Six Months on ICE – The LBMA Gold Price

Ronan Manly

Ronan Manly 0 Comments

0 CommentsIt’s now been 6 months since the LBMA Gold Price auction, the much touted replacement to the London Gold Fixings, was launched on an ICE Benchmark Administration (IBA) platform on Friday 20 March 2015.

For anyone not au fait with the gold price auction, the LBMA Gold Price is a twice daily auction that produces the world’s most widely used gold price benchmark, which is then used as a daily pricing source in gold markets and gold products across the globe.

The 6 month anniversary of the LBMA Gold Price’s launch thus provides an opportune time to revisit a few unresolved and little-noticed aspects of this recently launched auction a.k.a. global benchmark.

Manipulative Behaviour and the FCA

From 1 April 2015, the LBMA Gold Price also became a ‘Regulated Benchmark’ of the UK’s Financial Conduct Authority (FCA) along with 6 other systemically important pricing benchmarks, namely, the LBMA Silver Price, ISDAFix, ICE Brent, WM/Reuters fx, Sonia, and Ronia. These 7 benchmarks join the infamously manipulated LIBOR in now being ‘Regulated Benchmarks’.

Manipulating or attempting to manipulate prices in a Regulated Benchmark is now a criminal offence under the Financial Services Act 2012.

Benchmark administrators and contributors must comply with the FCA’s ‘key requirements’ for a regulated benchmark which “include identifying potentially manipulative behaviour, controlling conflicts of interest, and implementing robust governance and oversight arrangements."

The specifics are set out in Chapter 8 of the FCA’s Market Conduct sourcebook (“MAR”), with the details on ‘identifying potentially manipulative behaviour’ covered in MAR 8.3.6 which says that a benchmark administrator must:

“identify breaches of its practice standards and conduct that may involve manipulation, or attempted manipulation, of the specified benchmark it administers and provide to the oversight committee of the specified benchmark timely updates of suspected breaches of practice standards and attempted manipulation“

and also:

“notify the FCA and provide all relevant information where it suspects that, in relation to the specified benchmark it administers, there has been:

(a) a material breach of the benchmark administrator’s practice standards

(b) conduct that may involve manipulation or attempted manipulation of the specified benchmark it administers; or

(c) collusion to manipulate or to attempt to manipulate the specified benchmark it administers."

and furthermore that the arrangements and procedures referred to above:

“should include (but not be limited to):

(1) carrying out statistical analysis of benchmark submissions, using other relevant market data in order to identify irregularities in benchmark submissions; and

(2) an effective whistle-blowing procedure which allows any person on an anonymous basis to alert the benchmark administrator of conduct that may involve manipulation, or attempted manipulation, of the specified benchmark it administers."

Section 91 of the UK Financial Services Act 2012 deems it a criminal offence to intentionally engage “in any course of conduct which creates a false or misleading impression as to the price or value of any investment" which creates “an impression may affect the setting of a relevant benchmark".

Recent Manipulation of Auction Starting Price

All of these FCA rules and the criminalisation of price manipulation offences sound very good in principle.

It is therefore expected that the ICE Benchmark Administration Gold Price Oversight Committee have been liaising with the FCA about the following developments in the LBMA Gold Price auction that occurred within the period between 20 March 2015 and end of May 2015, which were documented as agenda item 4, on page 2 of the ‘redacted’ minutes of the ICE Benchmark Administration Gold Price Oversight Committee held on 1 June 2015 in London:

“4. Findings since go-live: IBA shared with the Committee that:

• IBA, and some direct participants, had observed the price of futures spiking during the minutes immediately before the afternoon gold auction starts.

IBA are now de-emphasising use of the futures as a related market to consider when determining the starting price ."

The fact that IBA has deemed it necessary to follow this course of action (i.e. de-emphasise the use of futures as a starting price determinant), and the fact that some entity or entities have been pushing around futures prices as a means of influencing the LBMA Gold Price starting price suggests that nothing has changed in the gold market since the introduction of the new auction, and that the same players who were actively manipulating the gold price back in 2012 are still doing so, despite this becoming a criminal offence under UK law.

