A First Look at the Chinese Gold & Silver Exchange

Koos Jansen

Koos Jansen

“Hong Kong was a traditional trading hub for gold in the past decades" Director General of the The People’s Bank of China Mr. Xie Duo, 2012.

A little known Asian precious metals hub is the Chinese Gold & Silver Exchange (CGSE) located at 12-18 Mercer street, Sheung Wan, Hong Kong. It opened it’s doors in 1910 and until today it only trades spot contracts. No futures or forwards can however include leveraged trading. When asking the CGSE on the details of their business this is what their Assistant Director, Corporate Communications Cherry Lai emailed me:

The CGSE is a gold exchange with the capability of settling the gold contract with physical delivery. Nevertheless, a contract must be done through the CGSE platform between members, according to the constitution of the CGSE. In the recent few years, the CGSE has developed more new gold and silver products, which can be settled with currencies other than HK dollars, e.g USD. Respective member of the CGSE can carry our business activities with their clients on a leverage arrangement according to market practice and credit of respective clients.

How much gold is traded on the international orientated CGSE is not published, we do have a few indications.

They have 11 accredited refineries of which Heraeus Limited recently got some attention in the gold community. William Kaye, manager of Hong Kong based hedge fund the Pacific Alliance Group, holds close ties with Heraeus. During an informal conversation they supposedly told him they melt gold bars from western central banks for the Asian Market. If true the CGSE could be a part of the supply chain.

