Deutsche Bank Returning to LBMA After Nine Years

Ronan Manly

Ronan Manly 0 Comments

0 CommentsIn a brazen development reminiscent of a culprit returning to a crime scene, news has emerged that Germany’s infamous Deutsche Bank is planning to re-join the London Bullion Market Association (LBMA), exactly 9 year after having fled the London gold and silver markets.

According to Bloomberg in an article dated 9 December 2022, titled “Deutsche Bank Seeks to Re-Join Key Gold Trading Club in London”:

“Deutsche Bank AG has applied to re-join the London Bullion Market Association – the world’s foremost standard setter for gold trading – as the German lender seeks to expand its trading unit.”

“The lender was previously one of the few clearers of London-based transactions, and also participated in daily price-setting auctions for gold and silver.”

“Membership [of the LBMA] would give Deutsche Bank a seat at the table where decisions are made on how the world’s top precious metals market is run and would eventually allow it to participate in daily price-setting auctions again.”

First Rat Jumped, Ship then Sank

For those who don’t know the background or have forgotten, recall that it was Deutsche Bank’s abrupt and suspicious departure from the London precious metals markets 9 years ago in January 2014 that actually led to the collapse of the old London Gold and Silver Fixings, as well as the sleight of hand switcheroo replacement of these Fixings with the ‘same old wine in a new bottle’ in the guise of the current LBMA Gold Price and LBMA Silver Price auctions.

This unraveling of the old Fixings then triggered the rest of the bullion banks to flee the sinking Fixings ship, which subsequently precipitated class action suits against Deutsche and its bullion bank peers, as well as US Department of Justice prosecution against Deutsche and other bullion bank traders for precious metals price manipulation.

Indeed, in a delicious example of karma and timing, the aftershocks of that period of corruption in the London precious metals markets are still being felt, for it was only this week on 23 January 2023, that the US Supreme court threw out appeals from two former Deutsche precious metals traders (James Vorley and Cedric Chanu) convicted of manipulating gold and silver prices, with the Supreme Court letting those convictions stand.

Not the ideal PR for Deutsche as it seeks to return to the LBMA fold. This is an entire scandal which Deutsche, headquartered in Frankfurt, and a neighbour of the European Central Bank (ECB), would rather sweep under the carpet.

However, instead of sweeping it under the carpet, now is the ideal time to look at how all of this hangs together, how and why Deutsche Bank panicked in 2014 and fled the old Fixings, how this impacted the LBMA Fixings, how Deutsche and its traders were taken through courts, and why at the end of the day the LBMA bullion banks protect their own while pretending to care about free and fair precious metals markets.

BaFin – All Bark no Bite

Many will remember that prior to investigations into precious metals price manipulations, there was LIBOR (London Interbank Offered Rate), a phrase with such negative connotations that it has come to represent the cesspit of investment bank corruption centred in London. Many will also most likely remember that 2012 marked the year in which the full extent of the LIBOR interest rate rigging scandal emerged, a scandal of such proportions that it attracted investigations by many financial regulators around the world into the collusion and manipulations of a mafia cartel of investment banks including Deutsche Bank, UBS, Barclays, JP Morgan, etc. See for example the FT article here.

At that time, regulators also conducted parallel investigations into the manipulation of another key interest rate benchmark, the Euro Interbank Offered Rate, or Euribor, which also involved Deutsche Bank and the same cartels of investment banks.

As 2012 became 2013 and regulatory fines were imposed and investigations trundled on, regulators (always behind the curve) began turning their attention to the manipulation of the precious metals markets benchmarks (the London Gold Fixing, the London Silver Fixing and the GOFO submissions) by the same bullion banks. These regulators included German financial regulator, BaFin.

News of BaFin’s investigation into precious metals manipulation first broke in December 2013, when the Financial Times revealed that BaFin was compelling Deutsche Bank to provide documents, and that the investigations into Deutsche’s precious metals price manipulations had already at that time been going on for a number of months since mid 2013.

According to Reuters, in an article titled “Deutsche Bank under scrutiny in gold price-fixing probe”, from 13 December 2013:

“German banking regulator Bafin has demanded documents from Deutsche Bank as part of a probe into suspected manipulation of benchmark gold and silver prices by banks, the Financial Times reported, citing sources.”

