IMF Gold Sales: Where 'Transparency' Means 'Secrecy'

Ronan Manly

Ronan Manly 0 Comments

0 CommentsWelcome to the twilight zone of IMF gold sales, where transparency really means secrecy, where on-market is off-market, and where IMF gold sales documents remain indefinitely “classified" and out of public view due to the “sensitivity of the subject matter".

Off and On Market

Between October 2009 and December 2010, the International Monetary Fund (IMF) claims to have sold a total of 403.3 tonnes of gold at market prices using a combination of ‘off-market’ sales and ‘on-market’ sales. ‘Off-market’ gold sales are gold sales to either central banks or other official sector gold holders that are executed directly between the parties, facilitated by an intermediary. For now, we will park the definition of ‘on-market’ gold sales, since as you will see below, IMF ‘on-market’ gold sales in reality are nothing like the wording used to describe them. In total, this 403.3 tonnes of gold was purportedly sold so as to boost IMF financing arrangements as well as to facilitate IMF concessional lending to the world’s poorest countries. As per its Articles of Agreement, IMF gold sales have to be executed at market prices.

Critically, the IMF claimed on numerous occasions before, during and after this 15-month sales period that its gold sales process would be ‘Transparent’. In fact, the concept of transparency was wheeled out by the IMF so often in reference to these gold sales, that it became something of a mantra. As we will see below, there was and is nothing transparent about the IMF’s gold sales process, but most importantly, the IMF blocked and continues to block access to crucial IMF board documents and papers that would provide some level of transparency about these gold sales.

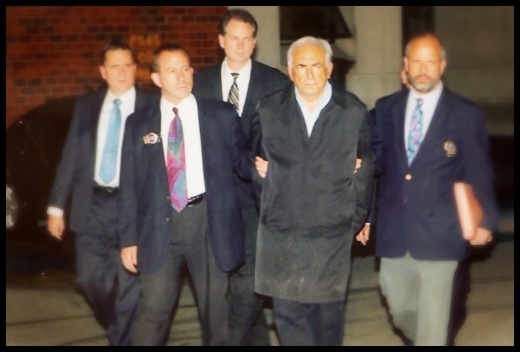

Strauss-Kahn – Yes, that guy

On 18 September 2009, the IMF announced that its Executive Board had approved the sale of 403.3 metric tonnes of gold. Prior to these sales, the IMF officially claimed to hold 3217.3 tonnes of gold. Commenting on the gold sales announcement, notable party attendee and then IMF Managing Director Dominique Strauss-Kahn stated:

“These sales will be conducted in a responsible and transparent manner that avoids disruption of the gold market.”

The same IMF announcement on 18 September 2009 also stated that:

“As one of the elements of transparency, the Fund will inform markets before any on-market sales commence. In addition, the Fund will report regularly to the public on the progress with the gold sales.”

On 2 November 2009, the IMF announced the first transaction in its gold sales process, claiming that it had sold 200 tonnes of gold to the Reserve Bank of India (RBI) in what it called an ‘off-market’ transaction. This transaction was said to have been executed over 10 trading days between Monday 19 November to Friday 30 November with sales transactions priced each day at market prices prevailing on that day. On average, the 200 tonne sales transaction would amount to 20 tonnes per day over a 10 day trading period.

Note that the Reserve Bank of India revealed in 2013 that this 200 tonne gold purchase had merely been a book entry transfer, and that the purchased gold was accessible for use in a US Dollar – Gold swap, thereby suggesting that the IMF-RBI transaction was executed for gold held at the Bank of England in London, which is the only major trading center for gold-USD swaps. As a Hindu Business Line article stated in August 2013:

“According to RBI sources, the gold that India bought never came into the country as the transaction was only a book entry. The gold was purchased for $6.7 billion, in cash.”

“The Reserve Bank of India bought 200 tonnes of gold for $1,045 an ounce from the IMF four years ago. The Government can swap it for US dollars,” said [LBMA Chairman David] Gornall."

Two weeks after the Indian purchase announcement in November 2009, another but far smaller off-market sale was announced by the IMF on 16 November 2009, this time a sale of 2 tonnes of gold to the Bank of Mauritius (the Mauritian central bank), said to have been executed on 11 November 2009. Another two weeks after this, on 25 November 2009, the IMF announced a third official sector sales transaction, this time a sale of 10 tonnes of gold to the Central Bank of Sri Lanka.

Overall, these 3 sales transactions, to the Reserve Bank of India, Bank of Mauritius and the Central Bank of Sri Lanka, totalled 212 tonnes of gold, and brought the IMF’s remaining official gold holdings down to 3005.3 tonnes at the end of 2009, leaving 191.3 tonnes of the 403.3 tonnes remaining to sell. All 3 of the above announcements by the IMF were accompanied by the following statement:

“The Fund will inform markets before any on-market sales commence, and will report regularly to the public on progress with the gold sales.”

For nearly 3 months from late November 2009, there were no other developments with the IMF’s gold sales until 17 February 2010, at which point the IMF announced that it was to begin the ‘on-market’ portion of its gold sales program. At this stage you might be wondering what the IMF’s on-market gold sales consisted of, which ‘market’ it referred to, how were the sales marketed, who the buyers were, and who executed the sales transactions. You would not be alone in wondering about these and many other related questions.