|

| Opening ceremony for the year of the snake |

|

| The visit of Malaysian government officials |

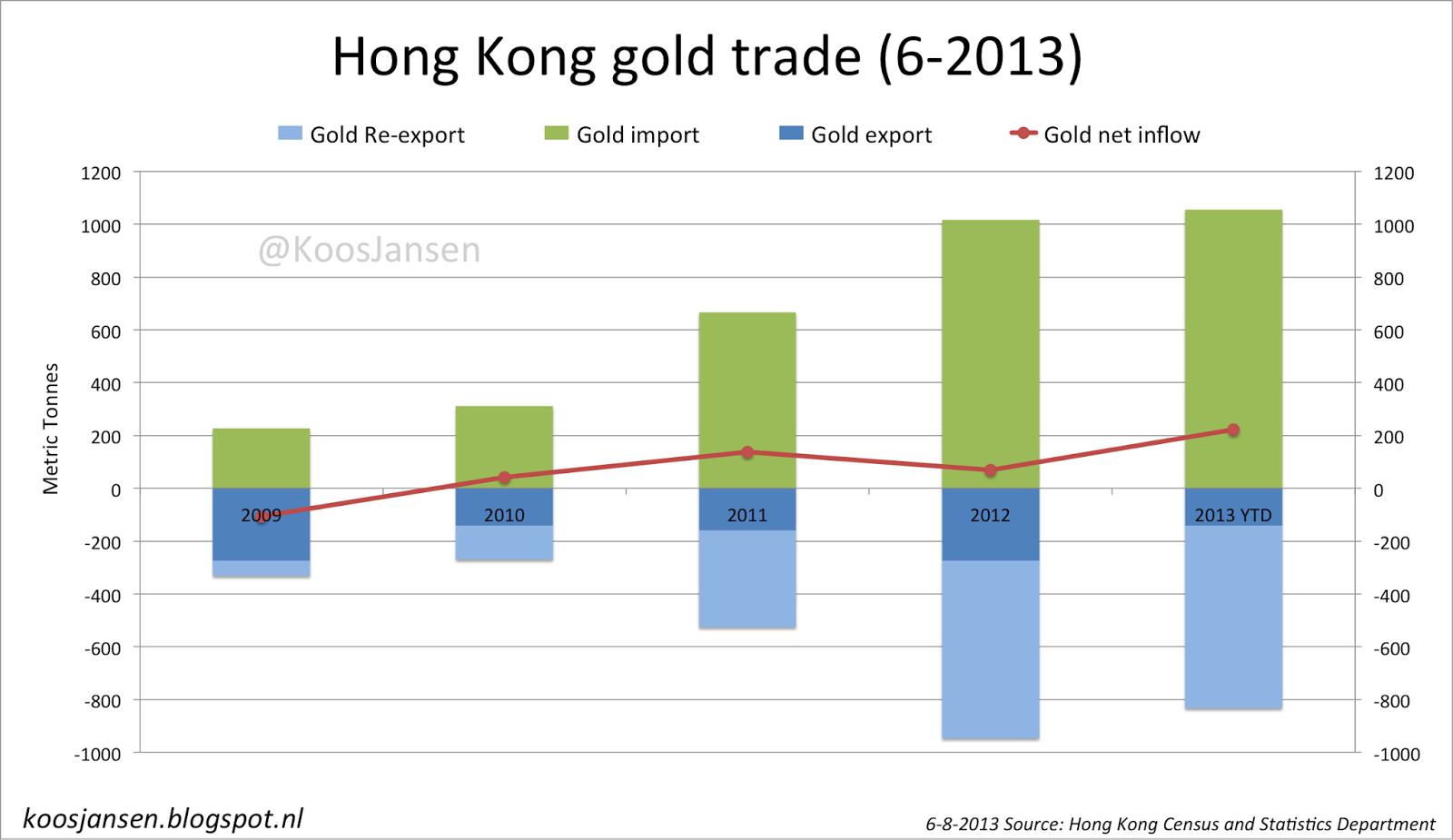

What we also know is that large amounts of precious metals are traded through Hong Kong. Year to date (2013 inc. June) total gold imports amounted for 1056t and total export (export + re-export) 834t, which left 222t inside the Special Administrative Region of the People’s Republic of China.

From the trade data I assume that CGSE gold delivery went up this year, but also from the fact that they were completely sold out in May. Something the president of the CGSE, Haywood Cheung, had never experienced. In this video shot in that period he states:

It’s a gold rush. I Have been in the gold industry for over 30 years, this is the first time I have seen anything like this. Before we also had major corrections (he refers to the price drop in April), but then investors would wait, they would wait for a lower price. This time everybody starts rushing out, trying not to miss the opportunity.

