LBMA Gold Vault Data: How Low is the London Gold Float?

Ronan Manly

Ronan Manly 0 Comments

0 CommentsThe London Bullion Market Association (LBMA) has just released a first update on the quantity of physical gold and silver holdings stored in the ‘LBMA’ London vaulting network. The LBMA press release explaining the move, dated 31 July, can be read here.

This vaulting network, administered by the LBMA, comprises a set of precious metals vaults situated in London that are operated by the Bank of England and 7 commercial vault operators. For simplicity, this set of vaults can be called the LBMA London vaults. The 7 commercial vault operators are HSBC, Brinks, ICBC Standard Bank, Malca Amit, JP Morgan, Loomis and G4S. ICBC Standard outsources its vault management to Brinks. It’s possible that to some extent HSBC also outsources some of its vault management to Brinks.

Strangely, the LBMA’s initial reporting strangely only runs up to 31 March 2017, which is 4-months prior to the first publication date of 31 July. This is despite the fact that new LBMA vault holdings data is supposed to be published on a 3-month lagged basis, which would imply a latest report coverage date of 30 April.

At the end of April 2017, the Bank of England separately began publication of gold vault holdings for the gold bars that the Bank stores in custody within its own vaults. The Bank of England reporting is also on a 3-month lagged basis (and the Bank actually adheres to this reporting lag). See BullionStar article “Bank of England releases new data on its gold vault holdings”, dated 28 April 2017, for details of the Bank of England vault reporting initiative.

Currently, the Bank of England is therefore 1 month ahead of the LBMA vault data, i.e. on 31 July 2017, the Bank of England’s gold page was updated with Bank of England gold custody vault holdings as of 30 April 2017.

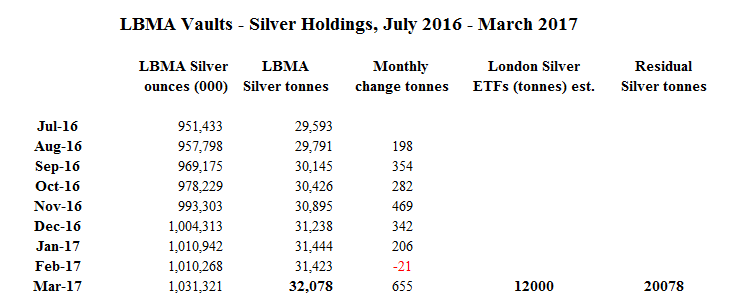

Ignoring the LBMA 3-month lagged vs 4-month lagged anomaly, the LBMA’s first vault reporting update, for vault data as of 31 March 2017, states that the 8 sets of vaults in question (which includes the Bank of England gold vaults) held a combined 7449 tonnes of gold and a combined 32078 tonnes of silver.

Also included in the first batch of LBMA data are comparable London vault holdings figures for gold and silver for each month-end date from July 2016 to February 2016 inclusive. Therefore, as of the 31 July 2017, there is now an LBMA dataset of 9 months of data, which will be augmented by one month each month going forward. Whether the LBMA will play catch-up and publish April 2017 month-end and May 2017 month-end figures simultaneously at the next reporting date of 31 August 2017 remains to be seen.

The New Vault Data – Gold and Silver

For 31 March 2017, the LBMA is reporting 7449 tonnes of gold stored across the 8 sets of vault locations. For the same date, the Bank of England reported 5081 tonnes of gold held in the Bank of England vaults. Therefore, as of 31 March 2017, there were 2368 tonnes of gold ‘not in the Bank of England vaults’ (or at least 2368 tonnes of gold not counted by the Bank of England data).

Of the gold not in the Bank of England vaults, about 1510 tonnes of this gold in London was held by gold-backed Exchange Traded Funds (ETFs), mainly with the custodians HSBC and JP Morgan. These ETFs include the SPDR Gold Trust and various ETFs from ETF Securities, Source, iShares, and Deutsche Bank etc. This 1510 tonnes figure is taken from an estimate calculated at the end of April 2017 using data from the GoldChartsRUs website. See BullionStar article “Summer of 17: LBMA Confirms Upcoming Publication of London Gold Vault Holdings” dated 9 May 2017 for details of this ETF calculation.

