Why the SEC Keeps Rejecting Bitcoin ETF Listings

JP Koning

JP Koning 2 Comments

2 CommentsLast week the U.S. Securities and Exchange Commission (SEC) refused to approve nine different proposals for bitcoin exchange traded funds (ETFs). This comes on top of a number of prior SEC refusals of bitcoin-based funds, including the SolidX Bitcoin Trust and two separate denials of the Winklevoss Bitcoin Trust, the first in 2017 and the second this summer.

Why have so many other U.S.-listed commodity ETFs been approved over the years whereas bitcoin ETFs keep getting rebuffed? It is tempting to view the SEC smackdown of these bitcoin ETF proposals as a sign of distaste for this new and anarchic technology. But I don’t think this reading is accurate. If anything, SEC vs Bitcoin is less about Bitcoin and more about the SEC’s attempt to impose standards in an age where Wall Street is trying to package almost everything into a broadly-available security.

Precious metals buyers will of course be familiar with ETFs. The granddaddy of all commodity ETFs, the SPDR Gold Trust, or GLD, has been around since 2004 and is currently backed by around US$29 billion in physical gold, or 760 tonnes. All ETF units trade on a stock market. A peculiar set of mechanics ensures that they replicate the price of their underlying index or commodity. Using GLD as an example, if the price of the ETF is above the current gold price, then special institutions (otherwise known as authorized participants) can buy physical gold, exchange it for new units of GLD, and sell those units at a profit. If GLD is trading below the gold price, these same authorized participants can buy the underpriced GLD units, redeem them for gold, and sell the commodity for a risk-free gain. Competition among authorized participants for profit ensures that the two prices do not diverge by very much. Regular investors do not have the ability to convert units into gold, or vice versa. (For a more thorough explanation, see Bullionstar’s introduction to gold ETFs.)

The SEC has approved ETFs that track gold, silver, platinum, palladium, copper, oil, natural gas, coffee, as well as broader-based ETFs that track baskets of commodities. Virtual currencies like Bitcoin, also known as cryptocurrencies, have been defined by the U.S. Commodity Futures Trading Commission (CFTC) to be commodities. The SEC’s refusal to allow bitcoin ETFs thus has nothing to do with bitcoin’s underlying nature: like gold, silver, and the rest, it is legally a commodity. Rather, the reason that the Winklevoss Bitcoin Trust, the first of the proposed bitcoin ETFs, has failed to make it through the SEC’s doors is that the SEC doesn’t like the way that the market for bitcoins is structured.

Cooperation from crypto exchanges – A tall order

Specifically, the SEC is unhappy with the inability of the the Bats BZX Exchange, the stock exchange on which the Winklevoss Bitcoin Trust is seeking a listing, to secure information sharing agreements (ISAs) with important bitcoin exchanges. An information sharing agreement between the Batz BZX exchange and, say, Chinese-based Binance, one of largest bitcoin exchanges, would obligate Binance to share relevant data about market trading activity and customer identities with Bats.

The SEC believes that information sharing agreements with significant exchanges are key to compliance with the Securities Exchange Act, the body of legislation that governs the SEC. Specifically, Section 6(b)(5) of the Act requires the SEC to ensure that the securities exchanges it regulates, including Bats BZX, are designed to prevent fraudulent and manipulative acts and to “protect investors and the public interest."

The SEC has chosen to take a very strict interpretation of 6(b)(5) when it comes to the listing of an overlying security, i.e. securities that derive their value from some underlying security or commodity (much like how units of the Winklevoss Bitcoin Trust overlie, or are underlain by, physical bitcoin). Not only must an exchange like Bats BZX ensure that it has controls to prevent manipulative behaviour of Bats-listed overlying securities, but it must also take reasonable steps to ensure that the underlying instrument to which it is linked is traded on an exchange that is held to the same standards. The SEC deems that an information sharing agreement between the relevant exchanges is sufficient to fulfill this requirement. That way, if there were to be suspicions of manipulation of bitcoin on the Binance exchange, Bats BZX would be able to get data from Binance and use it to conduct investigations into possible trading violations.