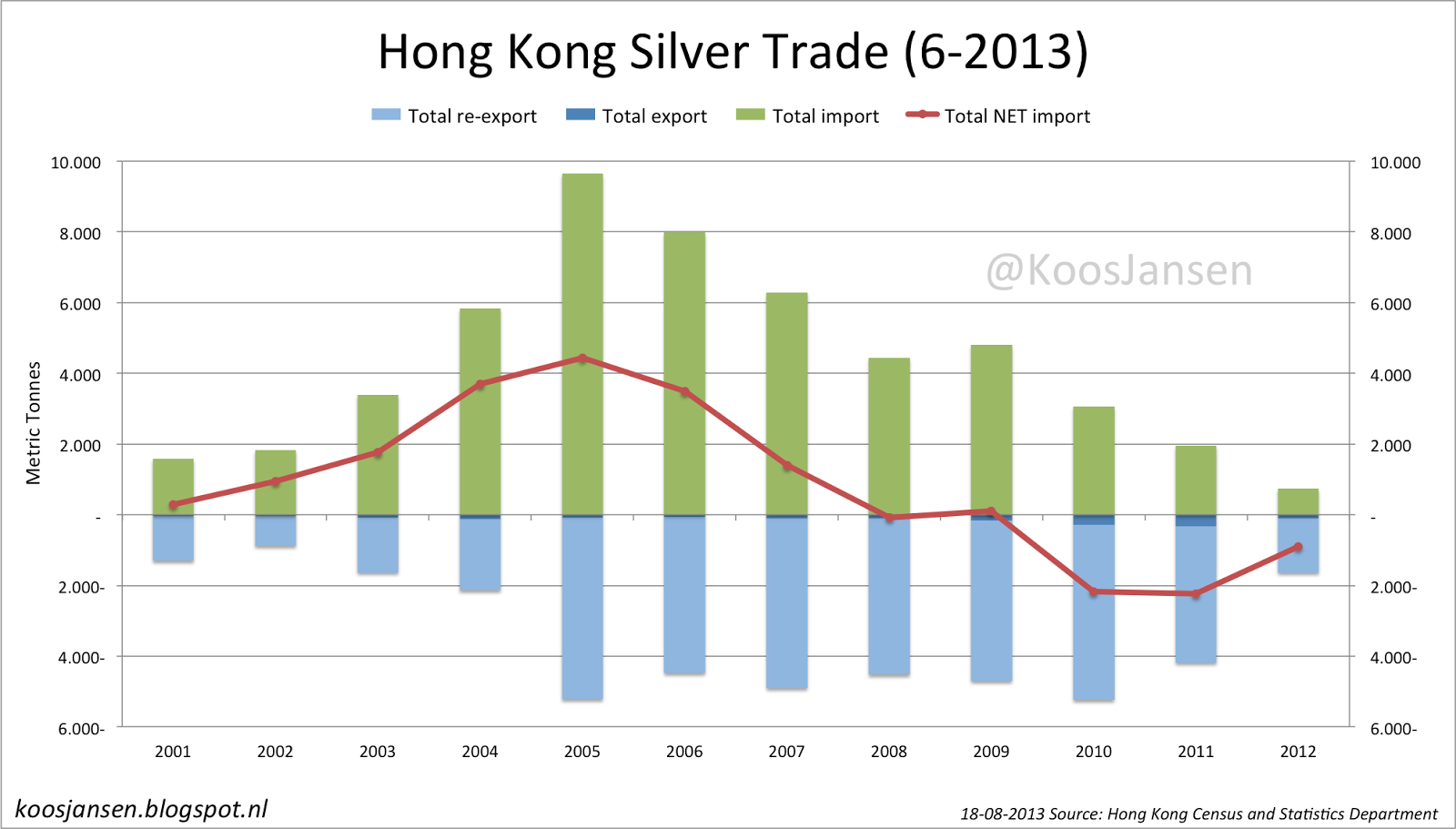

For the silver chart (that I haven’t published before) I combined HKHS (Hong Kong Harmonized System) codes:

28911 SILVER ORES AND CONCENTRATES (KG)

68113 SILVER, UNWROUGHT (KG)

68114 SILVER, SEMI-MANUFACTURED OR IN POWDER FORM (KG)

We can see Hong Kong has been hoarding silver before ’09, after that they became net exporters. Imports mainly come from Japan and the mainland, exports the last three years mainly went to India, Taiwan, South Korea and the mainland. These figures highlight the significant position of Hong Kong in Asia’s silver market. Also notice silver exports are predominantly re-exports – that go out the way they came in, without processing. In an email the Honk Kong Census and Statistics Department (HKCSD) wrote me:

Kindly note that in Hong Kong External Merchandise Trade, re-exports of goods refer to products which have previously been imported into Hong Kong and which are re-exported without having undergone in Hong Kong a manufacturing process which has changed permanently the shape, nature, form or utility of the product.

The CGSE has the ambition to become the leading silver hub in all of Asia and expand their trade with the rest of the world. November 11-13, 2013 the CGSE hosted the LBMA/LPPM precious metals conference in Hong Kong. Have a look at the long delegate list (which made me wonder why I wasn’t invited), present were people from bullion banks, mining companies, refineries, exchange’s and investment funds.

Here are a few of the one’s who stepped behind the microphone to share their view on the PM market:

– Stewart Murray, LBMA Chief Executive

– Haywood Cheung, President, Chinese Gold & Silver Exchange

– Wang Zhe, Chairman, Shanghai Gold Exchange

– Chu Juehai, Executive Vice President, Shanghai Futures Exchange

– Xie Duo, General Director, People’s Bank of China

– Yu Yongding, Institute of World Economics and Politics, former member of the PBOC

– Marc Faber, Editor and Publisher of “The Gloom, Boom & Doom Report"

– Charles Morris, Head of Global Asset Management, HSBC

– Bob Greer, Executive Vice President and Manager of Real Return Products, PIMCO

– Albert Cheng, Managing Director, Far East World Gold Council

– Zheng Zhiguang, General Manager, Precious Metals Dept, ICBC

– Kent Wong, Managing Director, Chow Tai Fook Jewellery Group

– Jochen Schlessmann, Head of Recycling Division Hong Kong, Heraeus

– Suki Cooper, Chairman, Precious Metals Analyst, Barclays

– Jamie Sokalsky, CEO, Barrick Gold Corporation

– Steven Lowe, Managing Director, Bank of Nova Scotia – ScotiaMocatta

– David MS Wang, Executive Director, Greater China Metals Marketing, JP Morgan

– Tom Kendall, Director, Precious Metals Research, Credit Suisse

Below a few slides, quotes and pictures from the conference to give you an impression of how an LBMA conference is like:

Wang Zhe, SGE

Chairman Gornall, Chairman Smith, Mr Murray, Ladies and Gentlemen, good morning. I am honoured to be able to attend this annual meeting as a representative of the Shanghai Gold Exchange and to have entertained you during the welcome party last evening together with the Shanghai Futures Exchange. We are glad that we have the opportunity to receive you as a host of the gold industry in Hong Kong. The size of this year’s annual meeting and the number of participants are beyond our expectation; on the other hand, they also reflect the success and prosperity of this industry. Your cheerfulness and vigour remind me of the words of Shakespeare:“The golden age is before us, not behind us.” It is true that, as the global economy remains weak, the gold market is facing rare historic opportunities; however, ahead of all the opportunities and challenges, the issue of how to consolidate the existing achievements and gain a more extensive space for development has become an important topic for all the giants in the world gold industry.

