Bitcoin Backwardation, Gold Contango

JP Koning

JP Koning 7 Comments

7 CommentsPeople often refer to bitcoin as digital gold because of the similarities between the two assets. One big difference between gold and bitcoin is currently playing out in their respective futures markets. Since bitcoin futures were introduced last December by the CBOE, futures prices have often been inverted, or in backwardation. This sort of phenomenon rarely happens in gold markets, which trade normally, or in contango. Let’s explore why inversion seems to be relatively common with bitcoin and whether this will continue to be the case in the future.

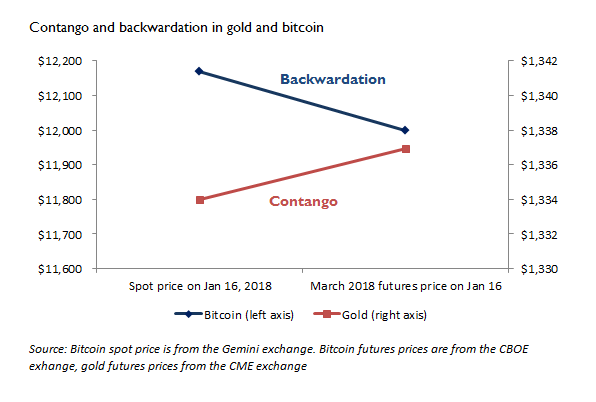

Backwardation or inversion is when future prices for a commodity lie below its current price. For instance, at lunch-time on January 16 (EST), when the current price for bitcoin was $12,170 on the Gemini bitcoin exchange, the March 2018 contract on the CBOE futures exchange was being bid at $12,000, a discount-to-spot of $170 or 1.4%.

At that very same point in time on January 16, gold’s spot price was at $1334 whereas the March futures contract was trading at $1336.90, a premium-to-spot of $2.90 or 0.2%. This is contango, or a normal-yielding market. I’ve illustrated both markets below.

In theory, the future price of a durable and easily storable commodity—say like gold, silver, and bitcoin—should always lie above the current price, or in contango. This is because storables incur holding costs, and a higher futures price is the market’s way of paying for those costs.

Contango as the fee for hoarding gold

To see how this works, let’s trek through an example. Say that you are jeweler. It is January and gold is trading at $1300/ounce, which you think is a fantastically cheap price. However, you can’t take possession of the gold right now because you have no space for it—your vault is already full. Three months from now, at the end of March, your existing inventory will have run down and you’ll have room for the stuff. Can you lock in today’s price while having someone else hold the metal for you until then? Say you strike a deal with a counterparty. They will buy the gold at today’s price of $1300 and store it in their vaults on your behalf, only delivering the stuff to you at the end of March.

Your counterparty won’t provide this service for free, they have to be compensated for the burdens of carrying the product for you. These costs include the interest payments on the loan required to buy the gold, vaulting fees, and insurance. So if gold is currently trading at $1300, and the total cost of carrying it till March is $10/ounce, then the contract you strike with the counterparty will be priced at $1310. Of this amount, $1300 allows the counterparty to pay off the face value of the loan they originally took out to buy an ounce of the yellow metal, the remaining $10 covers them for the cost of storing it, insuring it, and paying interest.

With the futures contract trading at $1310 and the current price at $1300, we say that the market is in contango. Contango is the fee—in this case $10—that buyers of gold-in-the-future pay to counterparties in order to induce these counterparties to hoard the metal on their behalf for a period of time.