The IMF’s press releases of 17 February 2010, titled ‘IMF to Begin On-Market Sales of Gold’ was bereft of information and merely stated that the IMF would “shortly initiate the on-market phase of its gold sales program” following “the approach adopted successfully by the central banks participating in the Central Bank Gold Agreement“, and that the sales would be “conducted in a phased manner over time”. The third Central Bank Gold Agreement (CBGA) ran from September 2009 to September 2014. These CBGA’s, which have been running since September 1999, ostensibly claim to support and not disrupt the gold market but in reality have, in their entirety, been highly secretive operations where vast amounts of central bank and official sector gold is channeled via the BIS to unspecified buyers in the bullion banks or central bank space, with the operations having all the hallmarks of gold price stabilization operations, and/or official sector gold redistribution between the world’s developed and emerging market central banks.

The February 2010 announcement also made the misleading claim that “the IMF will continue to provide regular updates on progress with the gold sales through its normal reporting channels". These regular updates have never happened.

An article titled “IMF ‘On-Market’ Gold Sales Move Ahead” in the ‘IMF Survey Magazine’, also dated 17 February 2010 reiterated this spurious transparency claim:

“Transparent approach

The IMF publicly announced each official sale shortly after the transaction was concluded. A high degree of transparency will continue during the sales of gold on the market, in order to assure markets that the sales are being conducted in a responsible manner.”

However, following this February 2010 lip service to transparency, there were no direct updates from the IMF exclusively about the on-market gold sales, even after the entire gold sales program had completed in December 2010.

One further IMF ‘off-market’ gold sale transaction was announced on 9 September 2010. This was a sale of 10 tonnes of gold to Bangladesh Bank (the Bangladeshi central bank) with the transaction said to have been executed on 7 September 2010. Adding this 10 tonnes to the previous 212 tonnes of off-market sales meant that 222 tonnes of the 403.3 tonne total was sold to central banks, with the remaining 181.3 tonnes sold via ‘on-market’ transactions. The Bangladesh announcement was notable in that it also revealed that “as of end July 2010, a further 88.3 metric tons had been sold under the on-market sales announced in February 2010". The addition of Bangladesh to the off-market buyer list that already consisted of India, Sri Lanka and Mauritius also resulted in the quite bizarre situation where the only off-market buyers of IMF comprised 4 countries that have extremely close historical, political, cultural and economic connections with each other. Three of these countries, India, Bangladesh and Sri Lanka, are represented at the IMF by the same Executive Director, who from November 2009 was Arvind Virmani, so their buying decisions were most likely coordinated through Virmani and probably through the Reserve Bank of India as well.

On 21 December 2010, the IMF issued a press release titled ‘IMF Concludes Gold Sales’ which stated:

“The International Monetary Fund (IMF) announced today the conclusion of the limited sales program covering 403.3 metric tons of gold that was approved by the Executive Board in September 2009.”

“The gold sales were conducted under modalities to safeguard against disruption of the gold market. All gold sales were at market prices, including direct sales to official holders.”

‘Modalities’ in this context just means the attributes of the sales including the approach to the gold sales, i.e. the sales strategy. This brief announcement on 21 December 2010 was again bereft of any factual information such as which market was used for the ‘on-market’ gold sales, the identity of executing brokers, the identity of counterparties, transaction dates, settlement dates / deferred settlement dates, method of sale, information on whether bullion was actually transferred between parties, publication of weight lists, and other standard sales transaction details. Contrast this secrecy to the 1976 -1980 IMF gold sales which were conducted by a very public series auction, and which were covered in minute details by the financial publications of the time.

As usual with its treatment of official sector gold transactions, the World Gold Council’s Gold Demand Trends report, in this case its Q4 2010 report, was absolutely useless as a source of information about the IMF gold sales beyond regurgitating the press release details, and there was no discussion on how the gold was sold, who the agent was, who the buyers were etc etc.

Lip Service to Transparency

When the IMF’s ‘on-market’ sales of 191.3 tonnes of gold commenced in February – March 2010, there were attempts from various quarters to try to ascertain actual details of the sales process. Canadian investment head Eric Sprott even expressed interest in purchasing the entire 191.3 tonnes on behalf of the then newly IPO’d Sprott Physical Gold ETF. However, Sprott’s attempts to purchase the gold were refused by the IMF, and related media queries attempting to clarify the actual sales process following the IMF’s blockade of Sprott were rebuffed by the IMF.

A Business Insider article from 6 April 2010, written by Vince Veneziani and titled “Sorry Eric Sprott, There’s No Way You’re Buying Gold From The IMF”, lays out the background to this bizarre stone-walling and lack of cooperation by the IMF. Business Insider spoke to Alistair Thomson, the then external relations officer at the IMF (now Deputy Chief of Internal Communications, IMF), and asked Thomson why Sprott could not purchase the gold that was supposedly available in the ‘on-market’ sales. Thomson’s reply is summarised below:

“The IMF is only selling gold though a qualified agent. There is only one of these agents at the moment and due to the nature of the gold market, they won’t reveal who or what that agent is.”

“Sprott can’t buy the gold directly because they do not deal with institutional clients like hedge funds, pension funds, etc. The only buyers can be central bankers and sovereign nations, that sort of thing.”

The IMF board agreed months ago how they wanted to approach the sale of the gold. Sprott is welcome to buy from central banks who have bought from the IMF, but not from the IMF directly."

While this initial response from the IMF’s Alistair Thomson contradicted the entire expectation of the global gold market which had been earlier led to believe that the ‘on-market’ gold sales were just that, sales of gold to the market, on the market, Thomson’s reply did reveal that the IMF’s ‘on-market’ gold sales appeared to be merely an exercise in using an agent, most likely the Bank for International Settlements (BIS) gold trading desk, to transfer IMF gold to a central bank or central banks that wished to remain anonymous, and not go through the publicity of the ‘off-market’ transfer process.

