What Drives Gold & Silver Prices? Key Macroeconomic Factors to Watch

Gold & Silver 101

Gold & Silver 101Gold and silver prices do not move at random. They react to a set of well-understood macroeconomic forces, and recognising those forces as they develop can help you plan ahead, position your allocation appropriately, and understand why prices are moving in a particular direction.

Below are the key drivers of gold and silver prices, explained in detail. While supply and demand ultimately set the price, each of the following factors shapes that supply-demand balance in important ways.

| Driver | Mechanism | Direction |

|---|---|---|

| Inflation | Rising inflation increases gold demand | Bullish for gold |

| Interest Rates | Higher rates raise opportunity cost of holding gold | Bearish for gold |

| US Dollar | Stronger USD means fewer dollars needed to buy gold | Bearish for gold |

| Geopolitical Risk | Instability drives safe-haven demand | Bullish for gold |

| Central Banks | Large-scale buying increases demand | Bullish for gold |

| Industrial Demand | Primarily affects silver; solar, EVs, electronics | Bullish for silver |

Please note that BullionStar does not provide investment or financial advice. The information below is for informational purposes only.

Inflation and Gold: Does Gold Really Protect Purchasing Power?

Yes, gold has historically served as one of the most effective hedges against inflation. Inflation erodes the purchasing power of fiat currencies over time: the same amount of money buys less as prices rise. Gold conversely tends to rise in line with, or at a higher rate than, inflation, helping investors preserve the real value of their wealth.

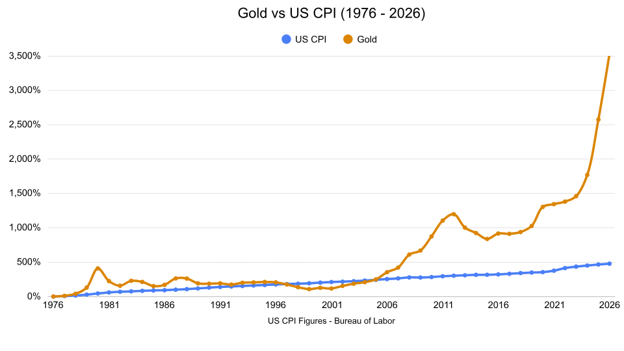

Over the past 50 years, the US dollar has lost roughly 83% of its purchasing power as cumulative inflation has compounded to almost 500%. The price of gold over the same period has risen by approximately 3,500%, substantially outpacing the erosion of currency value.

This relationship holds best over long timeframes. In any given year, gold can rise or fall regardless of inflation. Other factors such as interest rates and dollar strength often dominate in the short run, but across decades, gold’s record as a store of value against currency debasement is well established.

Silver’s relationship with inflation is less clean-cut. It has performed well during some inflationary periods (including scoring new all-time highs in 2025 and 2026) but because roughly half of its annual demand is industrial, the price of silver can diverge from gold during inflationary periods if industrial activity is weakening at the same time.

Interest Rates and Real Yields: The Strongest Single Driver

Interest rates are arguably the most powerful single driver of gold and silver prices. They affect precious metals through two distinct mechanisms.

First, gold and silver are non-yielding assets — they pay no dividend or coupon. This means that when interest rates rise, the opportunity cost of holding gold increases: the same capital could instead be deployed into bonds or savings accounts earning a yield. Conversely, when rates fall, the opportunity cost of holding gold disappears, making the metal more attractive.

What matters most is the real yield, the nominal interest rate minus inflation. When real yields are low or negative, gold tends to rise sharply. When real yields are high and positive, gold faces meaningful headwinds.

Second, higher US interest rates typically strengthen the US dollar. As discussed in the next section, a stronger dollar is independently bearish for gold because gold is a dollar-denominated asset. The interest rate effect on gold therefore works through two channels simultaneously, opportunity cost and dollar strength.