Recall that on 23 May 2014 when the FCA “fined Barclays £26 million for failings surrounding the London Gold Fixing“, in its ‘Final Notice’ explanation it included the following comments on futures prices influencing the fixing price during the protracted and manipulated afternoon fixing of 28 June 2012 :

4.12. At the start of the 28 June 2012 Gold Fixing at 3:00 p.m., the Chairman proposed an opening price of USD1,562.00. However, the proposed price quickly dropped to USD1,556.00, following a drop in the price of August COMEX Gold Futures (which was caused by significant selling in the August COMEX Gold Futures market, independent of Barclays and Mr Plunkett).

“4.18. …before the price was fixed, there were a number of further changes in the levels of buying and selling in the 28 June 2012 Gold Fixing, which coincided with an increase in the price of August COMEX Gold Futures.

4.19. As a result of these changes, the level of buying at USD1,558.50 exceeded the level of selling (155 buying/45 selling), and the proposed price was likely to move higher. Given that the price of August COMEX Gold Futures was trading around USD1,560.00 at this time, if the Chairman did move the proposed price in the 28 June 2012 Gold Fixing higher, it was likely to be to a similar price level (which was higher than the Barrier)."

You can read the entire FCA account of the saga of the 28 June 2012 afternoon fixing here, and think about the consequences and meaning of the IBA move to de-emphasis futures prices and what it signals.

Publicly Available Procedures – Not!

Which brings us to the procedures for establishing the auction starting price and subsequent prices for each round of the auction. On 28 April 2015, the IBA LBMA Gold Price web page, under ‘Auction Process’, stated that:

“The chairperson sets the starting price and the price for each round based on publicly available procedures.“

I was interested in reading these publicly available procedures, and learning about the price sources and price hierarchies used within the set of price determinants, so on 28 April 2015, I emailed the IBA communication group and asked:

Incredibly, IBA received my email that day, and then changed point 1 under ‘Auction Process’ by deleting the original reference to ‘publicly available procedures’ and by copying and pasting in the FAQ answer that I had referred to about ‘in line with current conditions and activity in the auction."

IBA then responded to my email on the same day, 28 April, without answering the question. The IBA response was:

“Please note the updated text: ‘The chairperson sets the starting price and the price for each round in line with current market conditions and the activity in the auction’. Thank you for pointing this out.“

So, not only did IBA avoid explaining the ‘publicly available procedures‘, they also covered it up and had the cheek to thank me for pointing it out to them. You can see for yourself the reactionary and firefighting tactics used by IBA in perpetuating non-transparency.

Furthermore, the fact that the original web page said that the procedures were publicly available and then they pulled it suggests that at least someone with responsibility in IBA, maybe naively, originally had been of the view that the pricing procedures were to be publicly available.

I emailed IBA again and said:

“This FAQ answer (to the question “How are the prices set for each round of the auction?) doesn’t really explain anything at all.

My question though is, apart from this one line FAQ answer, are there no more in depth ‘publicly available procedures’ available that explain how the opening price is set, what the price sources used are, what pricing hierarchy is used to select an opening price etc..?"

I’ve looked on your web site and in the FAQs and can’t find them. The only brief reference to price determination in the FAQs is that the chairperson"sets the price in line with current market conditions and activity in the auction."

To which IBA replied:

“This information is not available on our website. However, as you seem to have a few questions, would you be interested in me setting up an off the record briefing with IBA in the next few weeks?"

I did not take IBA up on that offer since I do not think that an off the record briefing is appropriate for something that should be in the public domain. It also highlights the extent to which the vast majority of the financial media are happy to use unidentified sources, off the record briefings, and quotes, and willingly act as the mouthpieces for entities that they are too scared of offending lest they will not get ‘access’ to write their next regurgitated press release for, nor get invited to that entity’s Christmas party.

Next we come to the Chairpersons.

Chairpersons Я‘Us

According to a Reuters article on 19 March about the new auction:

“‘Four ex-bankers have been appointed as chairs and will rotate in their duty in the initial six months‘, one source said."

And who are these four ex-bankers? Well, that is the billion dollar question, because, as Bulliondesk reported on 19 March in its article titled “ICE will not disclose names of chairs in new gold benchmark process“, after attending a press briefing with ICE:

“‘The names of those selected to oversee ICE’s new gold price benchmarking process will not be disclosed, Finbarr Hutcheson, president of ICE Benchmark Administration (IBA), said.

“We are keeping that anonymous – we don’t think that it’s meaningful to the marketplace to know who’s running that auction and, frankly, the more we kind of feed the story, there’s just going to be more speculation around that,” he said at a briefing at its offices here.

