Venezuela Says 'Adiós' to Her Gold Reserves

Ronan Manly

Ronan Manly 1 Comments

1 CommentsFive months ago in my article “Venezuela’s Gold Reserves – Part 2: From Repatriation to Reactivation“, I concluded that:

“given the deteriorating state of Venezuela’s international finances and international reserves at the present time, it may be sooner rather than later before Venezuelan gold could be on the move again out of the country.

One thing is for sure. Gold leaving Venezuela on a flight back to London, New York, or elsewhere, will not get the fanfare and celebration that was accompanied by the same gold’s arrival into Caracas a few short years ago.“

Those predictions now seem to have come to pass because there is now evidence that the Banco Central Venezuela (BCV) shipped gold out of Maiquetía Airport (Caracas international Airport) in early July 2015, and there is also separate evidence that Venezuela’s official gold reserve holdings, which are managed by the BCV, dropped by 60 tonnes between March and April 2015. These are two distinct events.

The 60 tonne drop in gold reserves in March-April

On 28 and 29 October respectively, Bloomberg and Reuters filed reports highlighting a decline in Venezuela’s gold reserves through the end of May 2015. The Bloomberg report is here, the Reuters report is here. Both reports merely focused on the currency value of Venezuela’s gold reserves, and neither report addressed the critical metric that is needed in any discussion of central bank physical gold dealings, i.e. quantity or weight of gold. Furthermore, neither Bloomberg nor Reuters seems to grasp how the BCV values its gold reserves.

From Reuters:

“Venezuelan central bank gold holdings declined in value by 19 percent between January and May, according to its financial statements, likely reflecting gold swap operations and lower bullion prices…

..Central bank financial statements posted this week on its website show monetary gold totaled 91.41 billion bolivars in January and 74.14 billion bolivars in May“

From Bloomberg:

“The value of the central bank’s bullion holdings fell 28 percent at the end of May from a year earlier, while the spot price for the metal declined just 12 percent."

The problem with the above is that comparing the change in value of Venezuelan gold reserves over two points in time relative to the spot price change of gold over those same two points in time is not the correct approach because the BCV does not use the latest market price to value its gold holdings. The BCV uses a nine month rolling average valuation price methodology.

Without knowing the correct valuation price used at each month-end valuation point, the quantity of gold being valued cannot be calculated accurately. Conversely, doing some simple research (looking up the footnotes to the BCV accounts) and a few quick spreadsheet calculations gives a very accurate estimate of quantity of gold held at each month-end valuation point. Perhaps next time the major financial news wires can go the extra mile.

[Note: The Spanish translations in this article use a combination of Google Translate and Yandex Translate, and some instinctive re-sequencing.]

Valuation of monetary gold by the BCV

The BCV’s valuation methodology for monetary gold holdings, taken from 2014 year-end accounts, is as follows:

“Oro monetario…se valora mensualmente utilizando el promedio móvil de los nueve (9) últimos meses del fixing a.m. fijado en el mercado de Londres,

“Monetary gold…is valued monthly using the moving(rolling) average of the last nine (9) months of a.m. fixings set in the London market“

Because the BCV holds a small percentage of its monetary gold in the form of gold coins, the valuation methodology also addresses how to value the coins, which, although not material to this discussion, is as follows:

“..más un porcentaje del valor promedio de la prima por el valor numismático que registren las monedas que conforman este activo.”

“..plus a percentage of the average value of the premium for the numismatic value of the coins which comprise this asset"

(Note 3.3. to the 2014 BCV financial accounts)

To check this moving average calculation and how it works, you can apply it to the 2014 year-end monetary gold valuation figure and make use of note 7 in the same set of accounts. Note 7 states:

“Nota 7 – Oro monetario

Al 31 de Diciembre de 2014, las existencias de oro monetario se encuentran contabilizadas a un precio promedio de USD 1.257,80 por onza troy y totalizan Bs. 91.879.349 miles, equivalentes a USD 14.620.691 miles y su composición y valoración se corresponde con los criterios descritos en la nota 3.3”

“At December 31, 2014, the stock of monetary gold is recorded at an average price of USD 1257.80 per troy ounce and total Bs. 91,879,349 thousands, equivalent to USD 14,620,691 thousands, and its composition and valuation corresponds to the criteria described in Note 3.3”

(Note 7 to the 2014 BCV financial accounts)

The Venezuelan accounting convention of USD 14.620.691 miles just means USD 14.6 billion.