Subtracting this 1510 tonnes of ETF gold from the 2368 tonnes of gold stored outside the Bank of England vaults means that as of 31 March 2017, there were only about 858 tonnes of gold stored in the LBMA vaults outside of the Bank of England vaults that was not held by gold-backed ETF holdings. See Table 1 below.

The lowest gold holdings number reported by the LBMA within its 9 months of vault data is actually the first month, i.e. July 2016. At month-end July 2016, the LBMA report shows total vaulted gold of 7283 tonnes. There was therefore a net addition of 166 tonnes of gold to the LBMA vaults between August 2016 and the end of March 2017, with net additions over the August to October 2016 period, followed by net declines over the November 2016 to February 2017 period.

Turning to silver, as of 31 March 2017, the LBMA is reporting total vaulted silver of 32,078 tonnes held in London vaults. The vaulted silver data also shows a notable increase over the period from the end of July 2016 to the end of March 2017, with a net 2485 tonnes of silver added to the vaults.

Since the Bank of England vaults only store gold in custody on behalf of customers and do not store silver, there are no silver holdings at the Bank of England and therefore there is no specific Bank of England silver reporting. The LBMA silver data therefore refers purely to silver vaulted with operators such as Brinks, JP Morgan, Malca Amit, HSBC, and Loomis.

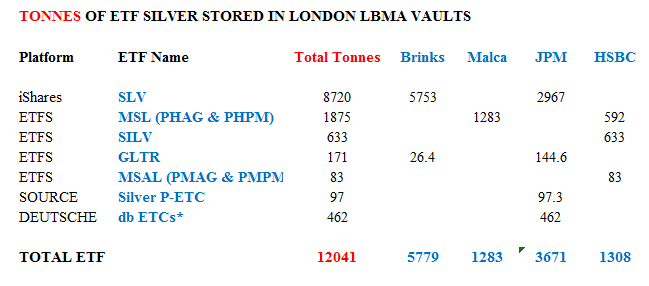

There are currently at least 12,000 tonnes of silver stored in London on behalf of silver-backed ETFs such as the iShares Silver Trust (SLV), various ETF Securities products, a SOURCE ETF and some Deutsche Bank ETFs. Subtracting these ETF holdings from the full 32,078 tonne figure being reported by the LBMA would suggest that there are an additional ~ 20,000 tonnes of non-ETF silver held in the London vaults.

Previous Vault Estimates for Gold and Silver

Prior to the new LBMA and Bank of England vault holdings data reports, the only way to work out how much gold and silver were in the London vaulting network was through estimation. Between 2015 and 2017, a number of these estimates were calculated for gold and published on the BullionStar website and the GoldChartsRUs website.

See BullionStar page “How many Good Delivery gold bars are in all the London Vaults?….including the Bank of England vaults" and GoldChartsRUs page “LBMA/BOE VAULTED GOLD, 2016 Update – The London Float”, and BullionStar page “Tracking the gold held in London: An update on ETF and BoE holdings”.

The “Tracking the gold held in London" article, published on 5 October 2016, took a LBMA statement of 6500 tonnes of gold being in London, the earliest reference to which was from 8 February 2016 Internet Archive page cache, and also took a Bank of England statement that the Bank held 4725 tonnes as of the end of February 2016 period, and then it factored in that the UK net imported more than 800 tonnes of non-monetary gold up to August 2016, and also that ETFs had added about 399 tonnes over the same period. It also calculated, using GoldChartsRUS ETF data, that the London-based gold-backed ETFs held about 1679 tonnes of gold as of the end of September 2016.

Therefore, as of the end of September 2016, there could have been at least 7300 tonnes of gold held across the LBMA and Bank of England vaults, i.e. 6500 tonnes + 800 tonnes = 7300 tonnes. As it turns out, this estimate was quite close to the actual quantity of gold held in the LBMA and Bank of England vaults at the end of September 2016, which the LBMA’s new reporting now confirms to have been 7590 tonnes. The estimate is a lower number because it was unclear as to which initial date the LBMA’s 6500 tonnes reference referred to (in early 2016 or before).

