As I’m mostly occupied researching the Chinese gold market I feel obliged, again, to respond to the latest World Gold Council (WGC) report on China; Understanding China’s Gold Market, published July 2014. For readers of China specials it may appear the WGC is exposing in-depth information on the Chinese gold market, while partially true, all publications contain inaccuracies and inconsistencies and do not disclose the most crucial data that indicates Chinese gold demand is significantly higher than widely assumed. The WGC consciously withholds this data from the mainstream audience - their motives are left for speculation.

Chinese wholesale gold demand in 2013 was 2197 tonnes, though the WGC states consumer demand was 1066 tonnes. Despite several attempts this enormous discrepancy has not been elucidated by the WGC until this day. However, as time goes by and knowledge about the Chinese gold market is slowly spreading through the international gold space, the more pressure is building on WGC demand numbers regarding China.

In this post we’ll analyze and compare the penultimate and last China special, China’s gold market: progress and prospects and Understanding China’s Gold Market, to truly get a better understanding of the Chinese gold market. We’ll begin discussing several quotes from Understanding China’s Gold Market.

Delivery

Whilst China is the simplest gold market on the globe because of the center role of the Shanghai Gold Exchange (SGE), the WGC retains stating the opposite; it’s a very complex market:

In Gold Demand Trends – our quarterly overview of market fundamentals – we publish data for China’s bar and coin and jewelry demand, and in its annual Gold Survey, GFMS, Thomson Reuters publish data on technology demand. Beyond this, the market becomes a little more difficult to piece together. This note, which follows on from our report China’s gold market: progress and prospects, aims to shed light on China’s gold flows and explain how they relate to end-user demand. It is broken down into two sections: the first provides an overview of the supply chain and gold flows, highlighting the complexities surrounding imports, recycling and SGE delivery data. Section two builds on these insights to present a view on China’s aggregate demand.