“There’s a legitimate desire to know but actually we don’t want this process to focus on any individual or names of people,” he added.

Not “meaningful to the marketplace to know who’s running the auction“? What sort of statement is that in a free market? If there is a legitimate desire to know, as Hutcheson concedes there is, then why hide the identities?

If anyone needs reminding, the predecessor to the LBMA Gold Price auction was a trading process which, on 23 May 2014, the UK Financial Conduct Authority (FCA) saw fit to fine Barclays £26 million “for failings surrounding the London Gold Fixing." This was also the first and only precious metals trading process in the UK ever to receive a fine from the FCA.

I would suggest that given the history of a ‘proven to have been manipulated daily gold price auction’, whose successor on launch day primarily consisted of the 4 incumbent participants that comprised the previous Gold Fixings auction (including Barclays), then it certainly is meaningful to the marketplace to know who’s running the new auction.

Bulliondesk continued:

“’We have a panel of chairpeople that we are going to use and we have internal expertise as well on that, but we are not disclosing the names of those chairmen,’ Hutcheson said. “It will rotate through the panel but we have a significant bench of available external expertise with back-up if you like.”

Hutcheson declined to name how many chairpeople are on the panel.

But if the oversight committee were to feel that it was appropriate for the names to be disclosed, this stance may change, he suggested."

And why would the oversight committee feel it to be appropriate or not to divulge the names of the chairpersons of the most important gold pricing benchmark in the world?

The Changing of the Guard

Its interesting to see how ICE Benchmark Administration’s description of the chairpersons evolved over a short period after the LBMA Gold Price auction was launched on 20 March.

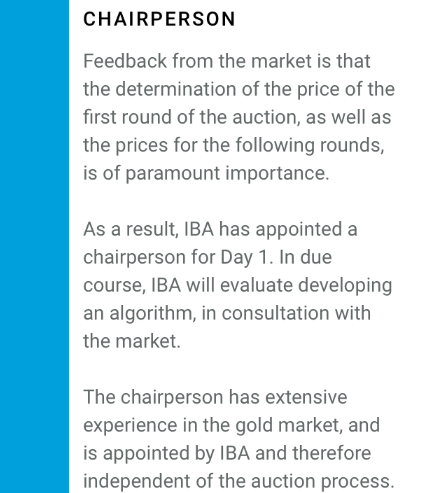

This was the initial version of the ICE IBA web site description of the Chairperson on 20 March (see screenshot 1 below also):

“The chairperson has extensive experience in the gold market, and is appointed by IBA, and therefore independent of the auction process."

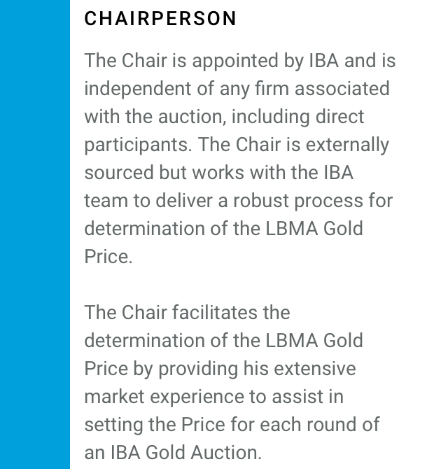

A week later, a revised, more lengthy version of the Chairperson description had appeared on the ICE IBA web site (see screenshot 2 below also):

“The Chair is appointed by IBA and is independent of any firm associated with the auction, including direct participants. The chair is externally sourced, but works with the IBA team to deliver a robust process for determination of the LBMA Gold Price."

The Chair facilitates the determination of the LBMA Gold Price by providing his extensive market experience to assist in setting the price in each round of an IBA gold auction."

By July, the second paragraph of the second version above had been changed to read:

“Both the initial and subsequent round prices are selected by the Chair using their extensive market experience and applied based on an agreed pricing framework."

So, there is a panel of chairpeople, as Hutcheson told Bulliondesk, who are 4 ‘ex-bankers’ according to Reuters, and who have ‘extensive experience in the gold market’ according to the IBA web site. So these people were previously bankers (which means investment bank staff) who gained their experience of the gold market in investment banks, and who have extensive knowledge of how a gold auction works, and since they are working with London-based IBA on a London-based daily auction, the chairpersons are either London-based or live proximate to London. And finally, according to one of the web site versions above, it’s a ‘He’ or set of ‘Hes’ so we know they are male.