361 tonnes of gold at year-end 2014

As at 31 December 2014, in its balance sheet, the BCV valued its monetary gold at Bs 91,879,349,000 (bolívares fuertes). Technically, since 2007, the Venezuelan currency is called the bolívar fuerte (strong bolivar) since at that time the Venezuelan government re-based the previous inflation ravaged bolivar and re-set 1000 old bolivars = 1 ‘strong’ bolivar. The updated name is in retrospect ironic given that the Venezuelan currency is now one of the weakest fiat currencies in the world as the Venezuelan economy begins to experience out-of-control price inflation.

This brings us to the next part of the BCV gold valuation equation. The BCV uses an ‘official’ Venezuelan exchange rate in its financial accounts. This official rate is a static 6.3 bolivars to the US dollar and is based on a February 2013 government edict called “Convenio Cambiario N° 14“.

Again, this exchange rate is another fantasy when compared to the unofficial market exchange rate for the Venezuelan bolivar in terms of the US dollar. This unofficial exchange rate, for example, is currently ~786 according to the Dolartoday website. The bolivar’s unofficial rate versus major currencies will no doubt go even higher in the near future as the currency continues to crumble and potentially goes into hyperinflationary territory.

The final part of the gold valuation equation is the London gold fixing (a.m.~morning) price (more recently LBMA Gold Price), whose daily price dataset can be downloaded here. Note that prior to 20th March 2015, the London gold auction ‘fixed’ price was known as the London gold fixing. Even though the London gold price is now still ‘fixed’ (in more ways than one) during the re-gigged auctions, the LBMA has opted for the less loaded name of the ‘LBMA Gold Price’ auction.

I calculate that the 9 month rolling average of the London morning gold price from 1 April 2014 to 31 December 2014 was USD 1257.49. This is pretty close to the BCV specified value of USD 1257.80 above. The BCV’s extra 31 basis points may reflect the numismatic premium on its gold coin holdings or some other calculation difference.

However, the important point to all of this is that the manual calculation method of arriving at the BCV’s gold valuation price (by calculating the 9 month moving average directly) looks accurate and is in line with the BCV’s number. Based on the BCV’s 31 December 2014 monetary gold value of Bs 91,879,349,000, and the BCV’s USD 1257.80 valuation price, Venezuela held 360.64 tonnes of gold at year-end 2014. This 360.64 tonnes figure is pretty close to the figure reported by the World Gold Council of 361.02 tonnes as at end of fourth quarter 2014 (which itself is not set in stone).

The Sale of 61 tonnes?

The BCV publishes monthly balance sheets (including the monetary gold valuation figure), but currently there is a 4 month lag on date publication, so the latest balance sheet is from May 2015 (the same month-end date that Bloomberg and Reuters referred to above). The monthly balance sheets for January to May 2015 can be downloaded here, here, here, here and here:

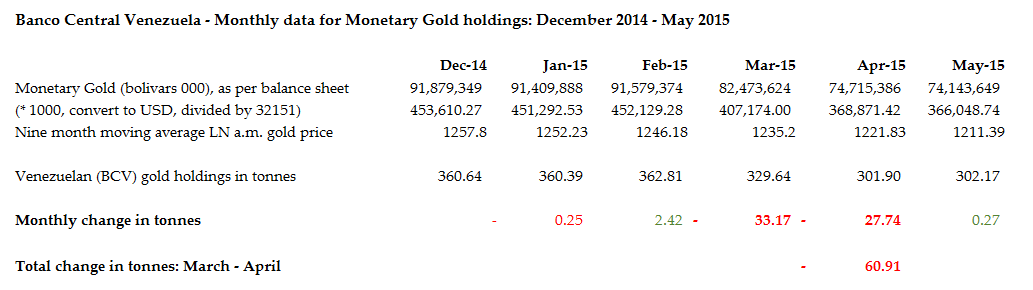

Using the valuation methodology described above, and some simple reverse engineering, shows that over the two month period between the end of February 2015 and the end of April 2015, the BCV’s gold holdings dropped by over 60 tonnes, with a 33 tonne drop in gold reserves during March, followed by a 27.7 tonne drop in April. The data below is taken from the 6 monthly balance sheets from Dec 2014 to May 2015, and the LBMA daily price dataset.