“The examinations were launched several months ago and are still ongoing,” a Bafin spokesman said.”

“Deutsche declined to comment on the FT report.”

Gold Price Manipulation

As to why at that time in 2013 BaFin was concerned about gold and silver benchmark price manipulation, the following quote from consultancy Fideres provides some context.

From the Financial Times on 23 February 23 2014, and quoted on the BullionStar website here:

“Global gold prices may have been manipulated on 50 per cent of occasions between January 2010 and December 2013, according to analysis by Fideres, a consultancy.

The findings come amid a probe by German and UK regulators into alleged manipulation of the gold price, which is set twice a day by Deutsche Bank, HSBC, Barclays, Bank of Nova Scotia and Société Générale in a process known as the “London gold fixing”.

Fideres’ research found the gold price frequently climbs (or falls) once a twice-daily conference call between the five banks begins, peaks (or troughs) almost exactly as the call ends and then experiences a sharp reversal, a pattern it alleged may be evidence of “collusive behaviour”.

“The behaviour of the gold price is very suspicious in 50 per cent of the cases. This is not something you would expect to see if you take into account normal market factors,“ said Alberto Thomas, a partner at Fideres.”

König’s Speech terrified Deutsche

One month after BaFin’s investigation became public knowledge, the president of BaFin, Dr. Elke König, addressed the precious metals manipulation issue directly during a New Year’s press reception speech in Frankfurt on Thursday 16 January 2014, when she said:

“Another topic has remained loyal to us beyond the turn of the year: the allegations of manipulation relating to important reference rates. While the focus was initially on LIBOR , Euribor & Co. , later allegations were made that the determination of reference values for the foreign exchange and precious metals markets was not done properly.

These allegations are particularly serious because, unlike LIBOR and Euribor, such reference values [of FX and precious metals prices] are typically based on real transactions in liquid markets and not on bank estimates.”

“The central reference values seemed beyond any doubt – and now there is a suspicion that they have been manipulated.”

“Who will keep an eye on whether these private supervisory authorities are actually independent? And can such authorities check whether benchmark interest rates are determined in an honest manner? I have my doubts.

The markets for money market transactions, foreign exchange and precious metals are organized in a decentralized manner. Trading takes place bilaterally to a large extent and not on exchanges or exchange-like platforms. Private supervisory bodies can therefore only observe and monitor a relatively small section of what is happening on the market.”

“When it comes to transparency and control, there is still a lot of catching up to do. But the first steps have already been taken, and more are in preparation. In Brussels, for example, an amendment to the market abuse directive is currently being prepared, according to which the manipulation of benchmarks is to be made a punishable offence.”

This speech by BaFin’s president caused direct panic in Deutsche Bank’s Frankfurt headquarters, because less than 24 hours later on 17 January 2014, Deutsche Bank announced that it was withdrawing from the London Gold Fixing and the London Silver Fixing. Perhaps the ‘punishable offence’ was too much for the Deutsche bigwigs.

As Reuters reported in a Friday 17 January 2014 article titled “Deutsche quits gold price-setting as regulators investigate fix”:

“Deutsche Bank will withdraw from gold and silver benchmark price setting, it said on Friday, as European regulators investigate suspected manipulation of precious metals prices by banks.”

“Bafin reiterated in December that besides benchmark interest-rate LIBOR and Euribor rigging by banks, it had been looking at other benchmark-setting processes such as gold and silver price fixings at individual banks.”

The same article also had the interesting revelation that during the same week, Deutsche had suspended a number of its traders in New York:

“On Wednesday [15 January 2014], global investigations into alleged currency market manipulation intensified as U.S. regulators descended on Citigroup’s Canary Wharf London offices and Deutsche suspended several traders in New York, sources told Reuters.”

A Bloomberg report from the same day, Friday 17 January 2014, added that Deutsche would try to sell its seat on the Gold and Silver fixings, and that it would also withdraw from submitting GOFO rates:

“Deutsche Bank AG will withdraw from participating in setting gold and silver benchmarks in London..”