Although, as per usual, the servile and useless mainstream media failed to pick up on this story, the IMF’s unsatisfactory and contradictory response was deftly dissected by Chris Powell of GATA in a dispatch, also dated 6 April 2010. After discussing the IMF’s initial reply with Eric Sprott and GATA, Business Insider’s Vince Veneziani then went back to IMF spokesman Alistair Thomson with a series of reasonable and totally legitimate questions about the ‘on-market’ gold sales process.

Veneziani’s questions to the IMF are documented in his follow-up Business Insider article titled “Five Questions About Gold The IMF Refuses To Answer”, dated 27 April 2010. These questions included:

- What are the incentives for the IMF not to sell gold on the open market or to investors, be it institutional or retail?

- Did gold physically change hands with the banks you have sold to so far or was the transaction basically bookkeeping stuff (the IMF still holds the physical gold in this case)?

- Are there available records on the actual serial numbers of bullion? How is the gold at the IMF tracked and accounted for?

- Does IMF support a need for total transparency in the sale of gold despite the effects it could have on various markets?

Shockingly, Alistair Thomson, supposedly the IMF press officer responsible for answering the public’s queries about IMF finances (including gold sales), arrogantly and ignorantly refused to answer any of the questions, replying:

“I looked through your message; we don’t have anything more for you on this.”

Another example of the world of IMF transparency, where black is white and white is black, and where press officers who have formerly worked in presstitute financial media organisations such as Thomson Reuters fit in nicely to the IMF’s culture of aloofness, status quo protection, and lack of accountability to the public.

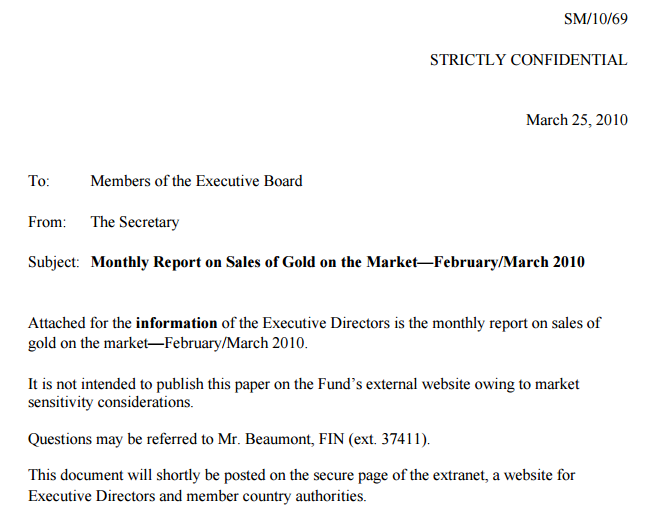

Monthly Report on Sales of Gold on the Market

Fast forward to July 2015. While searching for documents in the IMF online archives related to these gold sales, I found 3 documents dated 2010, titled “Monthly Report on Sales of Gold on the Market“. Specifically, the 3 documents are as follows (click on links to open):

- Monthly Report on Sales of Gold on the Market – February/March 2010 SM/10/69

- Monthly Report on Sales of Gold on the Market – March/April 2010 SM/10/102

- Monthly Report on Sales of Gold on the Market – April/May 2010 SM/10/139

Each of these 3 documents is defined by the IMF as a Staff Memorandum (SM), which are classified as ‘Executive Board Documents’ under its disclosure policy. The IMF Executive Board consists of 24 directors in addition to the IMF Managing Director, who was in 2009 the aforementioned Dominique Strauss-Kahn. According to the IMF’s Executive Board synopsis web page, the board “carries out its work largely on the basis of papers prepared by IMF management and staff."

The most interesting observation about these 3 documents, apart from their contents which we’ll see below, is the fact that only 3 of these documents are accessible in the IMF archives, i.e. the documents only run up to May 2010, and do not include similar documents covering the remainder of the ‘on-market’ sales period (i.e. May – December 2010). Therefore there are 7 additional monthly reports missing from the archives. That there are additional documents that have not been published was confirmed to me by IMF Archives staff – see below.

Each of the 3 reports is only 3 pages long, and each report follows a similar format. The first report spans February – March 2010, specifically from 18 February 2010 to 17 March 2010, and covers the following:

“summarizes developments in the first month of the on-market sales, covering market developments, quantities sold and average prices realized, and a comparison with widely used benchmarks, i.e., the average of London gold market fixings“

‘Market developments’ refers to a brief summary in graphical chart of the London fixing prices in US Dollars over the period in question. Quantities sold and the currency composition of sales are notable:

Sales Volume and Proceeds: A total of 515,976.638 troy ounces (16.05 metric tons) of gold was sold during the period February 18 to March 17. These sales generated proceeds of SDR 376.13 million (US$576.04 million), based on the Fund’s representative exchange rates prevailing on the day of each sale transaction.

Currency Composition of Proceeds: Sales were conducted in the four currencies included in the SDR valuation basket …., with the intention of broadly reflecting the relative quota shares of these currencies over the course of the sales program.

The 4 currencies in which the sales were conducted during the first month were USD, EUR, GBP and JPY. See table 1 in the document for more information. Perhaps the most revealing point in each document is the confirmation of the use of an agent and specifically an arrangement that the sales prices included a premium paid by the agent:

Sales Prices compared with Benchmarks: The sales were implemented as specified in the agreement with the agent. Sales were conducted at prices incorporating a premium paid by the agent over the London gold fixing, and for sales settled in currencies other than the U.S. dollar, the sales price also reflects market exchange rates at the time of the London gold fixings (10:30 am and 3:00 pm GMT), net of a cost margin.