My calculations for month-end January 2015 show Venezuela’s gold holdings to be 360.39 tonnes, nearly identical to the BCV’s month-end version for December 2014. I haven’t included any numismatic premium for gold coin holdings since its immaterial. My calculations show a 2.4 tonne increase in gold holdings at February month-end. I’m not sure what this increase refers to but it could be the monetization of some domestic gold mining production by the BCV (purchasing some Venezuelan mining output and classifying it as monetary gold), or conversion of some small residual BCV non-monetary gold holdings into monetary gold.

Adding domestically produced gold to monetary gold holdings in Venezuela has a precedent. So does conversion of already held non-monetary gold. For example in 2011 the BCV purchased 1.6 tonnes of domestic gold. The same year the BCV also converted 3.6 tonnes of ‘non-currency gold’ that it was already holding into monetary gold. For details, see section “Changes to Venezuela’s gold reserves since early August 2011" in my article “Venezuela’s Gold Reserves – Part 1: El Oro, El BCV, y Los Bancos de Lingotes“.

For March 2015, my calculations indicate that the BCV’s gold holdings witnessed a 33.17 tonne reduction, and ended the month at 329.64 tonnes. Similarly, in April 2015, my calculations find that the BCV gold reserves saw another outflow of 27.74 tonnes, bringing total holdings down to 301.90 tonnes. Between March and April, the combined gold reduction amounts to 60.91 tonnes. There was no material change in gold holdings between April and May, save a tiny 0.27 tonne increase, which could be calculation noise. The main damage to the gold holdings happened in the narrower time period of March and April, a fact that was not highlighted in the Reuters 4 month period reference, and the Bloomberg 1 year period reference.

On its website, the World Gold Council (WGC) publishes a “Quarterly times series on World Official Gold Reserves since 2000" spreadsheet, which is based on data from the “International Monetary Fund’s International Financial Statistics (IFS) and other sources where applicable."

Interestingly, this WGC spreadsheet states that as of the end of Q4 2014, Q1 2015, and Q2 2015, Venezuela’s gold reserves remained unchanged at 361.02 tonnes, and the WGC does not reflect any of the above monthly reductions in Venezuela’s gold holdings. The WGC spreadsheet also states in a disclaimer that “While the accuracy of any information communicated herewith has been checked, neither the World Gold Council nor any of its affiliates can guarantee such accuracy."

This just goes to show the many problems that can arise by relying solely on IMF and WGC data sources for official sovereign gold holdings, in addition to the more problematic ‘gold receivables’ accounting fictions employed by central banks.

BCV operations: First and Second?

To see what was happening with Venezuela’s gold holdings in March and April 2015, it is worth reading the last few sections of my “Venezuela’s Gold Reserves – Part 2: From Repatriation to Reactivation" article, especially the last section about the 5 questions Maria Corina Machado, parliamentarian and opposition party leader in Venezuela, posed to Nelson Merentes, president of the BCV on 12 March 2015.

Also important to know from that article are:

a) the details of the Venezuelan gold swap with Citibank which emerged in late April and was for only 1.4 million ounces (43.5 tonnes post haircut), and the gold to be used in the swap was the 50 tonnes of gold that had been left by the BCV in the Bank of England vaults in January 2012

b) the BCV was in discussions with a number of investment banks about harnessing its gold reserves, and that the BCV revealed on 5 March that six investment banks were making a pitch to the BCV, namely Credit Suisse, Goldman, BTGP Brazilian, Deutsche, Bank of America and Citibank. The favourites were said to be from a short-list of Deutsche Bank, Bank of America and Citibank, but another Caracas media source thought that Credit Suisse and Bank of America were involved

c) Goldman Sachs had previously been discussing a gold swap with the BCV, this news becoming public in November 2013

The 61 tonne reduction in Venezuela’s gold reserves over March-April 2015 cannot be accounted by the Citi gold swap since a) the Citi gold swap was for less than 45 tonnes, b) gold swaps usually stay on central bank balance sheets as an asset of the central bank, and c) if there was a gold swap transaction that did get taken out of the balance sheet, it would not be a reduction over 2 months, it would be one transaction.