“The German bank will sell its gold and silver fixing membership and stop submitting gold forward offered rates, according to a person familiar with the decision, who asked not to be identified because the information isn’t public.”

A week after Deutsche announced its hastily planned departure from the London Silver and Gold Fixings on 17 January 2014, more bad news hit Deutsche Bank, when it was announced that former senior risk executive William Broeksmit had committed suicide in his London apartment on 28 January 2014.

According to Reuters in an article dated 25 March 2014:

“The inquest at London’s High Court heard [William] Broeksmit retired from the bank in February 2013 but written medical evidence said he was “very anxious” that summer about authorities investigating areas of banking where he had worked, without giving further details.”|

William Broeksmit’s death also itself triggered a strange series of subsequent events, because his stepson Val Broeksmit then became a whistleblower against Deutsche Bank after accessing his step-father’s files, but he too ended up dying mysteriously in April 2022.

According to a New York Times article from 13 May 2022, titled “Val Broeksmit, 46, Who Blew the Whistle on Deutsche Bank, Dies”:

“when his stepfather, William Broeksmit, a senior Deutsche Bank executive, hanged himself in his London flat [on 26 January 2014], the next day [Monday 27 January], after finding passwords to his stepfather’s email accounts, Val Broeksmit gained access to confidential files incriminating the bank in suspect financial transactions.

“According to suicide notes, the elder Mr. Broeksmit, who colleagues said was an unofficial conscience at the bank, was distraught because he had failed to uncover the alleged fraud.”

“For nearly five years, the younger Mr. Broeksmit teased the F.B.I., congressional investigators and journalists into a hunt for the incriminating needles in a haystack of documents claiming to implicate Deutsche Bank in a run of malfeasance: laundering Russian rubles through stock transactions, manipulating interest rates at which banks lend to each other, and supposedly funneling money from Russian banks to lend to the Trump Organization.”

This same development was covered by Pam and Russ Martens in a WallStreetonParade article on 29 April 2022 titled “Another Raid of Deutsche Bank, Another Dead Whistleblower“, where they said that:

“the younger Broeksmit had obtained “a cache of confidential bank documents” left by his father that provided a “tantalizing” look into the internal workings of Deutsche Bank. Val Broeksmit was sharing the documents with the FBI.

And that:

“Federal and state authorities were swarming around Deutsche Bank. Some of the scrutiny centered on the lender’s two-decade relationship with President Trump and his family. Other areas of focus grew out of Deutsche Bank’s long history of criminal misconduct: manipulating markets, evading taxes, bribing foreign officials, violating international sanctions, defrauding customers, laundering money for Russian billionaires.”

If that was the general state of Deutsche Bank at that time, imagine the specifics of Deutsche’s operations in the precious metals markets.

Clubby Fixes until Deutsche ruined it

As a reminder, prior to its demise in 2014 after Deutsche Bank scarpered, the London Silver Fixing benchmark was a silver price auction conducted each business day in London by representatives of three bullion banks, namely, Deutsche Bank, HSBC Bank USA NA, and the Bank of Nova Scotia (Scotia Mocatta). These three banks operated the silver fixing via a company called The London Silver Market Fixing Limited (LSMFL), registered in London. Each bank had two directors in this company, making 6 directors in total.

At the time in December 2013 when the BaFin investigation into silver price fixing benchmark manipulation became public knowledge, London Silver Market Fixing Limited had the following directors, which you can see in the Companies office filing here:

- Matthew Keen and James Vorley of Deutsche Bank

- Peter Drabwell and David Rose of HSBC

- Simon Weeks and David Wilkinson of Nova Scotia

Then on 18 February 2014, Deutsche’s Matthew Keen resigned as a director of London Silver Market Fixing Limited, and on 22 May 2014, Deutsche’s James Vorley resigned as a director of London Silver Market Fixing Limited. Remember the name James Vorley because it comes up again below.

Given that there were only 3 participants in the London Silver Fixings, the exit of Deutsche Bank would leave the fixing with only two participants (from HSBC and Scotia), a situation which would have been untenable. This meant that Deutsche had to try to sell its seat on the London Silver Fixing to another bank. However, due to the regulatory investigations, no bank wanted to buy a seat into a benchmark process that was actively being investigated.

