contracts can be negotiated in the Over The Counter (OTC) market, at a different price than floats on the Exchange, and executed with anything that resembles the underlying asset; example given, eligible inventory. This settlement in the OTC market then circumvents normal physical delivery. In my opinion this insight is significant for our approach to COMEX trading.

Conventionally COMEX gold futures contracts are traded “on the Exchange” through CME’s electronic trading platform Globex or through the old fashion way of Open Outcry. Roughly 95 % of total GC trading volume is executed on the Exchange. Market takers can choose to sell short (or respectively buy long) GC contracts by submitting bid (ask) quotes at the Exchange, in order to make physical delivery (take delivery) of gold at a fixed date in the future, or for hedging or speculative purposes. If one has no interest in making (taking) delivery the short (long) position must be closed or rolled before delivery date is reached. When traders open new positions (short or long) the open interest is increased, when traders take opposite positions to existing positions they hold, or when physical delivery is made, positions are closed and the open interest is decreased.

The mechanism through which GC contracts can be traded in the OTC market is called Exchange For Physical (EFP). EFP can be seen as a forward swap whereby a futures contract is opened combined with the reverse spot trade. I will try to describe this phenomenon supported by quotes taken from official documents by CME Group (of which the COMEX is a subsidiary). The sources that I used for this post are The CME Group Risk Management Handbook, CME’s Market Regulation Advisory Notice RA1311-5R, The CME website, CME’s helpdesk (phone and email), the LBMA OTC Guide and The Gold Market by Grabbe.

To understand EFP trading in the OTC market and how it can increase or decrease the open interest we must start by establishing some nomenclature. All off-exchange (OTC) negotiated trading in CME’s contracts is what is referred to as Ex-Pit trading or Privately Negotiated Transactions (PNT). Ex-pit trades and PNTs can be subdivided in more specific types of which we will only discuss Exchange Of Futures For Related positions (EFRP) and EFP, as the rest is irrelevant for now. From The CME Group Risk Management Handbook we can read:

EX-PIT TRADING

… there are some circumstances in which a privately negotiated or ‘‘ex-pit’’ trade may be warranted. The term ex-pit trade refers to any transaction that is executed on a noncompetitive basis and outside of a traditional open outcry or electronic trading environment. The several varieties of ex-pit transactions serve slightly different purposes and may be subject to somewhat different rules. These transactions are known by a variety of names including exchange for physicals (EFPs), exchange for risk (EFRs), block trades, and cleared-only, or ClearPort, contracts. Whatever the nomenclature, they may collectively be referred to as ‘‘ex-pit’’ transactions.

…Although traditionalists in the futures industry are accustomed to referring to EFPs, … Over the years, these practices have been adopted in the context of futures markets and generalized as exchange of futures for related positions (EFRPs).

Let’s say EFP is a form of an EFRP (which both are types of ex-pit/PNTs).

On the homepage of GC at the CME website we can see it’s disclosed this contract can be traded off-exchange (OTC) through CME ClearPort.

What is ClearPort? Again, we’ll read a little in The CME Group Risk Management Handbook to understand:

CME ClearPort should not be thought of as a trading platform or as a clearing service. Rather it is best understood as an Internet or web-based gateway. The CME ClearPort system currently provides traders a wide degree of latitude to conduct transactions in literally hundreds of energy, metals, and other contracts. These transactions are executed off exchange in a bilateral transaction directly between buyer and seller. This is much like the execution of any other OTC derivatives contract.

… By submitting OTC transactions to the CME ClearPort process, one enjoys the financial sureties afforded by the Clearing House.

So ClearPort is a gateway through which market participants can use EFP to trade GC contracts OTC style.

