Bullion Banks Line Up to Support LME’s Gold Futures

Ronan Manly

Ronan Manly 0 Comments

0 CommentsThe London Metal Exchange (LME) and World Gold Council have just confirmed that their new suite of London-based exchange-traded gold and silver futures contracts will begin trading on Monday 10 July. These futures contracts are collectively known as LMEprecious.

The launch of trading comes exactly 11 months after this LMEprecious initiative was first official announced by the LME and World Gold Council on 9 August 2016. Anyone interested in the background to these LMEprecious contracts can read previous BullionStar articles “The Charade Continues – London Gold and Silver Markets set for even more paper trading" and “Lukewarm start for new London Gold Futures Contracts”.

This 10 July 2017 launch is itself over a month behind schedule given that LMEprecious was supposed to be launched on 5 June but was delayed by the LME.

Underlying What?

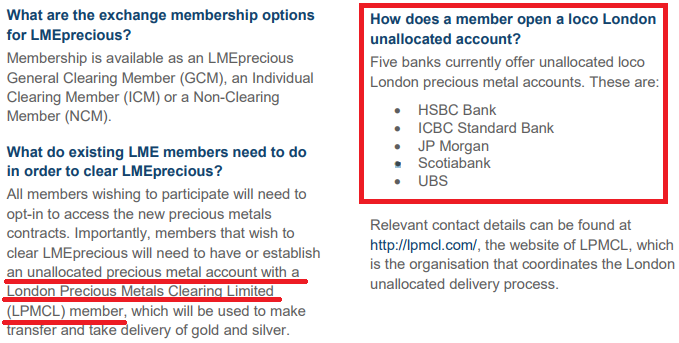

As a reminder, these LMEprecious gold futures and silver futures contracts represent unallocated gold and silver and there is no direct connection in the contracts to physical gold or physical silver, since settlement is via unallocated gold and silver balance transfers across LME Clearing unallocated metal accounts at member banks of London Precious Metals Clearing Limited (LPMCL).

Still, this hasn’t stopped LME from using terminology in the contract specs that attempts to link them by association to real precious metal. For example, the gold contract spec says that the:

“underlying material” is “Loco London Fine Gold held in London and complying with standards relating to good delivery and fineness acceptable to the Precious Metal Clearer of the Clearing House".

This is similar to how an estate agent (realtor) would describe a house that’s located in a bad area, i.e. that it’s not too far from a good area.

The LME also fails to mention the fact that the LBMA/LPMCL unallocated account system is a fractionally-based paper gold and paper silver trading system, with trading volumes of unallocated gold and unallocated silver that are 100s of times higher than the available physical metal sitting in the London precious metals vaults. Ironically, these gold and silver futures are starting to trade in a month in which the LBMA has still not begun publishing the actual quantities of gold and silver in the LBMA vaults in London, despite promising to.

For both gold and silver, the LME futures contract suite will consist of a daily trade date (T) + 1 contract (T+1), known as TOM, and daily futures from a T + 2 (equivalent to Spot settlement) out to and including all trade dates to T + 25. Beyond this, there are approximately 36 monthly futures contracts covering each month out to 2 calendar years, and then each March, June, September and December out to 60 calendar months (12 more quarters out to 5 years).

All LMEprecious contracts will centrally clear on LME’s clearing platform LME Clear. The contracts can be traded on LME’s electronic trading platform LMESelect between 1am and 8pm London time, and can also be traded 24 hours a day ‘inter-office’ over the blower (voice-based trading). Apart from trading hours differences, the only other difference between LMESelect and phone is that of the daily contracts, only T+1 to T+3 can be traded via LMESelect, while T+1 to T +25 can be traded over the phone.

The LME also plans to roll out options products and calendar spread products based on these futures, but as to when these will appear is not clear.

Banks, Banks and more Banks

The official line is that LMEprecious has been developed by a consortium of the LME, the World Gold Council and a group of investment consisting of Morgan Stanley, ICBC Standard, SocGen, Goldman Sachs and Natixis, as well as prop trading firm OSTC, but to what extent each of the 5 banks and OSTC has had input into the product development and trading rules of LMEprecious is unclear.

