Spotlight on LPMCL: London Precious Metals Clearing Limited

Ronan Manly

Ronan Manly 0 Comments

0 CommentsWithin the last 2 months, there have been a series of developments in the London Gold Market, each of which has involved Chinese-controlled banking group ICBC Standard Bank Plc.

- On 4 April, the London Bullion Market Association (LBMA) announced that ICBC Standard Bank had been reclassified as a LBMA Market Making member for the OTC spot trading markets in gold and silver.

- On 11 April, ICE Benchmark Administration announced that ICBC Standard Bank had been approved for direct participation in the daily benchmark LBMA Gold Price auctions beginning on 16 May.

- On 3 May, the LBMA announced in its Alchemist magazine that ICBC Standard Bank had joined the LBMA’s Physical Committee. This committee is responsible for aspects of the physical bullion market such as the LBMA’s Good Delivery List and it also liaises with the LBMA’s Vault Managers Working Party.

- On 11 May, the relatively obscure but powerful London Precious Metals Clearing Limited (LPMCL) announced that ICBC Standard Bank had joined LPMCL, the first membership addition to London’s monopoly bullion clearing group since 2005.

- On 16 May, ICBC Standard Bank announced that it had agreed to acquire a London-based precious metals vault currently owned by Barclays. This precious metals vault was built by, and is operated by Brinks, on behalf of Barclays. ICBC Standard says that the vault acquisition will be completed by July 2016.

Therefore, within a period of approximately 6 weeks, ICBC Standard has positioned itself front and centre of the closely protected London bullion trading, clearing and vaulting infrastructure.

[Note: On 1 February 2015, Chinese bank Industrial and Commercial Bank of China (ICBC) acquired a controlling interest in London headquartered Standard Bank Plc, hence the name change to ICBC Standard Bank PLC].

On Monday 16 May 2016, the LBMA also issued its own press release, announcing that ICBC Standard bank had joined LPMCL, and that it would become an ‘active member‘ of LPMCL in early June 2016.

The LBMA press release about LPMCL also quoted LBMA CEO Ruth Crowell as saying:

“I’m delighted to see ICBC Standard Bank join this vital organisation. The LPMCL clearing system is one of the great strengths of the London bullion market. The LBMA welcomes this addition and looks forward to continuing to assist LPMCL in its growth and development.”

Although the same bullion bank representatives, wearing different hats, run, and have always run, all of the precious metals entities that operate in the London market (via a series of different ‘puppet shows’), the ‘assistance’ that the LBMA is now providing to LPMCL is based on the following development that was highlighted by the LBMA CEO at the LBMA conference in Vienna in 2015, when she said:

“I’m delighted to inform you that the London Precious Metals Clearing company took part not only [in the LBMA] review, but we have now agreed to formalise our working relationship, with the LBMA providing Executive services going forward. I’m grateful to the LPMCL directors for their leadership and their support for removing fragmentation from the market."

Examination of the Barclays / Brinks vault (most likely near Heathrow in the Brinks complex) which ICBC is now acquiring, is left to a future analysis. This article concentrates solely on the LPMCL clearing system, the protected crux of the London precious metals markets, but an entity which is rarely given anything but a passing glance by the financial media in London or elsewhere.

One important point to mention here though is that it had been widely reported in January (initially by Reuters) that ICBC was acquiring another London-based precious metals vault, a vault that had been built by G4S in Park Royal on behalf of Deutsche Bank, and that had then been leased from G4S by Deutsche Bank. See “G4S London Gold Vault 2.0 – ICBC Standard Bank in, Deutsche Bank out" for details.

It turns out that the deal for the G4S / Deutsche Bank vault “did not go through“, according to ICBC. It appears that ICBC considered the Barclays / Brinks vault to be the preferred transaction over the Deutsche / G4S vault, and that when the Barclays / Brinks vault came on to the market, ICBC backed out of the transaction with Deutsche, in much the same as house-hunters change their mind when a better house comes on the market.

The future of the G4S / Deutsche vault is therefore still unknown. Possibly Standard Chartered, which was also mentioned as a name wanting to join LPMCL, could be a potential buyer of the Deutsche / G4S vault?

It’s also interesting to note that “London Precious Metal Clearing Limited (LPMCL) provides formal recognition of companies to provide vaulting services“, not the LBMA.

LPMCL – The Company

London Precious Metals Clearing Limited (LPMCL) is a UK private company limited by guarantee without share capital, that was incorporated on 5 April 2001, with a company number of 04195299. LPMCL is classified in Companies House with a Standard Industrial Classification (SIC) code of ‘Administration of financial markets‘. LPMCL has a registered address of C/O Hackwood Secretaries Limited, One Silk Street, London EC2Y 8HQ. Interestingly, this is the same registered address as the London Gold Market Fixing Limited and the London Silver Market Fixing Company Limited, both of which are still active companies and both of which are currently defendants in ongoing New York court class action suits where they and their member banks stand accused of price manipulation in the gold and silver markets, respectively. Hackwood Secretaries Limited is Company Secretary for LPMCL. Hackwood Secretaries is a Linklaters company used for company secretariat services. Linklaters is one of the better known global law firms that is headquartered in London.

LPMCL uses an electronic clearing platform called ‘AURUM’ to clear London-settled precious metals trades. This is done via book entry netting and clearing, entirely using unallocated accounts. The vast majority of the LPMCL clearing trades are processed by HSBC and JP Morgan.

As to the raison d’etre for LPMCL, perhaps the recent LBMA press release sums it up best:

“[the] London clearing system for gold, silver, platinum and palladium [is] managed by London Precious Metals Clearing Limited (LPMCL).