In its second refusal of the Winklevoss Bitcoin Trust, the SEC maintained that it has a long history of requiring information sharing agreements between SEC-regulated exchanges that list overlying securities and exchanges that list the underlying instrument. It points to a ruling it made in 1994 in which it required that the CBOE, which wanted to list equity options on American Depository Receipts (ADRs), would in certain cases be required to have a formal mechanism for getting information from the overseas exchanges trading the individual stocks underlying the ADR.

The SPDR Gold Trust as precedent

The SPDR Gold Trust (GLD) provides further precedent. When the SPDR Gold Trust was approved in 2004, the sponsoring exchange, the New York Stock Exchange (NYSE), was unable to establish information sharing agreements linked to spot trading. Securing agreements was deemed impossible since most gold spot exchanges occurs relatively informally via the London over-the-counter gold market.

In lieu of information about spot exchanges, the SEC decided that two factors were sufficient for the proposal to meet its requirements. First, it claimed that gold OTC markets are very liquid and thus difficult to manipulate. Second, the NYSE had an information sharing agreement with NYMEX, whose COMEX division listed the most popular set of gold futures contracts. Since the COMEX market is a regulated exchange that the SEC deemed “significant", the sharing of information between the NYSE and COMEX would help ensure that manipulation could be caught. The meaning of “significant" is sizable relative to overall trading volumes.

In the case of the Winklevoss Bitcoin Trust, the Bats BZX had entered into an information sharing agreement with the the Gemini Exchange, a New York-based bitcoin exchange that allows for spot trade. However, the SEC has decreed that this agreement is not sufficient to meet its requirements. The SEC maintains that bitcoin trading is dominated by unregulated non-US exchanges (like Binance). In this context, Gemini accounts for only a small fraction of global bitcoin trading, and therefore if a manipulation attempt were to succeed in causing a large change in the price of bitcoin, it would likely be carried out on a dominant exchange, like Binance, and not Gemini. Thus, an information sharing agreement with Gemini simply won’t be effective for sniffing out manipulators.

A quick perusal of Coinmarketcap.com, a website that tracks bitcoin trading statistics, confirms that unregulated non-U.S. bitcoin exchanges dominate bitcoin trading (see screenshot below). On 31 August 2018, for instance, Gemini ranked 74th in terms of 24-hour bitcoin volume, at $18 million, whereas Binance clocked in near the top at $295 million.

Nor is the existence of information sharing agreements with a regulated bitcoin futures market sufficient to change the SEC’s opinion. This is relevant because two large U.S. futures exchanges, the CBOE Futures Exchange (CFE) and CME, both launched trading of their bitcoin futures contracts in December 2017. Given that an information sharing agreement between the NYSE and NYMEX was sufficient to allow GLD to list, would an equivalent agreement between Bats BZX and either of these two futures exchanges constitute enough support for the Winklevoss Bitcoin Trust to proceed? Not so, says the SEC. In the case of other commodity ETFs like GLD, the SEC had sufficient evidence that the U.S. futures market for that commodity was large enough to be “significant." Regulated bitcoin futures still constitute a relatively unimportant part of overall bitcoin trading.

This logic used by the SEC needn’t just apply to bitcoin. It might explain why there is no rhodium ETF in the U.S., for instance, whereas there is one in both Europe and South Africa. Since there is no exchange that offers rhodium futures and the spot market is relatively opaque, it would not be possible for an SEC-regulated exchange to set up the information sharing agreements necessary for SEC approval of a rhodium-based financial product. This echoes what I said at the outset: the SEC’s decision is less about bitcoin and more about grappling with the complexity of market structure in an age in which financial magicians are trying to package everything into an exchange-traded product.

Dissent within SEC: underlying asset out of scope?

