Irish Central Bank Raises Gold Reserves by 33%

Ronan Manly

Ronan Manly 0 Comments

0 CommentsRecently the Central Bank of Ireland joined the ranks of sovereign gold buyers, adding 2 tonnes of gold to its monetary gold reserves in 2 months, consisting of a tonne of gold bought in each of September and October 2021.

While in relative terms, the actual quantity of gold added by the Irish central bank was quite small, in percentage terms it was very substantial, since in August Ireland only held 6 tonnes of gold (supposedly held at the Bank of England), and as of the end of October Ireland now holds 8 tonnes of gold, i.e. a 33% increase (and a significant number for those in the know).

These latest monetary gold purchases by Ireland’s central bank are also notable because it’s not often that a central bank that is a) a Western European country, b) a Euro member country, and c) an OECD member country, buys monetary gold. In this instance, Ireland ticks the boxes on all three.

For example, during October 2021, while three of the four largest sovereign buyers of gold in the world were the notable gold aficionados namely Kazakhstan (6 tonnes), India (3.8 tonnes), and Russia (3 tonnes), the fourth, was Ireland (1 tonne), not what you would expect.

What sparked the Central Bank of Ireland to add to its monetary gold reserves is unclear, because like all Euro puppet central banks and BIS lackeys, the Irish central bank thinks that it does not need to be democratically accountable when it comes to monetary gold.

On a Need to Know Basis – And you don’t need to know!

When asked by Bloomberg’s reporter last week as to why the Bank had bought 2 tonnes of gold, a Central Bank of Ireland official replied that the Irish central bank’s gold transactions “are commercially sensitive and no further comment can be made at this time”.

See Bloomberg report from 1 December “Irish Central Bank Makes First Reserve Gold Purchases Since 2009”. Also viewable at an Irish Times link here.

But why would an EU vassal central bank feel the need to say that buying a modicum of physical gold was ‘commercially sensitive’? Probably it’s what they’ve been told to say by the ECB or BIS, but beyond this maybe it’s because they want to the buy the ultimate monetary asset, gold, while hoping that no one will notice.

For anyone familiar with the secrecy of central banks as regards their monetary gold holdings and gold transactions as well as their disdain for transparency, the lack of cooperation by the Irish central bank official is not surprising.

But specifically, as regards the Central Bank of Ireland, this latest obfuscation also brings to mind the contempt for transparency which the Irish monetary authorities exhibited previously (both the Irish Department of Finance and Central Bank of Ireland) when I tried to find out information about the storage arrangements of Ireland’s gold held at the Bank of England.

See BullionStar articles “Ireland’s Monetary Gold Reserves – High Level Secrecy vs FOI”, 23 January 2017, and “Ireland’s Monetary Gold Reserves: High Level Secrecy vs. Freedom of Information – Part 2” 30 January 2017, for details.

On those occasions I had to use Freedom of Information requests, and the Irish monetary authorities went out of their way to refuse the requests and avoided answering simple questions such as the form in which Ireland’s monetary gold reserves were held, the identity details (weight lists) of the gold bars the Central bank of Ireland claimed to hold, and whether any of Ireland’s monetary gold was on loan with bullion banks (commercial banks) via the Bank of England.

Ludicrously, their FOI refusals (in 2015) used excuses such as “the record concerned does not exist or cannot be found after all reasonable steps to ascertain its whereabouts have been taken,’ and they even had the gall to claim that divulging such information “could have a serious, adverse effect on the financial interests of the State”.

At that time, the Central Bank of Ireland also had held conference calls with the Bank of England about my FOI requests, with the Bank of England telling the Irish central bank that “you absolutely cannot’ send a statement out with bars total and fine ounces since its ‘highly classified’.”

Upon making an FOI Appeal following it’s refusal to be transparent, the Irish central bank reluctantly in 2017 sent me 2 measly Swift records of Central Bank of Ireland gold at the Bank of England dated 2009 and 2010, which merely consisted of records showing varying gold balances against a total number of bars, i.e. they could not produce any weight lists of gold bars. This revealed that the Irish gold in London is not held on an earmarked set-aside basis but merely on a fine ounce basis (like a cash account). See Swift records here.