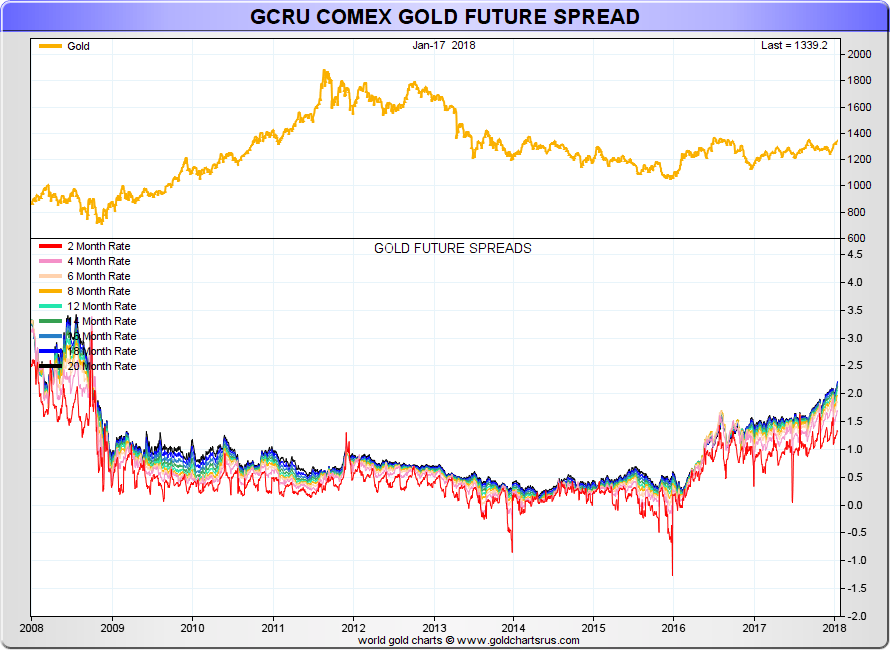

As the chart below shows, gold has spent most of the last ten years in contango. The spread, or difference between the spot price and the futures price (from 2 months out to 20 months out) almost always lies above 0%.

There have been two exceptions on the two and four-month spread (the red and pink lines), one in 2014 and another in 2016. I described the 2014 episode here. But inversions like these will only ever be fleeting, the dominant pattern in gold markets being a normal market characterized by futures prices trading above spot prices. (If you want to get into the specifics of the relationship between gold spot and future prices, Koos Jansen has written an in depth treatment here).

Backwardation as a negative fee

Compared to other commodities, gold compresses a lot of value into a small amount of space. Which means it is relatively cheap to store. For instance, ten bushels of wheat—which is worth around $40—would require an entire closet as storage space. To store $40 worth of value in the form of gold, a gram would be sufficient for the task. If we look at the data, with gold trading at $1334 and the March contract was $1336.90, the cost of storing gold in a vault, insuring it, and financing it until March is just $2.90.

Bitcoin’s $170 backwardation on January 16 meant the opposite. Counterparties who were offering to store bitcoin through to March were so desperate to provide this service that they were willing to pay a fee to do it rather than charging a fee. That anyone would take on the task of storing bitcoins for free, let alone paying to take on the burden, is especially odd given that the cost of securely “hodling" bitcoin is probably not that much less than storing gold. Commercial storage of bitcoin involves depositing private keys in vaults, much like how people keep the yellow metal safe. Consider this recent Times article that describes how the Winklevoss twins, who own a big bitcoin stake, have cut up printouts of their keys and scattered the pieces in safes all around the U.S., so if one safe is broken into the thief would still lack the full key. It is difficult to find insurers that offer bitcoin insurance products, this rarity presumably translating into fairly high insurance costs. And like gold, the financing necessary for purchasing bitcoin incurs interest expenses. So in theory, the price of bitcoin in March should permanently lies a hundred or so dollars above the spot price in order to cover these carrying costs, not below the spot price.

There are two theories for why bitcoin might be spending a disproportionate amount of time in backwardation.

1. Undeveloped market for short-selling

Imagine that a crowd of large Wall Street traders suddenly want to sell bitcoins short, but they can’t because their stringent investment mandates prohibit physical bitcoin positions. So they express their short bias by selling CBOE futures contracts which—because they are listed on a legitimate exchange—do not contravene these traders’ mandates. Bitcoin futures, which had been in contango, are abruptly driven into backwardation, a discount-to-spot.

