Why Does Money Inflate?

JP Koning

JP Koning 1 Comments

1 CommentsPeople who live in developed nations have grown used to inflation of around 2% a year over the last few decades. Why do prices generally rise by that amount? What drives the purchasing power of money in these countries? Why can’t prices stay constant year-over-year rather than increasing?

To help answer some of these questions, let’s go far back in time. We’ll divide the last one thousand or so years into three monetary eras: the silver coin period, metal-backed notes, and fiat money. How would the nature of inflation have changed as you passed from one era into the next?

The medieval coin era

Silver coins were the chief medium of exchange in the first five or six centuries of the last millennium. Even though coins were composed of scarce metal, inflation was a fairly common occurrence in medieval times. Coins were not perfectly durable. They suffered from wear and tear, both from sweaty hands and as they came into contact with other coins while in a pocket or purse. Since the value of a medieval coin was ultimately determined by the amount of silver in it, the purchasing power of the coinage would naturally decline each year as it shed silver. So rising prices, or inflation, was inherent to medieval coin systems.

The wear and tear of the coinage would often be accompanied by deliberate attempts on the part of the public to remove silver from coins. This came in the form of clipping, in which people would cut small bits of silver from the coin’s edge, and sweating, in which a bag of coins was shaken, the dislodged bits collecting at the bottom of the bag. Clipping and sweating were illegal and punishable by death during medieval times, but that didn’t stop people from doing it.

To make matters worse, from time to time kings and queens would adopt a policy of aggressively reducing the silver content of coins in order to raise revenues, mostly to fight wars. In medieval times, mints operated differently than they do now. Anyone could bring raw silver to the mint to be turned into coins, paying a small minting fee to the monarch. By reducing the silver content of the coinage, the monarch incentivized everyone to quickly bring in their old silver coins to be coined into new coins. After all, people could get more coins for each ounce of silver they owned, thus allowing them to pay off more debts than before. This would create a one-time spike in mint throughput, thereby boosting royal revenues from fees.

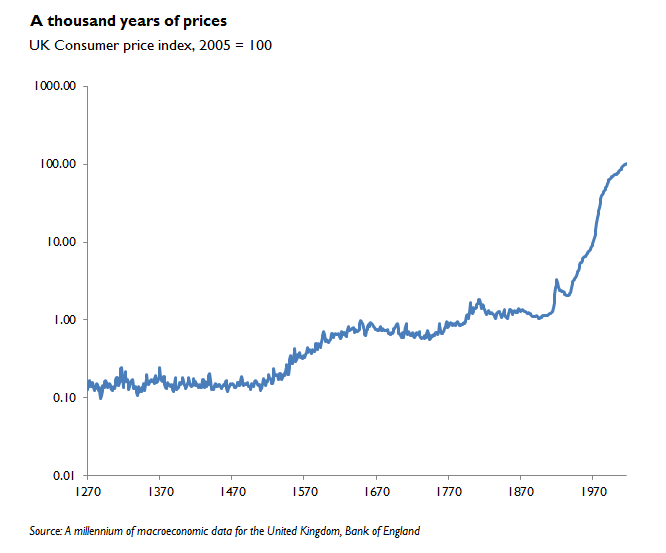

One of history’s most aggressive medieval debasers was Henry VIII, who announced ten debasements between 1542 and 1551, each in the region of 30-40%. These diminutions were so successful in driving silver to the royal mints that Henry had to erect six new ones just to meet demand. Between 1541 and 1556, the English consumer price index rose by 123%. It’s possible to see this spike in the chart below.

Not all kings and queens debased the currency. Every once in a while one of them would try to restore the standard by announcing a general recoinage. All citizens were obliged to bring in their coins to the mint where they would be weighed and then melted down into new coins. The new coins would have a restored amount of silver in them, thus undoing some of the wear-and-tear-induced inflation of previous years.

Finally, advances in silver mining technology and new discoveries had a major role to play in determining the level of medieval prices. If the supply of silver suddenly increased while demand remained unchanged, the price of silver would decline relative to that of other goods. And since coins were themselves composed of silver, their purchasing power would decline. Or, put differently, inflation would occur as all prices in the economy rose. Deflation, a fall in prices, was just as likely to occur under a silver coin standard. If the population was growing with the supply of silver failing to keep up, then the price of silver would have to rise, or a general deflation would set in.

To sum up, inflationary episodes during the medieval silver coin area could be explained by a complex combination of natural wear and tear of coins, debasement by kings and queens counterbalanced by the odd recoinage designed to restore the standard, and changes in the fundamentals of the underlying silver market. The strongest inflations occurred when all these forces were aligned. For instance, if a new drilling technique suddenly opened up deeper silver deposits for exploitation, and the monarch was simultaneously debasing the standard to help fund wars, then—combined with natural wear and tear—the result would be a rapidly increasing prices.