Previous Vault Estimates Silver

At the beginning of July 2017, an article on the BullionStar website titled “How many Silver Bars are in the LBMA Vaults in London?" estimated that there were about 12,000 tonnes of Good Delivery silver bars held across 4 LBMA vault operators in London on behalf of 11 silver-backed Exchange Traded Funds. These ETFs and the distribution of their silver bars across the 4 vault operators of Brinks, Malca Amit, JP Morgan and HSBC can be seen in the following table.

The above article about the number of silver bars in the London vaults also drew on some data from precious metals consultancy Thomson Reuters GFMS, which each year publishes a table of identifiable above ground global silver supply in its World Silver Survey. One category of silver within the GFMS identifiable above ground silver inventories is called ‘Custodian Vaults’. This is distinct from silver holdings in ETFs and silver holdings in exchange inventories such as in COMEX approved vaults in New York. A simple way to view ‘Custodian Vaults’ silver holdings is as an opaque ‘unreported holdings’ category as opposed to the more the transparent ETF holdings and COMEX holdings categories.

For 2016, according to GFMS, this ‘Custodian Vaults’ silver amounted to 1571.2 million ounces (48,871 tonnes), of which 488.7 million ounces (15,200 tonnes), or 31% was represented by what GFMS calls the ‘Europe’ region. Unfortunately, GFMS do not break out the ‘Custodian Vaults’ numbers by individual country because they say that they receive the data on a confidential basis and cannot divulge the granularity. The early July article on BullionStar had speculated that:

“With 488.7 million ozs (15,201 tonnes) of silver held in Europe in ‘Custodian vaults’ that is not reported anywhere, at least some of this silver must be held in London, which is one of the world’s largest financial centers and the world’s highest trading volume silver market."

“Apart from London, there would presumably also be significant physical silver holdings vaulted in Switzerland and to a lessor extent in countries such as Germany, the Netherlands and maybe Austria etc. So whats’s a suitable percentage for London? Given London’s extensive vaulting network and prominence as a hedge fund and institutional investment centre, a 40-50% share of the European ‘custodian vault’ silver holdings would not be unrealistic, with the other big percentage probably vaulted in Switzerland.

This would therefore put previously ‘Unreported’ silver holdings in the London vaults at between 6080 tonnes and 7600 tonnes (or an additional 182,000 to 230,000 Good Delivery Silver bars).

Adding this range of 6080 – 7600 tonnes to the 12,040 tonne figure that the 11 ETFs above hold, gives a total figure of 18,120 – 19,640 tonnes of silver stored in the LBMA vaults in London (545,000 – 585,000 Good Delivery silver bars).

But here’s the catch. With the LBMA now saying that as of the end of March 2017 there were 1.031 billion ounces of silver, or 32078 tonnes, stored in the LBMA vaulting network in London (and 31238 tonnes of silver in London as of end of December 2016), of which at least 12,000 tonnes is in silver-backed ETFs, then that still leaves about 20,000 tonnes of silver in the London vaults, which is higher than the silver total attributed to the entire ‘custodian vault’ category’ in Europe (as per the GFMS 2016 report).

Even the lowest quantity in the 9 months that the LBMA reports on, which is month-end July 2016, states that the LBMA vaults held 951,433,000 ounces (29,593 tonnes), which after excluding silver ETFs in London, is still higher than the total ‘Custodian Vault’ category that GFMS attributes to the European region in 2016.

These new LBMA vault figures are basically implying that all of the GFMS custodian vault figure for Europe (and some more) is all held in London and not anywhere else in Europe. But that could not be the case as there is also a lot of silver vaulted in Switzerland and other European countries such as Germany, to think of but a few.

This begs the question, does the GFMS Custodian vault number for Europe need to be updated to reflect the gap between the non-ETF holdings that LBMA claims are in the London vaults and what GFMS is reporting in a European ‘Custodian vaults’ category? If the LBMA reporting actually broke down the silver vaulting quantity number into Good Delivery silver bars and other categories, it might help solve this puzzle as it would give an indication of how much of this 32,000 tonnes of silver is in the form of bars that are accepted for settlement in the London Silver Market i.e. Good Delivery silver bars.