The use of a premium over the London fixing price is very revealing because this selling strategy, where the agent paid a premium over the average London gold fixing price, is identical to the sales arrangement which the Swiss National Bank (SNB) agreed with the Bank for International Settlements (BIS) when the BIS acted as sales agent for SNB gold sales over the period May 2000 to March 2001.

As Philipp Hildebrand, ex-governor of the SNB, revealed in 2005 when discussing the SNB gold sales strategy that had been used in 2000-2001:

“At the outset, the SNB decided to use the BIS as its selling agent. Between May 2000 and March 2001, the BIS sold 220 tonnes on behalf of the SNB. For the first 120 tonnes, the SNB paid the BIS a fixed commission while the performance risk resided with the SNB. For the next 100 tonnes, the BIS agreed to pay the average price of the AM and PM London gold fixing plus a small fixed premium.“

My conclusion is therefore that the IMF also used the Bank for International Settlements in Basel, Switzerland as selling agent for its ‘on-market’ gold sales over the period February to December 2010, with the sales benchmarked to average London fixing prices in the London Gold Market.

The pertinent details for the IMF’s March – April sales document are as follows:

“A total of 516,010.977 troy ounces (16.05 metric tons) of gold was sold during the period March 18 to April 16."

“Sales were conducted in three of the four currencies included in the SDR valuation basket" i.e. USD, EUR and JPY"

The relevant details from the April – May sales document are as follows:

“A total of 490,194.747 troy ounces (15.25 metric tons) of gold was sold during the period April 19 to May 18, 2010; no sales were conducted during the last two business days in April, owing to end of financial year audit considerations."

“Sales were conducted in three of the four currencies included in the SDR valuation basket" i.e. USD, GBP and JPY

Purely a Pricing Exercise?

The entire ‘on-market’ gold sales program of 181.3 tonnes may well have been just a pricing exercise by the Bank for International Settlements gold trading desk to determine the market prices at which to execute the transfers, with the gold transferring ownership after the event as book entry transfers at the Bank of England in the same manner as was applied to the Indian ‘off-market’ purchase of 200 tonnes.

Taking the sales quantities in the 3 published monthly reports, and incorporating quarterly IMF gold holdings time series data from the World Gold Council, it’s possible to calculate how much gold was ‘sold’ each single day over the entire ‘on-market’ gold sales program. As it turns out, for much of the program’s duration, identical quantities of gold were sold each and every day. The ‘on-market’ program commenced on 18 February 2010. Between 18 February and 17 March, which was a period of 20 trading days in the London gold market, the agent sold 515,976.638 troy ounces (16.05 metric tons) of gold. Between 18 March and 16 April, which was also a trading period of 20 trading days (even after factoring in 2 Easter bank holidays), the agent sold a practically identical quantity of 516,010.977 troy ounces (also 16.05 metric tons). This is a daily sales rate of 25,800 ozs or 0.8025 tonnes per trading day over these 40 trading days.

During the period from 19 April to 18 May 2010, which was 19 trading days excluding the 3rd May UK bank holiday and excluding the last 2 trading days of April on which the IMF program didn’t trade, the agent sold 490,194.747 troy ounces (15.25 metric tons) of gold, which again is…wait for it… 0.8025 tonnes and 25,800 ozs per day (0.8025 * 19 = 15.2475 tonnes & 25,800 * 19 = 490,200 ozs).

Following the combined Indian, Mauritian, and Sri Lankan ‘off-market’ purchases of 212 tonnes during Q4 2009, the IMF’s gold holdings stood at 3,005.32 tonnes at the end of 2009. Based on World Gold Council (WGC) quarterly data of world official gold reserves, the IMF’s gold holdings then decreased as follows during 2010:

– 24.08 MT (Q1) – 47.34 MT (Q2) – 67.66 MT (Q3) – 52.2 MT (Q4) = – 191.28 metric tonnes (MT)

…resulting in total remaining gold holdings of 2,814.04 tonnes at the end of 2010, an IMF gold holdings figure which remains unchanged to this day.

These WGC figures tally with the IMF monthly report figures. For example, the IMF says that 16.05 tonnes was sold up to and including 17 March, and with another 10 trading days in March 2010, a further 8.205 tonnes (0.8025 daily sales * 10) was sold by the end of March, giving total Q1 sales of 16.05 + 8.025 = 24.075 tonnes, which is identical to the WGC quarterly change figure. The IMF was active on 59 trading days in Q2 during which it sold 47.34 tonnes, which…wait for it…was an average of 0.8024 tonnes per day (47.34 / 59 = 0.8024).

Therefore, over Q1 and Q2 2010 (i.e. between February and the end of June 2010), the ‘on-market’ sales program sold 71.42 tonnes at a consistent ~ 0.8025 tonnes daily rate. This would suggest an algorithmic program trade which offered identical quantities each and every day, or more likely just priced these quantities so as to arrive at a sales consideration amount so that the IMF would receive ‘market prices’ for its gold. Recall that IMF gold has to be sold at market prices according to the Fund’s Articles of Agreement.

Given that 88.3 tonnes had been sold ‘on-market’ by the end of July 2010 as the IMF revealed in its Bangladesh announcement, we can infer that 16.88 tonnes was sold ‘on-market’ during July 2010. This 16.88 tonne sale in July was actually at a slightly lower pace than previous months since there were 22 trading days in July 2010, however the figure was chosen due to the following: With 191.3 tonnes on sale at the outset of the ‘on-market’ program, and 71.42 tonnes sold by the end of June, this left 119.88 tonnes to sell at the end of June. Whoever was choosing the monthly sales quantities wanted to finish July with a round figure of 103 tonnes, and so chose 16.88 tonnes to sell in July (i.e. 119.88 – 16.88 = 103 tonnes). Subtracting the 10 tonnes that Bangladesh bought in September 2010 (which would have been also factored in at that time) left a round 93 tonnes (2.999 million ozs) to sell as of the beginning of August.