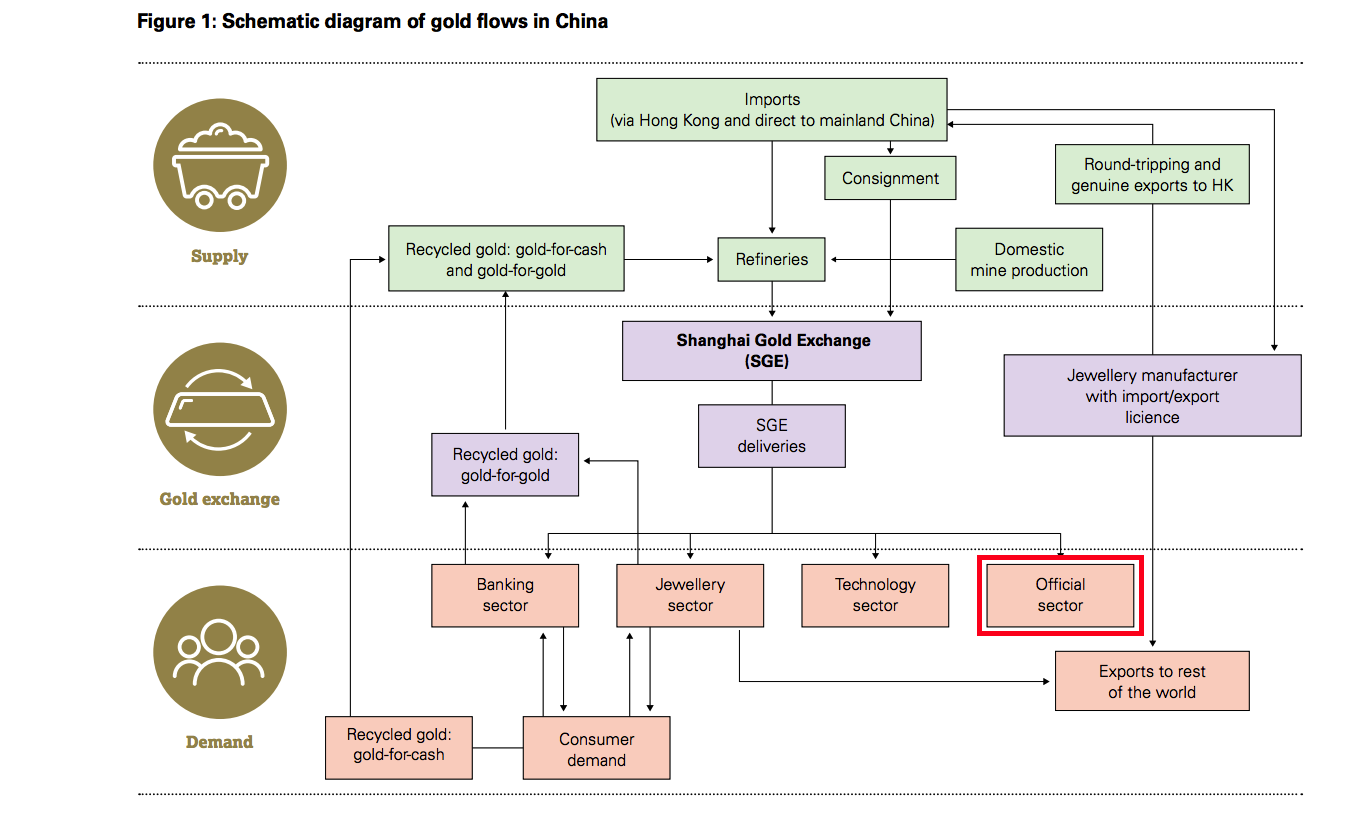

SGE delivery, which should be titled SGE withdrawals but for the sake of simplicity we’ll stick to delivery in this post, is the single most important data point in the Chinese gold market; it’s the key to physical demand, as I‘ve written about frequently. In Understanding China’s Gold Market it seems if the WGC is actually expanding on SGE delivery.

(in the next screen shot from the WGC report the red box is added by me)

But are they really? Including the flow chart SGE delivery is mentioned twelve times in the report, but only one concrete number is disclosed: cumulative SGE delivery from 2009 to 2013 was 5811 tonnes. Instead of giving the exact numbers of SGE delivery for each year and the direct implication of these numbers (delivery equals wholesale demand), they’re only passingly hinting SGE turnover has been large in recent years. Though forced to expand on the structure of this market the WGC withholds a number that would to crush their credibility and is likely too sensitive for the international monetary system; the Chinese people bought 2197 tonnes of physical gold in 2013 (note, 229 tonnes of this was recycled gold, more on that later).

I’ve had email correspondence with the WGC in December 2013 in which they admitted to me not to know where all SGE deliveries end up, as “China will never disclose this information”. One phone call to the SGE explained a lot, "huge amounts of gold are withdrawn from the vaults by (personal) SGE account holders", I was told. Below the surface recent WGC reports on the Chinese gold market are abject apologies for not adjusting previous demand numbers or ways to keep their members ignorant on how much Chinese physical gold demand in reality is. Subsequently the global authority on gold writes reports in the hopes to strengthen their paradigm.

Import

Let’s continue examining more quotes regarding Chinese import:

Trade data: There are two issues which cloud the picture of gold flows into China. The first is that data are limited. Mainland China does not publish its own trade statistics so analysts rely on other sources, such as trade data from the Hong Kong Census and Statistics Department. … Trade data includes gold jewelry, semi-manufactured products, scrap, doré, and concentrates. … So while import data are very useful, they need careful interpretation and should not necessarily be taken at face value.

Chinese gold import is not so hard to grasp as the WGC wants us to believe. Jewelry, scrap and concentrates can be easily filtered out through customs data from Hong Kong and other countries. With some basic research anyone can come up with fair estimates of Chinese net gold import. My estimate, made in March 2014, was 1500 tonnes, measured through SGE deliveries.

CPM Group also makes reasonable estimates on net import; 1410 tonnes for 2013. They even have access to reports of commercial bank imports available from the Shanghai Gold Exchange, one would expect the WGC has the same privileges. From the CPM Gold Yearbook 2014, published in March 2014:

Because official gold customs figures are not being reported, gross imports and exports are deduced from figures reported by China's trading partners to UN Comtrade and GTIS databases. Adjustments were made according to reports of commercial bank imports available from the Shanghai Gold Exchange.