The metal-backed banknote era

Bankers soon learnt how to make money out of paper. This would begin to change the complexion of inflation.

As long as bankers maintained full convertibility of their banknotes into the underlying commodity, then the banknotes they issued could not have any direct influence on the economy-wide price level. Alterations to the quality and nature of the coins themselves, as well as deeper changes in the underlying silver market, still dictated inflation, as they did in the coin era.

It’s worth investigating this point further. Inflation occurs when people have too much money in their wallets relative to demand. With nowhere to go, money becomes a hot potato. Merchant A doesn’t want to hold an extra $100 bill or silver coin in their wallet, so he spends it at Merchant B’s store, who doesn’t want it so she spends it at person C’s store, and on and on, each trade in this chain pushing up prices ever so much. The hot potato process only comes to a halt when all prices in the economy have been driven high enough that the $100 bill or silver coin is no longer unwanted, and it comes to a rest.

By providing an alternative exit for banknotes, convertibility short-circuits this hot potato effect. Say a banker had lent too many banknotes into circulation relative to demand. Rather than boomeranging through the economy hot potato-like, an unwanted $100 bill quickly returns to the issuing bank for redemption, long before it has exerted any influence on the price level.

Although they had no direct influence on the general level of prices, banknotes would have had an indirect influence on prices. As paper money gradually became more popular relative to coins, the demand for silver would have declined relative to the supply, and this would have put gentle downward pressure on the silver price and conversely upward pressure on the economy-wide price level. Second, as people opted to use paper money to meet their spending requirements, coins would have slowly disappeared into vaults. Since this mean that coins circulated less, the inflation that had historically occurred thanks to wear & tear, clipping, and sweating would have receded.

The real novelty in the age of metal-backed bank notes was when convertibility was temporarily suspended. During these periods, bankers and the banknotes they issued could have a direct influence on the economy-wide price level. With the traditional exit into specie or coin being severed, any banknote issued in excess of public demand would act like a hot potato. Rather than returning to their issuer, they caromed through the economy, pushing prices higher.

While there were a number of early paper money experiments, the most well-known include the Swedish experience under an inconvertible paper standard from 1745 to 1776, the British suspension of pound convertibility from 1797 to 1821, and the U.S. Greenback era from 1861 to 1878. Each of these periods of inconvertibility was accompanied by high inflation and coincided with major wars. For instance, in the mid-1700s the Swedes had entered into several conflicts including the Seven Years War, while by the late 1700s the British were on the verge of encountering Napoleon. In the U.S., greenbacks were used by the Union to finance their war against the Confederates.

Had banknotes remained redeemable during these conflicts, it would have been impossible for governments to issue large amounts of them—they would have quickly returned to the issuer. By severing the window, many more banknotes could be put into circulation than would have otherwise been the case.

All three suspensions were only temporary as they ended with a return to specie convertibility. It was only in the 20th century that the first permanently-inconvertible standards emerged.

The fiat money era

In 1971 President Nixon removed the ability of foreigner governments to convert U.S. dollars into gold. The world was now on a permanent fiat standard.

Under both coin-based monetary systems and fully-convertible paper standards, the monetary authorities had only a little bit of control over inflation. The key influences over the price level—wear and tear, clipping and sweating, and new precious metals discoveries—were things that happened to the currency, the monetary authority having little say in the matter. When they did exercise control, it was only through policies of coin debasement or attempts to restore the standard.

Under today’s permanent fiat system, these external influences have all but disappeared. Instead of being foisted on the economy by chance, the economy’s inflation rate is now created by the monetary authority. Those who are in charge can choose to have the currency gain purchasing power over time (i.e. deflation), stay constant, or lose purchasing power over time (i.e. inflation).

In most western democracies, the monetary authorities have chosen a 1-3% inflation rate. This may seem odd, given that a constant price level is attainable. One drawback of perpetual 1-3% inflation is that people must constantly face losses on their holdings of coins and banknotes. This induces wasteful behaviour. For instance, people may choose to hold less cash than they would otherwise prefer. And they will have to constantly make trips to the bank and back to deposit banknotes in order to earn interest (this is what economists refer to as shoe leather costs). If inflation was 0%, or even -1 to -2%, the public would no longer have to worry about perpetual losses from cash and could choose to hold comfortable amounts of the stuff.