Could some of this 32,000 tonnes of silver be in the form of silver jewellery, and private holdings of silver antiques and even silver artifacts? On the surface the LBMA reporting appears to say not since it states that:

“jewellery and other private holdings held by retailers, individuals and smaller vaults not included in the London Clearing system are not included in the numbers"

But because this statement reads rather ambiguously, by implication another interpretation of the LBMA statement could be that:

“jewellery and other private holdings held by retailers and individuals in vaults that are part of the London Clearing system are included in the numbers"

The London Clearing system here refers to the vaults of the 7 commercial vault operators.

Until GFMS comes back with a possible clarification of its ‘Custodian Vault’ figure for Europe, then this contradiction between the LBMA data for silver and GFMS data for silver will persist.

Large Bars but also Small Bars and Gold Coins

According to the LBMA’s press release, while “the LBMA vault holding data …represent the volume of Loco London gold and silver held in the London vaults offering custodian services“, surprisingly the new LBMA data includes “all physical forms of metal inclusive of large wholesale bars, coin, kilo bars and small bars.”

The inclusion of gold coins, smaller gold bars and gold kilobars in the LBMA vault data is bizarre because only large wholesale bars are accepted as Good Delivery in the London gold and silver markets, not gold coin, not smaller bars, and not gold kilobars. Even the LBMA website states that “the term Loco London refers to gold and silver bullion that is physically held in London. Only LBMA Good Delivery bars are acceptable for trading in the London market.”

Furthermore, the entire physical London Gold Market and physical London Silver Market revolve around the LBMA Good Delivery lists. Spot, forward and options trades on the London OTC gold and silver market are only referenced to a unit of delivery of a Good Delivery bar, both for gold and for silver.

For example, in the LBMA’s “A Guide to the London Precious Metals Markets” it states that:

“Unit for Delivery of Loco London Gold

This is the London Good Delivery gold bar. It must have a minimum fineness of 995.0 and a gold content of between 350 and 430 fine ounces…. . Bars are generally close to 400 ounces or 12.5 kilograms”

For silver, the same guide states that:

“Unit for Delivery of Loco London Silver

This is the London Good Delivery silver bar. It must have a minimum fineness of 999 and a weight range between 750 and 1,100 ounces, although it is recommended that ideally bars should be produced within the range of 900 to 1,050 ounces. Bars generally weigh around 1,000 ounces.”

Additionally, all the new London-based gold futures contracts launched by the LME, ICE and CME also reference, if only virtually, the unit for Delivery of loco London gold, i.e. the London Good Delivery gold bar. They do not reference smaller gold bars or gold coins.

In contrast to the LBMA , the COMEX exchange where the famous COMEX 100 ounce gold futures contract is traded only reports vault inventories of gold and silver where the bars satisfy that contract for delivery, i.e. the contract for delivery is one hundred (100) troy ounces of minimum fineness 995 gold of an approved brand in the form of either “one 100 troy ounce bar, or three 1 kilo bars”. COMEX do not report 400 oz gold bars or gold coins specifically because the contract has nothing to do with these products. Then why is the LBMA reporting on forms of gold that have nothing to do with the settlement norms of its OTC products in London?

Additionally, the LBMA website also states that “only bars produced by refiners on the [Good Delivery] Lists can be traded in the London market.“ All of this begs the question, why does the LBMA bother including smaller bars, kilogram bars and gold coins? These bars cannot be used in settlement or delivery for any standard London Gold Market transactions.

Perhaps these smaller gold bars and gold coins have been included in the statistics so as to boost the total reported figures or to make reverse engineering of the numbers more difficult? While the combined volumes of smaller bars and kilobars probably don’t add up to much in terms of tonnage, the combined gold coin holdings of central banks stored at the Bank of England could be material.

For example, the United Kingdom, through HM Treasury’s Exchange Equalisation Account (EEA), claims to hold 310.3 tonnes of gold in its reserves, all of which is held in custody at the Bank of England. The latest EEA accounts for 2016/2017, published 18 July 2017 state that “The gold bars and gold coin in the reserves were stored physically at the Bank’s premises.” See Page 43, Exchange Equalisation Accounts for details. Many more central banks, for historical reasons, also hold gold coins in their reserves. See Bullionstar article “Central Banks and Governments and their gold coin holdings” for some examples.