And here comes the punch line: SGE chairman Xu Luode gave us the exact amount of gold import for 2013 at the Fourth Commercial Bank Gold Investment Forum May 15, 2014. He stated it was 1540 tonnes. Why doesn’t the WGC mention this extremely important number in a China special written a month later?

Prior to 2012, when Chinese gold demand hadn’t reached the level of sensitivity it currently is subjected to, the PBOC published SGE Annual Reports and China Gold Market Reports that disclosed gold import. From The China Gold Market Report 2008:

Physical gold withdrawal on Shanghai Gold Exchange (SGE) topped 543.19 tons in the year, including gold imports of 81.44 tons by commercial banks, stock carry-over of 31.661 tons from 2007 and 282.007 tons of gold produced in the year. In theory, the gap of 148.082 tons was filled by recycled gold.

From the SGE Annual Report 2009:

Gold import dropped 43 % to 46.42 tonnes, 35.02 tonnes lower than that of last year.

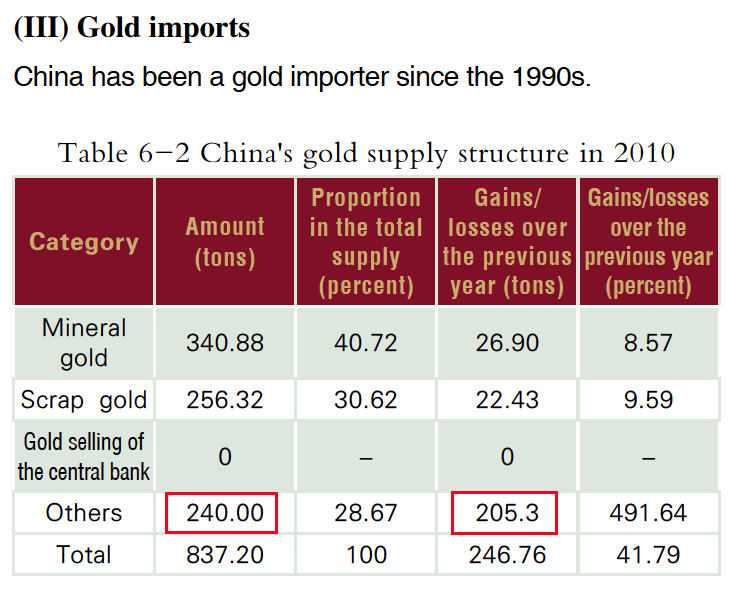

From the China Gold Market Report 2010:

We can see gold import (others) in 2010 was 240 tonnes, up 205.3 tonnes from the previous year.

In Understanding China’s Gold Market the WGC upholds a myth about unknown gold import in 2013. If they would disclose net import, 1540 tonnes, it would be severely in conflict to their consumer demand of 1066 tonnes, especially when adding 428 tonnes of domestic mining supply.

Moving on. From Understanding China’s Gold Market:

As reported in China’s gold market: progress and prospects and in GFMS, Thomson Reuters’ Gold Survey 2014, ‘round-tripping’ may flow through the SGE and could be captured in the Exchange’s delivery figures.

Round tripping does not inflate SGE deliveries! (click this link for a comprehensive analysis of round tripping and Chinese gold trade).Only fifteen banks, blessed with a PBOC general trade license, can import bullion into the domestic gold market which is required to be sold through the SGE. Commercial (state owned) banks are not involved in round tripping seeking cheap funds; banks already have access to the cheapest funds available. Additionally, bullion export from the mainland is prohibited as the WGC itself notes on page 4:

In addition, bullion exports are prohibited.

Round tripping is done by merchants and jewelers that don’t have a PBOC general trade license, but are allowed to import gold into a Free Trade Zone for processing. This processing trade is exempt from a PBOC license because the gold is required to be exported after it’s processed. Gold trade through Free Trade Zones does not intertwine with the domestic gold market and the SGE. The lion share of gold exported from China is processing trade.

Another misconception on page 3:

Importantly, gold which has been withdrawn from the SGE cannot be sold directly back to the Exchange by private investors or non-SGE members – it first needs to be re-cast into a new bar.