While monetary authorities understand the drawbacks of 1-3% inflation, they still choose it as a target because they see a much bigger threat in the form of sticky wages. In the simplest model of an economy, when a shock hits and demand suddenly disappears, prices fall until buyers are once again drawn back into the market. But if some of these prices are sticky, in particular the wage rate, then this downward trek in prices can never occur. Rather than reducing everyone’s salary, employers will be forced to fire workers. General unemployment and gluts of unsold inventory—or a recession—are the result.

Central bankers believe they can offset some of these unpleasant effects. While a $20 per hour wage rate may be so sticky that it can’t adjust in the face of an economic shock, an inflation rate of 1-3% means that even though the nominal value of that wage stays constant next year, its real value will have adjusted down to ~$19.60. So in the event of a shock to the economy, a central bank that targets an inflation rate of 1-3% provides the missing flexibility to wage rates, and thus promotes a quicker readjustment period.

The second reason for adopting an inflation target of 1-3% is that at these levels, short-term interest rates have typically ranged between 3-6%. After all, lenders need to make a profit, and will demand a sufficiently positive interest rate to compensate for losses from inflation. The tool that modern central bankers use to guide the price level is the overnight interest rate on balances maintained by commercial banks at the central bank. This tool becomes useless when it falls much below 0%, the effective lower bound to interest rates. Once interest rates are reduced to around -0.75%, banknotes (which yields 0%) begins to look quite attractive as an asset. Reduce interest rates a little bit more and a mass exit from bank deposits into cash will begin, the banking system imploding in the process. So by targeting an inflation rate of 1-3%, central bankers are attempting to build a big enough cushion into interest rates so that they can be sure that their main monetary policy tool has little chance of becoming useless.

And that’s why people in Western nations experience a 1-3% increase in prices each year.

What is in store for the future?

So if you had lived through the last 1000 years you’d have experienced a number of different monetary regimes, the price level dynamics different in each one. Even under commodity standards, inflation was a common occurrence. And even on a fiat standard, deflation is an entirely possible phenomenon.

In closing, will the current 1-3% inflation target that has been adopted by most Western monetary authorities ever change? In certain quarters, there is talk of central banks increasing their inflation targets to 4%- 5%. Over the last few years, interest rates have fallen close to—and even in some cases underneath—the 0% bound, muting the power of the central bank’s interest lever. If inflation was 4%, say many central bankers, then short-term rates would be much higher (say 6-7%), thus building in an even bigger cushion for subsequent interest rate reductions come the next crisis.

Alternatively, central bankers might one day decide to target an inflation rate of 0%. This would mean that short-term rates would be very low, leaving little-to-no cushion for further policy rate reductions when the next crisis hits. But there are several ways to guide interest rates far below 0%. Some economists talk of banning cash (especially high denomination notes like the ones below), for instance, or introducing a digital alternative on which a negative interest rate can be imposed. These measures would allow a central bank to reduce interest rates to -3% or -4% during a crisis without having to fret over an exodus out of bank deposits into banknotes. During these episodes with deeply negative rates, the public would flee into stocks or gold or cryptocurrencies—but this would be a sign that the desired hot potato effect was working. Having bought plenty of room to reduce interest rates into negative territory when a shock hits, central bankers could safely target 0% inflation rather than 1-3% inflation.

Finally, might we ever see inflation in the teens like we did in the 1970s? Western central bankers have exercised a large degree of independence from their political masters in the executive branch of the government over the last several decades. This has allowed them to maintain careful control over the price level. However, if some unforeseen event were to occur that led Western governments to require huge amounts of financing—say another world war—then governments may try to re-exert control over monetary policy. If so, keeping inflation under control could cease to be an important goal of the monetary authority, and the high inflation of the 1970s might return.

Popular Blog Posts by JP Koning

How Mints Will Be Affected by Surging Bullion Coin Demand

How Mints Will Be Affected by Surging Bullion Coin Demand

Banknotes and Coronavirus

Banknotes and Coronavirus

Gold Confiscation – Can It Happen Again?

Gold Confiscation – Can It Happen Again?

Eight Centuries of Interest Rates

Eight Centuries of Interest Rates

The Shrinking Window For Anonymous Exchange

The Shrinking Window For Anonymous Exchange

A New Era of Digital Gold Payment Systems?

A New Era of Digital Gold Payment Systems?

Life Under a Gold Standard

Life Under a Gold Standard

Why Are Gold & Bonds Rising Together?

Why Are Gold & Bonds Rising Together?

Does Anyone Use the IMF’s SDR?

Does Anyone Use the IMF’s SDR?

HyperBitcoinization

HyperBitcoinization