Xie Duo, PBOC

|

Yu Yongding, Institute of World Economics and Politics

Charles Morris, HSBC

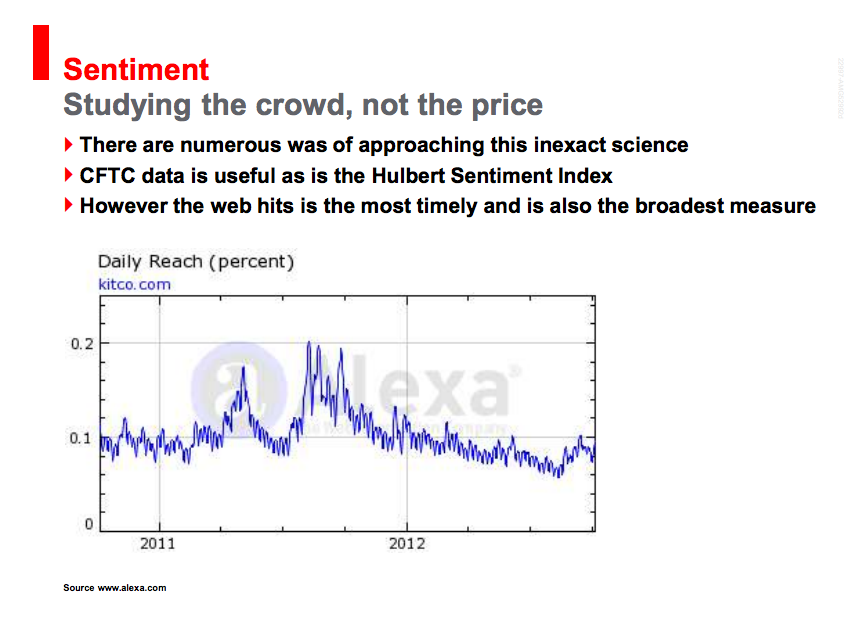

(k) Sentiment

The third one is crowd sentiment. There are many ways of measuring sentiment. We all know the COT data, looking at the futures market and the hedge funds are taking all the gold from one corner of the vault, selling it to the other guy and putting it in the other corner of the vault; they create the volatility in the market. Of course, the COT data always coincides with the medium term highs and lows, so it is useful, but it totally ignores the secular trend, which is driven by the real money. The real money of course comes from wealth preservers, whether they are central banks or wealthy individuals.

There are other indicators as well. The Hulbert Sentiment looks at all the newsletters in America and is very effective, but my favourite of all is internet hits. This is a graph from the kitco.com website measured by Alexa, showing the number of hits on their website. The general public is getting very excited about the gold market when there are highs and they could not care when it is low. Every single one of these highs exactly coincides with a high in the gold price, so I think sentiment is a very important factor to include in the tactical allocation.

|

| Matching slide Charles Morris |

Zheng Zhiguang, ICBC

Kent Wong, Chow Tai Fook Jewellery Group

Thank you, Philip. As many of you may already know, China is the fastest growing market for gold jewellery. But do you know the answers to these two questions: Firstly, what is behind this rise in demand? Secondly, what are customers buying? Well, as the jeweller with the largest market share in China, we actually have some very interesting insight to share. We can see that 2 consumers are gradually changing their buying behaviour, and the jewellery industry is changing with them. I think most of you know that Chinese people like to buy pure gold jewellery. Mainland China’s GDP increased 7.7% year-onyear in the last three quarters with retail sales of consumer products increasing by over 14%. Chinese people have more spending power and they are buying more jewellery, including pure gold jewellery. In fact, there’s a very long tradition, dating back to the Xia dynasty, which was the first dynasty in China about 4,000 years ago, that gold jewellery gifts should be part of a bride’s dowry. There is also an age-old tradition of giving jewellery gifts at weddings, births, Chinese holidays, birthdays and anniversaries. [PAUSE] We have some Westerners in today’s audience, but you do not buy the same kind of gold we Chinese buy, right? You like to buy 14 karat or 18 karat gold jewellery, because it is harder and more durable. In China and India, people traditionally prefer pure, 24 karat gold jewellery or “足金” (Zu Jin) in Chinese, mostly because the high purity of gold is more valuable and a better investment. We could generalise by saying that Westerners buy gold jewellery for decoration, but Asians buy it for both decoration and as an investment.