SGE members are not allowed to sell gold directly back either, this rule applies for every trader on the exchange. Once bars are withdrawn from the vaults they are not allowed to re-enter.

Scrap

From Understanding China’s Gold Market:

Given the complexity of the market there could be many reasons, but the most likely explanation is that the SGE delivery figure includes the flow of recycled gold-for-gold as well as gold-for-cash. As explained previously, while recycled gold-for gold will increase supply and demand, the net effect is market neutral. For this reason, demand and recycling estimates as reported in Gold Demand Trends and GFMS, Thomson Reuters’ Gold Surveys exclude recycled gold-for-gold. But because the structure of the Chinese gold market requires refined and recast recycled gold to be sold through the SGE, it is likely the delivery figure captures this circulation of recycled gold-for-gold.

First of all, refined and recast recycled gold is not required to be sold through the SGE! The reason a lot of gold is being recycled through the SGE is because gold on the SGE is exempt from VAT, which creates an incentive to sell it through the central bourse. This also explains why SGE delivery (wholesale demand) is so much higher than WGC consumer demand: Every Chinese citizen can open an SGE account through a commercial bank. On the SGE he or she can buy VAT free gold, while some (not all) gold products sold in retail include VAT or profit margins. SGE bars are the cheapest not the prettiest, but how many gold investors would care? While the WGC measures gold sales in retail, SGE delivery captures the true size of demand. Needless to say, all jewelers purchase their gold at the SGE, so SGE delivery includes retail sales.

Above, SGE 100 gram gold bar sold excluding VAT.

In China standard gold are bars of 50g, 100g, 1kg, 3kg and 12.5kg, with a purity of AU9999, AU9995, AU999 and AU995. This is VAT free if traded over the SGE or SHFE, if not traded over the SGE or SHFE standard gold is not VAT-free.

Second, yes, recycled gold-for gold flows through the SGE, we know this since 2008. From the China Gold Market Report 2008:

Gold scrap

At present, gold scrap in China mainly is in two major forms: repurchase of gold bars, only applicable to brand gold bars in reference to real-time gold price, and repurchase of gold jewelry through retailers.

I guess it took the WGC six years to figure this out.

Now scroll up and have another look at the last sentence from the first quote I presented from The China Gold Market Report 2008. “In theory, the gap of 148.082 tons was filled by recycled gold”. Note, The China Gold Market Report 2008 also states withdrawals accounted for 543.19 tonnes, import was 81.44, stock-carry over was 31.661 and domestic mining was 282.007 tonnes. We can clearly read the essence of the structure of the Chinese physical gold market. In a simplified equation:

Import + mine + scrap = SGE delivery

China mined 428 tonnes in 2013, which was required to be sold through the SGE. Net import, also required to be sold through the SGE, was 1540 tonnes. SGE delivery was 2197 tonnes and thus gold recycled through the SGE was 229 tonnes (neglecting stock carry-over). SGE delivery minus recycled gold was 1968 tonnes, which is the amount that was net added to private reserves in 2013.

The Official Sector

In China’s gold market: progress and prospects the WGC stated the glut in gold supply (the discrepancy between SGE delivery and consumer demand) may have been absorbed by the PBOC:

…the large and growing apparent ‘surplus’ in the local market, after taking into account supply, demand and net imports, has been suggested as pointing to unreported accumulation of gold by the state.

…in recent years supply of gold has risen even faster than demand because of a surge in bullion imports. This has fuelled talk of possible Chinese official gold purchases in the domestic market. Indeed, even taking into account very substantial amounts of financial arbitrage, gold exports, stock building and other phenomena, there still remains a large ‘residual surplus’ in the market, which some have interpreted as representing an implied build-up in official sector…

Back in April 2014 I have written it’s very unlikely the PBOC buys gold through the SGE as all gold on the SGE is quoted in renminbi and the PBOC would rather exchange US dollars for gold - likely buying gold overseas. I strengthened my theorem in a post from June 2014 when more pieces of the puzzle came out. In Understanding China’s Gold Market (July) the WGC writes:

China’s authorities have a range of options when purchasing gold. They may acquire some of the gold which flows into China; there has been no shortage of that. But there are reasons why they may prefer to buy gold on international markets: gold sold on the SGE is priced in yuan and prospective buyers – for example, the PBoC with large multi-currency reserves – may rather use US dollars than purchasing domestically-priced gold. The international market would have a lot more liquidity too.