Investors watching for gold price signals should pay particular attention to US Federal Reserve policy decisions, inflation data releases, and movements in real Treasury yields (commonly tracked via TIPS — Treasury Inflation-Protected Securities).

The US Dollar and Gold: An Inverse Relationship

Gold and silver are globally priced in US dollars. This creates a consistent inverse relationship between the dollar and precious metal prices: when the dollar strengthens, gold becomes more expensive in other currencies, dampening international demand and pushing the price lower. When the dollar weakens, gold becomes cheaper in other currencies, stimulating demand and pushing prices higher.

This relationship means that most factors affecting the US dollar also affect gold indirectly. Interest rate differentials between the US and other major economies, US economic growth relative to trading partners, national debt levels, and geopolitical events that influence capital flows into or out of dollar-denominated assets can all move gold through the dollar channel.

For investors based outside the US, including Singapore investors holding gold priced in SGD, the relative performance of their domestic currency against the dollar adds another layer. If the SGD weakens against the USD while gold holds steady in dollar terms, the SGD price of gold will rise, creating a gain for the Singapore-based investor.

Gold in Recessions and Stagflation

Gold typically rises during a recession, or sees meaningful gains in the months that follow, as investors rotate out of riskier assets such as equities and into safe-haven stores of value. The pattern has repeated across the major recessions of the past 50 years.

| Period | Event | Gold Performance |

|---|---|---|

| 1980–1982 | Two recessions driven by rising inflation and the 1979 energy crisis | Rose from ~$300 to over $700/oz |

| Early 2000s | Dot-com bubble collapse, brief recession in 2001 | Rose from ~$260 to $400/oz by Feb 2004 |

| 2007–2009 | Great Recession — subprime mortgage crisis | Rose from $640 to peak over $1,800 by 2011 |

| 2020 | Covid-19 pandemic shock | Rose from ~$1,600 (Feb 2020) to over $2,000 (Aug 2020) |

A recession is not a guarantee that gold will rise immediately. There can be initial selling pressure as investors liquidate assets across the board to raise cash. But gold’s record of recovering quickly and often hitting new highs in the aftermath of recessions makes it a consistent beneficiary of economic downturns over any meaningful timeframe.

Stagflation (a combination of low economic growth and high inflation) presents a particularly favourable environment for gold. High inflation supports gold as a store of value, while weak growth reduces the appeal of equities and other risk assets. The late 1970s is the classic historical example, when gold rose sharply during a prolonged period of stagflation. Central banks’ typical response to stagflation, raising interest rates aggressively to tackle inflation, can create short-term headwinds for gold, but the inflation-driven demand often dominates.

Central Bank Demand and Geopolitical Risk

Central bank demand for gold is a major and increasingly important driver of the gold price. Central banks buy gold to hold as reserve assets — a store of value that underpins national wealth and provides a hedge against currency risk and financial system instability. Unlike private investors, central banks operate on very long time horizons and tend to accumulate gold steadily rather than trade it actively.

The past decade has seen central bank gold purchases rising substantially. 2024 saw the highest gold reserve purchases on record, driven by a desire among central banks (particularly those in emerging markets) to diversify their reserves away from US dollar assets. Events such as the Russia-Ukraine war accelerated this trend after Russia’s foreign currency reserves were frozen by Western sanctions, demonstrating to other central banks the risks of holding reserves in foreign currencies that could be blocked.

Geopolitical risk more broadly (wars, trade disputes, sanctions, and political instability) tends to drive safe-haven demand for gold among private investors as well as governments. Periods of elevated geopolitical uncertainty have historically coincided with gold price spikes, as investors seek assets that hold value independent of any particular government, currency, or financial system.

Silver benefits less directly from central bank buying, as silver is not held as a monetary reserve asset in the same way. However, geopolitical risk can support silver prices indirectly through its general association with precious metals and safe-haven sentiment.

Frequently Asked Questions

Is gold a hedge against inflation?