As Reuters explained on 29 April 2014 in an article titled “Deutsche Bank resigns gold, silver fix seat, gives two weeks’ notice”:

“Deutsche Bank has resigned its seat on the London gold and silver fix without finding a buyer, a spokesman for the bank said on Tuesday.

A source close to the matter said the bank gave two weeks’ notice and it will cease to be part of the price-setting process as of 13 May.”

In a similar structure to the London Silver Fixings at that time in January 2014, the London Gold Fixings was operated by a company called The London Gold Market Fixing Limited (LGMFL), but whereas the Silver Fixings had 3 participant bullion banks of Deutsche Bank, The Bank of Nova Scotia and HSBC, the Gold Fixings had 5 participant bullion banks of Deutsche Bank, the Bank of Nova Scotia, HSBC, Barclays and Société Générale.

At the time in December 2013 when the BaFin investigation into silver price fixing benchmark manipulation became public knowledge, London Gold Market Fixing Limited had the following 10 directors, 2 from each bank, which you can see in the Companies office filings including the main list here:

- Matthew Keen and James Vorley of Deutsche Bank

- Peter Drabwell and David Rose of HSBC

- Simon Weeks and Steven Lowe of Nova Scotia

- Jonathan Spall and Martyn Whitehead of Barclays

- Vincent Domien and Francois Combes of SocGen

Then on 20 February 2014, Deutsche’s Matthew Keen resigned as a director of London Gold Market Fixing Limited (replaced by Deutsche’s Kevin Rodgers), and on 13 May 2014, Deutsche’s James Vorley resigned as a director of London Gold Market Fixing Limited (LGMFL). Kevin Rodgers then also resigned from LGMFL at the same time.

Matthew Keen also resigned as a director of the precious metals clearing company ‘London Precious Metals Clearing Limited’ on 20 January 2014. See here.

During February 2014, Deutsche Bank also ceased contributing to the GOFO benchmark and ceased being a LBMA market maker for precious metals forwards, and furthermore, in March 2014 Deutsche Bank’s representative on the London Bullion Market Association’s (LBMA) management committee, Ronan Donohoe, resigned from the LBMA management committee on 5 March 2014, only 7 months into a 2 year appointment.

Covering Tracks and Burying Evidence

Everything about Deutsche Bank’s exit from the London precious metals markets in 2014 was rushed and panicked. Including the fact that Deutsche Bank had commissioned the building of a massive precious metals vault at in London (operated by GS4) and then just walked away from it in 2014.

This was the vault in Park Royal (north-west London) which is discussed in the BullionStar article here and which is profiled in the BullionStar Gold University article here:

“In 2012, G4S Cash Solutions (UK) and Deutsche Bank announced that it had concluded an agreement for G4S to build and operate a precious metals vault in London on behalf of Deutsche Bank. The vault was constructed over 2013/2014 and opened in June 2014.

Deutsche Bank had entered a 10 year lease with G4S under which G4S was contracted to operate the vault exclusively on behalf of Deutsche Bank and its clients.

However in December 2014, Deutsche Bank announced that the lease on the vault was for sale since it had decided to withdraw from its precious metals operations in London. In early 2016, ICBC Standard Bank confirmed that it was buying the lease on the G4S vault from Deutsche Bank.”

While Deutsche Bank contractually had to take delivery of the vault in June 2014 and announce its opening, Deutsche then less that 5 months later announced the sale of the vault despite the huge level of commitment that Deutsche had made to the development of the vault for at least 4-5 years beginning in 2009.

By November 2014, Deutsche Bank announced that it was closing down its entire precious metals trading business. See the Reuters article from 27 November 2014 titled “Deutsche Bank shuts down physical precious metals trading”.

This included Deutsche Bank’s membership of London Precious Metals Clearing Limited (LPMCL), of which it had been a member alongside JP Morgan Chase, HSBC Bank USA, Scotia, UBS, and Barclays. Deutsche Bank resigned from LPMCL in August 2015.