As another example, the Banque de France in Paris holds 2435 tonnes of gold of which 100 tonnes is in the form of gold coins, and 2,335 tonnes of gold bars. Even though these gold coins are held in Paris, this shows that central bank gold coin holdings could materially affect LBMA gold reporting that includes ‘gold coins‘ within the rolled up number. But such gold coins cannot be traded within the LBMA / LPMCL gold trading / gold clearing system and if present would overstate the number of Good delivery gold bars within the system.

The Bank of England gold page on its website also only refers to Good Delivery ‘gold bars’ and says nothing about gold coins, which underlines the special status to which the Bank of England assigns Good Delivery gold bars in the London Gold Market. Specifically, the BoE gold page states that:

“..we provide gold storage on an allocated basis, meaning that the customer retains the title to specific gold bars in our vaults”

“Values are given in thousands of fine troy ounces. Fine troy ounces denote only the pure gold content of a bar.

“We only accept bars which comply with London Bullion Market Association (LBMA) London Good Delivery (LGD) standards. LGD bars must meet a certain minimum fineness and weight. A typical gold bar weighs around 400 oz“

The Bank of England has now confirmed to me, however, that the gold holdings number that it reports on its website “is the total of all gold held at the Bank" and that this “includes coins that belong to the Exchange Equalisation Account (EEA) which are held by the Bank on behalf of Her Majesty’s Treasury (HMT)"

This means that the total gold number being reported by both the Bank of England and the LBMA needs to be adjusted downward by some percentage so as to reflect the amount of real Good Delivery gold bars in the London vaults. What this downward adjustment should be is unclear, as neither the Bank of England nor the LBMA break out their figures by category of gold bars versus gold coins.

LBMA numbers – Obscured Rolled-up numbers

Another shortcoming in the LBMA’s vault reporting is that it does not break down the gold and silver holdings per individual vault. The LBMA will be only releasing 2 highly rolled-up numbers per month, one for gold and one for silver, for example, 7449 tones for gold and 32078 tonnes for silver in the latest month.

Contrast this to New York based COMEX and ICE gold futures daily reporting, which both do break down the gold holdings per New York vault. Realistically, the LBMA was never going to report gold or silver holdings per vault, as this would be a bridge too far towards real transparency, and would show how much or how little gold and silver is stored by each London vault operator / at each London vault location.

This does not, however, stop the LBMA from claiming transparency and in its 31 July press release it states that:

“According to the Fair and Effective Markets Review (see here for further details)

‘…in markets where OTC trading remains the preferred model, authorities and market participants should continue to explore the scope for improving transparency, in ways that also enhance effectiveness.’“

Real transparency, as opposed to lip-service transparency, would be supported by providing an individual breakdown of the number of Good Delivery gold and silver bars stored in each of the 8 sets of vaults at each month end. If they want to include gold coins, smaller gold bars, and gold kilo bars as extra categories, then this could also be itemised on a proper report. It would also only take any decent software developer about 1 day to write and create such a report.

There is also the issue of independently auditing these LBMA numbers. The issue is essentially that there is no independent auditing of these LBMA numbers nor will there be. So there is no second opinion as to whether the data is accurate or not.

The Bank of England gold vault reporting is also short of transparency as it does not provide a breakdown of how much of the reported gold is held by central banks, how much gold is held by bullion banks, how much of the central bank gold is out on loan with the bullion banks, and how much gold, if any, is held on behalf of ETFs at the Bank of England as sub-custodian. Real transparency in this area would provide all of this information including how much gold the LPMCL bullion clearing banks HSBC, JP Morgan, UBS, Scotia Mocatta and ICBC Standard hold at the Bank of England vaults.

On the issue of ETF gold held at the Bank of England, it has been proven that at times the Bank of England has acted as a gold custodian for an ETF, for example, during the first quarter 2016, the SPDR Gold Trust held up to 29 tonnes of gold at the Bank of England, with the Bank of England acting in the capacity of sub-custodian to the SPDR Gold Trust. See BullionStar article “SPDR Gold Trust gold bars at the Bank of England vaults" for details.