LPMCL operates a central electronic metal clearing hub, with deals between parties throughout the world, settled and cleared in London.

Most global ‘over-the-counter’ gold and silver trading is cleared through the London clearing system. The London bullion market clearing banks provide a service to their clients in providing the settlement of gold and silver transfers. Ultimately each clearer has to have access to reserves of physical metal and provides an array of services tailored to each client’s specific needs; the most important of which is intermediating credit and providing credit facilities.

This last paragraph in the press release was cut and pasted by the LBMA from the LPMCL website FAQ under the question: “Can you explain the benefits of the London bullion clearing system as compared with a clearing house?" so it can also be viewed there.

You will notice from the above press release that:

a) LPMCL is critically important due to its role as global clearer for all 4 precious metals, and

b) Access to physical precious metals plays a secondary role in the LPMCL system compared to ‘credit facilities and intermediating credit (i.e. The LPMCL system is a credit-based fractional-reserve system of unallocated metal holdings and transfers).

LPMCL was founded in 2001 by 7 bullion bank founding members, namely, NM Rothschilds, JP Morgan Chase, HSBC Bank USA, ScotiaMocatta, UBS AG, Deutsche Bank , and CSFB (Credit Suisse). Credit Suisse resigned in October 2001, Rothschilds resigned in June 2004, and then Barclays joined in September 2005. Deutsche bank resigned in August 2015. HSBC Bank USA NA resigned on 11 February 2015, and was replaced by HSBC Bank Plc. Gold and silver were the two metals originally cleared loco London by LPMCL’s system. Platinum and palladium clearing loco London was added to LPMCL’s clearing offering in September 2009. UBS (a LPMCL member) and Credit Suisse (a previous LPMCL member) also offer loco Zurich clearing of platinum and palladium.

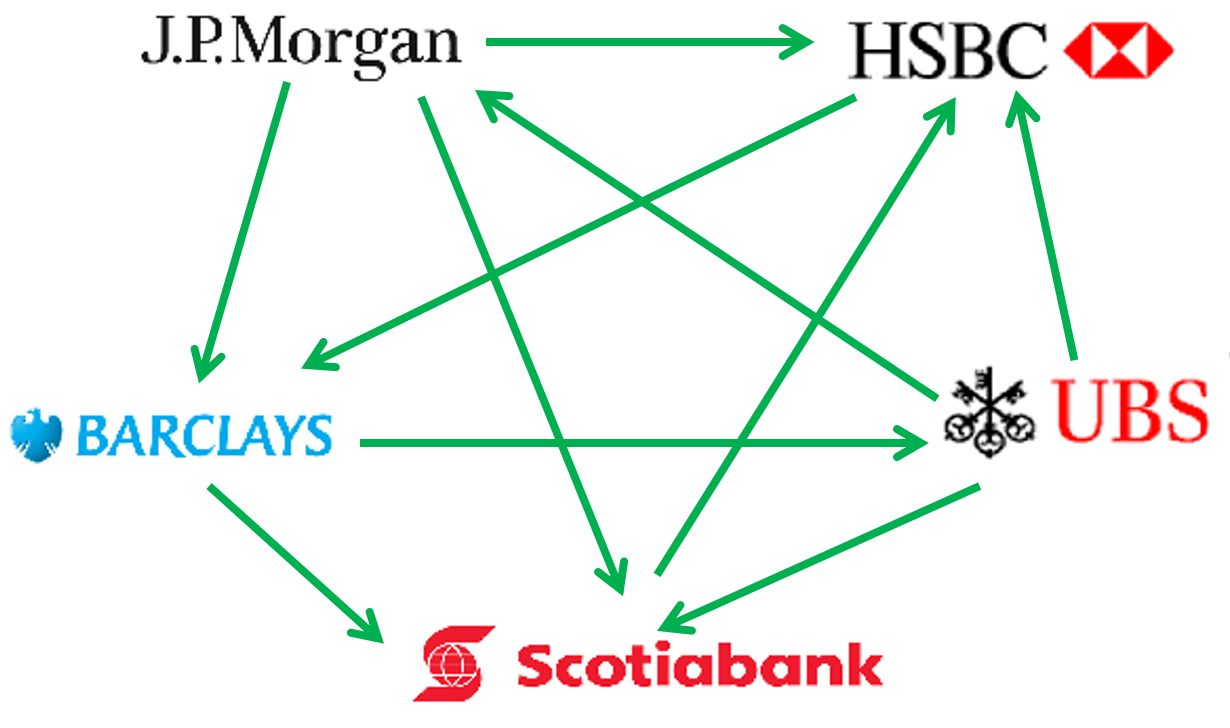

Including ICBC Standard Bank, the current membership of LPMCL as of May/June 2016 now consists of JP Morgan, HSBC, Scotia Mocatta, UBS, Barclays, and ICBC Standard. Since Barclays is withdrawing from much of its precious metals business in London, and is selling its London vault , its possible that Barclays will resign from LPMCL in the near future.

All LPMCL members either have their own precious metals vault in London, or access to vaulting facilities at London vaults. Many of the LPMCL members also have vaulting facilities in other financial capitals around the world. Here are some of the vault operations for each of the LPMCL members:

- HSBC – vaults in London, New York (Manhattan) and Hong Kong

- JP Morgan – vaults in London, New York (Manhattan) and Singapore (Freeport)

- Scotia – vaults in Toronto and New York (JFK)

- Barclays – vault in London (being sold), vault in Singapore

- UBS – vault in Zurich (Kloten) and Singapore (Freeport)

- Deutsche Bank (ex LPMCL) – trying to sell a lease on a G4S vault in London; has / had a vault in Singapore (Freeport)

- ICBC Standard – buying vault in London from Barclays. Standard Bank had vaulting facilities at JP Morgan’s vault in London. ICBC has many vaults in China.

