London Gold Fixing Website Taken Offline

Ronan Manly

Ronan Manly 0 Comments

0 Comments(Update 23/03/2015: The www.goldfixing.com website was permanently switched off in the early morning of Monday 23rd March 2015)

The last ever ‘Gold Fixing’ will take place on the afternoon of Thursday 19th March 2015 at 3.00pm.

Following the last fixing, the www.goldfixing.com website of the London Gold Market Fixing Limited will be immediately and permanently taken off-line as of close of business 19th March (i.e. the web server will be made inaccessible to web browsers).

London Gold Market Fixing Limited (LGMFL) recently confirmed to me that:

“The Gold Fixing website will be taken down completely as of the close of business on Thursday 19-3-15 and from 20-3-15 the new LBMA Gold Price will appear on their website www.lbma.org.uk. All the historical gold Fixing price data on the www.goldfixing.com website is already available on the LBMA website.“

This power-down and switching off of the web server follows a similar manoeuvre on the evening of 14th August 2014, when the web site of the London Silver Market Fixing Limited, www.silverfixing.com, was immediately and permanently switched off (without warning), leaving no trace of the live website.

By the time you read this, the www.goldfixing.com web site may be switched off.

This is very unusual behavior by the administrators of the fixing web sites and the bullion banks that run the Gold Fixing and Silver Fixing Companies to immediately make the web sites inaccessible. It’s as if the two Fixing Companies want to vanish without a trace from the internet.

The Gold Fixing website domain was first registered on 22 Dec 1999 by emilie.rivoire@rothschild.co.uk, and is listed with a tech support contact of barclaysmsosupport@sapient.com. See Domain lookup. So there is still a direct reference to Barclays in the web site and in the Sapient app, which is interesting given that Barclays was the firm that was fined by the FCA for manipulating the gold fixing in 2012 and whose trader Daniel Plunkett was also fined for the same offence.

Interestingly, the London Silver Market Fixing Limited has not been wound up, and still exists as a company, and its directors, until recently, represented HSBC, Scotia and Deutsche Bank. The only Deutsche director, New York based Eric Parker, resigned from the company last December. The HSBC and Scotia directors are still in situ.

The London Gold Market Fixing Limited also still exists as a company (obviously), and its directors are representatives of HSBC, Scotia, Barclays and SocGen, and all of these directors are still in situ. The two most recent Deutsche directors, Kevin Rodgers and James Vorley, resigned from the company on 14th May 2014, which was the same day that Deutsche Bank dropped out of the daily Gold Fixing process.

Both the Gold and Silver Fixing Companies have a registered address of c/o Hackwood Secretaries Limited, One Silk Street, London EC2Y 8HQ. Hackwood Secretaries Limited is a company belonging to Linklaters law firm. See the Linklaters ownership of Hackwood Secretaries here. Hackwood Secretaries is also the registered address of London Precious Metal Clearing Limited (LPMCL), the precious metals clearing company of Barclays, HSBC, Scotia, UBS, JP Morgan and Deutsche Bank.

Gold Price Data

From Friday 20th March 2015, the LBMA Gold Price data will appear on the London Bullion Market Association’s (LBMA) web site at http://www.lbma.org.uk/pricing-and-statistics. From 20th March, the daily fixings are being administered by ICE Benchmark Administration (IBA). There is some historical gold fixing price data already on the LBMA site, however it is less detailed than the historical gold price data which had appeared on the www.goldfixing.com web site.