Normally an arbitrageur would correct this discrepancy. If an arbitrageur is holding some bitcoins, the $170 discount means that the market is rewarding her not to store those bitcoins. She purchases futures at $12,000 and sells some of her bitcoins at $12,170, earning a risk free $170 profit. As long as this backwardation continues, she can keep earning profits by selling her bitcoins and buying futures until she has run out of bitcoins to sell. At which point she will try to borrow bitcoins from other people and sell them. The combined effect of her constant selling of physical bitcoins and futures buying should eventually drive the market price from its inverted state back into contango.

But if our arbitrageur can’t borrow enough bitcoin to counterbalance Wall Street’s demand to sell bitcoin short, say because lending markets are still undeveloped, then there is no way for her to fix the anomaly. Markets are stuck in backwardation. Both Kid Dynamite and Jayanth Varma have posts explaining the difficulties of arbitraging bitcoin in more detail.

An undeveloped market for borrowing and lending bitcoins is not innate to bitcoin. Presumably if bitcoin markets develop, these sorts of inefficiencies will be addressed and bitcoin—like gold—will trade more normally. That being said, bitcoin does have one innate property that can lead to backwardation: forks.

2. The omnipresent threat of forks

The second explanation for bitcoin backwardation is the ever-present threat of contentious forks.

To help understand how forks affect bitcoin futures prices let’s first look at how S&P 500 futures work, because there is an important similarity between the two assets. While storing gold is a drag, there is an upside to storing the S&P 500. The person who does the storing gets to enjoy dividend payments! As long as dividend payments are higher than the cost of paying interest on the loan originally used to buy the S&P 500 (there is no vaulting or insurance costs on equities), then it is possible to come out a net winner by carrying the S&P 500 through time.

Over the last ten years or so, S&P 500 futures have generally been inverted, with futures prices trading below spot prices. The reason for this is that short-term interest rates have generally been lower than dividend yields. Those who store equities through time on behalf of buyers of S&P 500 futures accept a discount-to-spot because the dividends they earn make up for it.

Although bitcoin doesn’t pay dividends, it does throw off an unusual set of rewards—forks. When a fork occurs, anyone who held x bitcoins now gets x newcoins in addition to their existing x bitcoins. Forks occur because participants in the Bitcoin network disagree about certain technical features of the code that runs the network. One set of actors continues to use the original code while the other modifies it, this modification leading to the creation of newcoins.

A futures market like the CBOE must define what sort of bitcoins are sufficient to settle a bitcoin futures contract. In the case of a chain split, this gets complicated. Is someone who owns a futures contract entitled to get just 1 bitcoin from the seller of a futures contract, or are the entitled to 1 bitcoin and 1 newcoin? The short answer is that the CBOE defines a ‘bitcoin’ in such a way that it does not include newcoin. So in the event of a fork, a futures seller who is storing a bitcoin in order to deliver it to a futures buyer gets to keep the newcoins for free.

Any newcoin that is created will hive off or steal a chunk of bitcoin’s original value—after all, you can’t get something for nothing. Thus, in the event of a fork, those who have bought a futures contract are now entitled to an inferior bitcoin, one that has had the value of a newcoin ripped out of it. Conversely, anyone who has been storing bitcoin on behalf of someone else no longer needs to deliver the full bitcoin when the futures contract expires; the terms of the futures contract stipulate that they get to retain a chunk of the original bitcoin in the form of a newcoin.

So to protect themselves against the potential for lost newcoins, those buying bitcoin futures will always demand a lower futures price than they would otherwise demand in a world in which bitcoin could not be forked. If the threat of a fork is deemed large enough, bitcoin futures will actually go into backwardation.

Think of it this way. Backwardation means that those storing bitcoin on behalf of others will not only do so for free, but will even pay to have the task thrust on them. This may sound odd, but if part of the calculus of storing bitcoins is that all free and valuable newcoins can be retained by the person who does the storing, then it makes sense that people will eagerly pay a fee for the right to store someone else’s bitcoins.