On 3 August 2016, the World Gold Council established a UK registered company called ‘EOS Precious Metals Limited’ to house the arrangement between the Council and the aforementioned banks and OTSC. The first director of EOS was Robin Martin, managing director of market infrastructure at the World Gold Council, while the first registered address of EOS was actually the World Gold Council’s London office at 10 Old Bailey in the City of London.

A slew of other directors were then appointed to EOS Precious Metals Ltd on 9 November 2016, namely:

- Aram Shishmanian, CEO of World Gold Council

- Raj Kumar – ICBC Standard Bank (formerly of Deutsche Bank and formerly a director of London Precious Metals Clearing Limited (LPMCL)

- Bradley Duncan – ICBC Standard Bank (resigned as director March 2017 and replaced by Richard England)

- Francois Combes – SocGen (formerly a director of London Gold Market Fixing Limited)

- Vinvent Domien – SocGen (formerly a director of London Gold Market Fixing Limited)

- Matthew Alfieri – Goldman Sachs (resigned May 2017 and replaced by Donald Casturo)

- David Besancon – Natixis

- Bogdan Gogu – Morgan Stanley

- Hanita Amin – Morgan Stanley

- Jonathan Aucamp – Exec chairman of OSTC

Some of these directors, as you can see above, are very much connected to the existing and previous mechanisms of the London Gold Market, eg, LPMCL and the old London Gold Fixing.

But apart from ICBC Standard Bank, suspiciously absent from the list of banks cooperating with the LME and World Gold Council are the big guns of the LBMA and LPMCl members, i.e. HSBC, JP Morgan, UBS, Scotia, all of which are big players in the London gold and silver markets and vaulting scenes in London, New York, and in UBS’s case Zurich. As they control LPMCL, perhaps there is no need for them to be involved in a gold and silvers futures sideshow.

Notably, also on 6 July, the LBMA held its Annual General Meeting in London at which the LMPCL member banks maintained their stranglehold on the LBMA Board:

- Peter Drabwell of HSBC was re-elected to the Board

- Sid Tipples, of JP Morgan was re-elected to the Board

- Raj Kumar of ICBC Standard (formerly of Deutsche Bank) was elected to the Board

- Kumar replaces Steven Lowe of Scotia who had been on LBMA board Vice-Chairman

When EOS Precious Metals Ltd was established, it only had 1 A share and 1 B share, both held by WGC (UK) Limited. In the incorporation documents, A shares were defined as having voting rights, an ability to appoint a director and a board observer but no rights to dividends. B shares were defined as having no voting rights but with an entitlement to dividends.

On 26 October, a further 999 A shares and 699 B shares were allotted and said to be paid-up. In the in the allotment filing, these B shares are listed in various tranches i.e. 400 B shares, 100 B Shares, 100 B shares, and 99 B shares, with different total amounts paid for each of these tranches.

In total, there are now 1000 A shares and 700 B shares issued in EOS (with a nominal value of US$ 0.10 each), but there is nothing in the filings listing how many shares of each class are owned by each of the companies and banks that have director representation. Given that there are 6 trading entities as well as the World Gold Council, it could be that each of the 7 entities holds 100 B shares.

There are currently also 10 directors on the EOS board, 2 each from the World Gold Council, SocGen, ICBC Standard, and Morgan Stanley, and 1 each from Goldman Sachs and Natixis. Therefore, its possible that the 1000 A shares could be divided out in the same ratio, 200 for each of the World Gold Council, SocGen, ICBC Standard, and Morgan Stanley, and 100 shares each for Goldman and Natixis.

In a related development, on 23 February 2017 Reuters reported that the LME had agreed a 50-50 revenue sharing agreement with EOS precious Metals under which Morgan Stanley, ICBC Standard, SocGen, Goldman, Natixis and OSTC will attempt to generate trading certain volumes (liquidity) in the LMEprecious gold and silver contracts in return for 50% of the LME’s revenue on the products. The terms of this agreement are not public and it’s unclear if the performance of the banks and OSTC will be measured on customer flow or liquidity guarantees, or perhaps some type of credibility measurement of the contracts in the marketplace.

