SGE Trading Surged 43% in 2016 Led by OTC & Deferred Trading

Ronan Manly

Ronan Manly 0 Comments

0 CommentsThe growing influence of the Shanghai Gold Exchange (SGE), the world’s largest physical gold exchange, is a topic familiar to many. So it is not surprising that trading volumes at the SGE continued their dramatic rise in 2016, with a record 24,338 tonnes of gold traded across physical delivery and deferred settlement contracts.

Volumes in 2016 were a staggering 43% higher vis-a-vis the 17,033 tonnes traded on the SGE during 2015, which itself was a strong year, since 2015 volumes were 84% higher than the 9,243 tonnes of gold traded at the Exchange in 2014. See “SGE Gold Trading Volume 2015 Up 84 % Y/Y Due To International Board" for more information about the 2015 volumes.

Therefore, in the space of three calendar years, the SGE has seen total trading volumes nearly triple, which is quite an achievement by any standard.

SGE Contracts: Physical Delivery and Deferred

Overall, there are 17 contracts listed on the SGE which can contribute to the trading volumes reported by the Exchange. On top of this, the trading volume generated by the SGE’s daily Shanghai Gold Benchmark Price auction (which was launched in April 2016) is also factored into the SGE’s overall trading volume.

The 17 contracts offered by the SGE cover trading in both physical products and deferred products. Five physical products trade on the Main Board of the Exchange (domestic) and a further 3 physical products trade on the Exchange’s International Board. These 8 products are as follows:

- Au50g (50 gram gold bar, 9999 fine)

- Au100g (100 gram gold bar, 9999 fine)

- Au99.99 (1 kg gold ingot, 9999 fine)

- Au99.95 (3 kg gold ingot, 9995 fine)

- Au99.5 (12.5 kg gold ingot, 995 fine)

- iAu100g (100 gram gold bar, 9999 fine)

- iAu99.99 (1 kg gold ingot, 9999 fine)

- iAu99.5 (12.5 kg gold ingot, 995 fine)

There are also 4 deferred settlement products offered by the SGE. These 4 products only trade on the Main Board. Deferred settlement contracts trade on margin, and as the name suggests, the contracts can be settled on trading day or at a later date. Two of the four are T + D contracts, the other two are T + N contracts:

T + D contract: Non-Fixed Maturity Dates

- Au(T+D) (1 kg per lot, delivery in 3 kg or 1 kg ingots)

- mAu(T+D) (100 gram per lot, delivery in 1 kg ingots) m = mini

These contracts do not have any pre-determined settlement date.

T + N contracts: Fixed Maturity Dates

- Au(T+N1) (100 gram per lot, delivery in 1 kg ingots)

- Au(T+N2) (100 gram per lot, delivery in 1 kg ingots)

The maturity date of the Au(T+N1) contract is 15 June.

The maturity date of the Au(T+N2) contract is 15 December.

In addition, 3 of the Main Board physical products (Au99.99 and Au99.95) and all 3 of the International Board products also trade bilaterally Over-the-Counter (OTC) between participants, but importantly, these OTC trades still settle on the SGE. Therefore the trading volumes of the OTC trades are still captured in the SGE systems and reported as part of SGE overall trading volumes. The SGE assigns a specific prefix P’ to these OTC products, but they are also sometimes written with a prefix of ‘OTC’. These 5 products are:

- OTC Au99.99 / PAu99.99

- OTC Au99.95 / PAu99.95

- OTCiAu99.99 / PiAu99.99

- OTCAu50g / PiAu50g

- OTCAu99.5 / PiAu99.5

Finally as mentioned, trading in the Shanghai Gold Benchmark Price auction (code SHAU) contributes to physical gold volume on the Exchange. Since SHAU was only launched on 23 April 2016, it’s volume for 2016 only represents just over 8 months worth of trading, and not a full trading year.

What traded in 2016?

In 2016, 13 of the 18 gold products (including SHAU) traded. These were: Au99.99, Au99.95, Au100g, iAu99.99, iAU100g, Au(T+D), Au(T+N1), Au(T+N2), mAu(T+D), OTC Au99.99, OTC Au99.95, OTC iAu99.99 and SHAU.

Five products did not trade at all in 2016. These 5 products were Au50g, Au995, iAu995, PiAu50g (OTC), and PiAu99.5 (OTC).