Notice also that 4 of the LPMCL member banks, HSBC, JP Morgan, Scotia and UBS are also 4 of the 6 banks represented on the LBMA Management Committee, therefore LPMCL members have a disproportionately large influence on the strategic direction and decision-making of the LBMA.

LPMCL’s original Memorandum and Articles of Association, signed by representatives of the 7 founding bullion banks can be seen here -> LPMCL Memorandum and Articles of Association October 2001. One of LPMCL’s main objectives in its Memorandum of Association is:

“to take on and continue the promotion, administration and conduct of precious metals clearing in the London precious metals markets"

According to the original Articles of Association, the registered ‘Office’ of LPMCL was “New Court, St Swithin’s Lane, London EC4P 4DU“, which is the headquarters of N.M. Rothschild & Sons in London. Rothschilds was also the company Secretary at that time. Interestingly, the respective addresses listed for JP Morgan and HSBC in the Memorandum and Articles of Association document are “60 Victoria Embankment", and “Thames Exchange, 10 Queen Street Place", which is the location of JP Morgan’s London precious metals vault, and a supposed location of HSBC’s London precious metals vault, respectively.

Why LPMCL was Established

According to the history section of the LPMCL’s website, the London bullion market first felt the need to develop an electronic clearing / matching system in the mid-1990s due to a combination of growing trade volumes, technological change, and also the need for better audit trails. This view is backed up by comments from Peter Smith of JP Morgan in a 2009 article for the LBMA’s Alchemist when he said that:

“Thirteen years ago [1996], the bullion clearers were exchanging transfers between themselves by telephone instructions – a situation that was causing considerable problems in the control and audit departments within those banks. Because of those concerns, the clearers realised that the only sensible and secure solution was to develop a central clearing hub, where transfer instructions could be up loaded and matched. This resulted in the establishment of LPMCL in April 2001"

The LPMCL website’s history section also reveals that the initial legwork on automating London precious metals clearing was done by the LBMA’s physical committee, since this committee “comprised the clearing members".

Until very recently, the LBMA physical committee was exclusively made up of LPMCL members, indeed, the LBMA physical committee literally looks like an alternate venue for LPMCL members to meet up in. For example, in September 2015, the only members of the LBMA physical committee were representatives from the then 5 members of LPMCL, i.e. JP Morgan, HSBC, Scotia, UBS and Barclays.

The addition of ICBC Standard and Standard Chartered to the LBMA Physical Committee was announced in the LBMA’s Alchemist on 3 May 2016. Currently, all 6 LPMCL members – JP Morgan (chair of physical committee), HSBC, ScotiaMocatta, Barclays, UBS, and ICBC Standard Bank are members of the LBMA physical committee, as is Standard Chartered (a potential member of LPMCL), and TD Bank (Toronto Dominion). Note that Standard Chartered and TD Bank are the 5th and 6th member banks of the LBMA Management Committee. Therefore all 6 bullion banks that are on the LBMA Management Committee are also on the LBMA Physical Committee.

The LBMA physical committee membership is rounded off by Brinks (notably, the vault transaction facilitator between Barclays and ICBC Standard Bank) . Note also, that there is a Bank of England ‘observer’ on the LBMA physical committee, an indication of the Bank of England’s keen interest in monitoring the London Gold Market and the gold market’s physical operations and transactions.

The LPMCL history goes on to say that:

“It was subsequently decided that the most effective way of carrying the electronic matching system project forward would be for the clearing members to form a separate company specifically for the purpose of developing and administering such a system. As a result LPMCL was formed in April, 2001.“

Obscurely, LPMCL was first incorporated on 5 April 2001 with a name of Itemelement Limited (basically a shell company). It changed name to London Precious Metal Clearing Limited on 2 October 2001 (‘Metal’ singular). It then changed name again on 2 November 2001 to London Precious Metals Clearing Limited (‘metals’ plural). The first tranche of LPMCL directors were then installed in November 2001 from the six remaining founder members companies (excluding Credit Suisse First Boston International since CSFB resigned in October 2001).

OM and LBT Computer Services

Its unclear what, if anything, LPMCL did as a company in 2002, however in April 2003 a press release was issued by Swedish technology company OM revealing that:

“London Precious Metals Clearing Limited (”LPMCL”) has chosen OM as an outsourcing partner for Facility Management of their proposed web-based automated bullion matching system to be provided by LBT Computer Services, an Information Technology service provider and partner to OM."

“We are happy to welcome LPMCL, the leading organization for precious metal clearing, as a Facility Management customer to OM."

This ‘web-based automated bullion matching system’ is “AURUM".

The same press release described LPMCL as:

“LPMCL is the administrative company set up by the six clearing members of the LBMA to facilitate the development of an electronic matching system to replace the existing clearing system which is conducted by telephone and / or facsimile."

In 2003, OM also merged with Finland’s NEX to form OMHEX. Following the merger OM continued to exist as the OM Technology division of OMHEX, providing transaction technology services to the financial and energy industries. OMHEX became OMX in 2004, and was then acquired by NASDAQ in 2007 to form the current group NASDAQ OMX.

However, the relevant entity here is LBT Computer Services, which is still around today as it’s website shows. The LBT web site also still has a short profile of its LPMCL project in the ‘case study’ section of its website, where is states, in a slightly childish way that:

“The LPMCL are the ‘clearing’ organisation for precious metal dealing and are based in London, the centre for such trading. They needed a way of linking together the precious metal bankers to match transactions/deals. They needed to do it in such a fashion that no bank could see anything other than their counterparty bank, and to do it with absolute security.