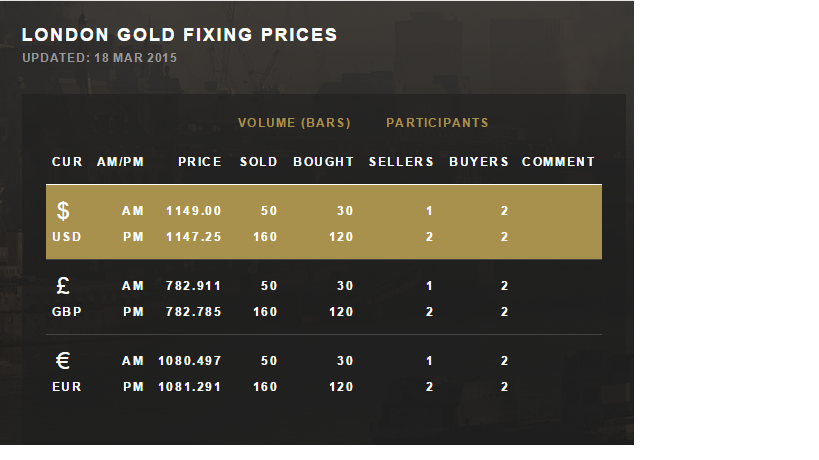

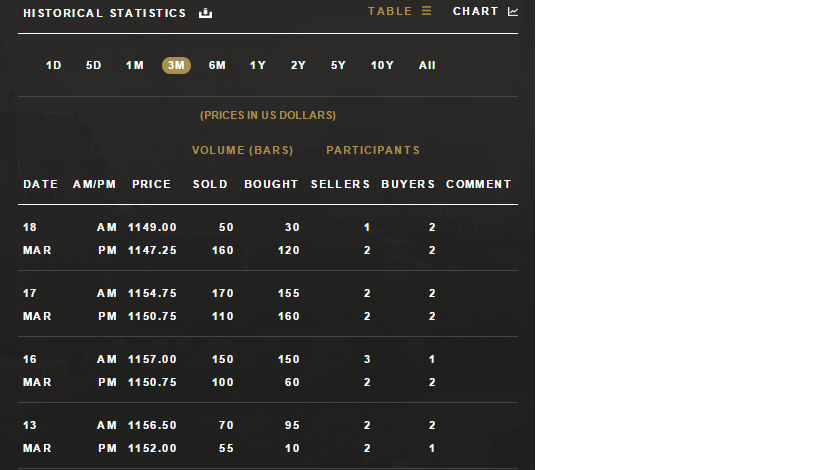

On the Gold Fixing web site, the daily and historical data both included the net volume of gold bars bought and sold at the fixing price, as well as the number of participants who had non-zero interest at the fixing price. This extra detail was added to the gold fixing website in the second half of last year. See screen shots below, both daily and historical. Historical data could also be toggled between dollars, euro and pounds.

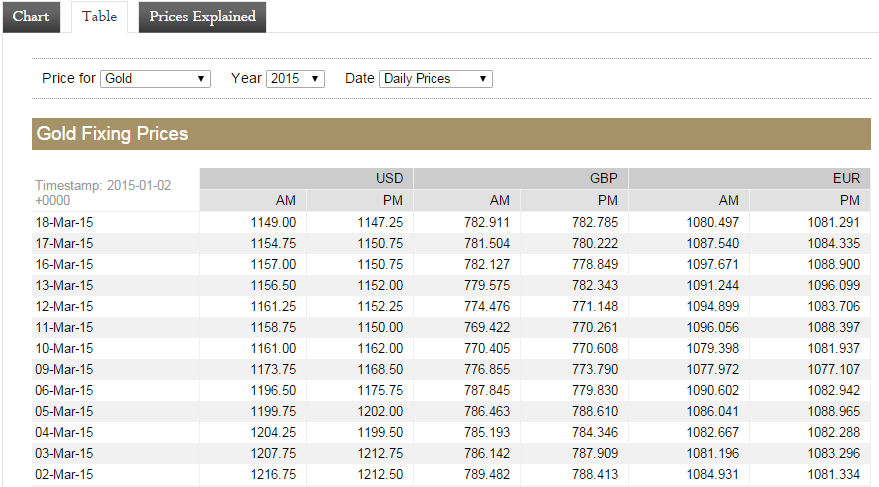

In contrast, the gold price data currently displayed on the LBMA web site does not include net volume of bars bought and sold at the fixing price, nor the number of participants declaring a buy or sell interest at the fixing price. See screenshot below.