Therefore, I think that this 61 tonne reduction over March-April 2015 represents something else entirely. It could be another transaction with one or more of the other investment banks above, or it could be an entirely separate gold sale to another entity such as the Chinese government.

Since Banco Central Venezuela is entirely non-cooperative in answering questions about gold posed by the media, some speculation is, in my opinion, acceptable. For example, for the articles referenced above, Bloomberg states that “The central bank’s press department declined to comment on the decline in gold holdings." Reuters states that “The central bank declined to comment“. Another example of arrogant central bankers who consider themselves above normal standards of accountability and transparency.

A few clues about the gold holdings reduction are in the letter Maria Corina Machado sent to Nelson Merentes on 12 March. In the letter Machado asked these 5 questions of Merentes:

- Are all of Venezuela’s gold reserves in the vaults of the Central Bank of Venezuela as stated by the former president Hugo Chavéz on 17 agusto 2011, when he ordered “repatriation of our gold”?

- Is the BCV in negotiations with foreign banks for the sale or pawning of monetary gold?

- Is it true that in the operation to pawn gold currently under discussion, it is intended to dispose of gold with a market value of US$ 2.6 billion? Does this represent / involve almost 20% of the total gold reserves of the Republic, in this first operation?

- Is it true that they would be negotiating a second operation similar to the previous one for an even greater amount?

- Do these operations involve removing the gold from the vaults of the BCV and returning it abroad?

Machado’s questions are very specific, i.e. US$2.6 billion, almost 20% of gold reserves, first operation, second operation, physical removal of gold, return of gold to abroad etc, and suggest that her questioning was based on sources that appear to have thought that this specific information was indeed factual.

In early March 2015, 20% of Venezuela’s gold reserves of 360 tonnes would be 72 tonnes, (while 61 tonnes would be 17% of gold reserves). Based on an average gold price of $1,200 in the first week of March, US$2.6 billion would be 67.4 tonnes. These figures are far closer to the actual reduction of gold holdings in March and April of 61 tonnes and suggest that there was a ‘first operation’ that was distinct from the gold swap with Citibank, and that necessitated the actual removal of 61 tonnes from the BCV balance sheet.

Then what about a ‘second operation‘ that could be ‘for an even greater amount‘ in the words of Machado?

Gold Flights from Caracas in July 2015

Caracas international Airport, where the flights laden with Venezuela’s repatriated gold arrived at during the period November 2011 to January 2012, is officially known as Simón Bolívar International Airport, but colloquially known as Maiquetía Airport since it’s in an area of Caracas called Maiquetía (the airport is beside the ocean).

On 01 July 2015, Venezuelan news site La Patilla published an article titled “El BCV reexporta para empeñarlo el oro que Chávez repatrió" (BCV re-exported for pledging, the gold that Chavez had repatriated), in which it featured two snippets from a letter written by the Banco Central Venezuela (BCV) to Maiquetia International Airport Air Customs (SENIAT) sometime just before July, probably written in June. SENIAT is the Venezuelan customs and tax authority, officially called Servicio Nacional Integrado de Administración Aduanera y Tributaria, or National Integrated Service for the Administration of Customs Duties and Taxes.

The first snippet of the BCV letter to SENIAT, and highlighted by La Patilla, stated:

“Tengo el agrado de dirigirme a usted en ocasión de manifestarle que el Banco Central de Venezuela realizará exportación de valores, cuyas especificaciones y demás características se detallarán en actas a suscribirse con con funcionarios del Ministerio del Poder Popular de Economía, Finanzas y Banca Pública -Seniat y este instituro, las cuales serán presentadas a las autoridades competentes el día de salida en la Aduana Principal Aérea de Maiquetía“

“I have the pleasure of addressing you on the occasion to inform you that the Central Bank of Venezuela will export values, whose specifications and other characteristics will be detailed in Minutes to be signed with officials from the Ministry of Popular Power for Economy, Finance and Public Bank -Seniat and this Institute, which will be presented to the competent authorities on the day of departure in Maiquetía’s Main Air Customs"

The La Patilla article commented that:

“Los “valores” a los que se refiere la comunicación sería oro monetario según nos respondieron dos economistas con experiencia en las operaciones del BCV."