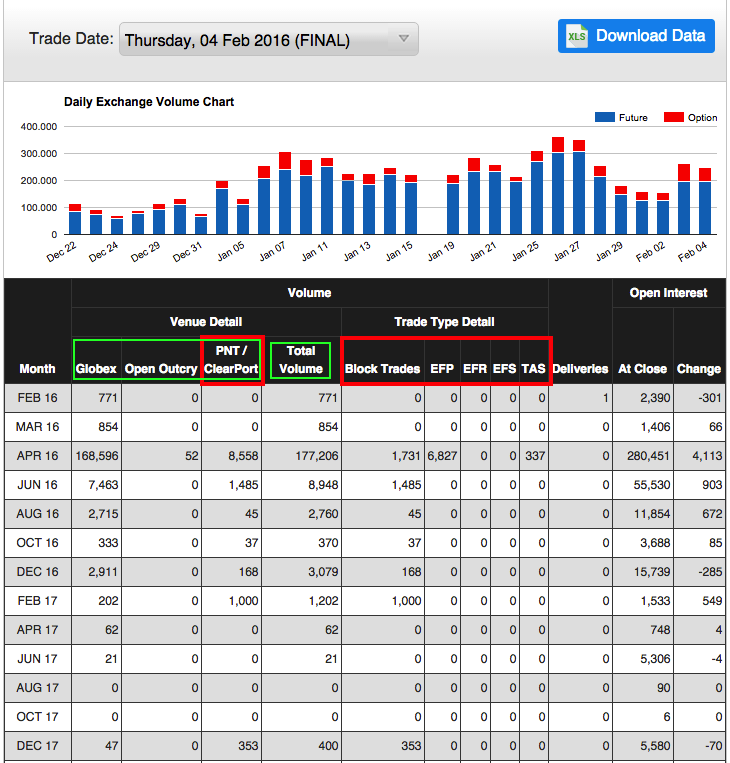

For an overview of what was just discussed, let’s head over to CME’s website and look at the volume page of GC. We can see PNT/ClearPort volume (framed in red in the screen shot below) is the sum of block trades, EFP, EFR, EFS and TAS, and Total Volume (framed in green in the screen shot below) is the sum of Globex, Open Outcry and PNT/ ClearPort volume. Have a look at the headers and the numbers below.

Again, Total Volume of GC consist of Globex, Open Outcry and PNT/ ClearPort trading.

The next step is to understand what EFP is. According to the most recent formulation by CME Group (Market Regulation Advisory Notice RA1311-5R, 2014):

An Exchange for Related Position (“EFRP”) transaction involves a privately negotiated off-exchange execution of an Exchange futures … contract and, on the opposite side of the market, the simultaneous execution of an equivalent quantity of the … related product … corresponding to the asset underlying the Exchange contract.

One party to the EFRP must be the buyer of the Exchange contract and the seller of (or the holder of the short market exposure associated with) the related position; the other party to the EFRP must be the seller of the Exchange contract and the buyer of (or the holder of the long market exposure associated with) the related position. …

(I will quote from the above paragraph later on.)

The related position component of an EFRP must be the cash commodity underlying the Exchange contract or a by-product, a related product or an OTC derivative instrument of such commodity that has a reasonable degree of price correlation to the commodity underlying the Exchange contract. The related position component of an EFRP may not be a futures contract or an option on a futures contract.

Where the related position component of an EFRP is a physical transaction … the transaction should be submitted for clearing as an EFP transaction type.

For the sake of simplicity we won’t discuss all varieties of EFP described by CME Group in the Market Regulation Advisory Notice RA1311-5R, but only what I believe is the common denominator: a forward swap. In a previous post I described what a forward swap is, how it’s executed in the London Bullion Market and that it’s usually referred to in short as a swap. When a (forward) swap is executed in the futures realm this is done through EFP, as James Orlin Grabbe wrote in the late nineties:

While forward gold is traded in the form of swaps, which combines a spot trade (buy or sell) with the reverse forward trade (sell or buy), gold futures can be traded in the form of EFPs (exchange for physicals), which combine a futures trade with the reverse spot trade.

The CME Group Risk Management Handbook (2010) also describes EFP to be a swap:

Technically, an EFP refers to a transaction in which a futures position is assumed in juxtaposition to an offsetting … spot transaction.

So, we’ll focus on the swap characteristics of EFP.

In EFP two parties sign a futures contract (short and long) and simultaneously make a spot transaction (buy and sell). One party sells short the futures contract and buys spot gold (the spot leg is referred to as the related position by CME), while the other party buys long the futures contract and sells the spot related position. EFP trading can increase the open interest, decrease the open interest or not change it, depending on the existing GC positions held by both parties before they enter into an EFP transaction.