And yet these same people are said to be “independent of any firm associated with the auction, including direct participants."

Given that there are now 11 direct participants in the LBMA Gold Price auction, namely, Barclays, Bank of China, Goldman Sachs, HSBC Bank USA, JPMorgan Chase Bank, Morgan Stanley, Societe Generale, Bank of Nova Scotia – ScotiaMocatta, Toronto-Dominion Bank, Standard Chartered and UBS, how could ex-bankers based in London with extensive experience of the gold market collectively be independent of all of these banks?

And that’s just the direct participants. What about all the firms associated with the auction, for example, indirect participants who route their auction orders via direct participants?

It would be interesting to hear what IBA and the LBMA define as ‘independent’. Is there any precedent on a definition of ‘independent’ for persons connected to a daily gold auction? Luckily, there is.

A number of policy documents were drawn up and introduced for the previous London gold price auction, the London Gold Fixing, in approximately mid 2014. One of these documents was a “Terms of Reference for a Supervisory Committee of the Board of the London Gold Market Fixing Limited (LPMCL)“. That document describes the composition of a supervisory committee and deems that the Board of directors of LPMCL may:

“appoint up to two independent qualified individuals to serve on the Committee. A person will be considered to be independent for the purposes of these Terms of Reference if he/she is not, and has not been at any time in the preceding year, an employee or consultant of any Member and does not otherwise have a personal interest in the fixing price or the Fixing Process."

While this document was referring to a committee whose Members were the directors of the banks running the former auction, at least there is some semblance of a definition of the concept of ‘independent‘ when applied to a gold auction.

So using that yardstick, it would be interesting to measure up the ex-banker chairpersons in the current auction as to how long exactly have they and their handler have been ‘ex’ bankers. Less than a calendar year before 20 March 2015 (i.e. 01 January 2014) would not cut it under a “has not been at any time in the preceding year, an employee or consultant of any Member" test.

And it also begs the question, why is the automated algorithm alluded to by ICE not being used in this LBMA Gold Price auction instead of a human chairperson?

Chairperson description 1

Chairperson description 2

Chairperson description version 3

The Algorithm

You will notice from the first description screenshot of the chairperson (above) that on 20 March 2015, ICE IBA stated that:

“Feedback from the market is that the price in the first round of the auction, as well as the prices for the following rounds, is of paramount importance.

As a result, BA has appointed a chairperson from Day 1. In due course, IBA will evaluate developing an algorithm in consultation with the market.“

Then notice that in the second version screenshot about the chairperson, there is no mention of any algorithm. It just vanished.

A slightly different version of the algorithm text appeared in the IBA gold price FAQ document published at launch time:

“Why are you using a Chairperson and not an algorithm for day one?

Feedback from the market is that the setting of the initial price of the first round of the auction, as well as prices for the following rounds, are important. As a result, it is appropriate to have a Chairperson on day one. In due course, IBA will consult on automating the auction process using an automated algorithm."

A point of information at this juncture. When IBA and LBMA refer to ‘the Market’ they are referring exclusively to LBMA members of the wholesale gold market and not to any of the other hundreds of thousands of global gold market participants who rely on the LBMA Gold Price benchmark as a pricing source. In fact it seems that ‘the Market’ means whatever the LBMA Management Committee decide it means.

It is also worth pointing out that many of the LBMA’s claims on consulting ‘the Market’ are just empty rhetoric, and the consultations are purely for window dressing for decisions that they have already decided on, a case in point being the EY bullion market review commissioned by the LBMA earlier this year that was announced on 27 April and wrapped up by June 2015. This is not too dissimilar to the way FIFA operates, as one correspondent pointed out.

In the case of the above ‘feedback from the market’ about wanting a chairperson, this could very well mean the 4 members of London Gold Market Fixing Limited (LGMFL) who all transitioned from the old auction to the new auction as if nothing had changed. It appears that they did not want anything to change. The old London Gold Fixing with 4 members had a chairperson (most recently Simon Weeks from Scotia) who rotated annually through the directors of (LGMFL), i.e. from Barclays, Scotia Mocatta, HSBC and SocGen.

