FTX Fiasco Highlights the Modern Banking & Gold Market Ponzi

Ronan Manly

Ronan Manly 0 Comments

0 CommentsThe recent collapse of crypto exchange FTX and associated crypto trading firm Alemada Research has shell-shocked the financial world while wiping out the assets of FTX and Alameda customers and dragging down investments in the wider crypto space.

It has also, in revealing a cesspit of corporate misconduct and fraud, brought the concepts of Ponzi schemes and Fractional Reserve schemes firmly to the fore of public consciousness, while inviting parallels with other parts of the financial system, not least, comparisons to the modern banking system and the paper gold market.

Since the news flow about the FTX debacle is seemingly non-stop (and increasingly more bizarre with each passing day), there is plenty of coverage on the web about what triggered FTX’s downfall, so I won’t repeat it all here, save for some points on the nature of FTX-Alameda holdings and transactions, their fraudulent and Ponzi nature, and their total lack of transparency.

FTX – Alameda Interconnected

FTX is/was a centralized cryptocurrency exchange, which was founded in 2019, and which entered into bankruptcy proceedings on 11 November 2022. FTX was founded by Sam Bankman-Fried (SBF) and Gary Wang, and during its meteoric rise, was at one stage the third largest cryptocurrency exchange in the world. SBF was CEO of FTX. The native token of the FTX exchange was/is FTT (in the same way, for example, that BNB is the native token of Binance, and KCS is the native token of Kucoin).

Alameda Research, which was also co-founded by Sam Bankman-Fried (in 2017), is/was a crypto quant trading firm as well as an investor in the crypto sector. Alameda Research also filed for bankruptcy on 11 November 2022. Caroline Ellison was CEO of Alameda at the time of the bankruptcy filing.

On 2 November 2022, an article by website Coindesk highlighted that a large chuck of the assets on Alameda’s balance sheet were in the form of the FTT token, a token which FTX creates out of thin air, and the implication then based on this balance sheet composition was that Alameda was insolvent due to losses that it had suffered on crypto investments from earlier in 2022 (possibly from 3AC and Luna losses during springtime), losses which it had up to then hidden, and that due to this the FTX exchange had been propping up Alameda with loans which were collateralized with the very token (FTT) which FTX had created itself (which is in itself a scam since you as a lender can’t accept collateral of something which you created yourself).

After the Coindesk article, Binance, a competitor crypto exchange, which was holdings US$ 500 million of FTT, then moved quickly to sell it’s FTT stake, which caused the FTT price to plummet, and which caused panic from FTX clients over the next week as they moved to withdraw their funds and coins from FTX, which was a sort of ‘bank run’ on FTX, despite the fact that FTX was not a bank. For example, on Sunday 6 November, FTX customers are said to have (by SBF) withdrawn $5 billion from the FTX platform.

Chapter 11 – on November 11th

During this time, FTX tried to raise funds from outside investors, but failed, including a stalled offer to buy the FTX exchange from Binance. Given the lack of options in fund raising, about 130 companies in the ‘FTX’ and ‘Alameda’ empire (across 4 silos of FTX.com, Alameda, FTX US, and a Ventures silo) then all simultaneously filed for bankruptcy on 11 November. So that’s Chapter 11 on 11/11 for all the numerologists. At this point SBF resigned as CEO of FTX. The bankruptcy was filed in a Delaware court. See here.

The new CEO of FTX appointed at the time of bankruptcy filing is insolvency specialist and attorney, John J. Ray. In the FTX Bankruptcy filing, Ray said:

“Never in my career have I seen such a complete failure of corporate controls and such a complete absence of trustworthy financial information as occurred here.

From compromised systems integrity and faulty regulatory oversight abroad, to the concentration of control in the hands of a very small group of inexperienced, unsophisticated and potentially compromised individuals, this situation is unprecedented.”

Ray also said that the objectives of the Chapter 11 bankruptcy filings included a) implementation of controls in areas such as accounting, audit, cash management, and risk management, which “did not exist or did not exist to an appropriate degree, prior to my appointment”, b) create transparency by deliberate investigation into FTX-Alameda, c) provide “Asset Protection & Recovery” in terms of “the location and security of property of the estate, a substantial portion of which may be missing or stolen”.