Contrast this parochial Irish small-mindedness with the openness and transparency of the central banks of Poland and Hungary when those central banks recently bought and repatriated huge quantities of gold, complete with press conferences and official announcements as well as multiple photos of their gold bars arriving back into their domestic vaults in Warsaw and Budapest, plus photos of the gold being repatriated by plane back from London. See here for Hungarian gold purchases and here for Polish gold repatriation,

Ireland’s Gold Purchase Data

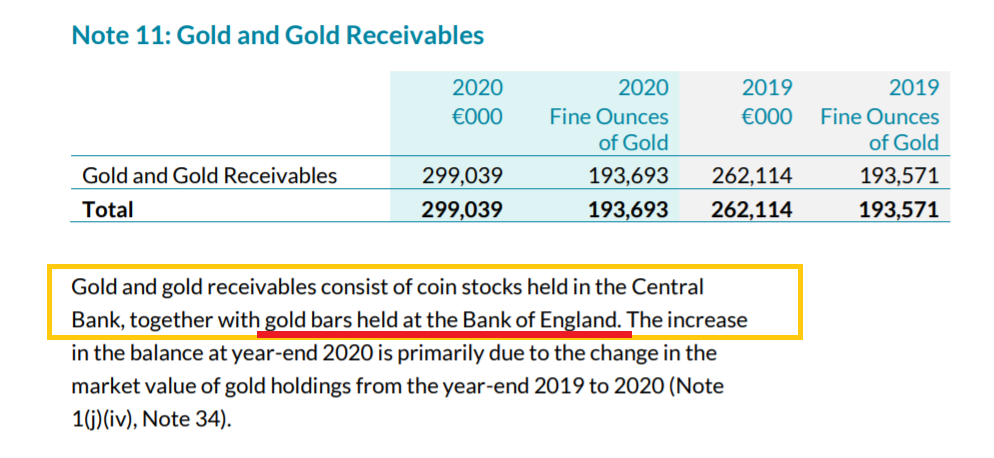

Looking quickly at the data behind the latest gold buying by the Irish central bank, what can we see? Before the gold buying in September and October 2021, Ireland claimed to hold 193,693 fine troy ounces of gold. As the latest Central Bank of Ireland annual report for 2020 – 2021 states, this consisted of:

“Gold and gold receivables [in the form of] coin stocks held in the Central Bank, together with gold bars held at the Bank of England.”

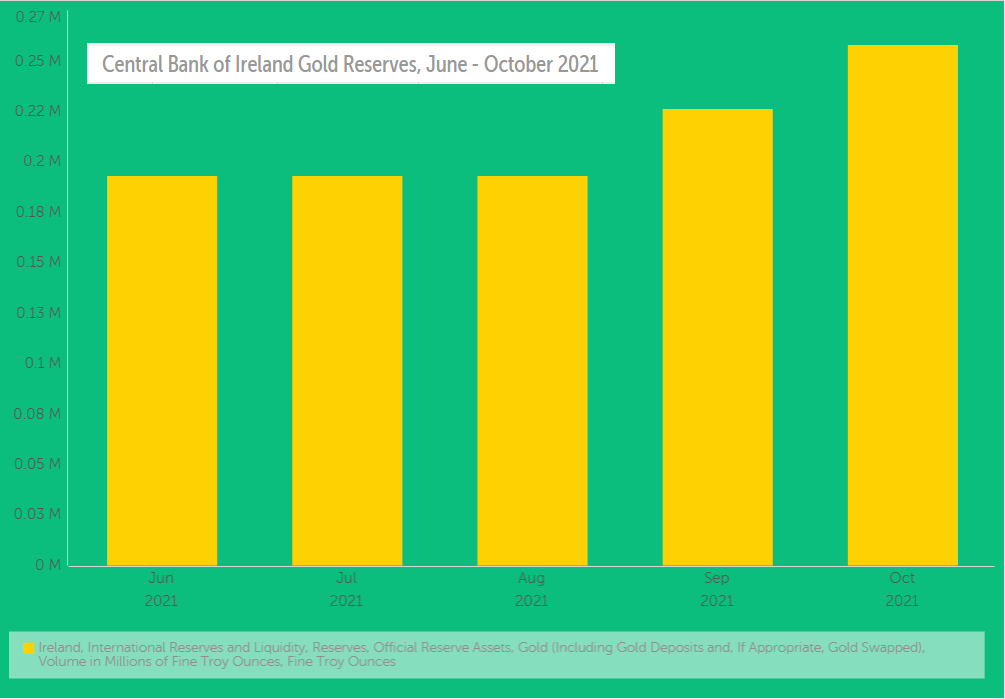

Looking at the IMF International Financial Statistics (IFS) database, and querying the ‘International Reserves” table for Ireland’s gold holdings, we see that as of the end of August 2021, Ireland held 0.19 million ounces of gold (which is the 193,693 ozs rounded up).

From the same IFS table, we see that by the end of September 2021, Ireland’s gold holdings had increased to 0.23 million ozs. By the end of October 2021, the IFS data shows Ireland’s gold holdings increasing to 0.26 million ozs.

Next we can look at a spreadsheet on the Central Bank of Ireland’s own website (here), namely the “Template on International Reserves and Foreign-Currency Liquidity” dated 31 October 2021.

In this table under the category ‘Official reserve assets and other foreign currency assets’ the first line item is “Monetary gold (including gold deposits and gold swaps)” worth € 395.8 (million).

Interestingly, this table says that all of this gold is ‘Gold Bullion’ and that it consists of a ‘volume in million of fine troy ounces’ of 0.258 (ie.e 258,000 ozs). and that none of this gold is held in ‘Unallocated gold accounts’. Likewise the table states that none of this gold is ‘monetary gold under swap for cash collateral’.