The London Float

The most important question with this new LBMA vault reporting is how much of the 7449 tonnes of gold stored in London as of the end of March 2017 is owned or controlled by bullion banks.

Or more specifically, what is the total level of LBMA bullion bank unallocated gold liabilities in the London market compared to the amount of real physical gold bars that they own or control.

This ‘gold owned or controlled by the bullion banks’ metric can be referred to as the ‘London Float’. LBMA bullion banks can maintain their own holdings of gold bars which they buy in the market or import directly, and they can also borrow other people’s gold thereby controlling this gold also. Some of this gold can be in the LBMA commercial vaults. Some can also be in the Bank of England vaults.

In its press release, the LBMA states that:

“The physical holdings of precious metals held in the London vaults underpin the gross daily trading and net clearing in London."

This is not exactly true. Only gold which is owned or controlled by the bullion banks can underpin gold trading in London. Allocated gold sitting in a vault that is owned by central banks, ETFs or investors and which does not have any other claim attached to it, does not underpin anything. It just sits there in a vault.

As regards gold bars stored in the LBMA vaults in London, these bars can either be owned by central banks at the Bank of England, owned by central banks at commercial vaults in London, owned by ETFs at the commercial vaults in London, owned or controlled by bullion banks, and owned by investors (either institutional investors, hedge funds, private individuals etc). On occasion, some ETF gold has at various times been at the Bank of England.

If central bank gold is held in allocated form and not lent out, then it is ‘off the market’ and can’t be ‘used’ by any other party such as a LBMA bullion bank. If central bank gold is lent out or swapped out to bullion banks, then it can be used or even sold by those bullion banks. The LBMA uses the euphemism ‘liquidity’ to refer to this gold lending. For example, from the LBMA’s recent press release on the new vault reporting it says:

“In addition, the Bank of England also offers gold custodial services to central banks and certain commercial firms, that facilitate central bank access to the liquidity of the London gold market."

ETF gold when it is held within an ETF cannot legally be used by other entities since it is owned by the ETF and allocated to the ETF. Institutionally owned gold or private owned gold when it is allocated is owned by the holder. It could in theory be lent to bullion banks also.

Some of the LBMA bullion banks have gold accounts at the Bank of England. How many of these banks maintain gold holdings within the Bank of England vaults nobody will say, not the Bank of England nor the LBMA nor the bullion banks, but it at least extends to the 5 members of London Precious Metals Clearing Limited (LPMCL) which are HSBC, JP Morgan, Scotia Mocatta, ICBC Standard and UBS. Gold accounts for bullion banks undoubtedly also extend to additional bullion banks beyond the LPMCL members because many bullion banks have been involved in gold lending at the Bank of England for a long time, for example Standard Chartered, Barclays, Natixis, BNP Paribas, Deutsche Bank, and Goldman Sachs, and these banks would at some point have to take delivery of borrowed gold at the Bank of England.

Note, the gold brokers of the London Gold Market have for a long time, as least since the 1970s, been able to store some of their gold bars at the Bank of England vaults. These brokers were historically Samuel Montagu, Mocatta, the old Sharps Pixley, NM Rothschild and Johnson Matthey.

Since LBMA bullion banks can maintain gold accounts at the LBMA commercial vaults in London, and because some of these banks have gold accounts at the Bank of England also, then this London “gold float" can comprise gold bars at the commercial vaults and gold bars at the Bank of England vaults. It is however, quite difficult to say exactly what size this London bullion bank gold float is at any given time.

Whatever the actual number, its not very big in size because if you subtract central bank gold and ETF gold from the overall LBMA gold figure (of 7449 tonnes as of the end of March 2017) then whatever is left is not a very big quantity of gold bars, and at least some of this residual gold stored in the LBMA commercial vaults is owned by institutions, hedge funds, private individuals and platforms such as BullionVault.