On 14 August 2014, the old London Silver Fixing was replaced by the new ‘LBMA Silver Price’ auction. The only difference was that instead of the 3 participants being Deutsche Bank. HSBC and Scotia, Deutsche Bank was absent, and the 3 participants were HSBC, Scotia and Mitsui & Co Precious Metals Inc.

On 20 March 2015, a similar switcheroo exercise occurred for the London Gold Fixing, which was replaced by the ‘LBMA Gold Price’ auction. The only difference was that Deutsche Bank had departed, with Barclays, HSBC, Scotia and SocGen being joined by UBS and Goldman Sachs.

Everything about Deutsche’s exit from the gold and silver markets in 2014-2015 suggests that it was a case of covering tracks and burying evidence, like when an intelligence operation is compromised and the unit has to evacuate and destroy evidence of its existence.

Class Actions – The Achilles Heel

However, despite Deutsche Bank fleeing the crime scene of the London gold and silver markets, this didn’t stop class action law suits and Government prosecutions which involved Deutsche as defendant.

One such class action lawsuit was titled “London Silver Fixing Ltd Antitrust Litigation, U.S. District Court, Southern District of New York, No. 14-md-02573" and was overseen by federal judge Valerie E Caproni in the US District Court for the Southern District of New York. This case involved a consolidated class of investors (the plaintiffs), who alleged that the defendants (Deutsche Bank, HSBC and Scotia and London Silver Market Fixing Company) colluded to fix the price of silver futures by publishing false silver prices, so that they, as members of London Silver Market Fixing Company would benefit from price movements.

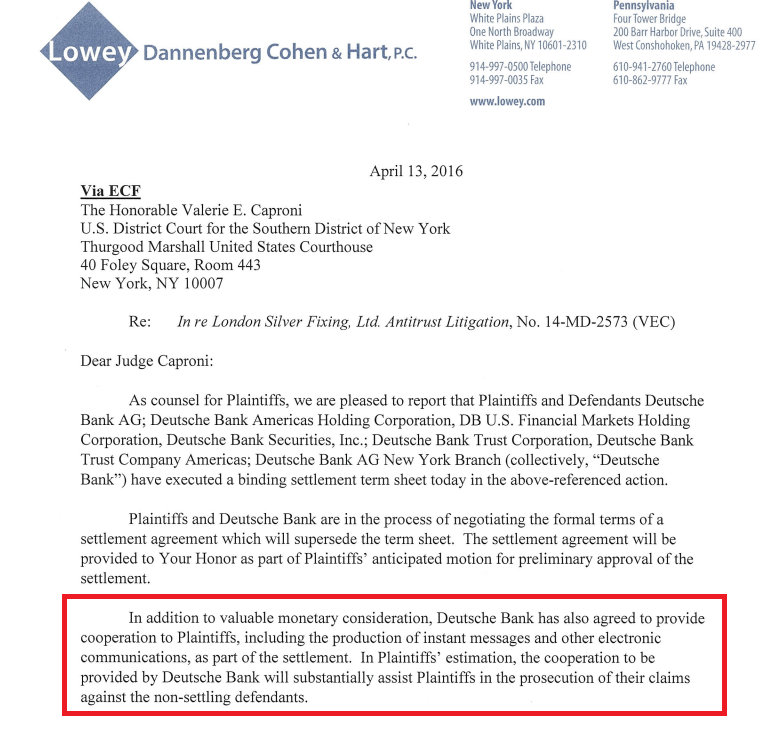

In April 2016, Deutsche Bank shocked the rest of the defendants by turning snitch and negotiating a formal settlement agreement with the plaintiffs. See full letter of Deutsche Bank’s legal representatives Lowey Dannenberg, Cohan & Hart to the federal judge Valerie E Caproni here. The letter stated that:

“In addition to valuable monetary consideration, Deutsche Bank has also agreed to provide cooperation to plaintiffs, including the production of instant messages, and other electronic communications, as part of the settlement.