London Gold Market Fixing Limited’s representative confirmed to me recently that all the historical Gold Fixing price data from www.goldfixing.com is already on the LBMA site. But without the volume and participant data, this claim is not entirely accurate. Adding in the volume (in bars) and the participant totals would make the data more complete.

ICE Benchmark Administration do mention a transparency report which will be published after each auction. This report will contain volume and participant numbers. It remains to be seen if this report will be published on the LBMA website. From the LBMA FAQ:

“At the end of the auction process, IBA will publish the benchmark price. IBA will also publish a Transparency Report showing for each round: the price in USD; the aggregated bid and offer volume; the number of participants; and the timings for each round."

The current gold price data disclaimer on the LBMA web site (for data up to 19th March) states that “Fixing data reproduced by kind permission of the London Gold Market Fixing Ltd" . Please refer to its website to see licensing requirements for the commercial use of the data as well as the time stamps."

Incidentally, this existing LBMA disclaimer continues with some very out of date text referring to BBA LIBOR. Now there’s a blast from the past…. “Neither the BBA LIBOR Limited, nor the BBA LIBOR Contributor Banks, nor Reuters, nor the LBMA can be held responsible for any irregularity or inaccuracy of BBA LIBOR (for more details, see “Prices Explained")."

The new LBMA Gold Price has its own disclaimer which is to be found on the new LBMA Gold Price page, and it reads “LBMA Gold Price (“Benchmark”) is owned by The London Bullion Market Association (“LBMA”), calculated and administered by IBA."

No Way Back

The reason for highlighting that the Gold Fixing web site is being taken offline is that now there will be no way to access it. This is so because it has not been archived in any meaningful way. This is so because the Gold Fixing website www.goldfixing.com has a ‘Terms’ page that appeared at the entry page which prevented the Internet Archive / Wayback Machine (www.archive.org) from archiving the site’s pages. This means that all of the non-price data on the site disappears when the web site is switched off.

Policy Documents

On the Gold Fixing web site, under a section called ‘Policy Documentation’ there were seven documents, including the Code of Conduct of the Gold Fixing company, the Terms of Reference of the gold fixing Supervisory Committee, the names of the people on the Supervisory Committee, and a document retention policy. For those interested, these documents can be found here:

Terms-of-Reference-for-the-Supervisory-Committee

List-of-Members-of-the-Supervisory-Committee

Policy-on-Complaints-and-Raising-Concerns

Under a link called ‘Trading Timeline’ there was a historical Goldfixing-Timeline-PDF.

Under a section called ‘Notices’, there was a Clarification-Document-re-Publication-of-Buy-Sell-Volumes document.

The website also contained an essay about the history of the gold fixing, which I noticed also is on another website here. On the Gold Fixing web site, there had been one small recent addition to this essay to reflect the fact that Deutsche Bank had resigned from the auction. This small addition stated “In May, 2014 Deutsche Bank resigned as a member and the line-up became: Barclays, HSBC, Bank of Nova Scotia Mocatta and Societe Generale."

The Gold Fixing web site had also prominently displayed the four Members and the most recent chairman, and the logos of the Member banks:

Shadowy Chairmen

Finally, there was an interesting section explaining “How is the Price Fixed?" which was not really explained very well elsewhere. This will be of relevance to anyone who wants to compare the old price determination process to the new one, and to gauge how much, or how little, the process has changed.

This is especially relevant because ICE Benchmark Administration will be employing a human chairperson in the new LBMA Gold Price auction to determine the opening price and the starting price of each round, as opposed to an algorithm. There will be a panel of chairpersons operating on a rotational basis.

Note that ICE and the LBMA are refusing to divulge the identity of these chairpersons.

ICE claim that this is to ‘preserve the anonymity of the auction. This is a totally bogus and unacceptable reason because without ICE confirming the identity of the chairperson, their claim that the chairperson is fully independent of the participants in the auction cannot be verified and will cause suspicion.

It is also shocking, especially since the identity of the chairperson in the Gold Fixing auctions has always been known, in every fixing from 1919 all the way through to 19th March 2015 (i.e. see the screen shots above).