“According to two economists with experience of BCV operations who responded to us, the ‘values’ to which the communication refers to is monetary gold.“

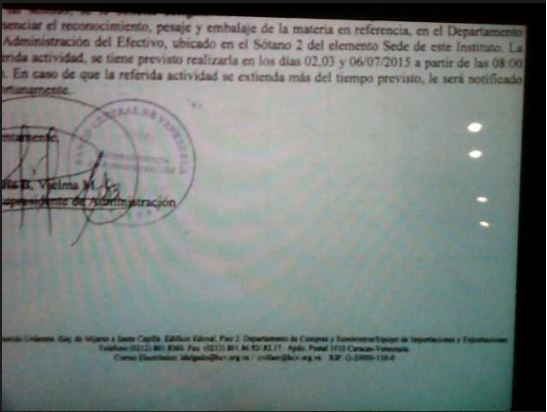

The 2nd snippet of the letter, with the BCV stamp, is even more interesting, and I have included it below:

Although not fully legible on the very left hand side of the photo, the text, as far as I can make out, says:

“…el reconocimiento, pesaje y embalaja de la materia en referencia, en el Departamento de administracion del Efectivo, ubicado en el sótano 2 del elemento Sede de esta instituto. La…[ ]… actividad, se tiene previsto realizarla en los dias 02, 03 y 06/07/2015, a partir de las 8:00…[ ]. En caso de que la referida actividad se extienda más del tiempo prevista, le será notificado…[ ]

“acknowledgement, weighing and packing of the material in question, in the Cash Management Department, located in Basement 2 of the Headquarters of this Institute. The .. [ ].. activity is planned for the days 02, 03 and 07.06.2015, from 8:00…[ ]. In the event that the referred to activity extends beyond the planned time, you will be notified…[ ]"

It’s not unusual for letters about specific gold shipments from central banks to security carriers or other agencies to avoid to mention the actual cargo. I have seen the same approach used in historical Bank of England letters to companies like MAT Transport and the Metropolitan Police, phrases such as “we would like to go ahead with the matter we discussed’, and ‘we have now completed the aforementioned assignment bla bal bla, I trust everything was in order". It’s merely phrased this way for security reasons.

Venezuela is short of hard currency bank notes such as USD and EUR. Venezuela would hardly be flying out hard currency cash. Nor would it be flying out worthless bolivar bank notes. The BCV letter refers to weighing and packing, which can only mean gold bullion.

The letter snippets in this ‘La Patilla’ news article look to be what they purport to be, and they do indeed appear genuine, so there is a high probability that the BCV was flying out cargos of monetary gold from Caracas International Airport on 2nd July (Thursday), 3rd July (Friday) and 7th July 2015 (Tuesday), and maybe after 7th July if the operation needed extended time as the contingency in the letter planned for.

When the last flight of repatriated gold flew into Caracas from Eorope on 30 January 2012, it was carrying 14 tonnes of gold in 28 crates. Based on this metric, 3 flights going out from Caracas in early July 2015 could carry 42 tonnes of gold, if not more. Therefore there is a realistic upper bound of at least 42 tonnes to the amount of gold that the BCV could have been flying out of Maiquetía airport on 2nd, 3rd and 7th July 2015.

This article has focused on two sets of events, 1) the drop in Venezuela’s monetary gold reserve holdings in March and April 2015 which looks to be distinct from the Bank of England vaulted gold used in the BCV-Citibank gold swap, and 2) a series of cargo flights of what looks like BCV monetary gold being flown out of Caracas International Airport in early July 2015.

Venezuela’s international reserves, managed by the BCV, are now down to USD 15.120 billion as at 29th October 2015, from USD 16.4 billion at the end of September 2015. Investment bank reports and the financial media are abuzz with speculation that (to paraphrase) “Venezuela will need to use its gold reserves to raise international funds for imports etc etc“. Which is no doubt true, but what the analyst reports and media reports are missing, in my opinion, is that a good chunk of Venezuela’s gold reserves are already in play and that any new repos, swaps or sales will have to line up and utilise whatever Venezuelan gold reserves are not already under lien, claim, encumbrance or collateralisation.

In the second half of October, Barclays’ two New York based Latin American economists, the two Alejandros (Arreaza and Grisanti) said that:

“Our quarterly cash flow model suggests that Venezuela will have a deficit of approximately USD10bn just during this quarter and will have to finance almost all of it with its own assets. Currently, liquid international reserves are likely less than USD0.5bn. The rest of the reserves are gold, SDRs and the position at the IMF. Therefore, assets besides reserves will need to be used.