Ray’s team somehow assembled or were given balance sheets of the 4 groups of companies which filed for bankruptcy, but he literally didn’t believe any of the figures, since in the filing, Ray states on multiple occasions that since their balance sheets were:

“produced while the Debtors were controlled by Mr. Bankman-Fried, I do not have confidence in [them], and the information therein may not be correct as of the date stated.”

Balance Sheets – From Bad to Worse

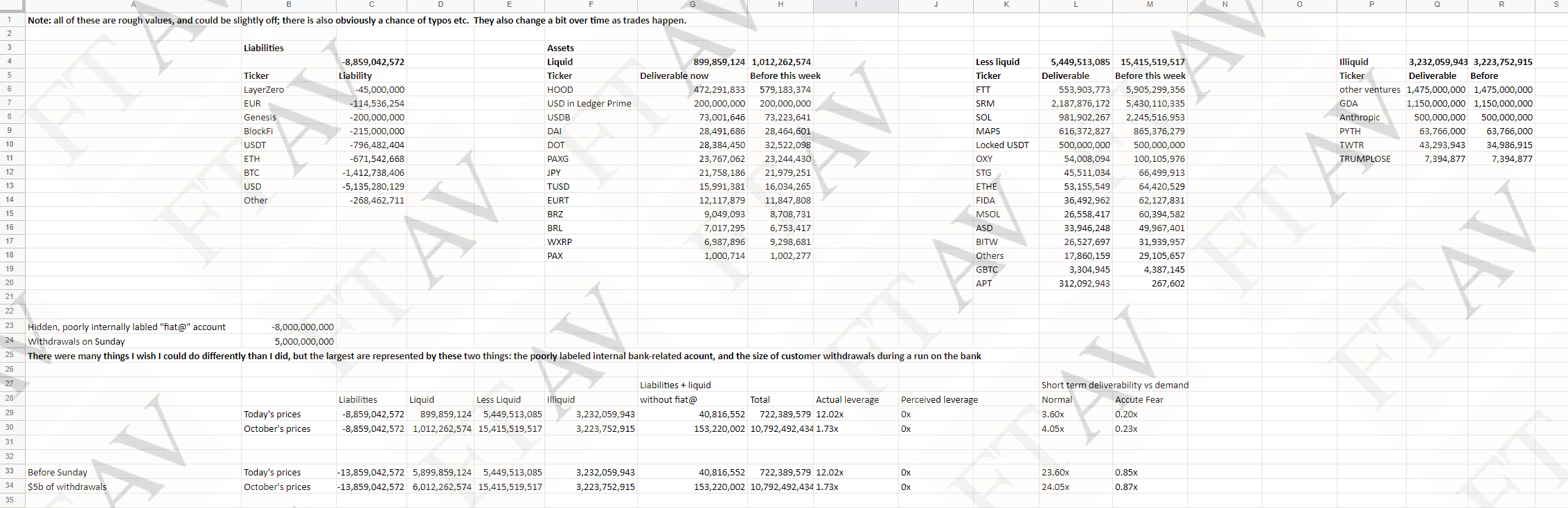

Then on 12 November, the Financial Times got its hands on another sort of balance sheet, this time an amateur Excel page printout of an FTX balance sheet, dated 10 November, that Sam Bankman-Fried had cobbled together and had circulated during the final fundraising attempt.

This 1 pager XLS worksheet (see here) which was created by SBF himself, claims that the FTX exchange had customer liabilities of US $ 8.86 billion but at the same time only had liquid assets of US$ 900 million (and more than half of this $900 million was equity stock of the brokerage Robinhood (i.e. stock in ticker HOOD)). So that straight away was an $8 billion deficit of liabilities compared to liquid assets.

The XLS worksheet also listed ‘less liquid’ and ‘illiquid’ assets, the ‘less liquid’ assets being a majority of tokens created by FTX such as the tokens FTT, Serum (SRM) and another token MAPS – all of which were created out of thin air.

FTX’s liabilities of $8.86 billion included about 1.4 billion of Bitcoin (BTC), yet according to the spreadsheet, FTX actually held no BTC whatsoever. So FTX was pretending that it had bought Bitcoin for its customers, when there was no BTC at all held by FTX. In this instance, not only was there no 1:1 backing of coins for claims, there appears to have been no backing.

For a neat visual of SBF’s FTX ‘balance sheet’, see the visual graphic created by Visual Capitalist, dated 15 November here.

