Hungary Boosts Gold Reserves by 3,000% in Under 3 Years

Ronan Manly

Ronan Manly 0 Comments

0 CommentsThe central bank of Hungary, the Magyar Nemzeti Bank (MNB), has just announced a purchase of a massive 63 tonnes of Good Delivery gold bars, and in doing so tripled the nation’s gold holdings from 31.5 tonnes to 94.5 tonnes.

In its press release about the huge transaction, published 7 April, the Hungarian central bank explains its rationale for the dramatic purchase of what is approximately 5040 large (400 oz) gold bars, highlighting that gold has no credit risk and no counterparty risk, and so reinforces sovereign trust over all economic environments (normal and extreme), while being one of the most crucial reserve assets that a central bank can hold.

From 10 Fold to 30 Fold

For those who may remember, this is not the first major gold purchase by the Hungarians in recent times, as the Hungarian central bank also caused shockwaves in October 2018 when it purchased 28.4 tonnes of gold, on that occasion increasing its gold reserves 10 fold from 3.1 tonnes of 31.5 tonnes, or a 1000% increase. See the BullionStar article “In surprise move, Central Bank of Hungary announces 10-fold jump in its gold reserves” from October 2018.

This means that over exactly two and a half years, the Hungarians have increased their sovereign gold reserves by a staggering 3000%, or 30 fold, from 3.1 tonnes to 94.5 tonnes, an absolute increase of 91.4 tonnes. How’s that for a conviction trade?

On the October 2018 occasion, the Hungarians purchased their 28.4 tonnes of gold at the Bank of England in London, and repatriated it back to Hungary in the same month, announcing the purchase and the repatriation at the same time, saying that ‘the repatriation has already taken place‘.

On this occasion, the MNB does not say where it bought its 63 tonnes of gold, but it may well have been again at the Bank of England in London. Nor does the MNB say if the 63 tonnes of gold has been repatriated to Hungary yet. However, going on the previous pattern from 2018, one would expect that yes it has been brought back to Hungary by plane and under heavily armed guard.

A No Confidence Vote in the System

Interestingly, this time around in 2021, the Magyar Nemzeti Bank says that part of the motivation for the new gold purchase is in “managing new risks arising from the coronavirus pandemic”, which is a subtle way of saying that since central banks and governments around the world have used the Covid excuse to ramp up debt levels, ramp up quantitative easing and ramp up money supply growth, therein debasing their fiat currencies and introducing inflationary risks to bond holders, the Hungarians are simultaneously ramping up their physical gold holdings to counter this insanity.

Or said in the diplomatic language of the latest Hungarian central bank press release, these concerns “further increase the importance of gold in national strategy as a safe-haven asset and as a store of value.”

The language of the NMB in 2021 is also similar to that which it used in 2018 when the Monetary Council of the Hungarian central bank said it was buying large quantities of physical gold since:

“Gold is still considered to be one of the world’s safest assets, whose characteristics can be attributed to gold’s unique properties such as finite supply of physical gold, and lack of credit and counterparty risk given that gold is not a claim against a specific partner or country.”

and

“gold remains one of the safest instruments in the world, and, even under normal market conditions, provides a stability and confidence-building function.”

The latest Hungarian central bank press release also describes its new 63 tonne gold purchase as part of a process, the first phase of which was the increase in its gold reserves by a factor of 10 in October 2018. So this new 2021 purchase can now be seen as phase 2, and as the MNB says “with these purchases [in 2021], the MNB continued the process it started in 2018.” In both sets of gold transactions, the Bank describes the gold buying as being in line with its “long-term national and economic policy strategy objectives”.

While the phase 1 gold purchases took place over the first 2 weeks of October 2018, the Bank does not state exactly when the new 63 tonnes of gold was acquired, but assuming in was within the last month, it also looks like good timing, as the spot gold price has been mostly trading in a range of $1750 – $1700.

The average LBMA Gold (fix) Price (an average of both the AM and PM fixes) over the month of March 2021 was $1720, so this would put the 63 tonnes gold transaction at an average purchase value of US $3.484 billion.