LBT built an application that is hosted on the Internet and which connects to each bank via a secure link to collect transactions which it then matches to the counterparty bank’s transactions and send the results back to both banks. It runs 24 x 7, unattended, other than via an on-line link. Unfortunately we cannot say more about this innovative solution.“

Why can’t LBT Services say anything more about the LPMCL automated platform? This statement from LBT is perhaps the first clue as to the secrecy, paranoia, and obsessive protectionism that surrounds LPMCL, a company that is the global clearer for all 4 precious metals, yet lies at the heart of the opaque system that is the global precious metals trading system run out of London where real trade-level data that runs through AURUM is never publicly reported.

Between 2003 and the present day, the AURUM platform would obviously have gone through a number of changes, and it may not even be hosted on the LBT platform any longer. Given that lack of publicly available information on the design and functionality of AURUM, its hard to say. There is however a current ‘LPMCL Technical Committee‘ comprising IT and Business Analyst representatives of the member banks (see various Linkedin profiles for details), so perhaps AURUM was brought in-house between the bank members. Many of the in-house systems that AURUM interfaces to would also have changed over the years, requiring various upgrades of the AURUM platform too, and therefore a rationale for the existence of a ‘LPMCL Technical Committee’.

ICBC Standard’s Membership Application to LPMCL

When Reuters reported back in January of this year that ICBC Standard was looking to take on the vault lease for the Deutsche Bank / G4S vault, Reuters also reported in the same article that ICBC Standard had:

“also applied to become a clearing member of the London gold and silver over-the-counter business [LPMCL]"

“These banks are shareholders of the London Precious Metals Clearing (LPMCL) company. They will decide whether to accept or reject ICBC Standard Bank’s application within the next few months."

“They [ICBC] are applying for clearing membership at the moment, but that’s still subject to a vote, which has not taken place yet"

Therefore, LPMCL’s announcement that it had allowed ICBC Standard to join wasn’t really a surprise. But the application and voting procedure referred to by Reuters gels with the new membership procedure laid out in the Articles of Association of LPMCL, which states that membership of LPMCL is open to “other eligible persons as the directors in their discretion may admit to membership“. (person here means company entities that wish to become members).

In the LPMCL company each ‘member’ (bank) appoints a director. Each director can also appoint an alternate director. During the ICBC membership application, there were 9 directors listed as current directors of LPMCL, comprising 5 directors from each of the 5 members banks of JP Morgan, HSBC, ScotiaMocatta, UBS and Barclays, and 4 alternate directors from all the member banks except Barclays. A list of the current directors names can be seen here.

According to the 2015 annual accounts of LPMCL, the 5 LPMCL directors are Tony Dean (HSBC), Jane Lloyd (Scotia), Andrew Lovell (JP Morgan), Marco Heil (UBS), and Vikas Chamaria (Barclays). The 4 alternate directors are Peter Smith (JP Morgan), William Wolfe (HSBC), Conway Rudd (Scotia) and Daniel Picard (UBS).

Former Deutsche bank LPMCL director , Raj Kumar, has now moved to ICBC Standard Bank and should be in the front running to be appointed a LPMCL director representing ICBC Standard. If Standard Chartered also joins LPMCL, then former Barclays LPMCL director, Martyn Whithead, who moved to Standard Chartered, may also be expected to re-appear as a LPMCL director representing Standard Chartered.

LPMCL’s latest annual Accounts

The most recent set of annual accounts filed by LPMCL at UK Companies House are the accounts for the full year to 31 March 2015. These accounts were, audited by Kingston Smith LLP, signed off on 8 September 2015, and filed with Companies Office on 8 October 2015. The most interesting items in the accounts are as follows:

– 2015 Turnover (Revenue) totalled £223, 599 and is entirely derived from subscription income. This revenue is accounted for on an accruals basis, meaning that it refers to subscription income for the year to 31 March 2014. With 6 bank members of LPMCL for the period under consideration, thats £38,933 per member, which is very small change for investment banks.

– For the year to March 2015, LPMCL actually made an operating loss of £64,944 because Administrative Expenses were £288,543. The bottom line loss was a similar figure.

– The biggest components of Administrative Expenses were Computer Service Fees: £151,978, and Legal and Professional Fees: £118,384, which together totalled £270,362.

Computer Service Fees obviously refers to costs in running AURUM, running the LPMCL web site, and possibly other technology costs that can be billable by the member banks to LPMCL such as, for example, electronic communications and interfacing software for sending trades to and receive data from AURUM. ‘Fees’ suggests a payment to an external provider.

The ‘Legal and Professional Fees’ line item is more unusual. Why would LPMCL need to spend £118,384 on legal and profession fees in one year, which is 41% of total admin expenses, and 78% as large as the ‘computer service fees’? This legal and professional fees line item is also eye-opening since it increased from £69,194 in 2014 to £118,384, a 71% increase. Auditing fees would be fairly constant from year to year, so there is a relatively new and quite large expense under this category. Could it be a legal expense, and if so why?

What does LPMCL’s AURUM actually do?

The London bullion market’s clearing system is a monopoly bullion clearing system run by LPMCL for bullion settled loco London, with “all bullion transactions between the clearing members of the LBMA settled and cleared by The London Precious Metals Clearing Limited." “Loco London" traditionally meant gold and silver bullion physically held in London. With the rise of the unallocated account transfer system, to what extent unallocated bullion accounts are backed by physical bullion is debatable. The system is now a fractional-reserve credit system. LPMCL’s electronic clearing platform, AURUM, clears all bullion trades via book-entry netting and clearing using unallocated accounts.