Example given how EFP can increase the GC open interest: Suppose two traders, Mister A and Mister B, have no existing GC positions. Mister A and B connect through CME ClearPort and privately negotiate to enter into an EFP transaction. Through EFP Mister A buys long 1 GC (the buyer of the Exchange contract) and simultaneously sells spot gold (the seller of … the related position). Mister B sells short the corresponding GC (the seller of the Exchange contract) and simultaneously buys the corresponding spot gold (the buyer of … the related position). In this example the open interest is increased by 1, counted unilaterally, as both Mister A and B open a new GC position (1 short, 1 long). The movement in the related position (the spot leg) is irrelevant to the open interest.

Example given how EFP can decrease the GC open interest: Suppose, Mister A is short 1 GC to be delivered in December 2016 and Mister B is long 1 GC to be delivered in December 2016. Mister A and B connect through CME ClearPort and privately negotiate to enter into an EFP transaction. Through EFP Mister A buys long 1 GC December 2016 (the buyer of the Exchange contract) and simultaneously sells spot gold (the seller of … the related position). Mister B sells short 1 GC December 2016 (the seller of the Exchange contract) and simultaneously buys the spot gold (the buyer of … the related position). In this example the open interest is decreased by 1, as the existing positions by Mister A and B before entering into the EFP transaction have been offset by both taking an opposite futures position through EFP and simultaneously exchanging spot gold. What happened is that Mister A and B settled their existing GC December 2016 position (short and long) through EFP. This settlement can only be performed if both parties agree in EFP. No short or long GC position can be forced to settle through EFP.

Naturally, EFP can leave the GC open interest unchanged if either Mister A or B has an existing position and the other one not before both enter into an EFP transaction.

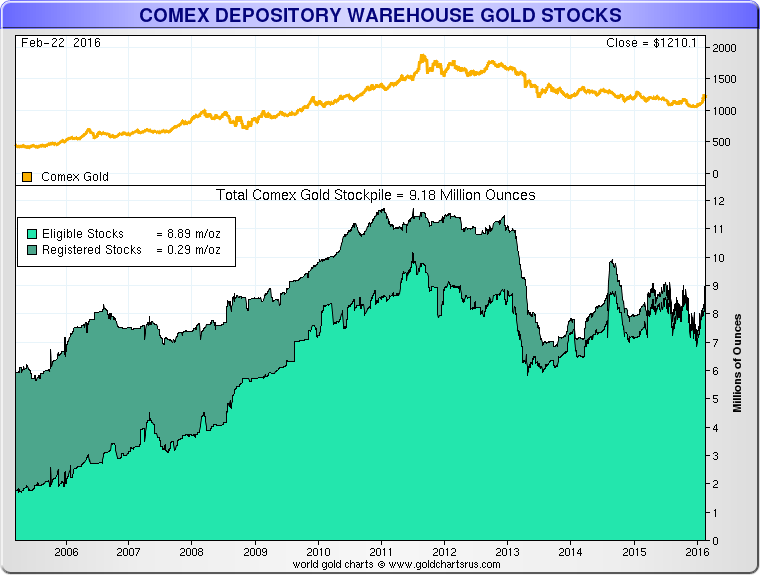

Let us move further to the essence of this post. The COMEX publishes the amount of gold stock in its approved depositories in two categories: eligible and registered inventory. Factually, gold stock recorded as eligible or registered is required to respect exactly the same specifications and are both stored in vaults “within a 150-mile radius of the City of New York“. The only difference between the two is that registered gold has a warrant attached to it. From the COMEX rulebook we can read:

Eligible metal shall mean all such metal that is acceptable for delivery against the applicable metal futures contract for which a warrant has not been issued. Registered metal shall mean an eligible metal for which a warrant has been issued.

…A warrant shall mean a document of title … demonstrating that the referenced quantity of the covered metal, stored in the facility referenced thereon, meets the specifications of the applicable metal futures contract.

Through the conventional process – without OTC trading – GC is physically delivered with “either one (1) 100 troy ounce bar, or three (3) one (1) kilo bars, … with a weight tolerance of 5% either higher or lower, … [assaying] to a minimum of 995 fineness”, which is located in a COMEX approved depository in New York and has a warrant attached to the gold. On the warrant the serial numbers of the bar(s) are written, and it is this warrant that changes hands when the gold is delivered from a short to a long. Because physical delivery is done with warrants, often only registered inventory is presented by analysts when comparing COMEX gold stock to the open interest or other economic parameters.