Hungary – Now a Major League Gold Holder

This huge new gold purchase also catapults Hungary into 36th position in the international rankings of country gold reserves (excluding IMF, ECB and BIS gold), from 56th position previously. Going back to pre-October 2018, the combined gold purchases of 91.4 tonnes in 2018 and 2021 boost Hungary from a minnow gold holder which was languishing in about 87th position in the international league table, to a major player on the central bank stage within the top 30% of central banks.

Hungary will obviously now turn more heads at the BIS central banker cocktail parties in Basle. But maybe more importantly to the Hungarian central bankers, the latest gold purchase boosts Hungary from the 6th largest to the 3rd largest sovereign gold holder in the Central and Eastern European (CEE) region, and boosts gold reserves per capita in Hungary from 0.1 ounce to 0.31 ounce, the highest gold reserves per capita in the CEE region.

It also boosts the MNB’s gold as a percentage of its total reserve assets from 4.7% to about 14.1%, assuming the same reserve base. So since 2018, Hungary has now risen from far down in the international gold reserves league table to a respectable position towards the top, in terms of both the absolute size, and the proportion of gold reserves to total reserves that it holds.

Last time around in October 2018, the Hungarian central bankers said that:

“the possession and the increase of nations’ precious metals holdings appear to be decisive international trends.”

This time around, the MNB press release puts figures on the huge combined gold buying by this select group of central banks over recent years, acknowledging that:

“the role of gold within international reserves has been enhanced at several central banks. At 656 tons, central banks’ demand for gold reached record highs in 2018 and also in 2019 (669 tons).”

These exact figures were actually highlighted in a recent BullionStar infographic about ‘Central Bank Gold Buying and Gold Repatriation’, which can be seen here. In fact, the Hungarian gold purchase and repatriation from 2018 is prominently featured in that infographic.

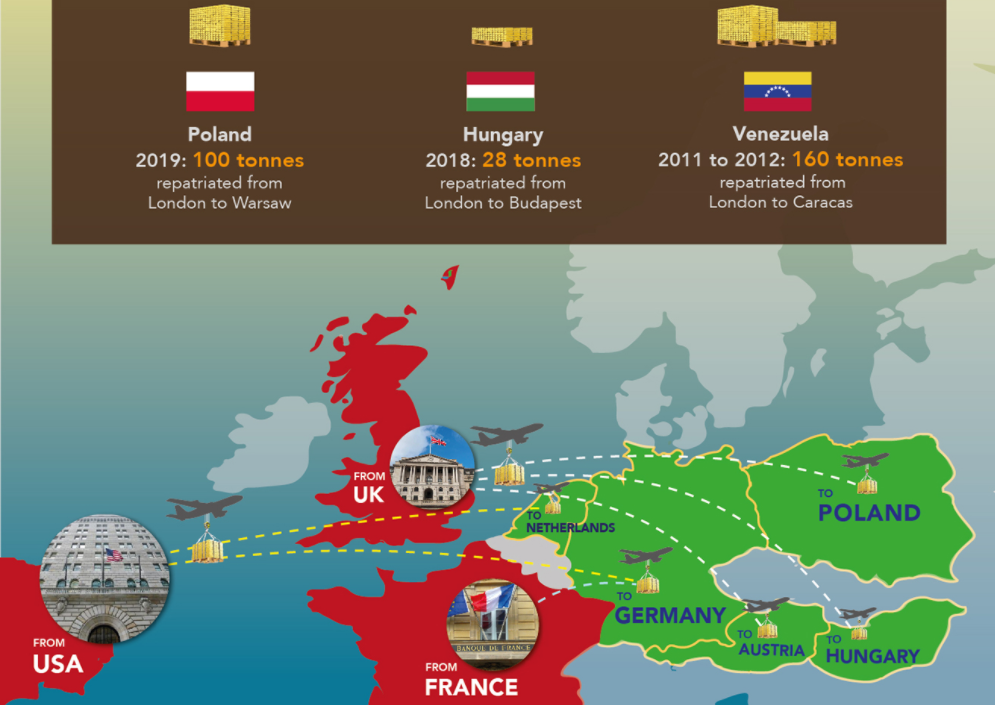

Furthermore, the 63 tonne gold transaction by Hungary is the largest accumulation of gold by any central bank in 2021, the second biggest gold purchase by any central bank since the start of 2020 (and the biggest if excluding Turkey whose central bank gold purchases are difficult to decipher since they are intertwined with Turkey’s commercial banking system). The Hungarian 63 tonne transaction is also one of the biggest ‘on market’ central bank gold transactions since the start of 2019, second only to Poland’s 100 tonne purchase in 2019. Note that Russia purchased 158 tonnes of gold in 2019 but that gold was from domestic mining production.

