Types of Gold Standards

JP Koning

JP Koning 4 Comments

4 CommentsThis blog post is a guest post on BullionStar’s Blog by the renowned blogger JP Koning who will be writing about monetary economics, central banking and gold. BullionStar does not endorse or oppose the opinions presented but encourage a healthy debate.

People often throw out the phrase “gold standard" into conversation, but it’s worth keeping in mind that there have been several iterations of the gold standard over the course of history. This article describes each type of gold standard using historical examples for clarity.

1. The Gold Coin Standard, or Specie Standard

-Bimetallic Coin Systems-

Medieval coinage systems were typically bimetallic, relying on both gold and silver. To ensure the realm was well-supplied with coins, the monarch maintained a network of mints. Mints in the medieval times operated very differently than they do now. According to the principles of free coinage, access to these mints was available to anyone. By bringing their stash of raw precious metals to the mint, members of the public could ask the mint master to turn it into a specified number of coins, albeit for a fee.

To ensure that a variety of large and small transactions could be made by the public, the mint typically produced a range of small and large coin denominations. In England’s case, by the 1500s it was issuing pennies, farthings (1/4 pennies), groats (4 pennies), testoons (12 pennies), half crowns (30 pennies), gold nobles (100 pennies), and more.

Minting low denomination coins like farthings and pennies out of gold was generally not a feasible option because the resulting coin would be tiny and easily lost. Twinning gold with a large amount of base metals like copper might have resulted in a larger and more manageable low-denomination gold coin, but then it would be susceptible to counterfeiting. As for high denomination silver coins, they would be large and bulky. Thus bimetallism amounted to a sensible sharing of the monetary load by both gold and silver coins.

-Accidental Monometallic Gold Coin Systems-

Bimetallic standards sometimes careened off course and became what are known as monometallic standards, with either gold or silver dominating. Thus emerged the first true gold standards, albeit entirely by accident. The mechanism underlying this muddling into monometallism was rooted in the fixed price between the two metals as enforced by the monarchs’ mints.

To illustrate how this fixed price worked, consider that in August 1464 anyone could bring raw silver to the London Mint and have it minted into English pennies that contained 0.72 grams of silver. The mint would also turn raw gold into English nobles which contained 6.69 grams of gold. Since law stipulated that a noble was worth 100 pennies, that meant that the mint effectively valued a fixed amount of gold at 11 times the same amount of silver. (I get this data from John Munro [pdf]).

When the mint’s chosen gold-to-silver ratio diverged too far from the global market ratio of gold-to-silver, then one of the two metals would begin to be ejected from the domestic monetary system. The reason for this is that a divergence effectively meant that the monarch was undervaluing one metal and overvaluing the other, and since no one who owned gold (or silver) coins wanted their property to be less than its true worth, the undervalued metal would be taken off the market.

For instance, if the mint was undervaluing silver, then anyone who purchased £1000 worth of raw silver and brought it to the mint for conversion into coins would get less purchasing power than if they had bought £1000 worth of gold and bought it to the mint. So the flow of silver to the mints would grind to a halt. Furthermore, any high quality silver coin already in circulation would be sent overseas in order to take advantage of the true gold-to-silver ratio. At this point a gold standard had emerged.

England stumbled onto a monometallic gold standard in the 18th century after having operated on a bimetallic basis for centuries. The gold-to-silver ratio used by the mint in the later 1600s and early 1700s undervalued silver and overvalued gold, so England’s silver coins were steadily being shipped to the continent, causing silver coin shortages. Isaac Newton, the famous physicist who was appointed Master of the Mint in 1699, counseled the government to bring the ratio in line with the market. But when he finally moved to fix the problem in 1717, he undershot the amount of adjustment necessary, so that silver remained undervalued and the export of silver coins continued. Thus England was pushed onto a gold standard.