The Q3 2010 sales of 67.66 tonnes comprised the 10 tonne ‘off-market’ sale to Bangladesh on 7 September and 57.66 tonnes of on-market sales. Given 16.88 tonnes sold in on-market sales in July, there was therefore 40.78 tonnes sold over August – September, or an average of 20.39 tonnes in each of August and September (which represented a combined 43 trading days). Overall, there were 65 trading days in Q3 and 58 trading days in Q4 (assuming that the sales wrapped up on 21 December as per the IMF announcement). From the beginning of August to the 21 December, a period of 101 trading days, the IMF sold the remaining 93 tonnes, which would be a daily sales pace of 0.93 tonnes per day.

So overall, the IMF’s 403.3 tonnes of gold sales between November 2009 and December 2010 consisted of 222 tonnes sold ‘off-market’ to India, Bangladesh, Sri lanka, and Mauritius, 88.3 tonnes sold ‘on-market’ between February and July 2010, and 93 tonnes sold ‘on-market’ between August and December 2010′.

Given that the IMF’s 4 gold depositories are the Federal Reserve Bank of New York, the Bank of England in London, the Banque de France in Paris and the Reserve Bank of India in Nagpur India, and given that the IMF gold in New York is mostly in the form of US Assay Office melts, and the gold in Nagpur is a hodgepodge of mostly low quality old gold (read non-good delivery gold), then it would be logical for the IMF to sell some of its good delivery gold which is stored in London (which, until at least the late 1970s, was predominantly held in the form of Rand Refinery 400 oz gold bars), or even in Paris, since the Banque de France has been engaged in an ongoing program of upgrading the old US Assay office gold bars in its custody to good delivery bars.

As the Banque de France’s Alexandre Gautier commented in his 2013 speech to the LBMA annual conference in Rome:

“Our bars are not all LGD [London Good Delivery quality], but we have an ongoing improvement programme.”

This Banque de France gold bar upgrading program was also confirmed in February 2011 in a National Geographic Magazine article which stated:

“Buyers don’t want the beat-up American gold. In a nearby room pallets of it are being packed up and shipped to an undisclosed location, where the bars will be melted down and recast in prettier forms."

Top Secret Foot Notes

There are 2 interesting footnotes on page 1 or each of the 3 above documents. The first footnote states that ‘The Executive Board was briefed on the plans for on-market sales prior to the announcement’, the announcement in question being the IMF’s 17 February 2010 announcement IMF to Begin On-Market Sales of Gold.

The second footnote, which is a footnote to a sales process and sales performance summary, refers to 2 further IMF papers as follows: “Modalities for Limited Sales of Gold by the Fund (SM/09/243, 9/4/09) and DEC/14425-(09/97), 9/18/09“.

As mentioned above, SM are Staff Memorandums which are classed under Executive Board Documents. DEC series document are ‘Text of Board Decisions’ (hence the DEC) and these documents are also deemed to be Executive Board Documents. After searching for both of these documents (SM/09/243 and DEC/14425-(09/97)) in the IMF archives, it became apparent that they were not there, i.e. they were not returned and not retrievable under IMF archive search results.

This was surprisingly since the IMF claims to have what it calls its “IMF Open Archives Policy", part of which is Article IX, Section 5, which is the “Review of the Fund’s Transparency Policy—Archives Policy“. This policy, prepared by the IMF Legal Department includes the following:

Access will be given as follows:

- 2. (i) Executive Board documents that are over 3 years old

(ii) Minutes of Executive Board meetings that are over 5 years old;

(iv) Other documentary materials maintained in Fund archives over 20 years old.

- 3. Access to Fund documents specified in paragraph 2 above that are classified as “Secret” or “Strictly Confidential” as of the date of this Decision will be granted only upon the Managing Director’s consent to their declassification. It is understood that this consent will be granted in all instances but those for which, despite the passage of time, it is determined that the material remains highly confidential or sensitive.

Given that the 2 above gold sales documents, as well as 7 other monthly reports about ‘on-market’ gold sales were missing from the archives, but all the while the IMF claimed its on-market gold sales to be “Transparent", the next logical step was to contact the IMF Archives people and seek explanations. What follows below is the correspondence I had with the IMF Archives staff. The IMF Archives staff were very helpful and their responses were merely communicating what they had found in their systems or had been told ‘from above’. My questions and emails are in blue text. The IMF replies are in red text. My first set of queries were about the SM/09/243 and DEC/14425 documents:

02 August 2015: My first question

Hello Archives,

Hello Archives,

3 August: IMF Archives reply

Thank you for contacting the IMF Archives. Both documents you are referring to in your recent communication, SM/09/243 and DEC/14425, are not available to the public. Please visit our website to consult on IMF Policy on Access to the Archives.

3 August: me

Can you clarify why these documents are not available to the public? i.e. have they received a certain classification?

4 August: IMF Archives

You are absolutely right, despite the time rule, these two documents are still closed because of the information security classification. We hope it answers your question.

4 August: me

Thanks for answer. Would you happen to know when (and if) these files will be available…..assuming it’s not a 20 year rule or anything like that.

5 August: IMF Archives

Could you please provide some background information about your affiliation and the need to obtain these documents. Classified documents undergo declassification process when such a request is submitted. It can be a lengthy process up to one year.