We estimate that disposable assets (in and out of reserves) are about USD15.1bn. Assuming a gold repo of USD3.0bn before year-end, the disposable assets could end the year at about USD8.0bn. With these assets and a possible additional use of gold reserves, we expect Venezuela to meet its debt obligations at least until Q1 16"

Which is all very fine, except the fact that if the BCV gold reserves are 61 tonnes lighter due to outflows in March and April, and if there were additional gold outflows via international cargo flights in July, which looks likely, then a further USD 3 billion repo (circa 80 tonnes without deep haircut) will have to use additional BCV vaulted gold, a lot of which is in US Assay Office melt bars, which are not necessarily up to the expected quality of modern-day Good Delivery bars.

From my Part 1 article, I had calculated that “there were 12,357 bars held in the BCV vaults in Caracas before the gold repatriation started, and 25,176 bars in the BCV vaults when the repatriation completed“, since “12,819 good delivery bars" (160 tonnes) were repatriated. About 4,089 bars were left in London in 2012. The bars that were originally in Caracas are mainly if not exclusively US Assay office bars.

If the Caracas vaulted gold is being sold by Venezuela in the international market, it most likely would be of current Good Delivery standard (not US Assay office bars). With 160 tonnes of repatriated Good Delivery bars in 2011-2012, then if 61 tonnes was sold in March-April, and various flights happened in July 2015, there may not be enough modern Good Delivery bars remaining in Caracas to satisfy an additional USD 3 billion transaction.

In my Part 2 article in May, I had said:

“Venezuela (via the BCV) will put up 1.4 million ozs of gold as collateral in exchange for a $1 billion loan of foreign currency from Citibank. Since 1.4 million ozs of gold, valued at the late April 2015 price of $1,200, is roughly $1.68 billion, then Venezuela is having to accept a near 40% discount on the specified gold collateral.“

Note that 1.4 million ounces is about 43.5 tonnes.

Interestingly, Barclays analysts Feifei Li and Dane Davis in their ‘Metals Markets Outlook’ piece from 26 October 2015 (last week) titled ‘Mixed Messages’ reiterated the above view and said:

“Earlier this year Venezuela executed a gold swap to raise $1bn. About 45 tonnes of gold was committed, indicating a haircut of around 40% for gold prices at the time. If we apply a similar haircut to the current gold price, it would imply that close to 140 tonnes of gold would be needed for $3bn. Thus if $3bn extra gold swaps were executed, half of Venezuela’s 361 tonne gold reserve would have been utilised."

But 140 tonnes of gold will bring into play a lot of Venezuela’s US Assay Office bars, given that some other counterparties have already raided the Caracas vaults to get the best bars. While a lot of Venezuela’s US Assay office bars probably contain the fine gold count that they claim to hold, some probably don’t, as was illustrated in the sardonic yet jovial Zerohedge article “No Indication Should, Of Course, Be Given To The Bundesbank…" published back in September 2012.

So its buyer beware time for the counterparties that are now queued up to get their hands on Venezuela’s last remaining ingots of gold, before the entire Caracas stash may well get looted.

Popular Blog Posts by Ronan Manly

How Many Silver Bars Are in the LBMA's London Vaults?

How Many Silver Bars Are in the LBMA's London Vaults?

ECB Gold Stored in 5 Locations, Won't Disclose Gold Bar List

ECB Gold Stored in 5 Locations, Won't Disclose Gold Bar List

German Government Escalates War On Gold

German Government Escalates War On Gold

Polish Central Bank Airlifts 8,000 Gold Bars From London

Polish Central Bank Airlifts 8,000 Gold Bars From London

Quantum Leap as ABN AMRO Questions Gold Price Discovery

Quantum Leap as ABN AMRO Questions Gold Price Discovery

How Militaries Use Gold Coins as Emergency Money

How Militaries Use Gold Coins as Emergency Money

Hungary Announces 10-Fold Jump in Gold Reserves

Hungary Announces 10-Fold Jump in Gold Reserves

Planned in Advance by Central Banks: a 2020 System Reset

Planned in Advance by Central Banks: a 2020 System Reset

Surging Silver Demand to Intensify Structural Deficit

Surging Silver Demand to Intensify Structural Deficit