Furthermore, trading volume in Au100g was very low and trading volume in iAu100g was miniscule.

Au100g and Au50g (and their International Board versions) are designed for the retail market, but the lack of trading volume in the Au50g suggests that even retail players on the SGE shun these 50g contracts. Likewise, the 100g product does not generate much interest on the Main Board, and generates zero interest on the International Board (which is mostly frequented by institutional participants anyway).

The lack of trading volume in the Au995 specifications on both the Main Board (Au995 and PAu995(OTC)) and on the International Board (iAu995) also confirms that neither domestic participants nor international participants on the SGE are active in trading the large 12.5 kg wholesale gold bars (a.k.a. aka Good Delivery bars) which these contracts represent.

It also underscores that the Chinese central bank, the People’s Bank of China (PBoC), which like all central banks has a preference for holding wholesale 12.5 kg (400 oz) gold bars, is not an active buyer on the SGE. Instead, the PBoC prefers to buy its gold bars in Good Delivery form on international gold markets, then monetise that gold (so as to avoid it being reported in customs trade statistics). The PBoC then ships these gold bars to Beijing surreptitiously. This buying route by the PBoC has been confirmed by gold market consultancy sources in the London market.

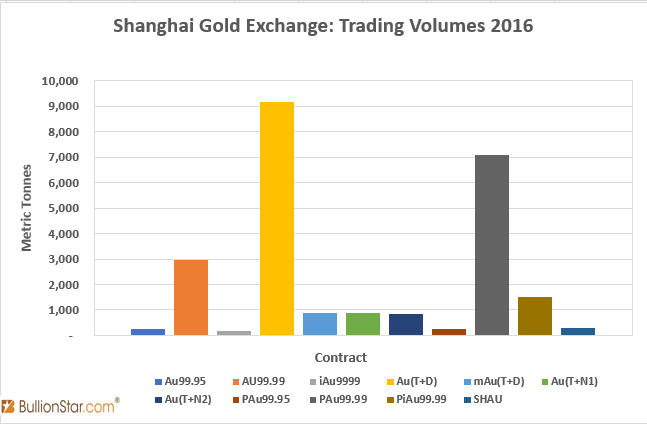

Excluding the SGE’s 100g contracts and the non-traded 50g and Au995 variants, there were 11 contracts (including SHAU) traded in 2016 which together accounted for the bulk of SGE trading volume. The individual volumes of these contracts in metric tonnes are illustrated in the following chart:

Volume was highest in the deferred Au(T+D) contract at 9186 tonnes, followed by 7080 tonnes in the physically delivered OTCAu99.99 contract. The on-exchange physically delivered Au99.99 contract registered trading volume of 2975 tonnes. Together, the Au99.99 and OTCAu99.99 generated 10,055 tonnes of physical trading which resulted in immediate physical delivery of gold. OTC trading of the iAu99.99 (i.e. PiAu99.99) generated trading volume of another 1511 tonnes of gold.

Looking at the volumes by category, there were just over 3200 tonnes traded on Exchange in the Main Board physically delivered contracts, 190 tonnes traded on Exchange in the International Board physically delivered contracts, 8850 tonnes traded OTC in physically delivered contracts, and 11,800 tonnes traded on Exchange in the Deferred contracts.

Year-on-Year Growth

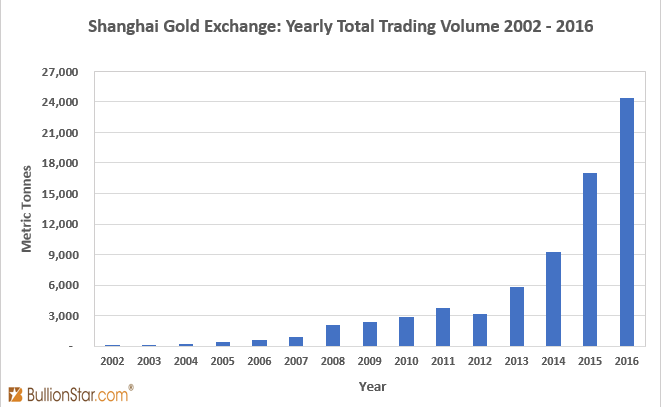

The dramatic rise in SGE trading volumes, especially since 2012, can be seen in the next chart. In 2012, SGE trading volumes totalled 3165 tonnes of gold. By 2013, this figure had risen to 5,775 tonnes of gold. In 2014, trading volumes across physically delivered and deferred gold contracts rose by 60% and hit 9243 tonnes.