5 August: me

I was interested in these specific documents because I am researching IMF gold sales for various articles and reports that I’m planning to write.

6 Aug: IMF

Thank you for providing additional information regarding your inquiry. Please send us a formal request for the declassification of these two documents specifying your need to have access to them. We will follow through on your behalf and get back to you with a response.

Before I had replied with a formal request, the IMF archives people contacted me again on 12 August 2015 as follows:

12 Aug: IMF

While waiting for your official request we made preliminary inquiries regarding the requested documents. The decision communicated back to us is not to declassify these documents because of the sensitivity of the subject matter.

In the meantime, we want to make sure you have checked publicly available documents on the same topic accessible from the IMF.org: https://www.imf.org/external/np/sec/pr/2009/pr09310.htm

12 August: me

Thank you for the clarification. That’s surprising about the classification given that the IMF on-market gold sales were supposed to be transparent.

Was there any information fed back to Archives on why the ‘subject matter’ is deemed sensitive?

14 Aug: IMF Archives

“Thank you for your follow-up email. Unfortunately, these particular documents are still deemed classified and no further explanation has been communicated to the Archives.”

My next set of questions to IMF Archives in August 2015 addressed the 7 missing monthly gold sales reports that should have covered May – December 2010. Since there is a 3 year rule or maybe at max a 5 year rule under the IMF’s Transparency Policy (Archive Policy), I thought that maybe the May/June, June/July, and July/August 2010 files might be due for automatic release under the 5 year rule by the end of August 2015.

22 August 2015: Me:

“I have a question about documents which appear in the online Archive after the 5 year schedule.

Is there a scheduled update or similar which puts newly available documents in the Archive when the 5 years has elapsed?

For example, I see some documents in the Archive from June 2010, but not July/August 2010. Is there an automated process that runs, but that hasn’t yet run for July/August 2010, that puts the latest documents into the publicly available Archive?”

24 August: IMF

“Thank you for your inquiry. The review and declassification of eligible documents that meet the time rule is done by batches. Therefore, publication does not happen in real time. It is a process that takes time and might cause a delay. We will let you know when July and August documents are posted.”

2 October 2015: me

“Do you know when documents from June 2010 onwards will be added to the IMF online archive? I still don’t see any yet.

Is there a batch of declassifications for June 2010 / July 2010 / August 2010 happening soon?”

2 October: IMF

“Thank you for contacting the IMF Archives. Unfortunately, we are unable to speculate about the documents website availability and provide a more specific timeframe than the one already communicated in the attached correspondence. As already promised, we will let you know when July and August documents are posted.”

Then about 30 minutes later (on 2 October 2015) the IMF sent me another email:

2 October: IMF

“Dear Mr. Manly,

I ran a sample search of Executive Board minutes available via IMF Archives catalog and was able to find minutes issued in June and July 2010. Is there a specific document you are looking for which you are unable to find?

Sincerely”

2 October: Me

“I was searching for the next months’ reports in the below series, report name “Monthly Report on Sales of Gold on the Market" – see screenshot attached.

The current search retrieval brings back 3 reports spanning February- May 2010, but nothing after May 2010. Report names in the retrieved search results are:

SM/10/69

SM/10/102

SM/10/139”

I was wondering if a couple of months in this series after May 2010 are available now?”

5 October: IMF

“The reports after May 2010 haven’t been declassified for public access because of the sensitivity of the subject matter, and therefore they are not available for retrieval.

We apologize for any inconvenience this may cause.”

5 October: Me

“Thanks for the reply. Out of interest, why were the reports from February to May 2010 declassified, since surely the June-December 2010 monthly reports are identical to the first three months in that they are also just providing monthly updates on the same batch of gold ~180 tonnes of gold which was being sold over the 10 month period?”

7 October: IMF

“Dear Mr. Manly,

This series of reports is under review at the moment, and according to security classification they are currently closed.

Sincerely,

IMF Archives”

And there you have it folks. This is IMF transparency. As per the IMF Archive disclosure policy, only Christine Lagarde, current IMF Managing Director, has the authority to consent to the declassification of classified Executive Board documents.

Sensitivity of Subject Matter – China and Bullion Banks

The above IMF responses speak for themselves, but in summary, here we have an organization which claims to be transparent and which claims to have run a transparent ‘on-market’ gold sales program in 2010, but still after more than 6 years it is keeping a large number of documents about the very same gold sales classified and inaccessible to the public due to the ‘sensitivity of the subject matter’. What could be so sensitive in the contents of these documents that the IMF has to keep them classified? Matters of national security? Matters of international security? And why such extremely high level security for an asset that was recently described by the august Wall Street Journal as a ‘Pet Rock’?

The secrecy of keeping these documents classified could hardly be because of sensitivity over the way in which the sales were executed by the agent, since this was already revealed in the February – May reports that are published, and which looks like a normal enough gold sales program by the Bank for International Settlements on behalf of the IMF? Could it be to do with the identities of the counterparties, i.e. the buyer(s) of the gold? I think that is the most likely reason.

Two counterparties that spring to mind that might request anonymity in the ridiculously named ‘on-market’ sales process would be a) the Chinese State / Peoples Bank of China, and b) a group of bullion banks that were involved in gold swaps with the BIS in 2009/2010.

Chinese discretion – Market Speculation and Volatility

Bearing in mind another one of the IMF’s mantras during the 2009-2010 gold sales processes that it wanted to “avoid disruption of the gold market", and the Chinese State’s natural surreptitiousness, the following information reported by China Daily on 24 February 2010 (which was the first week of ‘on-market’ sales) is worth considering. The article, titled ‘China unlikely to buy gold from the IMF‘, stated the following:

“Contrary to much speculation China may not buy the International Monetary Fund’s (IMF) remaining 191.3 tons of gold which is up for sale as it does not want to upset the market, a top industry official told China Daily yesterday.