Entities trading in the London bullion market maintain a series of unallocated accounts with one or more of the LPMCL clearers. The LMPCL members maintain unallocated accounts between each other used for clearing. The LPMCL also maintain bullion clearing accounts at the Bank of England. Each day, each client of each bullion clearer sends its LPMCL member clearing bank details of bullion trades between that client and its counter-parties. At the end of each trading day, each LPMCL member then processes position settlements by first netting out, in-house, to whatever extent possible, the bullion trades done by its own clients and clients of those clients.

Following this, the LPMCL members send their netted trade data to AURUM which then clears the clearers’ positions. The majority of LPMCL trades cleared are processed by LPMCL members HSBC and JP Morgan. The clearers also ‘settle’ their own positions with each other between 4pm and 4:30pm each day via broker transfers usually involving 3 brokers. This is done to prevent excessive overnight credit exposure between the clearers. The clearing process also involves “close liaison with the Bank of England and the many overseas bullion depositories“.

According to the LBMA, the LPMCL members:

“utilise the unallocated gold and silver, in accounts they maintain between each other, to make ‘paper transfers’ to settle mutual trades. They also settle third-party loco London bullion transfers, conducted on behalf of clients and other members of the London Bullion Market. This system of ‘paper transfers’ avoids the security risks, costs and impracticality of physically moving metal bars"

An overview of the London clearing process can be read on BullionStar’s Gold University profile of the London gold market here. The LBMA web site also provides a summary here. A similar summary is also in an article titled “Gold and Silver Clearing “Loco London” Through the Central Hub Developed by London Precious Metal Clearing Ltd" in Issue 55 of the Alchemist , dated July 2009. The most visible part of LPMCL and AURUM is the generally useless high level monthly clearing statistics that the LPMCL has produced each month since early 1997, and that are published on the LBMA website. These clearing statistics report the “net volume of loco London gold and silver transfers settled between clearing members of the LBMA."

For each of gold and silver, the statistics are calculated as daily averages and reported each month as three sets of figures, namely, a figure of millions of ounces transferred per day, the USD value of those ounces transferred per day, and also the number of transfers per day. Note that these clearing figures are just a fraction of what the real underlying trading figures are. Overall trading figures of the London gold market are anywhere up to 10 times or more larger than the clearing figures would suggest, since the clearing figures are ‘netted’ trading figures.

London-settled gold and silver clearing statistics were first published in January 1997, with the first clearing data reported for the Q4 period 1996. This was prior to the automation of the daily clearing operations through AURUM.

Even back then in 1997, the daily clearing figures for gold and silver through London were baffling and opaque since the daily clearing volumes were huge compared to the quantities of physical gold and silver that exists in the entire world, and there was no granular explanation or categorisation as to the trade types and client types that these clearing figures represented. In this regards, nothing has changed. Then as of now, the LPMCL only reveal that the monthly figures include 3 types of data:

– Loco London book transfers from one party in a clearing member’s books to another member in the same member’s books or in the books of another clearing member.

– Physical transfers and shipments by clearing members

– Transfers over clearing members accounts at the Bank of England

For example, the LBMA clearing statistics for April 2016 state that 16.5 million ounces (513 tonnes) of gold were cleared each day during the month. With 21 trading days in April 2016, that would be 346 million ounces (10,777 tonnes) of gold cleared during April. Since there is said to be a 10 :1 ratio between the amount of gold traded in London and the amount of gold cleared through AURUM, these clearing figures can be rolled up by a multiple of 10.

The trouble with this type of high level reporting is that it doesn’t even reveal the percentage of transfers in each of the above three groups, but physical transfers would be very very small percentage of the total, because, by definition, physical transfers couldn’t be any larger given that there is only a fraction of physical gold being transacted in the world on any given day relative to these gigantic clearing & trading figures.

An article called “Clearing Volume on the London Bullion Market" in Issue 6 of the Alchemist, by Peter Smith of JP Morgan, dated January 1997, first introduced these predominantly useless clearing statistics and revealed the 3 categories above. Nothing has changed in the reporting since 1997 and this LBMA lack of transparency remains right up to today. Ironically, Issue 6 of the LBMA’s Alchemist was titled ‘Towards Transparency‘ but there was little transparency divulged at that time, and the same opacity of the London bullion market still remains 20 years later.

Issue 6 of the Alchemist also had an introductory editorial from the then chairman of the LBMA, Alan Baker, whose opening line in the editorial was:

“The bullion market in London is often criticised by observers for being secretive and lacking in information and data. Unfortunately to an extent this is inevitable given the need for a duty of care to clients which dictates that a high level of discretion is an essential element in so much of the business that takes place in the market, particularly for gold."

Notice the secrecy is inevitable spin. The LBMA has been making excuses for the lack of transparency for at least 20 years now. Frankly, I don’t agree with any of the above explanations on the need for opacity. It’s a fiction. Reporting of trade volumes in all other markets globally such as equities, bonds, FX, money market and exchange-based commodities, is detailed, publicly available, and usually granular by transaction types and client types, and this does not, and has never, compromised client confidentiality in any of these asset classes. Why then do the precious metals markets, and the gold market in particular need to be the exception? They do not.