The financial media should really be asking ‘Who is this Chairperson?’, and reporting on this issue.

According to Reuters, ICE has now said that there will be four chairpersons rotating over a six month period and that these will be ‘four ex-bankers‘. The identities of these four ex-bankers have not been revealed. If anything, this appears to cement the control of the incumbent bullion banks over the entire London Gold Fixing process. Reuters also says that none of the Chinese banks will be participants in the auctions.

How the Price was Fixed

The “How is the Price Fixed?" process from the Gold Fixing site can be read below:

- The fixing process is governed by a set of Rules for the Administration and Conduct of The London Gold Market Fixings (the “Fixing Rules”). The current version of the Fixing Rules, made under Article 15.01 of the London Gold Market Fixing Limited’s Articles of Association, became effective on 14 July 2014.

- The Company has a Supervisory Committee which is responsible for the oversight of the fixing process. The Company has various policies and procedures to ensure the integrity and quality of the gold fixing price which are available on the Company’s website.

- Pursuant to the Fixing Rules, representatives of the four members of the London Gold Market Fixing Limited (the “Company”) dial-in to a secure conference facility to determine the single trading price for gold at 10:30 am and 3:00 pm London time on each London business day.

- The fixing process commences with the chairman of the fixing (the “Chair”) determining and announcing the opening price of gold.

- (The opening price): The Chair shall identify the opening price. The opening price should be the prevailing US dollar mid-market price for London gold and is identified by the Chair after appropriate consideration of the prevailing spot price and the prevailing bid/offer price in the gold futures market.

- (Declaration of interests): Assuming this price, the fixing members aggregate all orders received from clients (both prior to the fix and those received in real-time during the fix) with their own proprietary trading position. Members then declare whether or not they have a net buying or selling interest or if they have no buying or selling interest at the opening price.

- (No buying or selling interest): If there is no buying or selling interest, the Chair will announce the trading price as fixed at the opening price. Similarly, if at any point during the fixing process there is no buying or selling interest at a given price, the Chair will announce the price as fixed.

- (Only buying or selling interest): If there is only buying or selling interest at the opening price and those buying or selling interests represent more than two of the fixing members (e.g. there are three sellers and one no interest), the Chair will move the opening price higher or lower.

- Alternatively, if those buying or selling interests represent two or fewer of the fixing members (e.g. two buyers and two no interests), the Chair will ask the fixing members to indicate the net quantity of gold that they are willing to buy or sell at that price.

- Fixing members must declare their net interest in increments of five gold bars and must not declare any interest of less than five bars. If the total quantity offered or wanted is 50 bars or less, the Chair will declare the price as fixed at the opening price. If the total quantity offered or wanted is more than 50 bars, the Chair will move the opening price higher or lower.

- Similarly, if at any point during the fixing process there is only buying or selling interest at a given price, the Chair will act as described in paragraphs 8 to 10 above.

- (Two way interest:) If there is two-way interest at a given price, the Chair will ask members to indicate the net quantity of gold that they are willing to buy or sell at that price.

- If supply meets demand, or the difference between supply and demand is 50 bars or less, the Chair may declare the trading price as fixed. Otherwise, the Chair will progressively move the price up or down in an attempt to meet supply and demand.

- An upwards price adjustment will cause (i) the potential fixing price to exceed some purchase order limits, which will have the effect of reducing demand as those orders drop out of the members’ net buying interests; and (ii) the potential fixing price to exceed some sale order limits, which will have the effect of increasing supply as those orders are included in the members’ net selling interests.

- A downwards price adjustment will cause (i) the potential fixing price to fall below some purchase order limits, which will have the effect of increasing demand as those orders are included in the members’ net buying interests; and (ii) the potential fixing price to fall below some sale order limits, which will have the effect of decreasing supply as those orders drop out of the members’ net selling interests.

- The Chair will repeat this adjustment procedure until supply and demand meet or the imbalance is 50 bars or less and the Chair is able to declare the price as fixed.

- (Price increments:) The fixing price must be moved in increments of at least 5 cents and in multiples of five cents during the fixing process, in all case taking account of prevailing market conditions.