So BlockFi is a creditor to FTX that lent to Alameda that lent to Emergent which is a shell company owned by SBF that bought Robinhood shares that were pledged as collateral to guarantee to BlockFi the loan to FTX that was used to bailout BlockFi itself

— ayko2718 (@ayko2718) November 29, 2022

SBF’s Infantile Excuses

There were also two startling entries on the XLS, one for ‘Withdrawals on Sunday’ of US$ 5 billion (which showed the run on FTX on Sunday 6 November), and also a bizarre deceptive entry for an additional liability, described as a ‘Hidden, poorly internally labeled “@fiat” account’ which was for a massive US$ 8 billion.

This $8 billion looks like a transfer out of FTX, and could be FTX customer funds illegally transferred to Alameda. So that gives a total of FTX net liabilities of US$ 8 billion (from the balance sheet liabilities minus the liquid assets) plus another US$ 8 billion, for a total of US$ 16.8 billion of net liabilities.

Given that most of the FTX ‘assets’ listed by SBF are tokens created out of thin air by FTX, then where did all the customer money go, and for that matter where did the investment money from the likes of Singapore’s Temasek, and Sequoia go?

As Matt Levine of Bloomberg in an article dated 14 November puts it:

“$16 billion of dollar liabilities and assets consisting mostly of some magic beans that you invented yourself and acquired for zero dollars? WHAT?

Never mind the valuation of the beans; where did the money go? What happened to the $16 billion?

Spending $5 billion of customer money on Serum would have been horrible, but FTX didn’t do that, and couldn’t have, because there wasn’t $5 billion of Serum available to buy. FTX shot its customer money into some still-unexplained reaches of the astral plane.”

Transfers to Alameda

The core of ‘Where did the money go?’, at least to a large extent, seems to involve the connections and massive conflicts of interest between FTX and Alameda. Reuters reported on 13 November that SBF secretly moved US$ 10 billion in customer funds from FTX to Alameda, and that $1 billion – $2 billion in client money was unaccounted for.

And there were flows in the other direction also, with Business Insider highlighting on 17 November that according to the bankruptcy filing “Sam Bankman-Fried and a company he owns got $3.3 billion in loans from Alameda”.

Letter SBF sent today to FTX employees h/t @CoinDesk pic.twitter.com/YERO3yfKnI

— Liz Hoffman (@lizrhoffman) November 22, 2022

Another infantile reference by SBF to bank accounts came in an email that he sent to FTX employees on 22 November, trying to justify why FTX had collapsed, saying that he had forgotten about “old fiat deposits before FTX had bank accounts”. This ‘story’, obtusely, refers to FTX customer funds flowing into Alameda, and is also connected to the “Hidden, poorly internally labeled “@fiat” account” referred to in SBF’s spreadsheet.

so SBF’s story of how Alameda lost $8bil of FTX user funds. FTX was using Alameda’s bank account for user wires. poor internal accounting, forgot to transfer to FTX. meantime Alameda gambled and lost it, but they had enough FTT & FTX related tokens to buy back. until they didn’t. pic.twitter.com/SgS72xIuFV

— Adam Back (@adam3us) November 16, 2022

Taking Client Funds – Breach of FTX Terms

On SBF’s first full interview since the FTX collapse, which was conducted by Tiffany Fong, and published on 29 November on YouTube (see here), SBF continues to push this ridiculous story to cover up massive transfers to Alameda being, again saying that this was due to mis-labeled bank accounts and customers wires going into Alameda accounts by the fluke of the account set-ups at that time:

2:05 [SBF] “a very poorly labeled accounting thing, which was a historical artifact of a time before FTX had bank accounts” … “people would wire money to Alameda and ask to be credited on FTX”

So the core of this scandal is why FTX customer deposits disappeared, and where they went. FTX was supposed to custody customers funds and crypto coins and tokens on behalf of its customers. Not take in deposits and lending out or invest these deposits. Even the FTX Terms of Service states this. The FTX Terms of Service can be seen at this link here, and also in the pdf accessible here (upload the pdf). As section 8.2.6 of the FTX Terms of Service says:

8.2.6 All Digital Assets are held in your Account on the following basis:

(A) Title to your Digital Assets shall at all times remain with you and shall not transfer to FTX Trading. As the owner of Digital Assets in your Account, you shall bear all risk of loss of such Digital Assets. FTX Trading shall have no liability for fluctuations in the fiat currency value of Digital Assets held in your Account.