In September 2015, a study of central bank gold held at the Bank of England calculated that about 3779 tonnes of Bank of England custody gold can be accounted for by central bank and monetary authority gold holdings. See “Central bank gold at the Bank of England” for details and GoldChartsRUs page “LBMA/BOE VAULTED GOLD, 2016 Update – The London Float”. Compared to the 4725 tonnes of gold held at the Bank of England at the end of February 2016, this would then mean that there were about 946 tonnes of gold at the Bank of England that was “unaccounted for by central banks". This was about 20% of the total amount of gold held at the Bank of England at that time.

If we look back now at the LBMA vault data for gold as of 31 March 2017, how much of this gold could be bullion banks (London float) gold.

LBMA total gold vaulted: 7449 tonnes

Bank of England gold vaulted: 5081 tonnes

Gold in commercial LBMA vaults: 2368 tonnes

Gold in ETFs: 1510 tonnes

Gold in commercial vaults not in ETFs: 858 tonnes

Gold in commercial vaults not in ETFs that is allocated to institutions & hedge funds = x

i.e. 7449 – 5081 = 2368 – 1510 = 858

Assume 10% of the gold at the Bank of England is bullion bank gold. Also assume bullion banks gold hold some gold in LBMA commercial vaults.

Therefore total bullion bank gold could be (0.1 * 5081) + (858 – x) = 508 + 858 – x = 1366 – x.

Since x has to be > 0, then the bullion bank London float is definitely less than 1300 tonnes and probably less than 1000 tonnes. The bullion banks might argue that they can borrow more gold from central banks, take gold out of the ETFs, and even import gold from refineries. All of these options are possible, but still, the London bullion bank float is not that large. And it is this number in tonnes of gold which should be compared to the enormous volumes of ‘paper gold’ trading that occur in the London Gold Market each and every trading day.

In May 2011, during a presentation at the LBMA Bullion Market Forum in Shanghai China, on the topic of London gold vaults, former LBMA CEO Stewart Murray included a slide which stated that:

Investment – more than ETFs

ETFs

- Gold Holdings have increased by ~1,800 tonnes in past 5 years, almost all held in London vaults

- Many thousands of tonnes of ETF silver are held in London

Other holdings

- Central banks hold large amounts of allocated gold at the Bank of England

- Various investors hold very substantial amounts unallocated gold and silver in the London vaults

The last bullet point of the above slide is particularly interesting as it references “very substantial amounts’ of unallocated gold and silver. Discounting the fact for a moment that unallocated gold and silver is not necessarily held in vaults or held anywhere else, given that it’s just a claim against a bullion bank, the statement really means that investors have ‘very substantial amounts‘ of claims against the bullion banks offering the unallocated gold and silver accounts i.e. very substantial liabilities in the form of unallocated gold and silver obligations to the gold and silver unallocated account holders.

If a small percentage of these claim holders / investors decided to convert their claims into allocated gold and silver, especially allocated gold, then where are the bullion banks going to get the physical gold to give to these converting claim holders? Neither do the claim holders of unallocated positions have any way of knowing how accurate the LBMA vault reporting is, because there is no independent auditing of the positions or of the report.

UBS and LBMA

The last line of the LBMA press release about the new vault reporting states the following:

“A detailed explanatory commentary follows, prepared by Joni Teves, Precious Metals Strategist, UBS”

This line includes an embedded link to the Teves report within the press release. This opens a 7 page report written by Teves about the new vault reporting. By definition, given that this report is linked to in the press release, it means that Joni Teves of UBS had the LBMA vault reporting data before it was publicly released, otherwise how could UBS have written its summary.

In her report, Teves states that a UBS database estimates that there are “1,485 tonnes of gold worth about $60bn and about 13,759 tonnes of silver worth about $7.85bn are likely to be held in London to back ETF shares“.

These UBS numbers are fairly similar to the ETF estimates for gold (1510 tonnes) and silver (12040 tonnes) that we came up with here at BullionStar, and so to some extent corroborate our previous ETF estimates. Teves also implies that some of the gold in the Bank of England figure is not central bank gold but is commercial bank gold as she says:

“let’s say for illustration’s sake that about 80% to 90% of BoE gold holdings are accounted for by the official sector.“

The statement on face value implies that 10% – 20% of Bank of England gold is not central bank gold. But why the grey area phrase of “let’s say for illustration’s sake". Shouldn’t the legendary Swiss Bank UBS be more scientific than this?