- The Chair identifies price increments based on an assessment of the current price of gold in the spot and futures markets and the level of buying and selling interests declared in the fixing process.

- (The discretion): Where the Chair has been unable to exactly match supply and demand, the fixing members will pro rata the difference between supply and demand amongst themselves.

- For example, if there is more buying than selling interest (with two buyers and two sellers) and the difference is 20 bars, each buyer will reduce their buying interest by five bars and each seller will increase their selling interest by five bars. This pro rata arrangement is purely between the fixing members and only affects the amount of gold traded as between those members; it does not affect underlying customer orders.

- Where the Chair is unable, through moving the price in increments of 5 cents, to achieve an imbalance of 50 bars or less and three attempts have been made to fix the price at a particular level, the Chair may ask the other fixing members to accept an imbalance of up to 100 bars. All members must agree to this increase.

- (Flags): Throughout the fixing process members communicate with their clients who are able to cancel, increase or decrease their interest depending on price changes and the level of buying and selling interest.

- If, at any time, a member or one of its clients choose to increase, decrease or withdraw a previously declared buying or selling order, that member may require a short pause to recalculate its net interest. In these circumstances the member may call a “flag” which brings the fixing process to a temporary halt. The gold price cannot be declared by the Chair during such a pause.

- The term flag is a reference to when the fixing members would meet in a single place to determine the gold trading price. When a member required a pause they would raise a small flag. The flag would be lowered again when they were ready to proceed with the fixing process.

- (Execution): Following the determination of the fixing price, the members will execute trades for gold amongst themselves at 15 cents above the fixing price and in the amounts offered during the fixing process.

- The Chair will specify the trades that should be executed between the members. The Fixing Rules specify that the largest seller’s order is filled first by matching that order with the largest buyer’s order, with members’ orders then being matched in descending order size.

- Settlement takes place two London/New York business days after the fix. Execution of trades between the members does not affect any arrangements agreed between the members and their clients.

- (Determination of the fixing price in euros and pounds sterling): The trading price is published by the Company in three currencies: pounds sterling, euros and US dollars. The fixing process takes place in US dollars. Once the trading price is fixed, the Chair will provide the equivalent trading prices in pounds sterling and euros. The Chair uses the then prevailing exchange rates published on Bloomberg or Reuters for this purpose.

- (Publication of the fixing prices): Immediately following a fixing, the Chair posts the fixing price, the time at which the price was fixed, the final buy/sell volume figures on an anonymised basis and the basis on which the price was fixed if the discretion was increased from 50 bars, on the Company’s website. The Chair also sends an email confirmation of the fixing price and the time that the price was fixed to the other members.

- The published price is the price for one troy ounce (just over 30 grams) of gold delivered in London in the form of LBMA Good Delivery Bars (approximately 400 troy ounces each).

Popular Blog Posts by Ronan Manly

How Many Silver Bars Are in the LBMA's London Vaults?

How Many Silver Bars Are in the LBMA's London Vaults?

ECB Gold Stored in 5 Locations, Won't Disclose Gold Bar List

ECB Gold Stored in 5 Locations, Won't Disclose Gold Bar List

German Government Escalates War On Gold

German Government Escalates War On Gold

Polish Central Bank Airlifts 8,000 Gold Bars From London

Polish Central Bank Airlifts 8,000 Gold Bars From London

Quantum Leap as ABN AMRO Questions Gold Price Discovery

Quantum Leap as ABN AMRO Questions Gold Price Discovery

How Militaries Use Gold Coins as Emergency Money

How Militaries Use Gold Coins as Emergency Money

Hungary Announces 10-Fold Jump in Gold Reserves

Hungary Announces 10-Fold Jump in Gold Reserves

Planned in Advance by Central Banks: a 2020 System Reset

Planned in Advance by Central Banks: a 2020 System Reset

China’s Golden Gateway: How the SGE’s Hong Kong Vault will shake up global gold markets

China’s Golden Gateway: How the SGE’s Hong Kong Vault will shake up global gold markets