(B) None of the Digital Assets in your Account are the property of, or shall or may be loaned to, FTX Trading; FTX Trading does not represent or treat Digital Assets in User’s Accounts as belonging to FTX Trading.

(C) You control the Digital Assets held in your Account. At any time, subject to outages, downtime, and other applicable policies (including the Terms), you may withdraw your Digital Assets by sending them to a different blockchain address controlled by you or a third party.

Fraud – Ponzi – Money Laundering?

So were FTX customer deposits and assets stolen or lent out without authorization or illegally invested, or all three? Why were client account balances commingled with FTX funds and not segregated from FTX’s own funds? Why was there no accounting system to record what was going on nor a governance system to oversee the firms’ operations? Were FTX customer funds used as collateral to fund FTX and Alameda loans? What kind of leverage did Alameda and FTX take using FTX client funds? What kind of massive margin calls did FTX and Alameda get which seems to have made FTX take huge amounts of customer assets to meet margin calls?

FTX was also a Ponzi scheme, where money taken in from new customers was used to pay out existing customers. It fell apart, as all Ponzi schemes do, when customer withdrawals hit escape velocity limit, and there was not enough capital to pay all the customers who demanded an exit. FTX tried various tactics to prolong the Ponzi such as attempting to ‘buy’ the assets of Voyager Digital, and also do a capital raise in November, but none of this worked.

As Marc Cohodes, said:

“FTX is not a crypto scam. It is a massive money laundering, Ponzi scheme fraud with a crypto wrapper. This has nothing to do with crypto.”

Marc Cohodes @AlderLaneEggs to @KeithMcCullough today

— Hedgeye (@Hedgeye) November 14, 2022

“FTX is not a crypto scam. It is a massive money laundering, Ponzi scheme fraud with a crypto wrapper. This has nothing to do with crypto. This shit needs to stop."

Watch on-demand replay free: https://t.co/ezPmXRgxy5 pic.twitter.com/XLgDtZ3ze2

There is widespread speculation and rumour that FTX was engaged in money laundering. Money came in and then went out. But to where? The money has to have gone somewhere.

Is it possible that some of the US government funds sent to Ukraine went to FTX, and then on to political donations?

— Rudy Havenstein: Summers in Rangoon & Luge Lessons (@RudyHavenstein) November 16, 2022

Bankman-Fried was also the second biggest donor to Joe Biden’s presidential campaign and overall Bankman-Fried gave US$ 40 million to political campaigns in the run up to the US 2022 midterm elections.

There are also rumours that FTX was a giant psyop, deliberately created by ‘Gov’, and the financial establishment so as to torpedo the image of private crypto and create fabricated pleas for regulation by the SEC and CFTC, with Bankman-Fried as a frontman but with the real puppet-masters hiding in the wings. Sam Frontman-Fried? Only time will tell, if those elements of the scandal even come out.

Modern Fractional-Reserve Banking

But the reason for highlighting the cesspit of FTX-Alameda here is to show that FTX was using customer funds in a fractional reserve manner, and also fraudulently doing so. As to whether fraud was the intent from day 1 or whether the customer funds became increasingly used to plug holes and gaps as the FTX-Alameda edifice started to keel over, will be something which will come out in time. FTX was operating like a fractional reserve bank, But it didn’t have a banking license. FTX was operating its scheme on the assumption that all customers didn’t want their money back at the same time. But when they did want their money back, it immediately showed that FTX was illiquid (if not insolvent). But at least illiquid.

Holy gaslighting, per FTX’s own terms of service, user deposits belonged to the users and could not be loaned out, and yet they were anyways

— ChainLinkGod.eth (@ChainLinkGod) November 23, 2022

All deposits should have been backed 1:1, as exchanges are not banks, therefore a bank run shouldn’t have even been possible

FTX should not even have been following a fractional reserve model, as it was illegal for it to do so. But what the FTX debacle does do is neatly highlight the dangers and risks inherent in other areas of the financial markets which employ fractional reserve models.

This is similar to how modern commercial banking works and also how ‘gold’ trading in London works. Not asking for your money back is what the entire modern commercial banking system is based on. Note wanting physically allocated gold is what the entire gold credit trading system operated by the LBMA bullion banks is based on.