“It is not feasible for China to buy the IMF bullion, as any purchase or even intent to do so would trigger market speculation and volatility," said the official from the China Gold Association, on condition of anonymity."

To me, these comments from the ‘anonymous’ China Gold Association official are a clear indication that if China was the buyer of the remaining 181.3 tonnes (ie. 191.3 tonnes – 10 tonnes for Bangladesh), then China certainly would have conducted the purchase in secrecy, as ‘it does not want to upset the market’, and “any purchase or even intent to do so would trigger market speculation and volatility”

In the same China Daily article, there was also a comment reported from Asian Development Bank economist Zhuang Jian, who was in favor of China buying the IMF gold, as he thought that “buying IMF gold would not only help China diversify its foreign exchange reserves but also strengthen the yuan as an international currency”, and that China would “have a bigger say in the IMF through the gold purchasing deal”.

Zhuang Jian also stated that “China can start with small purchases on the international market like the 191.3 tons of IMF gold. In the short-term, the market will see volatility, but in the long-term the prices will return to normal”.

BIS Swaps and Bullion Bank Bailouts

In late June 2010, the Bank for International Settlements (BIS) published its annual report to year-end March 2009. This report revealed that the BIS had, during its financial year, taken on gold swaps for 349 tonnes. The Wall Street Journal (WSJ) initially reported in early July 2010 that these swaps were with central banks, however the BIS clarified to the WSJ that the gold swaps were in fact with commercial banks. The Financial Times then reported in late July 2010 that “Three big banks – HSBC, Société Générale and BNP Paribas – were among more than 10 based in Europe that swapped gold with the Bank for International Settlements." Notice that two of the named banks are French banks.

Since the BIS refuses to explain anything material about these swaps, which was most likely a gold market fire-fighting exercise, the details remain murky. But the theory that best explains what actually happened was advanced by the late Adrian Douglas of GATA in early July 2010. Douglas proposed that bullion bank gold bailout tripartite transactions actually created the BIS gold swaps. Since IMF gold is stored at both the Bank of England vaults in London and at the Banque de France vaults in Paris, IMF ‘on-market’ gold held in Paris or London would be very easy to transfer to a group of bullion banks who all hold gold accounts at the Bank of England and, it now appears, also hold gold accounts at the Banque de France.

In May 2012, George Milling-Stanley, formerly of the World Gold Council, provided some insight to the publication Central Banking about the role of the Banque de France in being able to mobilize gold. Milling-Stanley said:

“Gold stored at the Bank of England vaults … can easily be mobilised into the market via trading strategies, or posted as collateral for a currency loan"

‘Of the Banque de France, Milling-Stanley says it has ‘recently become more active in this space [mobilising gold into the market], acting primarily as an interface between the Bank for International Settlements in Basel [BIS] and commercial banks requiring dollar liquidity. These commercial banks are primarily located in Europe, especially in France’."

It’s interesting that two of the three banks named by the Financial Times as being involved in the BIS gold swaps are French, and that Milling-Stanley mentioned that most of the commercial banks that interfaced with the BIS are French banks. Given that the then Managing Director of the IMF, Dominique Strauss-Kahn, is French, as is his successor Christine Lagarde, could some of the ‘on market’ IMF gold sales been a case of the French controlled IMF bailing out French bullion banks such as SocGen and BNP Paribas?

Applied to the IMF gold sales, and under a tripartite transaction, as I interpret it, the following transactions would occur:

IMF gold is transferred by book entry to a set of bullion banks who then transfer the title of this gold to the BIS. The BIS transfers US dollars to the bullion banks who then either transfer this currency to the IMF, or owe a cash obligation to the IMF. The sold gold is recorded in the name of the BIS but actually remains where it is custodied at the London or Paris IMF Gold Depositories, i.e. at the Bank of England or Banque de France vaults.

In this scenario, the IMF gold could have been transferred to bullion banks and further transferred to the BIS during 2009, with the ‘on-market’ pricing exercise carried out during 2010. With the BIS as gold sales agent, the entire set of transactions would be even more convenient since the BIS gold trading desk would be able to oversee the gold swaps and the gold sales.

So, in my opinion, the IMF ‘on-market’ gold on offer was either a) bought by the Chinese State, or b) was used in a gold market fire-fighting exercise to bail out a group of bullion banks, or c) a combination of the two.

Modalities of Gold Sales

As to why the IMF paper “Modalities for Limited Sales of Gold by the Fund" (Sept 4th 2009) SM/09/243" is under lock and key and can only be declassified by the IMF Managing Director Christine Lagarde, the conclusion is that it too must contain references to something that the IMF are extremely worried about allowing into the public domain. For the simple reason is that a similarly named IMF paper from 25 June 1999, titled “Modalities for Gold Sales by the Fund" (EBS/99/110)" is accessible in the IMF Archives, and while revealing in a number of respects, it hardly contains ‘sensitive material’. This paper was prepared when the IMF had been thinking about conducting gold sales back in 1999 which never materialized, except in the form of an accounting trick to sell to and simultaneously buy back a quantity of gold to and from Mexico and Brazil. This 1999 paper “Modalities for Gold Sales by the Fund" is very interesting though for a lot of reasons as it sketches out the limitations on IMF gold sales, the approaches to the sales that were considered by the IMF at that time, and it’s also is full of pious claims that the gold sales process should be ‘transparent’, such as the following:

“it will be critical to ensure transparency and accountability of the Fund’s gold operations through clear procedures for selecting potential buyers and determining prices, and through public disclosure of the results of the sales after they have taken place. The need for transparency and evenhandedness, which is essential for an international financial institution, argues for providing as much information as possible to the public."