In Plaintiff’s estimation, the cooperation to be provided by Deutsche Bank will substantially assist Plaintiffs in the prosecution of their claims against the non-settling defendants.“

See BullionStar article from 14 April 2016, titled “Deutsche Bank agrees to settle with Plaintiffs in London Silver Fixing litigation”. For some more background to that case see the articles by Allan Flynn on the BullionStar website titled “‘Very skeptical’ judge – former FBI/SEC official eyes London gold and silver fix lawsuits" and the eye-opening “How to Trigger a Silver Avalanche by a Pebble: ‘Smash(ed) it Good‘" which discusses:

“transcripts showing conspiracy to manipulate silver, provided by Deutsche Bank as part of an April settlement agreement, includes extensive smoking gun evidence involving UBS and other banks. Plaintiffs describe a “multi-year, well-coordinated and wide-ranging conspiracy to rig the prices of silver and silver financial instruments that far surpasses” that of the previous complaint, including potentially incriminating evidence of UBS precious metals traders allegedly conspiring with other banks."

“Five additional banks to the remaining defendants HSBC and Bank of Nova Scotia are mentioned including Barclays Bank, BNP Paribas, Standard Chartered Bank, Bank of America and Merrill Lynch.“

“Included in the memo are numerous astounding transcripts indicating coordination between UBS and other banks of “pushing,” ”smashing,” ”bending,” ”hammering,” ”blading,” ”muscling,” and “ramping” the prices of silver and silver financial instruments.“

At the same time, Deutsche Bank became snitch and reached settlement with the Court in the parallel class action against the London Gold Market Fixing Company and its member banks for manipulating gold futures prices (i.e. Commodity Exchange Inc., Gold Futures and Options Trading Litig., S.D.N.Y., 14-md-02548, 4/14/16). See Bloomberg article “Deutsche Bank Settles Silver, Gold Price-Manipulation Suits“. Deutsche Bank paid US$ 60 million to get out of the suit – see here.

Bu November 2021, all the remaining defendants (Barclays, HSBC, SocGen, and Scotia) had also paid to exit the suit. See BullionStar article from November 2021 titled “Bullion Banksters pay $50 million to Get Out of Jail Free“.

Big Guns Enter – Department of Justice

Following the progress of the class action suits, there then followed official government prosecutions against various precious metals traders and their employer banks. This included the US Department of Justice criminally charging Deutsche Bank’s James Vorley and Cedric Chanu. According to the DoJ charges in January 2018:

“James Vorley, 37, of the United Kingdom, and Cedric Chanu, 39, a French citizen, are charged in a criminal complaint with conspiracy, wire fraud, commodities fraud, and spoofing offenses in connection with executing a scheme to defraud involving both solo and coordinated spoofing on the COMEX while they were employed as precious metals traders at a leading global financial institution [Deutsche Bank]. Vorley was based in London, United Kingdom and Chanu was based in London, and the Republic of Singapore."

In parallel during January 2018, the Commodity and Futures Trading Commission (CFTC) charged James Vorley and Cedric Chanu in a civil action:

“The Commodity Futures Trading Commission (CFTC) announced the filing of a civil enforcement action in the U.S. District Court for the Northern District of Illinois against James Vorley, a U.K. resident, and Cedric Chanu, a United Arab Emirates resident, charging them with spoofing and engaging in a manipulative and deceptive scheme in the precious metals futures markets."

According to the US DoJ indictment, and which is explained in another Allan Flynn article from April 2018 on the BullionStar website. titled “US Gold and Silver Futures Markets – ‘Easy Targets‘":

“from at least May, 2008, Vorley was running a ‘self enrichment scheme’ to defraud the COMEX precious metals futures markets and spoof training a new employee. His collaborators: Chanu and other Deutsche Bank traders, and those at another bank.

According to the indictment, the FBI uncovered over ‘a thousand’ instances of Vorley trading in a pattern consistent with spoofing, ‘placing over ten thousand Opposite Orders,’ presumably withdrawn, and coordinating in spoofing with his Deutsche Bank colleague Cedric Chanu ‘over one hundred times’ up to March, 2015.

Included, an episode on March 16, 2011, when Vorley is recorded chatting to his colleague about “spoofing it up / ahem ahem” in relation to simultaneous platinum and gold futures trades.