Interestingly, one of the four SEC Commissioners, Hester Pierce, dissented from the regulator’s decision to disallow the Winklevoss Bitcoin Trust to be listed. Her reasoning is that a reading of Section 6 of the Exchange Act does not permit the SEC to focus on the underlying market for a proposed security, whether that underlying market be the bitcoin or gold spot market. Pierce believes the SEC only has the right to regulate the market for the overlying asset, i.e. units of a Bitcoin ETF or a Gold ETF. Pierce has previously advocated a Hayekian view of markets, in which the dispersed nature of information leaves no roll for a single “omniscient" regulator:

“Regulators are people, and they are people without great access to information, so we’re asking them to do a task that they’re destined to fail at… not because they don’t have good intentions and not because they don’t work hard… they do… they’re hard working people but they’re just not going to be able to succeed at the task."

Pierce’s criticism would constitute not just a roll-back of the SEC’s bitcoin decisions, but would also throw out a decade or two of previous SEC decisions related to information sharing practices of proposed commodity-linked ETFs.

The next Bitcoin ETF – Further rejections likely

The next big bitcoin ETF that is slated for an SEC decision is the CBOE Exchange’s proposal to list the VanEck SolidX Bitcoin Trust. Given that Pierce’s dissent is unlikely to sway the three remaining SEC commissioners, I don’t expect this ETF to be approved. Let’s look at the part of the proposal that has to do with information sharing agreements:

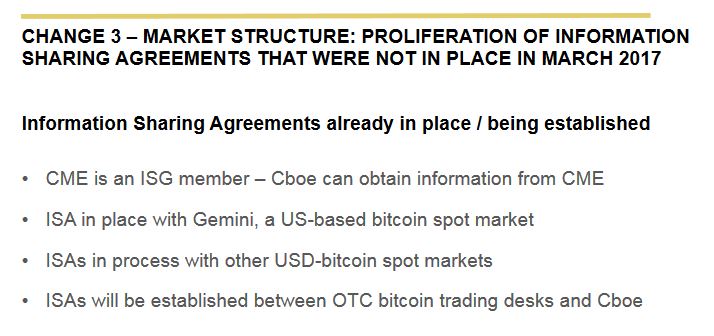

The creators of the VanEck SolidX Bitcoin Trust point to a number of information sharing agreements into which the sponsor, the CBOE, has signed (or expects to sign). We already know that those with the CME, which lists bitcoin futures, and Gemini will not be sufficient to establish significance. What about the agreements signed between the CBOE and Bitcoin over-the-counter trading desks? The creators claim that the relevant OTC markets account for around US$250–$500 million in trading per day. But with overall exchange-related bitcoin volumes said to come in at around $4 billion per day, it will be difficult for the creators to prove that OTC trading constitutes ‘significant’.

Lastly, the creators of the trust point to “other USD-bitcoin spot markets." I interpret this to mean that they may succeed in getting other U.S.-based bitcoin exchanges to join Gemini in sharing information. But if it can’t get some of the largest actors in the list above, say Binance, Bitfinex, or OKEx, all of which are based outside of the US, it’s hard to see how the SEC will provide its stamp of approval.

Popular Blog Posts by JP Koning

How Mints Will Be Affected by Surging Bullion Coin Demand

How Mints Will Be Affected by Surging Bullion Coin Demand

Banknotes and Coronavirus

Banknotes and Coronavirus

Gold Confiscation – Can It Happen Again?

Gold Confiscation – Can It Happen Again?

Eight Centuries of Interest Rates

Eight Centuries of Interest Rates

The Shrinking Window For Anonymous Exchange

The Shrinking Window For Anonymous Exchange

A New Era of Digital Gold Payment Systems?

A New Era of Digital Gold Payment Systems?

Life Under a Gold Standard

Life Under a Gold Standard

Why Are Gold & Bonds Rising Together?

Why Are Gold & Bonds Rising Together?

Does Anyone Use the IMF’s SDR?

Does Anyone Use the IMF’s SDR?

HyperBitcoinization

HyperBitcoinization