Yes, gold has long served as a hedge against inflation. Over the past 50 years, gold has risen by approximately 3,500% while the US dollar has lost around 83% of its purchasing power, making it one of the most effective long-run stores of value against currency debasement. The relationship works best over long timeframes; in any given year other factors can dominate.

Does gold go up in a recession?

Gold typically rises during a recession, or in the months that follow, as investors rotate out of riskier assets into safe-haven stores of value. Gold rose during the dot-com recession in the early 2000s, the 2008 Great Recession, and following the Covid-19 shock in 2020. A recession does not guarantee an immediate price rise, but gold’s medium-term record during recessions is consistently positive.

Why does gold fall when interest rates rise?

Higher interest rates increase the opportunity cost of holding gold, since the same capital could earn a yield in bonds or cash. High rates also typically strengthen the US dollar, which is independently bearish for gold as a dollar-priced asset. For these reasons, gold tends to face headwinds in rising rate environments, although the net effect depends heavily on what is happening to inflation at the same time.

What is a real yield and why does it matter for gold?

A real yield is the nominal interest rate minus inflation. When real yields are negative or very low (meaning inflation is running ahead of interest rates) the opportunity cost of holding gold effectively disappears, and gold prices tend to rise sharply. When real yields are high and positive, gold faces more competition from interest-bearing assets. Real yields on US Treasuries (tracked via TIPS) are therefore closely watched as a leading indicator for gold.

Why do central banks buy gold?

Central banks buy gold to hold as a reserve asset — a store of value that hedges against currency risk, inflation, and financial system instability. Gold is also uniquely appealing because it cannot be frozen or sanctioned by foreign governments, unlike foreign currency reserves. Central bank gold demand has risen sharply over the past decade, with 2024 seeing record purchases, driven in part by efforts to diversify away from US dollar reserves.

Does silver follow gold prices?

Silver prices are broadly correlated with gold but with higher volatility. Silver tends to outperform gold when both metals are rising and underperform when both are falling. The key difference is silver’s significant industrial demand from solar panels, electric vehicles, and electronics, which adds a layer of sensitivity to economic growth that gold does not have. The gold-silver ratio (how many ounces of silver one ounce of gold can buy) is a widely used tool for tracking the relative value of the two metals.

Stay Ahead of the Gold and Silver Market

Understanding what drives gold and silver prices is the foundation of any informed precious metals investment strategy. Whether you are positioning for inflation, a shift in interest rate policy, or rising geopolitical risk, BullionStar gives you access to GST-free physical gold and silver bullion in Singapore — with allocated vault storage, 24/7 online trading, and full transparency over your holdings.

Ready to act on what the macro environment is telling you? Buy gold and silver in Singapore through BullionStar online or in person at our bullion centre.

Popular Blog Posts by Gold & Silver 101

Here Are Different Ways to Invest in Gold & Silver Bullion

Here Are Different Ways to Invest in Gold & Silver Bullion

An Introduction to Gold & Silver Investing

An Introduction to Gold & Silver Investing

Should I Invest in Gold, Silver, or Platinum Bullion?

Should I Invest in Gold, Silver, or Platinum Bullion?

Should I Invest in Precious Metals Bars or Coins?

Should I Invest in Precious Metals Bars or Coins?

Learn About Precious Metals' Exemption From Singapore's GST

Learn About Precious Metals' Exemption From Singapore's GST

Storing Precious Metals, Gold, and Silver Bullion

Storing Precious Metals, Gold, and Silver Bullion

Gold & Silver Bullion Investing FAQs

Gold & Silver Bullion Investing FAQs

The Gold Standard: History, Mechanics, and Modern Relevance

The Gold Standard: History, Mechanics, and Modern Relevance

Buy Physical Gold and Silver with PAXG and XAUT

Buy Physical Gold and Silver with PAXG and XAUT

How to Test Silver: A Complete Guide

How to Test Silver: A Complete Guide