The excuses by people such as the ex LBMA chairman are merely helping to protect an entrenched system of opacity in which central banks, sovereign institutions, monetary authorities, the Bank for International Settlements, large bullion banks, and other large operators can move within the gold market without being concerned that any of their transactions and interventions will ever be noticed and reflected in gold price discovery. This is not an efficient market. Far from it. This is a protected and hidden physical trading system upon which is overlaid a massive pyramid of fractional-reserve paper gold trading.

The trade types of the trades from which the massive MPMCL clearing figures are generated could easily be reported by LPMCL and the LBMA, but they choose not to report this information. All positional, transactional, account, account type, and physical allocation data in every database table in AURUM and in every bullion trade database table of each LPMCL member bank could be published publicly while stripping out clients’ account-sensitive data and would still not jeopardize client confidentiality.

Trade Types behind the LPMCL Clearing figures

LPMCL provided one glimpse into London bullion market trade types in October 2003, in an article in Alchemist 32, titled “Clearing the Air Discussing Trends and Influences on London Clearing Statistics“, when the then LMPCL chairman, Peter Fava, and JP Morgan’s Peter Smith, both involved in the compilation of the original clearing statistics in 1997, were interviewed about “some changes in the nature of the market and over the intervening years that might have had an impact on the reported numbers." This is the only insight that I am aware of that provided a small window into some of trade types of bullion transactions that are processed through AURUM.

Fava was asked about the “changes in the overall pattern of trading activity from certain counterparts". He then gave a rundown of various bullion trading activities that were showing up in the clearing data. The activities mentioned were:

- central bank gold deposits, rolling over monthly, and the hedging transactions connected to that borrowing

- interest rate swaps and longer-term collateralised agreements

- speculative trading activity on a leveraged, forward basis that is closed out before maturity

- investment fund participation via spot transactions* (generally netted by the counterparty banks against EFPs – exchange for physicals) but if not netted would show up in clearing

- interbank market trading (multiple times per day)

- consignment accounts in physical markets, notably Istanbul, Dubai and India" with purchases out of the consignment account hedged loco London

Since that 2003 article was written, there has been a huge growth in Exchange Traded Fund (ETF) trading, a trading activity that can be added to the above list. In 2014, in the LBMA Silver Price competition proposals, ETF Securities’ bid stated that “our physical precious metal ETCs are created and redeemed for physical metal, with the metal being cleared through the LBMA clearing system and the securities being cleared through the CREST clearing system which is used for LSE trading“.

I have analysed the above London bullion market trade types in more depth, but due to space constraints, I’ll cover this is a future posting, but for now, the point to note is that a lot of London bullion trading activity has very little to do with physical metal movements.

Recall also that Stewart Murray (ex LBMA CEO) had said in a 2011 presentation that investment funds had ‘very large’ unallocated positions in the market.

“Various investors hold very substantial amounts unallocated gold and silver in the London vaults"

I wonder if investment funds which presume they own unallocated gold or silver (which is just a long unallocated spot position put on by a bank), are aware that their positions are then offset against futures. Some unsophisticated funds might think they are actually hold pooled gold or silver holdings within a London bank vault.

Circling the Wagons: Protection of LPMCL’s clearing monopoly

In 2014, the daily fixing auctions for all 4 precious metals in the London market were moved to new electronic platforms. In the case of gold and silver, competitions were held (organised by the LBMA) to decide on which companies would become the new administrators and calculation agents for the auctions. Ultimately, Thomson Reuters / CME Group secured the contract to run the new Silver auctions (LBMA Silver Price), and ICE Benchmark Administration secured the contract to run the new Gold auctions (LBMA Gold Price). In the case of the platinum and palladium auctions, as to whether a competition was held is debatable, since neither LPPM nor the London Platinum and Palladium Fixing Company (LPPFC) would confirm this when asked. However, the London Metal Exchange was ultimately awarded the mandate to run the new platinum and palladium auctions (LBMA Platinum Price and LBMA Palladium Price).

After Thomson Reuters and CME Group had secured the contract for the silver auctions, CME Group maintained (in a public presentation) on 29 July 2014 that it would soon introduce a centrally cleared platform for these auctions trades so as to widen participation in the auctions and eliminate credit risk between participants.

“[for] Extended Participation, we envisage central clearing via CME Clearing Europe under the auspices of the UK and European regulated authorities which should effectively open the door for most participants.”

“We’re basically starting the process as soon as possible. Let’s get this up and running by 15thAugust [2014] and then it’s all hands to the pumps on the clearing side so hopefully it will happen soon.”

“The work we’ve got to do is to set this up so that’s it’s part of the platform so it’s a level playing field for participants…"

“Anindya Boral will be starting to do a big drive to enable cleared transactions through our clearing house and wider participation in August"

In its presentation, CME Group featured a slide which stated that:

“Central counterparty clearing will enable greater direct participation in the London Silver Price”.

We anticipate using CME Group’s London Clearing House – CME Clearing Europe – for the London Silver Price

By serving as the counterparty to every transaction, CME Clearing Europe will become the buyer to every seller and the seller to every buyer, virtually eliminating credit risk between market participants“

However, the CME’s promise of central clearing never happened and its plans to introduce central clearing were mysteriously dropped. See BullionStar blog “The LBMA Silver Price – Broken Promises on Wider Participation and Central Clearing" for full details.

Likewise, when the LME announced that it had been awarded the contract by LPPFC to run the platinum and palladium price auctions, the LME issued a press release on 16 October 2014 stating that it planned to introduce clearing of platinum and palladium auction trades using its clearing platform LME Clear, so as to maximise participation and overcome the credit risk obstacle:

“To maximise participation in the London pricing mechanism, the LME also plans to introduce a cleared platinum and palladium service, which will mitigate the difficulty associated with participants taking bilateral credit risk in positions.