An example: backwardation and the failed Segwit2x fork

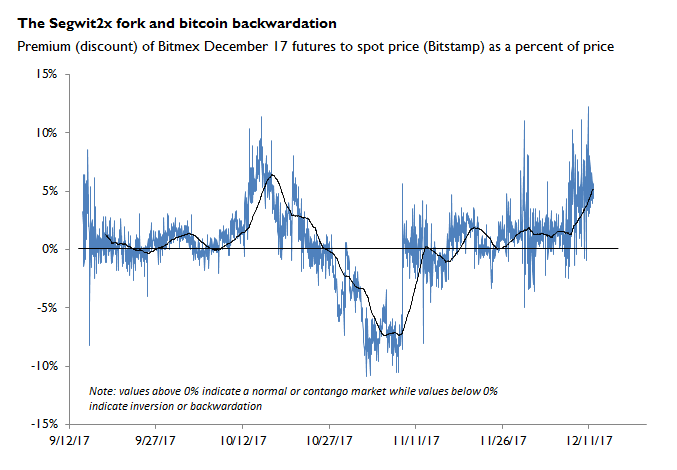

We can see an example of a fork-induced backwardation happening back in the fall of 2017, when a proposed change to Bitcoin’s source code called Segwit2x was on the verge of leading to the creation of a newcoin. Bitmex, a fledgling futures exchange, stressed to its users at the time that its December 2017 bitcoin futures contract would not include the Segwit2x newcoin.

Through late October and early November, Bitmex’s December futures contract fell to an ever deeper discount relative to the spot price of bitcoin. You can see this in the chart below. This inversion occurred in conjunction with growing odds that the upcoming newcoin’s debut would be a success and that it would ‘steal’ quite a bit of value from each already-existing bitcoin. A futures buyer who wanted to take delivery of one bitcoin in December 2017 needed to adjust for the fact that this bitcoin could have a large chunk ripped out of it by Segwit2x. Driving Bitmex’s futures contract into backwardation was the market’s way of making this adjustment.

The Segwit2x fork was abruptly cancelled on November 8, and Bitmex’s December 2017 contracts immediately reverted to contango. Since the cancellation of Segwit2x meant that existing bitcoins would not have any value sucked out of them, there was no need for futures buyers to protect themselves.

To sum up…

Because bitcoin is a young and inefficient market, borrowing bitcoins in size may be challenging. And that may explain at least some of the observed backwardation in bitcoin futures prices. But even if the market matures, Bitcoin will always be subject to the threat of contentious forks. This permanent threat gives rise to a set of forces that will always pressure the future price of bitcoin down relative to spot price. When the odds of a fork are low, these forces will not be sufficient to drive futures prices into full backwardation—they will simply push them down until they are relatively flat relative to the current price. But as the odds of a fork grow, all-out backwardation will be the result.

As for gold, there is no way it can be forked. Thus gold futures should spend far more time in contango than bitcoin futures should.

Popular Blog Posts by JP Koning

How Mints Will Be Affected by Surging Bullion Coin Demand

How Mints Will Be Affected by Surging Bullion Coin Demand

Banknotes and Coronavirus

Banknotes and Coronavirus

Gold Confiscation – Can It Happen Again?

Gold Confiscation – Can It Happen Again?

Eight Centuries of Interest Rates

Eight Centuries of Interest Rates

The Shrinking Window For Anonymous Exchange

The Shrinking Window For Anonymous Exchange

A New Era of Digital Gold Payment Systems?

A New Era of Digital Gold Payment Systems?

Why Are Gold & Bonds Rising Together?

Why Are Gold & Bonds Rising Together?

Does Anyone Use the IMF’s SDR?

Does Anyone Use the IMF’s SDR?

HyperBitcoinization

HyperBitcoinization

More On the Puzzle of Negative Interest Rates

More On the Puzzle of Negative Interest Rates