Poland and Hungary – In Sync

Speaking of Poland, its worth a reminder that the central bank of Hungary’s regional neighbour to the north, the National Bank of Poland (NBP), purchased 100 tonnes of gold in the first half of 2019, also at the Bank of England in London (see here), and over the next few months, airlifted that 100 tonnes of gold back to Poland to the NBPs vaults in Warsaw.

A total of eight flights transported the Polish gold over a few months, with one thousand gold bars in each flight, with the final flight being in November 2019. See here for details. This gave the NBP a sizeable 228.6 tonnes of gold in its reserves, as it had purchased 25.7 tonnes of gold in 2018, and prior to that claimed to hold 103 tonnes of gold.

Not only that, but very recently in an interview in mid-March 2021, the governor of the Polish central bank, Adam Glapinski, said that the NBP now wants to buy another 100 tonnes of gold and store this gold in its vaults in Warsaw – “’Over the course of a few years we want to buy at least another 100 tonnes of gold and keep it in Poland as well,’ he said”. See Polish language report of this interview here.

Like Hungary, Glapinski thinks that having large gold reserves increases “the perception of the state and its economic strength”, and he actually wants the NBPs gold reserves to increase to 20% of total NBP reserve assets, from the current 9% now.

Do you believe Bloomberg?

The Polish central bank’s actions also may have been in the minds of the Hungarian central bankers when deciding upon an appropriate gold accumulation and benchmark level for Hungarian gold reserves. Could we now be witnessing a physical gold accumulation race between the savvy central bankers of central and eastern Europe. It sure looks like it!

This all seems to be lost, however, on Bloomberg’s Joe Weisenthal who ironically on 5 April, two days before the Hungarians’ huge 63 tonnes of physical gold purchase was announced, tweeted that “GOLDBUG MACRO IS DEAD. I’m officially calling it. Goldbugs have had enough time to make their case. They failed. It’s over.”

GOLDBUG MACRO IS DEAD

— Joe Weisenthal (@TheStalwart) April 5, 2021

I’m officially calling it. Goldbugs have had enough time to make their case. They failed. It’s over.https://t.co/Pl5nZqsNJq pic.twitter.com/gXAlgCHUZk

So who do you trust, the central banks of old Europe such as Hungary and Poland who say that “gold has a confidence-building effect in normal times and can play a role in stabilizing and defending, and also gold is for extreme market environments, structural changes in the international financial system, and deeper geopolitical crises”, or do you trust a Bloomberg columnist in Manhattan who has “officially called it” and said that gold “is over”?

Popular Blog Posts by Ronan Manly

How Many Silver Bars Are in the LBMA's London Vaults?

How Many Silver Bars Are in the LBMA's London Vaults?

ECB Gold Stored in 5 Locations, Won't Disclose Gold Bar List

ECB Gold Stored in 5 Locations, Won't Disclose Gold Bar List

German Government Escalates War On Gold

German Government Escalates War On Gold

Polish Central Bank Airlifts 8,000 Gold Bars From London

Polish Central Bank Airlifts 8,000 Gold Bars From London

Quantum Leap as ABN AMRO Questions Gold Price Discovery

Quantum Leap as ABN AMRO Questions Gold Price Discovery

How Militaries Use Gold Coins as Emergency Money

How Militaries Use Gold Coins as Emergency Money

Hungary Announces 10-Fold Jump in Gold Reserves

Hungary Announces 10-Fold Jump in Gold Reserves

Planned in Advance by Central Banks: a 2020 System Reset

Planned in Advance by Central Banks: a 2020 System Reset

China’s Golden Gateway: How the SGE’s Hong Kong Vault will shake up global gold markets

China’s Golden Gateway: How the SGE’s Hong Kong Vault will shake up global gold markets