Finbarr Hutcheson had also referred to this price calculation ‘Algorithm’ on 19 March, the day before the LBMA Gold Price launch. To quote Bulliondesk again:

“The panel of the independent chairs will be responsible for overseeing the process although ICE has indicated that it will be looking to make the process electronic in future.“

The LBMA Silver Price Algorithm

The LBMA Silver Price auction has a separate administrator, Thomson Reuters and a separate platform provider, CME Group. Thomson Reuters has this to say about the opening price on page 8 of its LBMA Silver Price methodology guide:

3.7 Starting Price

The auction platform operator (CME Benchmark Europe Ltd) is responsible for operating the LBMA Silver Price auction, including entering the initial auction price.

The initial auction price value is determined by the auction platform operator by comparing multiple Market Data sources prior to the auction opening to form a consensus price based on the individual sources of Market Data. The auction platform operator enters the initial auction price before the first round of the auction begins….

For intra-auction prices for each round, the methodology guide says that:

3.8 Manual Price Override

In exceptional circumstances, CME Benchmark Europe Ltd can overrule the automated new price of the next auction round in cases when more significant or finer changes are required. When doing so, the auction platform operator will refer to a composition of live Market Data sources while the auction is in progress.

In the LBMA Silver Price methodology, only the first round is manually input. Subsequent rounds are calculated automatically by the ‘platform’. See page 7 of the guide:

“3.4 End of Round Comparison

[bullet point 2] If the difference between the total buy and sell quantity is greater than the tolerance value, the auction platform determines that the auction is not balanced, automatically cancels orders entered in the auction round by all participants, calculates a new price, and starts a new round with the new price."

So this is different to the LBMA Gold Price where:

“The chairperson sets the starting price and the price for each round in line with current market conditions and the activity in the auction."

Conclusion

Six months after the fanfare launch on 20 March 2015, unanswered questions remain:

- How robust is the LBMA Gold Price auction mechanism, when within 3 months of launch date, IBA have to tinker with the price sources used to determine the starting price, and de-emphasise one price source due to volatile and seemingly delibrately manipulative futures price movements?

- Why does the LBMA Gold Price auction needs a human chairperson throughout the auction and the LBMA Silver Price does not?

- What happened to the plans for introducing an algorithm into the auction?

- Why have ICE gone to great lengths to prevent the public knowing the identities of the chairpersons?

- Why did ICE backtrack on a reference to ‘publicly available procedures‘ that would have explained how the starting price and round prices are determined?

- What’s going to happen when the initial six months of the chairpersons’ rotating duties run out on Monday 21 September, as Reuters alluded to back in March?

To that list some further questions could be added:

- Where are the Chinese banks ICBC and China Construction, Bank which both expressed interest in becoming direct participants in the LBMA Gold Price auction, going to join?

- Where are all the gold mining and gold refining entities that have expressed interest in being direct participants going to join, participants that the ICE auction platform can accommodate right now?

- When will the LBMA Gold Price auction move to central clearing on an exchange distinct from LMPCL’s monopoly on clearing predominantly unallocated metal?

- When will the prohibitive credit lines enforced by the LBMA be removed as as to allow other non-bank participants to directly participate in the auction without maintaining credit arrangements with the incumbent bullion banks?

These are just some of the questions which financial journalists cannot bring themselves to write about when covering this topic.

Popular Blog Posts by Ronan Manly

How Many Silver Bars Are in the LBMA's London Vaults?

How Many Silver Bars Are in the LBMA's London Vaults?

ECB Gold Stored in 5 Locations, Won't Disclose Gold Bar List

ECB Gold Stored in 5 Locations, Won't Disclose Gold Bar List

German Government Escalates War On Gold

German Government Escalates War On Gold

Polish Central Bank Airlifts 8,000 Gold Bars From London

Polish Central Bank Airlifts 8,000 Gold Bars From London

Quantum Leap as ABN AMRO Questions Gold Price Discovery

Quantum Leap as ABN AMRO Questions Gold Price Discovery

How Militaries Use Gold Coins as Emergency Money

How Militaries Use Gold Coins as Emergency Money

Hungary Announces 10-Fold Jump in Gold Reserves

Hungary Announces 10-Fold Jump in Gold Reserves

Planned in Advance by Central Banks: a 2020 System Reset

Planned in Advance by Central Banks: a 2020 System Reset

China’s Golden Gateway: How the SGE’s Hong Kong Vault will shake up global gold markets

China’s Golden Gateway: How the SGE’s Hong Kong Vault will shake up global gold markets