LME Clear, launched on 22 September 2014, was built specifically to enable efficient clearing of metals exposures and will extend its existing precious metals clearing functionality to clear platinum and palladium.“

However, the LME mysteriously pulled its press release a few hours after it had been published, and replaced it with an amended version where the above two paragraphs had been deleted. See BullionStar blog “LPPM – The London Platinum and Palladium Market" for full details.

And so, LME Clear was never introduced for clearing platinum and palladium auction trades.

Similarly, in its Executive Summary proposal submitted to the LBMA in October 2014 to run the new gold price auctions, a contract which it ended up winning, ICE Benchmark Administration (IBA) stated that its solution could employ pre-collateralisation to eliminate bi-lateral credit risk between participants, and therefore widen auction participation. ICE also made reference to the logic of using a centrally cleared model, but was shrewd enough at that point in time to defer to the powerful interests of the clearing members who essentially run the LBMA, knowing that the CME Group and LME clearing solutions for Silver and Platinum/Palladium had been shot down:

“It is through the Oversight Committee that the LBMA will continue to have significant involvement in the auction process, including… the decision on whether to move to a centrally cleared model (until that time, weaker credit names can be accommodated via pre-collateralisation).”

“One of the key benefits of WebICE is its ability to allow clients to participate in the auction process with the same information and order management capabilities as the direct participants. This reduces both operational and regulatory risk for direct participants, even before increasing the number of direct participants or moving to a centrally cleared model.”

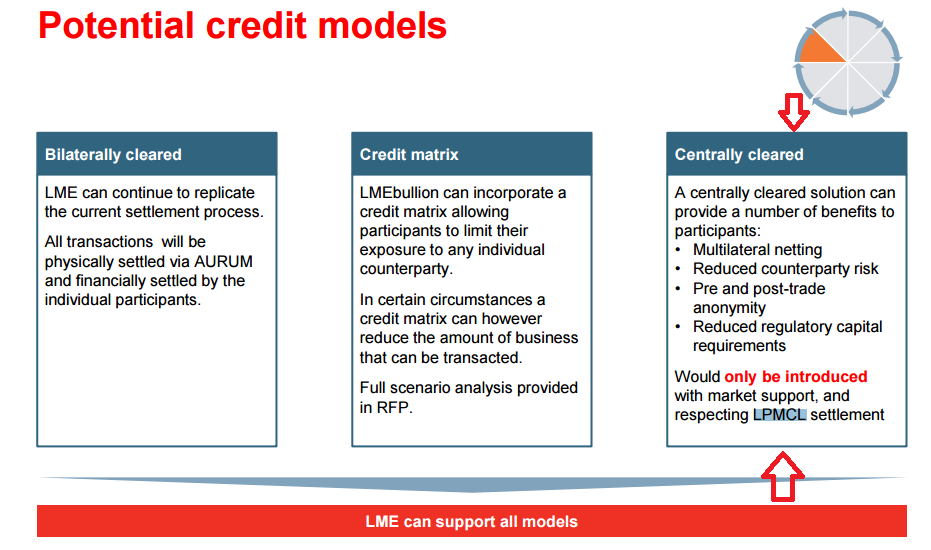

In its presentation submission to the LBMA in October 2014 during the competition to run the London gold auctions, the LME also seemed to have gotten the message that the LPMCL’s clearing monopoly and its AURUM clearing system were not to be tampered in any proposed LME platform. In a slide titled “Potential credit models" the LME said that a centrally cleared solution “would only be introduced with market support and respecting LPMCL settlement“. See right-hand box in below slide:

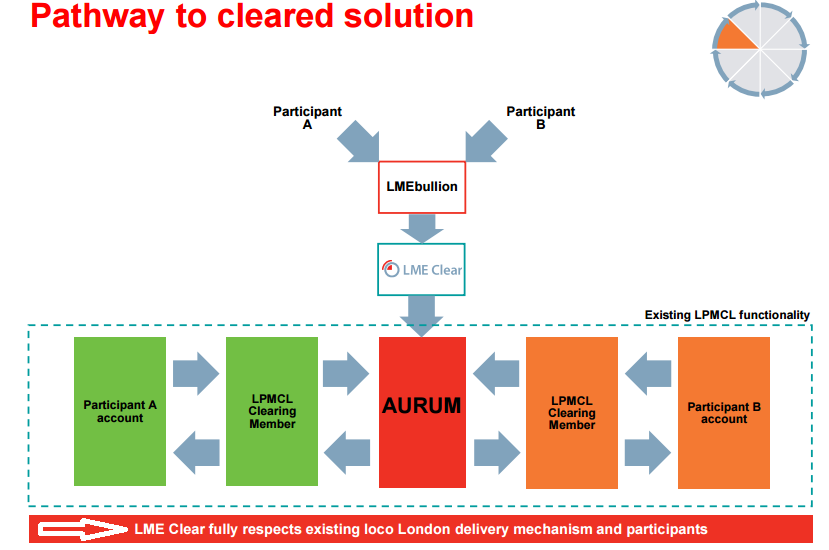

Likewise, in the slide that followed the above one, the LME again made it abundantly clear that it had got the message that LMPCL was not to be touched – “LME Clear fully respects existing loco London delivery mechanism and participants“:

The only reference by the LBMA to central clearing counterparties is a short comment on its website about centrally clearing OTC forward trades where it states:

“..members of a common ‘Central Counterparty’(CCP), that has a facility to clear forwards, may novate their trades and thus avoid bilateral credit risk. In the absence of an exchange, the trade remains one of an OTC nature but has the ability to be cleared. This method of credit mitigation is known as OTC Cleared."