In early March, Reuters also reported that 3 additional banks and a broker had agreed to come on board with LMEprecious as clearing members, specifically, Commerzbank, Bank of China International, Macquarie Bank, and broker Marex Financial

Most recently, on 6 July, Reuters reported that of these 4 additional participants from the Commerzbank / Bank of China / Macquarie / Marex group, the LME has said that only Marex is ready to participate as a “general clearing member”.

Clearing Unallocated into LPMCL

This brings us to the different types of LME clearing members. Of the 6 participants which came on board to LMEprecious in 2016, 4 of these (SocGen, Goldman, Morgan Stanley and ICBC Standard) are General Clearing Members (GCMs) for LMEprecious. However, Natixis is only an Individual Clearing Member (ICM). Furthermore, OSTC is a Non-Clearing Member (NCM). Marex, as mentioned above, is also a General Clearing Members (GCM). See list of GCMs, ICMs and NCMs for LMEprecious here.

According to LME Clear’s membership rules (Rule 3.1 Membership Categories and Application Process):

a “General Clearing Member" or “GCM", which may clear Transactions or Contracts on its own behalf and in respect of Client Business

an “Individual Clearing Member" or “ICM", which shall be permitted only to clear Transactions or Contracts on its own behalf

On 6 July, Reuters also reported that an algorithmic trading firm called XTX Markets which is based in Mayfair in London, will also start as a Non-Clearing Member (NCM) participant. Obviously, the Non-Clearing Member (NCM) don’t clear trades, instead they use ‘Administrative clearers’ to do their clearing. XTX will use Marex, and OSTC will use SocGen.

As to why Commerzbank, Bank of China International and Macquarie Bank are still not ready to participate is unclear, but this seems odd given that they announced their intent to participate over 4 months ago.

Meet the New Boss, Same as the Old Boss

In Summary:

– there are now 8 bullion banks, a prop trading firm, and a high speed algo firm lined up to help these LME gold and silver futures get out the gate

– these LMEprecious futures will be trading unallocated gold and unallocated silver.

– unallocated gold and unallocated silver is fractionally-backed paper gold and paper silver

– clearing members of LMEprecious require an unallocated precious metal account with an LPMCL member so as to transfer these unallocated gold and silver balances

– the 5 LMPCL banks offering these unallocated accounts are HSBC, JP Morgan, UBS, Scotia and ICBC Standard

– the trading of these LMEprecious futures therefore comes full circle and does nothing to change the structure of the London Gold Market or the London Silver Market

– the World (Paper) Gold Council, which claims to promote gold on the behalf of the gold mining industry, is instead front and center in the promotion of more paper gold trading

With similar recently launched London gold futures from CME Group and ICE not having taken off, all eyes will be on these LMEprecious products to see if they can go where no London gold futures have gone before. Therefore, the LME monthly trading volumes page will be one to watch in future.

Popular Blog Posts by Ronan Manly

How Many Silver Bars Are in the LBMA's London Vaults?

How Many Silver Bars Are in the LBMA's London Vaults?

ECB Gold Stored in 5 Locations, Won't Disclose Gold Bar List

ECB Gold Stored in 5 Locations, Won't Disclose Gold Bar List

German Government Escalates War On Gold

German Government Escalates War On Gold

Polish Central Bank Airlifts 8,000 Gold Bars From London

Polish Central Bank Airlifts 8,000 Gold Bars From London

Quantum Leap as ABN AMRO Questions Gold Price Discovery

Quantum Leap as ABN AMRO Questions Gold Price Discovery

How Militaries Use Gold Coins as Emergency Money

How Militaries Use Gold Coins as Emergency Money

Hungary Announces 10-Fold Jump in Gold Reserves

Hungary Announces 10-Fold Jump in Gold Reserves

Planned in Advance by Central Banks: a 2020 System Reset

Planned in Advance by Central Banks: a 2020 System Reset

China’s Golden Gateway: How the SGE’s Hong Kong Vault will shake up global gold markets

China’s Golden Gateway: How the SGE’s Hong Kong Vault will shake up global gold markets