Teves also says assume “negligible amount (in commercial vaults) comprises official sector holdings“, and she concludes that “this suggests that over the past year, an average of about 2,945 to 3,450 tonnes ($119-$139 bn) of investment-related gold was held in London."

What she is doing here is taking the average of 9 months of gold holdings held in the LBMA commercial vaults (which is 2439 tonnes) and then adding 10% and 20% respectively of the 9 month average of gold held at the Bank of England (which is 506 and 1011 tonnes) to get the resulting range of between 2945 and 3451 tonnes.

Then she takes the ETF tonnes estimate (1485) away from her range to get a range of between 1460 and 1965 tonnes, as she states:

… “Taking these ETF-related holdings into account would then leave roughly around 1,460 to 1,965 tonnes or about $59bn to $79bn worth of gold in unallocated and allocated accounts as available pool of liquidity for OTC trading activities“

But what this assumption fails to take into account is that some of this 1,460 to 1,965 tonnes that is in allocated accounts is not available as a pool of liquidity, because it is held in allocated form by investors precisely so that the bullion banks cannot get their hands on it and trade with it. In other words, it is ring fenced. Either way, a model will always output what has been input into it. Change the 10% and 20% range assumptions about the amount of commercial bank gold in the Bank of England vaults and this materially alters the numbers that can be attributed to be an ‘available pool of liquidity for OTC trading activities’.

Additionally, the portion of this residual gold that is in ‘unallocated accounts’ is not owned by any investors, it is owned by the banks. The ‘unallocated accounts’ holders merely have claims on the bullion banks for metal that is backed by a fractional-reserve trading system.

In her commentary about the silver held in the London vaults, Teves does not comment at all about the huge gap between her ETF silver in London (which UBS states as 13,759 tonnes), and the full 32000 tonnes reported by the LBMA,and does not mention how this huge gap is larger than all the ‘Custodian Vault’ silver which Thomson Reuters GFMS attributes to the entire ‘Europe’ region.

Conclusion

The amount of gold in the London LBMA gold vaults (incl. Bank of England) that is not central bank gold, that is not ETF gold, and that is not institutional allocated gold is quite a low number. What this actual number is difficult to say because a) the LBMA will not produce a proper vault report that shows ownership of gold by category of holder, and b) neither will the Bank of England in its gold vault reporting provide a breakdown between the gold owned by central banks and the gold owned by bullion banks. So there is still no real transparency in this area. Just a faint chink of light into a dark cavern.

On the topic of London vaulted silver, there appears to be a lot more silver in the LBMA vaults than even GFMS thought there was. It will be interesting to see how GFMS and the LBMA will resolve their apparent contradiction on the amount of silver stored in the London LBMA vaults.

Popular Blog Posts by Ronan Manly

How Many Silver Bars Are in the LBMA's London Vaults?

How Many Silver Bars Are in the LBMA's London Vaults?

ECB Gold Stored in 5 Locations, Won't Disclose Gold Bar List

ECB Gold Stored in 5 Locations, Won't Disclose Gold Bar List

German Government Escalates War On Gold

German Government Escalates War On Gold

Polish Central Bank Airlifts 8,000 Gold Bars From London

Polish Central Bank Airlifts 8,000 Gold Bars From London

Quantum Leap as ABN AMRO Questions Gold Price Discovery

Quantum Leap as ABN AMRO Questions Gold Price Discovery

How Militaries Use Gold Coins as Emergency Money

How Militaries Use Gold Coins as Emergency Money

Hungary Announces 10-Fold Jump in Gold Reserves

Hungary Announces 10-Fold Jump in Gold Reserves

Planned in Advance by Central Banks: a 2020 System Reset

Planned in Advance by Central Banks: a 2020 System Reset

China’s Golden Gateway: How the SGE’s Hong Kong Vault will shake up global gold markets

China’s Golden Gateway: How the SGE’s Hong Kong Vault will shake up global gold markets