During 2015, a record 17,033 tonnes of gold was traded on the SGE. This record was again surpassed in 2016 when gold trading volumes reached 24,338 tonnes, a 43% year-on-year increase. It’s important to remember that the Shanghai Gold Exchange is a physical gold exchange which has been designed to facilitate the throughput of physical gold in the vast Chinese gold market. The immediate delivery trading contracts represent real physical gold that sits in the SGE’s network of 61 precious metals vaults in 35 cities across China and where applicable, the SGEI vault in the Shanghai Pilot Free Trade Zone. Likewise, the deferred contracts can, if actioned, lead to physical delivery in the SGE vaults.

Shanghai vs London and New York

While the SGE is not the largest gold trading venue in the world by trading volume, it is the world’s largest physical gold trading venue, since the two other larger venues, London OTC and COMEX, are predominantly not physical markets. The London Gold Market predominantly trades unallocated fractionally backed paper gold claims, while the COMEX platform trades gold futures.

As of now, the London OTC gold market does not publish trading volumes. But based on London gold clearing volumes for 2016, trading volumes in the London OTC gold market are estimated to have been in excess of 1.5 million tonnes of gold (gold equivalent). However, the vast majority of this trading was in unallocated metal, a trading mechanism which is just a set of debit and credit book entries between accounts which is removed from physical delivery.

Likewise, trading volumes of the 100 ounce COMEX gold futures contract totalled 57.5 million contracts during 2016. This is equivalent to 179,000 tonnes of gold. However, in 2016, only 222 tonnes of gold were delivered within COMEX vaults based on this 179,000 tonnes of trading, Therefore 99.99% of trading did not result in the delivery of any gold.

While estimated gold trading volumes on the London OTC gold market in 2016 were about 8.4 times higher than trading volumes in the COMEX 100 oz gold futures contract, the same London trading volumes were a staggering 61.6 times higher than the 24,338 tonnes traded at the SGE. The COMEX 100 oz contract also traded 7.4 times more volume in 2016 than total SGE gold trading volumes. It should thus be apparent that the vast majority of trading on the London OTC gold market and COMEX has nothing to do with the physical gold market and is just leveraged speculation.

Will the growth in trading volumes on the SGE continue in 2017? The answer is maybe, but probably at a reduced pace. During the first quarter of 2017, SGE trading volumes totalled 5693 tonnes of gold. Annualised, this is 22,773 tonnes, which would be a slight reduction on 2016’s total. However, Q1 2016 was also the quietest trading period on the SGE, so the remainder of 2017 could see trading volumes higher than Q1 which would push 2017 SGE trading volumes slightly above the equivalent figure for 2016. But it might be too much to expect large double-digit growth in SGE volumes this year.

Popular Blog Posts by Ronan Manly

How Many Silver Bars Are in the LBMA's London Vaults?

How Many Silver Bars Are in the LBMA's London Vaults?

ECB Gold Stored in 5 Locations, Won't Disclose Gold Bar List

ECB Gold Stored in 5 Locations, Won't Disclose Gold Bar List

German Government Escalates War On Gold

German Government Escalates War On Gold

Polish Central Bank Airlifts 8,000 Gold Bars From London

Polish Central Bank Airlifts 8,000 Gold Bars From London

Quantum Leap as ABN AMRO Questions Gold Price Discovery

Quantum Leap as ABN AMRO Questions Gold Price Discovery

How Militaries Use Gold Coins as Emergency Money

How Militaries Use Gold Coins as Emergency Money

Hungary Announces 10-Fold Jump in Gold Reserves

Hungary Announces 10-Fold Jump in Gold Reserves

Planned in Advance by Central Banks: a 2020 System Reset

Planned in Advance by Central Banks: a 2020 System Reset

China’s Golden Gateway: How the SGE’s Hong Kong Vault will shake up global gold markets

China’s Golden Gateway: How the SGE’s Hong Kong Vault will shake up global gold markets