-The Hybrid Circulation of Coins and Paper Money-

By the 17th century, banknotes had joined coins in circulation. Paper money was originally convertible into a fixed amount of coins, issuers holding enough reserves in their vaults to ensure that ready convertibility was possible. A banknote is far easier to carry and handle than a coin, and since the public generally trusted the issuers of these notes, gold coins were pushed out of circulation and into bank vaults or non-monetary uses like jewellery. By the 1800s, it was rare to see a gold coin circulating in England.

Even as banknotes came to dominate, the British standard effectively remained a gold coin standard. Since a banknote was convertible into a fixed amount of coin, the note’s purchasing power was regulated by the value of the coin itself. If there was any divergence between the two, say notes became more valuable than underlying coins, than arbitrageurs would push them back into line by buying coins for 99p and converting them into £1, earning 1 penny in risk-free profits.

Substituting out metal with paper resulted in a cheaper payments system. Adam Smith was one of the earlier writers to comment on this, describing gold and silver coins as a highway that “carries to market all the grass and corn of the country." Bank-provided paper money was a more superior sort of thoroughfare, in Smith’s words a “waggon-way through the air." The replacement of gold by paper money allowed the nation to convert barren highways – its metallic coinage – into goods pastures and cornfields, thus increasing the annual produce of the country.

2. The Gold Bullion Standard

If gold coins weren’t used much in trade, might it be possible to cease minting them altogether yet remain on a version of the gold standard? This was the idea behind the gold bullion standard, first conceived by the famous English economist David Ricardo in early 1816 and eventually adopted in Britain some one hundred years later, in the aftermath of WWI. Under a bullion standard, an issuer of paper money promised to redeem its banknotes not with gold coins, or specie, but for a given amount of raw bullion.

At the same time, the mint ceased to allow free coinage of gold, effectively closing itself to the public. Existing gold coins were called in and demonetized. The mint now focused its resources on providing the government with low denomination token coins for use as small change. The value of token coins wasn’t regulated by the metal inside of them. After all, a token coin with the face value of £1 might contain just a few cents worth of silver, copper or nickel. Rather, a £1 token circulated at its face value of £1 because the monetary (or fiscal) authority promised to buy those tokens up at their face value.

The adoption of a gold bullion standard resulted in a reduction in the costs of running the payments system. By pushing gold coins entirely out of circulation and replacing them with a combination of token coins and paper money, gold was conserved and could be put towards better uses. It was one step forward towards Adam Smith’s waggon-way through the air.

3. The Gold Exchange Standard

A gold exchange standard takes the principle of gold conservation even further. Where the shift onto a gold bullion standard meant that any institution that issued paper money was now obligated to redeem their notes with raw bullion rather than coins, under a gold exchange standard these same issuers could no longer redeem their notes with raw bullion but were required to offer notes of a second-party issuer that was itself on a gold coin or gold bullion standard.

A number of nations adopted this sort of standard in the 1800s and early 1900s, including the Philippines and India. But perhaps the most famous example was the Bretton Woods system that dominated after WWII up until 1971. Under the Bretton Woods system, the U.S. Treasury promised to redeem its notes directly for gold. Most other nations in turn agreed to redeem their notes with a fixed quantity of U.S. Dollars. So while French Francs and Japanese Yen and Canadian Dollars weren’t directly redeemable in gold, they were indirectly convertible.

4. A Partially Convertible, or Limping Gold Bullion Standard

Limping standards originally emerged when bimetallic coin standards were adjusted in such a way that the mints continued to allow free coinage of one of the metals, say gold, but ceased to freely coin the other, say silver. The silver coins were not removed, however, and continued to circulate along with gold coins, the silver coinage “limping on" so to say.