Under a fractional reserve banking model, customers deposit money to a commercial bank. The deposit is an IOU, and the deposit becomes the bank’s property. The bank is also only required to hold a small percentage (if any) as reserves (cash in vault) to meet customer withdrawals, while lending out the rest of the deposits at a higher interest rate than it gives on the deposits.

The customer deposits are accounted for as liabilities of the bank. The bank’s loans are accounted for as assets of the bank. Since commercial bank loans literally create new money and have a multiplier effect (loans can be deposited and then lent out again in multiple loops), commercial loans are a huge source of money supply creation.

The percentage of deposit funds needed to be held back as reserves is called the bank’s required reserves. This ‘reserve requirement’ is a percentage dictated by the country’s central bank and it could even be zero. While a banking system can have a deposit insurance scheme to attempt to prevent bank runs, these schemes only cover deposits up to a limit, and an increase in bad loans or a plummet in collateral values can wipe out depositors.

This is how modern central banking works, despite most people not being aware of its fractional reserve nature. And it’s totally legal, and endorsed by regulators. But at its heart, fractional reserve banking is a giant Ponzi. Because if every depositor wants their money back at the same time, this is not possible. Because the banks have lent out the depositor money. Which is why when bank lending portfolios deteriorate, this also creates bank runs, as depositors rationally assume that the bank is illiquid and potentially insolvent. Which then necessitates bank bail-outs (rescues by governments using taxpayer money) or bank bail-ins (the bank’s bond holders and depositors get seized and bondholders and depositors don’t get repaid in full).

So there are obvious parallels between FTX and fractional reserve bank that implodes. Like a fractional reserve bank whose lending book gets wiped out and the bank depositors can’t be paid back, FTX customer cash, crypto and investments can’t be repaid due to FTX having in various ways seized and used those funds. The global fractional-reserve banking sector, like FTX, also lobbies and donates millions to politicians, and when banks need bailout (such as the Great Financial Crash of 2007-2009), the money bribes to politicians don’t get repaid.

Except that FTX was not supposed to be running as a fractional reserve system. Although in practice, through fraud, FTX was being run as a fractional reserve system. This is why it’s ludicrous that regulators are calling for crypto exchanges to be regulated like fractional reserve banks. Crypto exchanges should not be running fractional-reserve schemes.

London Gold Market – The biggest has Yet to Come

LBMA fractional-reserve gold and silver trading https://t.co/AdCzmNKc6h

— BullionStar (@BullionStar) November 10, 2022

Which brings us to the biggest fraud of all. Bullion banking as practised by the London Bullion Market Association (LBMA) banks in London.

Bullion Banking as practiced by the LBMA banks in London is a gigantic fractional reserve system, where massive amounts of gold credit that are created out of thin air, are traded on a daily basis with no connection to underlying physical gold. The same is true of these bullion banks creating and trading silver credit, created out of thin air. This gold credit and silver credit is created and traded using the sleight of hand trick called unallocated gold and unallocated silver, a.k.a paper gold and paper silver.

BullionStar has explained all of this in minute detail in various places on the BullionStar website such as here in the ‘Bullion Banking Mechanics’ article in BullionStar’s Gold University pages.

Some extracts:

“In contemporary bullion banking, the amount of gold circulating in the bullion banking system is not fully backed by physical gold. It’s only fractionally backed, and in some cases may be unbacked.”

“You might think, I can see how new fiat currency can be created out of thin air since its either printed or credited electronically, but gold can’t be created out of thin air, can it? The answer is that, in the modern bullion banking system, “gold” can be created out of thin air, and is created out of thin air, as a form of paper gold or synthetic gold.”

“Under LBMA definitions, an ‘unallocated’ gold account is one in which the customer merely has a claim on the bullion bank account provider for an amount of gold (assuming the account balance is in credit).

The bullion bank in turn has a liability to the customer for the same amount of gold. Importantly, in the LBMA system, the customer ‘is an unsecured creditor’ of the bank.”

“This LBMA unallocated accounts and positions system is at the heart of the bullion banking fractional reserve system and nearly all of the activities that bullion banks are involved in.”

Unallocated gold and silver credits underlie everything in the LBMA system from trading to clearing and lending and borrowing. A highly leveraged, fractional reserve system of credit where the holders never intend to take delivery.