Deutsche Bank co-conspirator turned informant David Liew whom Vorley trained in spoofing, testifies that Vorley preferred the term ‘jam it’ when referring to the illegal act.

After one operation assisting Liew getting an order filled on November 3, 2010, Vorley ‘submitted and cancelled 29 buy orders at 10 contracts each’, and celebrated after: ‘was cladssic [sic] / jam it / woooooooooooo…bif [sic] it up.’

As a sign of gratitude, his understudy Liew responded glowingly: ‘tricks from the…master.'"

Completing the Circle back to Vorley

You will notice here that the Deutsche Bank precious metals trader James Vorley in the US DoJ indictment and the CFTC civil action, is the same James Vorley who was a director of the London Gold and Silver Fixing Companies and who resigned from the Fixing companies in May 2014 as Deutsche Bank fled the LBMA and the London gold and silver markets.

Which is even spelled out in black and white in a BullionStar article from 18 September 2020, aptly titled “Deutsche trader under DoJ prosecution, was a long time director of London Gold and Silver Fixings“, which explains Vorley’s gold and silver fixing background in detail and the DoJ and CFTC charges against him for manipulating gold and silver futures. A connection which was pretty obvious but which the mainstream financial media somehow ignored.

On 25 September 2020, a Chicago federal jury found Vorley and Chanu “guilty today of fraud charges for their respective roles in fraudulent and manipulative trading practices involving publicly-traded precious metals futures contracts." See DoJ press release titled “Two Former Deutsche Bank Traders Convicted of Engaging in Deceptive and Manipulative Trading Practices in U.S. Commodities Markets“. Both Vorley and Chanu were sentenced to prison for a year and a day for “for ‘spoofing’ the futures market for gold and silver between 2008 and 2013."

Last month in December 2022, Vorley and Chanu petitioned the US Supreme Court to overturn their convictions. See submission document here. However, on 23 January 2023, the Supreme Court rejected Vorley and Chanu’s appeals. See the Reuters report here.

Conclusion – A Leopard Doesn’t Change its Spots

In February 2016, German financial regulator BaFin highlighted the complete corruption of the regulator-investment bank nexus when it unbelievably closed its investigation into Deutche Bank’s precious metals price manipulations without any charges or reprimand. According to Reuters in an article from 25 February titled “BaFin closes Deutsche Bank special audits on Libor, Monte dei Paschi“:

“German financial watchdog Bafin has closed special audits on Deutsche Bank and will take no further action against the lender for its role in the interest rate rigging and precious metals price fixing scandals as well as a derivatives trade with Italy’s Monte dei Paschi.

Bafin does not see the need to take further action against the bank or former and current members of the management board with respect to the closed special audits,” Deutsche Bank said in a statement on Thursday."

This is despite numerous other regulators such as the UK’s FCA, the European Commission, and the New York State Department of Financial Services, to name but a few, imposing huge fines on Deutsche Bank, for interest rate benchmark manipulation.

For example, in April 2015, the UK Financial Conduct Authority (FCA) handed:

“Deutsche Bank AG (Deutsche Bank) a £227 million ($340 million) fine, its largest ever for LIBOR and EURIBOR-related (collectively known as IBOR) misconduct. The fine is so large because Deutsche Bank also misled the regulator, which could have hampered its investigation.”

This case stands out for the seriousness and duration of the breaches by Deutsche Bank – something reflected in the size of today’s fine. One division at Deutsche Bank had a culture of generating profits without proper regard to the integrity of the market. This wasn’t limited to a few individuals but, on certain desks, it appeared deeply ingrained.” ‘

In 2013, the European Commission fined 8 investment banks including Deutsche Bank a combined € 1.49 billion for participation in illegal cartels in markets for financial derivatives. Deutsche, along with Barclays, were the longest serving members of the Euro Interest Rate Derivatives (EIRD) cartel, at 32 months a piece.