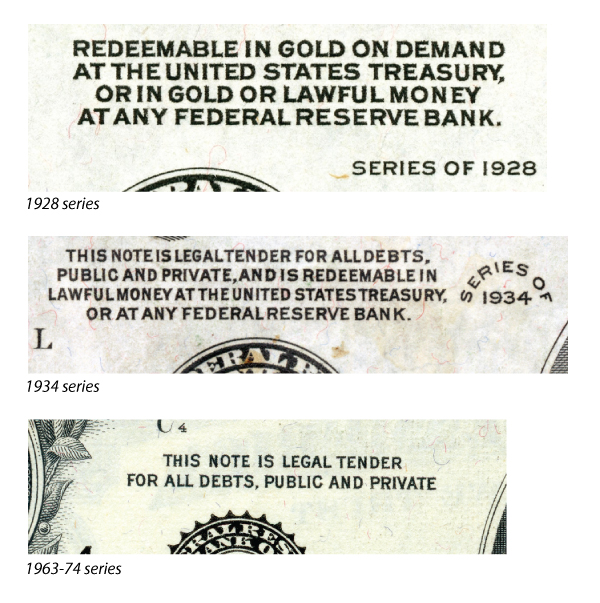

But we are more interested in the limping standard’s more modern incarnation, a partially-convertible gold bullion standard. Rather than allowing everyone the ability to redeem paper banknotes for gold, a central bank (or any other issuer) imposed conditions on who could convert their banknotes. In 1934, for instance, the U.S. ceased allowing private individuals and businesses to convert their notes into gold, limiting this feature to foreign governments and other large government-sponsored entities.

Partially-convertible systems are more convenient for issuers to maintain since they reduce the infrastructure costs involved in maintaining universal convertibility. We see this same principle applied to modern-day Exchange Traded Funds (ETFs), for instance. Although ETF units are convertible into an underlying instrument (say the S&P 500 or gold), only a few select authorized participants have permission to invoke this convertibility option. As long as these authorized participants are motivated by profits, the value of the ETF units will never diverge very far from the value of the underlying instruments. If ETF providers were required to allow everyone to redeem their units, they would have to build out and maintain the requisite infrastructure, the resulting costs pushing up fees.

Likewise, partially-convertible gold bullion standards such as the one that the U.S. ran from 1934 to 1971 could, in principal, lever the financial expertise of a few authorized participants to achieve the same fixedness to gold as a regular gold bullion standard or an old-fashioned gold coin standard, but at far less cost to society. Complicating matters in the U.S.’s case was the fact that only foreign governments could convert dollar banknotes into gold, and these governments were not as efficient as profit-minded ETF authorized participants in policing the link between gold and dollars.

In Summary…

There have been a number of different gold standards over the last thousand or so years. Each iteration brought with it a reduced role for the monetary metals, the resulting reduction in storage and handling costs and the diversion of gold to better uses being a net gain to society.

At the same time, even though gold has had a smaller role to play, the purchasing power of the nation’s monetary units throughout this evolution continued to be tethered to the yellow metal rather than being dictated by some more arbitrary force. Put differently, from one version of the gold standard to the next, society benefited from the price stability afforded by a link to gold while being liberated from some of the metal’s inconvenient physical burdens.

Popular Blog Posts by JP Koning

How Mints Will Be Affected by Surging Bullion Coin Demand

How Mints Will Be Affected by Surging Bullion Coin Demand

Banknotes and Coronavirus

Banknotes and Coronavirus

Gold Confiscation – Can It Happen Again?

Gold Confiscation – Can It Happen Again?

Eight Centuries of Interest Rates

Eight Centuries of Interest Rates

The Shrinking Window For Anonymous Exchange

The Shrinking Window For Anonymous Exchange

A New Era of Digital Gold Payment Systems?

A New Era of Digital Gold Payment Systems?

Life Under a Gold Standard

Life Under a Gold Standard

Why Are Gold & Bonds Rising Together?

Why Are Gold & Bonds Rising Together?

Does Anyone Use the IMF’s SDR?

Does Anyone Use the IMF’s SDR?

HyperBitcoinization

HyperBitcoinization