Jamie Sokalsky, Barrick Gold Corporation

Great publicity for the CGSE, I bet Haywood and friends made even more friends. Busy times, in that same month they also held the first Annual CGSE International (Silver) Conference.

On the Chinese Gold and Silver Exchange they have open outcry trading and electronic.

These are the open outcry products:

– 99 Tael Gold Contract, 100 Tael (3.743 Kg) in HK$. Fineness 99.

– HKD Kilo Gold Contract, 5 Kg in HK$. Fineness 999.9.

Electronic products:

– 500 Ounce Loco London Silver Contract, 5000 ounce in US$. Fineness 9999 or up.

– Loco Hong Kong Silver Contract, 15 KG in HK$, Fineness 9999 or up.

– Renminbi Gold Kilobar Contract, 1 Kg in RMB. Fineness 9999 or up.

– 999.9 Tael Gold Contract, 100 Tael (3.743 Kg) in HK$. Fineness 9999 or up.

Their newest contract is the “Loco Hong Kong Silver". This is what president Cheung had to say on it in the press release May 2, 2013:

Our Exchange (CGSE) will set up gold and silver vaults at the Hong Kong International Airport and VIAMAT, a professional warehousing and logistics company. CGSE gained widespread support and recognition from international and local silver merchants after hosting a large scale international silver conference in Hong Kong in November last year. In addition to a trading platform for spot silver, CGSE also has well-established mechanisms for Loco Hong Kong Silver in respect of trade settlement, physical delivery and settlement for international liquidity, which are comparable to the operation model of Loco London Gold. CGSE’s Loco Hong Kong Silver’s is the only spot silver trading platform in the entire Asian region which combines these four key functions. I believe that Loco Hong Kong Silver will establish its right of silver fixing in Asian trading session in the foreseeable future.

There most remarkable contract is the “Renminbi Gold Kilobar", launched October 17, 2011 intended to internationalize the mainland’s currency, the Renminbi. From Cheung:

I believe Renminbi Gold Kilobar, which is the world’s first offshore renminbi-denominated gold contract, can truly help promote the internationalization of the renminbi, and attract overseas and local gold dealers to engage in arbitrage activities to capitalize on price spreads. In addition, this product offers investors a new-found opportunity to participate in leveraged trading of renminbi. The first batch of Renminbi Kilobar Gold dealing participants (AA grade) are 27 CGSE Members. Institutional investors and retail investors may engage in trading of Renminbi Kilobar Gold by opening an account with CGSE’s AA grade Members. To effectively mitigate the price risks, they can choose the method of final settlement for their trades either through Renminbi-denominated gold contract or spot gold delivery.

If China wants to preserve a lead role on the world stage of economics, they have to free their currency. At this moment capital control restricts the flow of Renminbi in and out of China. Little by little the PBOC breaks down the wall by allowing some trade in RMB and making swap deals with other central banks (currently 30). They also know that in order to have a stable and sustainable currency they should hold adequate gold reserves to support their currency, something they’re quietly working on (not very likely through the CGSE). Their latest heads up was in 2009 and stated they own 1054t, which they at least should have doubled by now. Another confession is expected before 2015. In the meantime other small steps are being taken to mature the RMB through gold, like the launch of the “Renminbi Gold Kilobar Contract".

Popular Blog Posts by Koos Jansen

China’s Secret Gold Supplier is Singapore

China’s Secret Gold Supplier is Singapore

Audits of U.S. Monetary Gold Severely Lack Credibility

Audits of U.S. Monetary Gold Severely Lack Credibility

China Gold Import Jan-Sep 797t. Who’s Supplying?

China Gold Import Jan-Sep 797t. Who’s Supplying?

The Gold-Backed-Oil-Yuan Futures Contract Myth

The Gold-Backed-Oil-Yuan Futures Contract Myth

Estimated Chinese Gold Reserves Surpass 20,000t

Estimated Chinese Gold Reserves Surpass 20,000t

PBOC Gold Purchases: Separating Facts from Speculation

PBOC Gold Purchases: Separating Facts from Speculation

U.S. Mint Releases New Fort Knox Audit Documentation

U.S. Mint Releases New Fort Knox Audit Documentation

China Net Imported 1,300t of Gold in 2016

China Net Imported 1,300t of Gold in 2016

Why SGE Withdrawals Equal Chinese Gold Demand and Why Not

Why SGE Withdrawals Equal Chinese Gold Demand and Why Not