But, as we just learned GC can also be settled through EFP. The punch line of EFP is that the related position (the spot leg) can be anything that resembles 100 ounces of gold. Through EFP “the quantity of the related position component … must be approximately equivalent to the quantity of the Exchange component”. Therefor, the related position is allowed to be gold recorded as eligible inventory in New York, but it can also be Good Delivery bars or a bag of gold coins located anywhere on this planet. Yes, CME confirmed to me in black and white the related position in EFP has no geographical limitations. The physical gold used in EFP for settlement of GC does not have to be located in New York.

Does CME generally inspect what these related positions are? Well, CME can ask EFP parties to show their offsetting (/related positions) accounts. From The CME Group Risk Management Handbook we can read [brackets added by me]:

The … spot … position that is traded opposite to the futures contract must be a product that represents a legitimate economic offset.

After the two counterparties consummate the [EFP] transaction, the futures position is reported to the CH [CME Clearing House] through a clearing member via electronic systems. The cash position [/related position] continues to be held in appropriate accounts established by the EFP counterparties and is not reported to the exchange upon execution. If called on during the course of a periodic audit, however, clearing members may be required to produce statements that show the offsetting position was transacted and meets exchange standards as a valid offsetting position.

What about the price at which EFP is executed? Again, these trades are OTC so the price is privately negotiated between the EFP participants – and are not likely to be in line with prevailing prices on CME’s Globex. A CME representative told me over the phone that EFPs are usually quoted by brokers in dollars that reflect the difference in price between the spot (related position) and the futures leg. From the Market Regulation Advisory Notice RA1311-5R we can read:

EFRPs may be transacted at such commercially reasonable prices as are mutually agreed upon by the parties to the transaction.

… The price of the Exchange leg of an EFRP transaction is not publicly reported. EFRP volumes are reported daily, by instrument, on the CME Group website.

From The CME Group Risk Management Handbook we can read:

An EFP may be transacted at any time and at any price agreed on by the two counterparties. Two customers may transact an EFRP among themselves provided that the resulting futures position is subsequently submitted to the CME Clearing House (CH) through the facilities of a clearing member.