In April 2015, the New York State Department of Financial Services (NYDFS) announced that it had fined Deutsche Bank US $ 2.5 billion. The no holes barred press release from the NYDFS actual begins as follows:

“NYFDS announces Deutsche Bank To Pay $2.5 billion, Terminate And Ban Individual Employees, Install Independent Monitor For Interest Rate Manipulation

Widespread Effort by Bank Employees to Manipulate Benchmark Interest Rate Submissions for LIBOR, EURIBOR, TIBOR

Deutsche Bank Employee: This “is a corrupt fixing and DB is part of it!"

Deutsche Bank Employee Seeking to Obtain Lower Rate: “I’m begging u, don’t forget me… pleassssssssssssssseeeeeeeeee… I’m on my knees…"

Now you can see how corrupt BaFin was for not taking action against Deutsche Bank for interest rate manipulation. And that’s not even getting started looking at BaFin’s refusal to take action against Deutsche Bank for precious metals benchmark and price manipulation, manipulation which was proven by the class actions against Deutsche and the Fixing Companies, was even in records which Deutsche Bank handed over to the federal judges in the class action cases, and was even in evidence which was also used to convict Vorley and Chanu in the US DoJ case.

Unbelievably (or not), a few weeks ago in December 2022, Deutsche Bank was still being fined by regulators for breaching rules on benchmark submissions. On 29 December 2022, in an article titled “Deutsche Bank Faces $9.8 Million Fine by German Finance Watchdog”, Bloomberg reported that:

“Germany’s finance watchdog fined Deutsche Bank EUR 8.66 million over its handling of submissions for Euribor, a reference rate at the heart of a scandal that rocked the industry.

The lender temporarily didn’t have effective systems and controls for contributions to the benchmark, BaFin, said in a statement.

More than a decade after the financial crisis revealed rampant misconduct and deficient controls, banks are still working through remediation measures and regulatory investigations. While comparatively small, the BaFin fine suggests that Deutsche Bank hasn’t fully delivered on pledges it made after facing the industry’s highest penalties in the Libor benchmark-rigging scandal.”

Not only that but in November 2022, Deutsche Bank was again in the crosshairs of BaFin, this time for money laundering concerns. According to a Financial News London report on 7 November 2022:

“Germany’s top financial watchdog threatened to fine Deutsche Bank if it doesn’t implement controls against money laundering by a set deadline, suggesting the regulator isn’t satisfied with the bank’s efforts to police dirty-money flows.”

So now you can see, this is the same Deutsche Bank which has now again applied to become a member of the London Bullion Market Association (LBMA), and which “would give Deutsche Bank a seat at the table where decisions are made on how the world’s top precious metals market is run and would eventually allow it to participate in daily price-setting auctions again.”

Why do criminals return to the scene of a crime? Is it because they feel powerful or invincible, or that they are obsessed with their past activities? As to why Deutsche Bank is returning to the London gold and silver markets, maybe we need to ask a criminal psychologist. Maybe Deutsche now represents powerful European interests who want a seat at the gold table, or maybe it’s more simple and as bank robber Willie Sutton famously answered when asked why he robbed banks, replied “because that’s where the money is."

Popular Blog Posts by Ronan Manly

How Many Silver Bars Are in the LBMA's London Vaults?

How Many Silver Bars Are in the LBMA's London Vaults?

ECB Gold Stored in 5 Locations, Won't Disclose Gold Bar List

ECB Gold Stored in 5 Locations, Won't Disclose Gold Bar List

German Government Escalates War On Gold

German Government Escalates War On Gold

Polish Central Bank Airlifts 8,000 Gold Bars From London

Polish Central Bank Airlifts 8,000 Gold Bars From London

Quantum Leap as ABN AMRO Questions Gold Price Discovery

Quantum Leap as ABN AMRO Questions Gold Price Discovery

How Militaries Use Gold Coins as Emergency Money

How Militaries Use Gold Coins as Emergency Money

Hungary Announces 10-Fold Jump in Gold Reserves

Hungary Announces 10-Fold Jump in Gold Reserves

Planned in Advance by Central Banks: a 2020 System Reset

Planned in Advance by Central Banks: a 2020 System Reset

China’s Golden Gateway: How the SGE’s Hong Kong Vault will shake up global gold markets

China’s Golden Gateway: How the SGE’s Hong Kong Vault will shake up global gold markets