Comparing the latest figure of 258,000 ozs to the end of August total of 193,693, this gives a net increase of 64,307 ozs, which is exactly 2 metric tonnes. Hence, the Irish gold reserves have increased from 6.02 tonnes to 8.02 tonnes (or about 640 London Good Delivery gold bars) As to where exactly this 2 tonnes of gold was purchased and where it is now stored, we cannot say, but in all probability it was bought at the Bank of England and was at the time of purchase still stored in the Bank of England. The only gold of Ireland that is stored in Ireland are the gold coin stocks held at the Central Bank of Ireland Mint in Sandyford, Co. Dublin.

Note though that this International Reserve table and it’s accounting can deceive you, and some or all of this Irish gold (even if it’s not in unallocated form) could still be out on loan at the Bank of England. Hence the caveat ‘including gold deposits’ categorization in “Monetary gold (including gold deposits and gold swaps)”.

Until such time as the Central Bank of Ireland comes clean and publishes full details of the location of its gold holdings and it’s current and historic gold lending positions, and a full weight list of all 640 of its London Good Delivery gold bars held, along with refiner serial number, refiner name, and fine troy ounce weight, the jury would be wise treat the unencumbered nature of this gold, and even its existence, with suspicion.

As Chris Powell of GATA sometimes says:

“The amounts, location, and disposition of government gold reserves are secrets more sensitive than the amounts, location, and disposition of nuclear weapons.

Indeed, under nuclear weapons control treaties, governments with nuclear weapons have often shared that sort of information, even with hostile powers. But gold reserve information is far more tightly held and most gold information provided officially is actually disinformation.“

While the Irish central bank and it’s partners in crime the Bank of England will never allow publication of a real gold bar weight list to happen, it still may be a good time to now fire off a new FOI request to the Central Bank of Ireland. For as they say “Nothing Ventured, Nothing Gained”.

Conclusion – Inflation Ahead

As Bloomberg noted in its article:

“While the [Central Bank of Ireland] has given no reason for the increase in its [gold] stockpile, the Governor Gabriel Makhlouf last week warned that policy makers cannot afford to be complacent on inflation.”

What Bloomberg was referring to here were remarks made by Makhlouf in a speech on 23 November titled “Inflation dynamics in a pandemic: maintaining vigilance and optionality”, in which the Irish central bank governor began by saying that:

“After more than a decade of very low inflation in the euro area, and especially in Ireland, prices for many goods and services have risen faster in 2021.”

Makhlouf continued that:

“A key challenge for central banks in the euro area and around the world is how to respond to this change in inflation dynamics.

The key judgement we need to make is whether current developments are mainly transitory and will fade over time, or if there have been structural changes that lead to broad-based and persistent inflation trends.

In other words, are we going back to familiar territory or to something different?”

Given that the ‘inflation is transitory’ narrative has fallen apart, and given the ramping up of Ireland’s gold reserves in September and October by a whopping 33%, it appears that the Governor Makhlouf of the Central Bank of Ireland now thinks that the inflation coming down the pipe is indeed “something different”.

Gabriel Makhlouf is an economist and former Secretary to the New Zealand Treasury, as well as former Private Secretary to then British Chancellor of the Exchequer, Gordon Brown. While Brown is infamous (among other things) for being at the helm and pushing through the disastrous UK gold sales at firesale prices over 1999-2002 (a bullion bank bailout now known as Brown’s Bottom), perhaps Makhlouf learned a thing or two from that episode and understands that in times of financial crises, the ultimate asset to buy and hold is real gold.

Popular Blog Posts by Ronan Manly

How Many Silver Bars Are in the LBMA's London Vaults?

How Many Silver Bars Are in the LBMA's London Vaults?

ECB Gold Stored in 5 Locations, Won't Disclose Gold Bar List

ECB Gold Stored in 5 Locations, Won't Disclose Gold Bar List

German Government Escalates War On Gold

German Government Escalates War On Gold

Polish Central Bank Airlifts 8,000 Gold Bars From London

Polish Central Bank Airlifts 8,000 Gold Bars From London

Quantum Leap as ABN AMRO Questions Gold Price Discovery

Quantum Leap as ABN AMRO Questions Gold Price Discovery

How Militaries Use Gold Coins as Emergency Money

How Militaries Use Gold Coins as Emergency Money

Hungary Announces 10-Fold Jump in Gold Reserves

Hungary Announces 10-Fold Jump in Gold Reserves

Planned in Advance by Central Banks: a 2020 System Reset

Planned in Advance by Central Banks: a 2020 System Reset

China’s Golden Gateway: How the SGE’s Hong Kong Vault will shake up global gold markets

China’s Golden Gateway: How the SGE’s Hong Kong Vault will shake up global gold markets