CME Group already offers a very sparsely used (or not even used) centralised clearing service for OTC unallocated gold forwards using collateral or cash margin. “Delivery occurs at LPMCL member banks via book entry transfer of ‘London Good Delivery’ gold, which means unallocated loco London book entry gold claims on an LPMCL bank”.

Not surprisingly, the LBMA web site, says nothing about the pros and cons of centrally clearing OTC spot trades nor is there any discussion about exchange-based trading and clearing of any London bullion trades.

The LPMCL web site mentions an alternative clearing system (a clearing house), but not surprisingly, this approach is only mentioned as a foil for undermining it, as follows:

Q: Can you explain the benefits of the London bullion clearing system as compared with a clearing house?

A: “…a clearing house usually has a rigid settlement structure, does not provide credit, or assume intra-day or term credit risks, and not being in the banking business, has no ability to use any underlying liquidity. It will thus most likely be less flexible, less efficient and more expensive – particularly as clearing houses by their nature are non-competitive, whereas the London bullion clearing banks compete for clients by providing competitive services and pricing."

Q: Could a clearing house replace the London bullion clearing system?

“Yes, but it would prove to be less efficient and more expensive than the current arrangement. It would also most likely need strong financial backing and insurance cover – which then directs us back to the London bullion clearing banks, as above, all of whom are first tier global institutions."

Why is LPMCL being Protected?

In conclusion, why does the LBMA think that LPMCL is a ‘vital organisation’? as the LBMA CEO phrases it.

- Firstly, LPMCL keeps the entire pyramid of London’s unallocated precious metals trades spinning. By not reporting any trade information, the LBMA and LPMCL keep the entire gold world in the dark about the extent of the London paper gold trading scheme

- Secondly, LPMCL preserves opacity and prevents public reporting of precious metals trades, including central bank gold lending and gold swaps, and therefore keeps this major gold market trading activity out of focus, with the spotlight off the role of the Bank of England in the London Gold Market.

- Thirdly, the most powerful banks in the LBMA are the LPMCL members which are also the vaulters in London and the member banks of the LBMA Management Committee. These banks want to maintain the monopoly status quo of LPMCL and to maintain the status quo of the London precious metals vaulting system and their vaulting fees. The same banks run the trading, clearing and vaulting of the entire London bullion system. Perhaps the FCA should be looking at anti-competitive behaviour here, for example vaulting fees, and clearing fees.

- Fourthly, the current LPMCL system masks huge amounts of trading for the LBMA members banks and brokers. Huge trading makes large trading commissions. The same system generates the need for the banks to provide credit to bullion market participants, which generates interest income.

- Fifthly, by propping up LPMCL, its member banks can push back on any competing initiatives that are proposing a ‘gold exchange’ in London, such as the exchange initiative that’s backed by the World Gold Council and a number of other (non LPMCL) bullion banks.

As the Financial Times said in October 2015 when reporting about the LBMA’s so-called moves to provide trade reporting in light of other initiatives by the LME / World Gold Council and banks such as Goldman, SocGen, Citibank and Morgan Stanley (and previously including ICBC Standard) to move gold trading on to an exchange platform using exchange defined gold contracts:

“In the other camp is the LBMA, the official body set up by the Bank of England in 1987 to regulate the bullion market, which has close ties to the vaulting banks. Many of its biggest members want physical gold trading in London to remain off-exchange, but have conceded that a move towards all trades being cleared in one place could add transparency."

Look at what the incumbent LBMA banks do, not what they say to newspapers. What the LBMA – LPMCL co-op (same people, different hats) has just done is welcomed another bank (ICBC Standard) into ‘this vital organisation" (the LPMCL), and the LBMA is now looking forward to “continuing to assist LPMCL in its growth and development."

ICBC Standard had been in the LME / World Gold Council / Goldman / SocGen/ Citi / Morgan Stanley camp, buton the face of it, ICBC now appears to have deserted that faction and fully aligned with the LPMCL cartel of HSBC / JP Morgan / Scotia / UBS and Barclays. ICBC Standard may have been using the LME / Goldman camp as a bargaining tool with which to exert access pressure to join the LPMCL gang, and now that it has done so, it would be surprising if ICBC continues to align itself with the LME’s upcoming gold exchange proposal. However, as a Chinese controlled bank with long-term planning horizons, ICBC may wish to play a strategic game with a seat at both tables.

Popular Blog Posts by Ronan Manly

How Many Silver Bars Are in the LBMA's London Vaults?

How Many Silver Bars Are in the LBMA's London Vaults?

ECB Gold Stored in 5 Locations, Won't Disclose Gold Bar List

ECB Gold Stored in 5 Locations, Won't Disclose Gold Bar List

German Government Escalates War On Gold

German Government Escalates War On Gold

Polish Central Bank Airlifts 8,000 Gold Bars From London

Polish Central Bank Airlifts 8,000 Gold Bars From London

Quantum Leap as ABN AMRO Questions Gold Price Discovery

Quantum Leap as ABN AMRO Questions Gold Price Discovery

How Militaries Use Gold Coins as Emergency Money

How Militaries Use Gold Coins as Emergency Money

Hungary Announces 10-Fold Jump in Gold Reserves

Hungary Announces 10-Fold Jump in Gold Reserves

Planned in Advance by Central Banks: a 2020 System Reset

Planned in Advance by Central Banks: a 2020 System Reset

China’s Golden Gateway: How the SGE’s Hong Kong Vault will shake up global gold markets

China’s Golden Gateway: How the SGE’s Hong Kong Vault will shake up global gold markets