“Although the terms of the unallocated bullion account usually provide for the account holder’s right to demand the physical delivery of gold, the reality of unallocated bullion trading is that buyers and sellers rarely intend for physical delivery to ever take place.

Unallocated bullion is used as a means to have “synthetic” holdings of gold and so obtain exposure to the price of gold by reference to the London gold fixing.”

The fractional-reserve gold credit system employed by the London Gold Market was also explained by Daniel March in his interview for BullionStar Perspectives in November 2020, the relevant part of which can be seen here.

And gold ‘credit’, as issued by LBMA bullion banks, entails credit risk, counterparty risk and default risk, since this ‘credit’ is issued by commercial banks. These LBMA bullion banks are supposed to store a certain amount of physical gold as reserves to cover cases where a counterparty requests physical delivery, but in reality their reserves are dwarfed by the sheer scale of gold ‘credit’ traded on a daily basis, and most of the physical gold in gold is held by central banks and ETFs, not by bullion banks for reserve requirements.

Like FTX, the LBMA bullion banks are running a fractional reserve scheme, only in this case the scheme has the blessing of the Bank of England and the UK Financial Conduct Authority (FCA). Like FTX/Alameda, the LBMA fractional reserve metals scheme is opaque and lacking in transparency.

But if a run on bullion banks occurred, where more paper gold holders wanted to convert their paper claims into real physical gold than the amount of physical available, then paper markets would become illiquid, triggering panic and a rush to sell. And, like in the case of FTX, when confidence goes, the whole house of cards goes Boom.

So why are the mainstream financial media, such as Bloomberg, not investigating the opaque fractional reserve system that is the London gold and silver markets, and calling for the LBMA to issue audited “Proof of Reserves’ as to what backs the gigantic daily paper gold and silver trading?

I think we all know the answer to that, and it also, you might be surprised to know, has a parallel with the FTX collapse.

On 21 November, major website Hedgeye highlighted how in July, Fraud exposer Marc Cohodes gave the entire FTX fraud story to Bloomberg Crypto in London, but Bloomberg failed to act on it.

“Consider this. Fraud exposer and veteran shortseller Marc Cohodes handed the entire SBF/FTX fraud story to Bloomberg Crypto in London in July. They passed on it. Let that sink it. Their reason? ‘They thought it was too hard, too complicated, and might interfere with gaining access to SBF going forward,’ Cohodes says.”

‘Fraud exposer Marc Cohodes handed the entire SBF/FTX fraud story to Bloomberg Crypto in London in July. They passed on it. Their reason? “They thought it was too hard, too complicated & might interfere with gaining access to SBF,” Cohodes said. https://t.co/T5Ixs2vx2J

— BullionStar (@BullionStar) November 28, 2022

Now you can see why Bloomberg in London never investigates the fractional reserve London gold market, nor investigates the LBMA bullion banks operating this scheme. So when the unallocated, fractional reserve, synthetic, gold (and silver) credit system of the LBMA eventually fails, as it invariably will if a small subset of claim holders ask for delivery at the same time, don’t let Bloomberg (or Reuters) off the hook for not investigating when they plead that they didn’t know.

Popular Blog Posts by Ronan Manly

How Many Silver Bars Are in the LBMA's London Vaults?

How Many Silver Bars Are in the LBMA's London Vaults?

ECB Gold Stored in 5 Locations, Won't Disclose Gold Bar List

ECB Gold Stored in 5 Locations, Won't Disclose Gold Bar List

German Government Escalates War On Gold

German Government Escalates War On Gold

Polish Central Bank Airlifts 8,000 Gold Bars From London

Polish Central Bank Airlifts 8,000 Gold Bars From London

Quantum Leap as ABN AMRO Questions Gold Price Discovery

Quantum Leap as ABN AMRO Questions Gold Price Discovery

How Militaries Use Gold Coins as Emergency Money

How Militaries Use Gold Coins as Emergency Money

Hungary Announces 10-Fold Jump in Gold Reserves

Hungary Announces 10-Fold Jump in Gold Reserves

Planned in Advance by Central Banks: a 2020 System Reset

Planned in Advance by Central Banks: a 2020 System Reset

China’s Golden Gateway: How the SGE’s Hong Kong Vault will shake up global gold markets

China’s Golden Gateway: How the SGE’s Hong Kong Vault will shake up global gold markets

{kind=link}