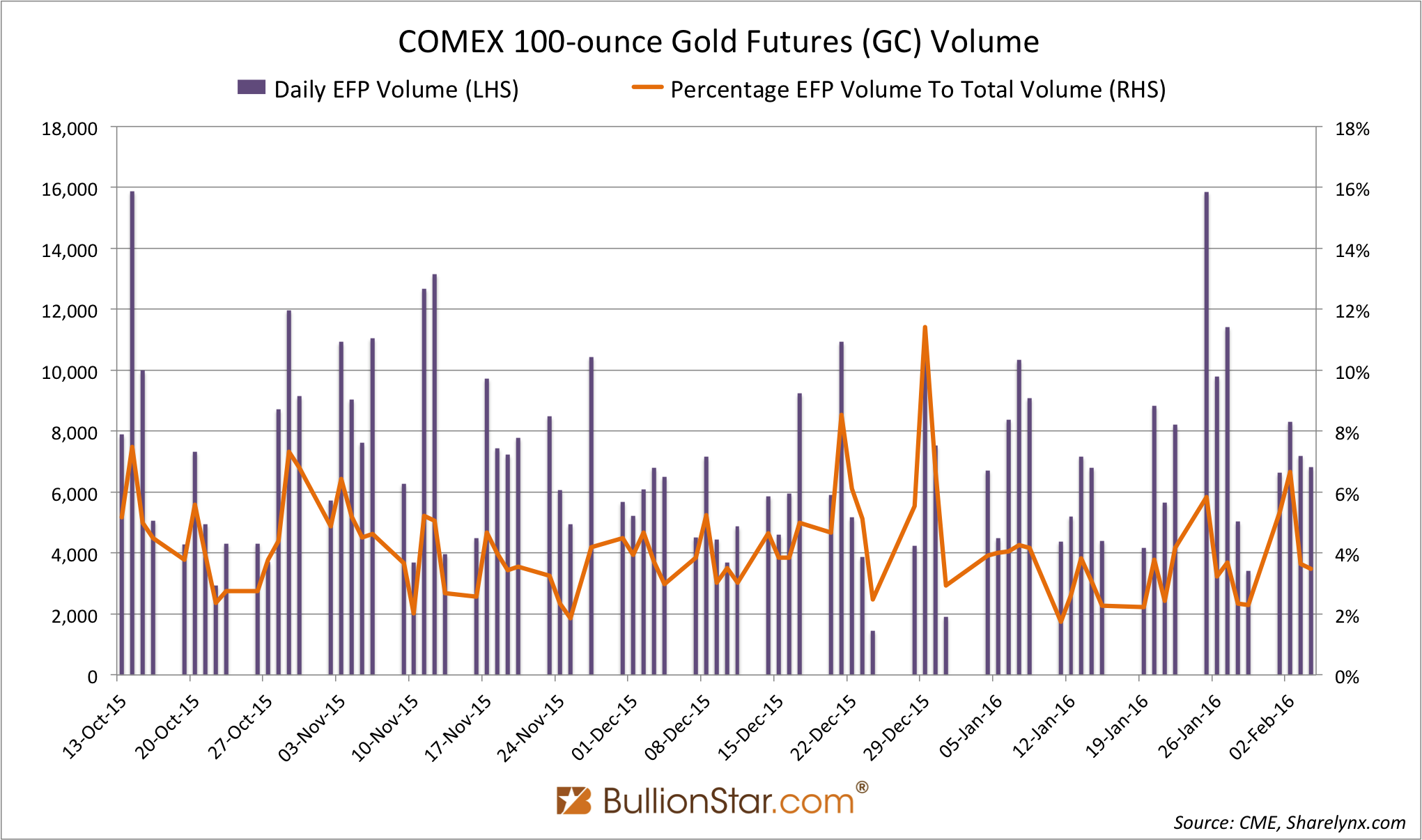

Last but not least; below is a chart showing EFP volume, clearly this concept is not something unusual. On average 4 % of total daily trading volume in GC is performed through EFP. If EFP volume is 8,000 a day the lower bound is that the open interest is decreased by 8,000 contracts, the upper bound is that the open interest is increased by 8,000 contracts.

This concludes the introduction of EFP. More will be discussed in forthcoming posts.

Addendum

Btw, this is helpful as wel. From CME:

113102.E. Termination of Trading

No trades in Gold futures deliverable in the current month shall be made after the third last business day of that month. Any contracts remaining open after the last trade date must be either:

(A) Settled by delivery which shall take place on any business day beginning on the first business day of the delivery month or any subsequent business day of the delivery month, but no later than the last business day of the delivery month.

(B) Liquidated by means of a bona fide Exchange for Related Position (“EFRP”) pursuant to Rule 538. An EFRP is permitted in an expired futures contract until 12:00 p.m. on the business day following termination of trading in the expired futures contract.

Popular Blog Posts by Koos Jansen

China’s Secret Gold Supplier is Singapore

China’s Secret Gold Supplier is Singapore

Audits of U.S. Monetary Gold Severely Lack Credibility

Audits of U.S. Monetary Gold Severely Lack Credibility

China Gold Import Jan-Sep 797t. Who’s Supplying?

China Gold Import Jan-Sep 797t. Who’s Supplying?

The Gold-Backed-Oil-Yuan Futures Contract Myth

The Gold-Backed-Oil-Yuan Futures Contract Myth

Estimated Chinese Gold Reserves Surpass 20,000t

Estimated Chinese Gold Reserves Surpass 20,000t

PBOC Gold Purchases: Separating Facts from Speculation

PBOC Gold Purchases: Separating Facts from Speculation

U.S. Mint Releases New Fort Knox Audit Documentation

U.S. Mint Releases New Fort Knox Audit Documentation

China Net Imported 1,300t of Gold in 2016

China Net Imported 1,300t of Gold in 2016

Why SGE Withdrawals Equal Chinese Gold Demand and Why Not

Why SGE Withdrawals Equal Chinese Gold Demand and Why Not