This is exactly what I wrote in my post in April; the PBOC has a strong incentive to exchange some of their supererogatory dollars for gold abroad (not exchange renminbi for gold on the SGE).

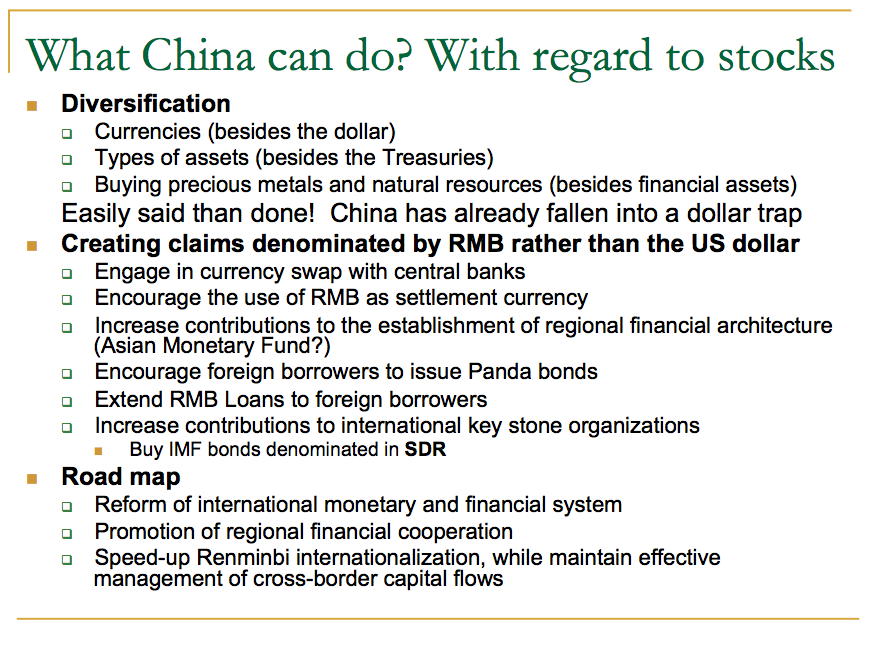

There is another strong indication the PBOC does not buy gold through the SGE. The foreign exchange reserves of the PBOC exceed $4 trillion. This is one of the largest stacks on the planet and it’s estimated two-thirds is denominated in US dollars. Prominent Chinese economist Yu Yongding illustrated the situation in a power point presentation as follows:

China needs to diversify its US dollar holdings and buy precious metals (next to a very interesting list of additional steps of which most are currently being taken). However, given the size of their reserves just a tiny move would greatly affect the market. This is why the PBOC is forced to buy gold in utmost secret, which it is perfectly capable of doing. China’s central bank is not your local pawn shop around the corner, it can easily buy gold anywhere on the globe and ship it home without declaring anything to any customs, that’s why there is no gold analyst that knows the exact amount of Chinese official gold reserves. For this reason I believe everything we see (Hong Kong, UK, Swiss gold exports to the mainland, SGE delivery, etc) is not related to PBOC purchases. The PBOC would never leave a single trace and, therefore, SGE delivery solely relates to non-government demand.

Koos Jansen

PS in future posts I will expand on gold loans/leasing and the VAT structure for precious metals in China mainland.

info@ingoldwetrust.ch

Copyright information: BullionStar permits you to copy and publicize blog posts or quotes and charts from blog posts provided that a link to the blog post's URL or to https://www.bullionstar.com is included in your introduction of the blog post together with the name BullionStar. The link must be taret="_blank" without rel="nofollow". All other rights are reserved. BullionStar reserves the right to withdraw the permission to copy content for any or all websites at any time.

We use cookies to enhance the user experience, analyse traffic and handle essential functionality. By using our website, you accept that cookies are used. Learn more in our Privacy Policy.