On the actual approaches to gold sales, the 1999 Modalities paper introduces the topic as follows:

“This paper considers four main modalities for the sale of gold by the Fund: (i) direct sales to another official holder of gold; (ii) placements into the market through a private intermediary or a group of intermediaries, such as bullion banks; (iii) placements into the market through the intermediation of a central bank with experience in gold sales or the BIS; and (iv) direct sales to the market through public auctions, as was the case with the gold sales by the Fund between 1976 and 1980"

On the topic of publication of sales results, the 1999 paper states:

“Publication of results: In all cases, the Fund would make public at regular, say monthly, intervals the quantity sold and the prices obtained, as well as, depending on the modality decided by the Board, the names of the buyers. In the case of a forward sales strategy involving an intermediary, the Fund would make public the quantities and delivery dates of the forward sales. It would be for consideration whether the Fund would announce the names of the intermediaries selected by the Fund to sell the gold, if that modality would be chosen"

On the topic of limitations to IMF gold sales, the 1999 paper says:

“Under the Articles, the Fund is only authorized to sell gold; that is, to transfer ownership over gold on the basis of prices in the market, taking into account reasonable transactions costs. The Articles prescribe the objective of avoiding the management of the price, or the establishment of a fixed price, in the gold market (Article V, Section 12 (a)). This implies that the Fund “must seek to follow and not set a direction for prices in the gold market.“

Under the Articles, the Fund cannot engage in gold leasing or gold lending operations, enter into gold swaps, or participate in the market for gold options or other transactions that do not involve the transfer of ownership over gold."

A second shorter 1999 IMF paper on the modalities of gold sales, titled “Concluding Remarks by the Chairman Modalities of Gold Sales by the Fund, Executive Board Meeting 99/75, July 9, 1999, BUFF/99/81" gave some indication on which approach (modality) the Executive Board were leaning to at that time to execute gold sales:

“Directors generally expressed the view that private placements of gold, either through a group of private institutions or through the intermediation of central banks or the BIS, had many advantages in terms of flexibility, both in terms of timing as well as in the discretion that the Fund’s agents could employ in the techniques that they could use to channel gold into the market.“

And from the discussion, using the services of the BIS (or another central bank) appeared to be most favorable option:

“Directors further noted that there would be considerable practical difficulties in the choice of the institution or group of institutions through which the sales of gold could be conducted, even though these would be limited-but not entirely eliminated-by choosing a central bank or the BIS.“

IMF Comedians

In conclusion, for sheer comedy reading, there is a tonne of material in the IMF’s latest ‘transparency’ smoke and mirrors claims, dated 24 March 2016, which contains such comedy gems as:

“Greater openness and clarity by the IMF about its own policies and the advice it provides to its member countries contributes to a better understanding of the IMF’s own role and operations, building traction for the Fund’s policy advice and making it easier to hold the institution accountable. Outside scrutiny should also support the quality of surveillance and IMF-supported programs."

“The IMF’s efforts to improve the understanding of its operations and engage more broadly with the public has been pursued along four broad lines: (i) transparency of surveillance and IMF-supported programs, (ii) transparency of its financial operations; (iii) external and internal review and evaluation; and (iv) external communications."

“The IMF’s approach to transparency is based on the overarching principle that it will strive to disclose documents and information on a timely basis unless strong and specific reasons argue against such disclosure."

Again, what could these “strong and specific reasons" arguing “against such disclosure" be for the 2010 IMF gold sales?

By now you will begin to see that the IMF’s interpretation of transparency on gold sales diverges massively from any generally accepted interpretation of transparency. The IMF appears to think that merely confirming that a gold sale took place or will take place is the epitome of transparency, when it would more accurately be described as obfuscation and a disdain for actual communication with the public. IMF transparency is anything but transparent.

Perhaps the usually useless mainstream financial media may finally sit up and next time they bump into the IMF’s Ms Lagarde at a press conference, ask her why the IMF continues to block access to its 2010 gold sales documents, which remain classified due to, in the IMF’s own words, “the sensitivity of the subject matter". Here’s hoping.

Popular Blog Posts by Ronan Manly

How Many Silver Bars Are in the LBMA's London Vaults?

How Many Silver Bars Are in the LBMA's London Vaults?

ECB Gold Stored in 5 Locations, Won't Disclose Gold Bar List

ECB Gold Stored in 5 Locations, Won't Disclose Gold Bar List

German Government Escalates War On Gold

German Government Escalates War On Gold

Polish Central Bank Airlifts 8,000 Gold Bars From London

Polish Central Bank Airlifts 8,000 Gold Bars From London

Quantum Leap as ABN AMRO Questions Gold Price Discovery

Quantum Leap as ABN AMRO Questions Gold Price Discovery

How Militaries Use Gold Coins as Emergency Money

How Militaries Use Gold Coins as Emergency Money

Hungary Announces 10-Fold Jump in Gold Reserves

Hungary Announces 10-Fold Jump in Gold Reserves

Planned in Advance by Central Banks: a 2020 System Reset

Planned in Advance by Central Banks: a 2020 System Reset

China’s Golden Gateway: How the SGE’s Hong Kong Vault will shake up global gold markets

China’s Golden Gateway: How the SGE’s Hong Kong Vault will shake up global gold markets